Dumplings and Broth: Reflecting on VB Insights and Healthcare IT in 2017 – A 2018 Lunar New Year Special

Before drafting this article, I have been reflecting on what I truly wish to convey. Ten years is a period that feels both long and short. In the traditional healthcare industry, ten years merely spans the cycle from drug research and development to market launch. However, for healthcare informatics, ten years is akin to crossing an entire century. The emergence of any disruptive technology has the potential to alter its evolutionary trajectory.

Throughout 2017, I authored a total of 205 articles on the healthcare informatics industry, amounting to approximately 610,000 Chinese characters. These pieces included industry reports, in-depth analyses, industry roundups, and news briefs. Of course, this classification is based solely on article categories, which may appear somewhat rigid.

Throughout my industry observations, each of my articles and updates has played a distinct role. Rather than being isolated, they are interconnected and mutually corroborative. After careful consideration, I have decided to structure my writing around three perspectives: “What I Have Seen,” “What I Have Heard,” and “What I Have Thought.”

A brief disclaimer: This article is by no means a roundup or in-depth analysis, nor is it a mere compilation of events. Rather, it reflects my personal insights into the health IT industry over the past year. Since it’s the Lunar New Year season, let’s dial down the usual seriousness and keep things light.

What I See

The image above shows my flight route map for the past year, which is hardly worth mentioning compared to those of many journalists or founders. However, I find it quite interesting and thus worth sharing.

In 2017, the cities I visited for conferences (excluding trips by bullet train or high-speed rail) were: Hangzhou (4 times), Beijing (3 times), Guangzhou (2 times), Shanghai (1 time), Tianjin (1 time), Shenzhen (1 time), Hohhot (1 time), Xi’an (1 time), Wenzhou (1 time), Wuxi (1 time), and Wuhan (1 time). The vast majority of these visits were at the invitation of healthcare IT companies, with a small portion attending events in other fields.

Below, I will share my thoughts on a few selected cities:

First, Hangzhou. What impressed me most was a family doctor contract signing training session led by the Department of Primary Health Care of the National Health and Family Planning Commission in August. At that meeting, several directors from Hangzhou Third People’s Hospital and the Zhanongkou Street Community Health Service Center in Jianggan District shared their experiences and achievements in contract signing.

After the speech, a large crowd of community health center staff, directors, and even reporters surrounded Fan Minhua (Director of the Kaixuan Subdistrict Community Health Center in Jianggan District, Hangzhou), asking her how to properly implement contract-based services. Despite her slim build—standing under 1.7 meters tall and weighing only 55 kilograms—it took tremendous effort for me to squeeze into the circle.

My biggest takeaway from that experience was that family doctor contracting has truly become the central focus of community health centers across China. Professionals within the healthcare system are paying close attention to it, discussing it, researching it, and putting it into practice. However, many regions still lack a clear methodological framework to support these efforts, making it difficult for the general public to perceive the presence of family doctors.

In such a promising market, there are abundant opportunities for healthcare informatization. Many IT companies I am aware of, including publicly listed ones, are ramping up their efforts in this sector.

The second city to discuss is Beijing. Apart from leaving a deep impression with the VCBeat Future Healthcare 100 (no advertising intended), the most notable entities are Tencent and Ant Financial.

Why is mobile payment so ubiquitous in China? Because they are truly relentless. Throughout 2017, for Tencent and Ant Financial, it was akin to a campaign of storming cities and capturing strongholds, as they partnered with one city after another (although I have not visited most of them). Even in the healthcare sector, which is not known for its rapid pace of development, both companies demonstrated the fast-paced DNA characteristic of internet giants.

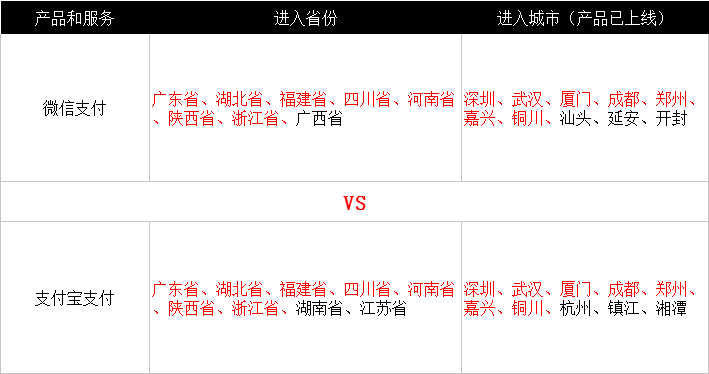

The two figures below present information confirmed with two companies during the inventory review conducted in December 2017, covering both market and capability dimensions (note that these data may have changed since then and are provided for reference only):

Markets Already Launched

(Red indicates shared)

(Data source: Public information from Tencent and Ant Financial; as of November 2017)

Market data reveals a high degree of overlap between the two parties in terms of provinces and cities where their solutions have been implemented, with overall progress being virtually neck and neck.

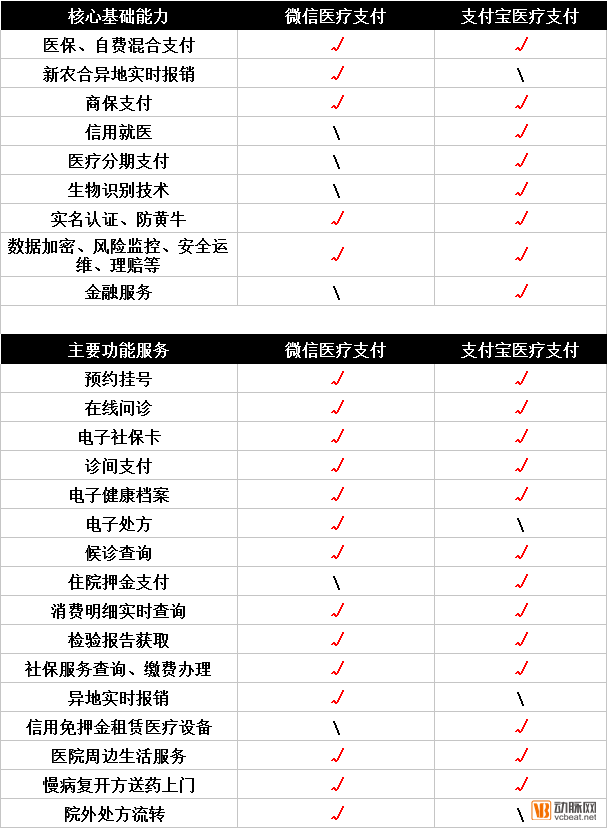

Comparison of Capabilities and Functions

(Check “√” for Yes, “\” for No)

A comparison of their core capabilities and primary functional services reveals that Alipay holds a slight edge in core capabilities, while WeChat has a slight advantage in features and services. Overall, the two are evenly matched.

Beyond the first-tier cities of Hangzhou and Beijing, Wuxi is another place that has left a deep impression on me. It is a city known as the “Birthplace of China’s Internet of Things.”

Since Premier Wen Jiabao proposed the establishment of a “Sensing China” center in Wuxi in August 2009, the Internet of Things (IoT) has taken deep root in the city.

If you drive through Wuxi, the most common words you’ll see on building signs and lightbox advertisements along the way are “Internet of Things” and “sensing.” Since 2016, the World Internet of Things Exposition has been held for two consecutive years, becoming a renowned hallmark of the city. Ask any local resident on the street, and they can readily share a few thoughts on the term “Internet of Things.”

The 2017 Internet of Things (IoT) Conference was a real eye-opener for me. There, I had my first “close encounter” with leading figures in the medical IoT sector, including SiChuang YiHui, H3C, AstraZeneca, ShiLing Technology, and DaoYiXun. After returning to Chongqing, I wrote a feature article on each of them and established long-term “♂” relationships.

Overall, the medical IoT industry was somewhat quiet in 2017. However, the situation is likely to change in 2018 as 5G arrives. (Further reading:The Arrival of 5G: What Changes Will It Bring to Healthcare? How Can Medical IoT Companies Strengthen Ties with Telecom Operators?)

What I Heard

“Qilin Block, C12-4, Chongqing Liangjiang New Area Innovation and Entrepreneurship Building” is not only the headquarters of VCBeat but also one of the primary mailing addresses for my colleagues and me.

As a media outlet deeply rooted in western China, VCBeat is far removed from Beijing, Shanghai, and Guangzhou—hubs that churn out new topics and generate fresh buzz daily. Yet this has not dampened our enthusiasm; we remain fully dedicated to journalism and content creation.

Without the hustle and bustle, WeChat, QQ, and phone calls enable us to access information across all areas of healthcare regardless of time or space (which is the same concept as telemedicine). The majority of journalists’ interviews are also conducted via mobile phones.

A special “thank you” to iFLYTEK Hear.

Based on an estimate of 100 interviews, its speech-to-text function saved me at least 200 hours in 2017. Even though it was pricey, my efficiency-driven boss was still willing to pay for it (see, good technology always finds a monetization model).

Throughout 2017, the keyword I heard most frequently in interviews regarding digitalization was “cloud,” with numerous public cloud companies securing substantial financing.

In June 2017, QingCloud secured RMB 1.08 billion in Series D financing; in December 2017, Kingsoft Cloud announced the completion of its USD 300 million Series D financing, among others.

Zhang Shu, an analyst at IDC China, noted last year: “The rapid growth of China’s public cloud IaaS market has been driven by the swift upgrading of infrastructure by enterprise users amid the wave of digital transformation. As provincial and municipal governments roll out specific action plans in response to national cloud computing policies and advance related demonstration projects, the industrial demonstration effect will further accelerate the development of China’s public cloud market.”

Mr. Zhang’s assessment of the macro environment is accurate, but the healthcare sector is evidently far more challenging to navigate than the government affairs sector.

China’s medical resources are unevenly distributed, with low utilization rates and the presence of resource silos. The only way to optimize resource allocation is to achieve “regional collaborative healthcare,” for which cloud infrastructure serves as the most fundamental informational safeguard. From both technical and commercial perspectives, the cloud service model is the optimal platform for supporting the healthcare informatization industry.

In which medical scenarios are public clouds poised to stand out? Through interviews, several professionals revealed to me the following promising directions:

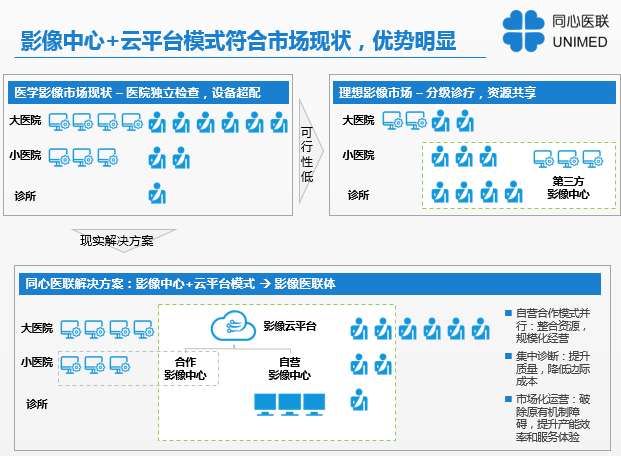

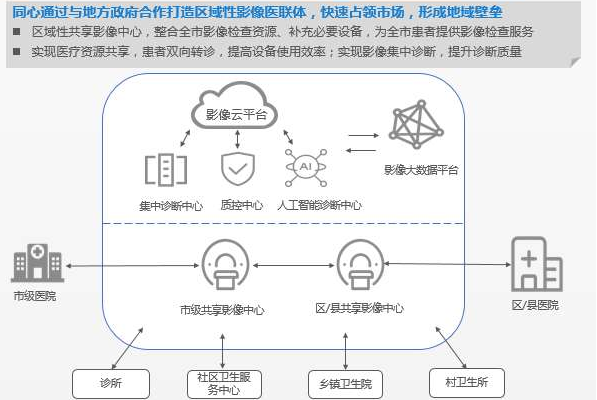

First is the Imaging Cloud. The two figures below illustrate an imaging medical consortium built by Tongxin Medical Alliance, a company that leverages the “imaging center + cloud platform” model in alignment with China’s tiered diagnosis and treatment policy and the principles of the sharing economy:

Primary healthcare institutions, constrained by physicians’ limited diagnostic capabilities and low patient volumes, prioritize patient retention to build a stable patient base as their core objective; collaborating with tertiary hospitals represents an effective pathway to achieve this. Mid-tier hospitals, facing low patient volumes, suboptimal utilization of medical equipment, and inadequate operational capabilities, seek to enhance patient referral flows and service delivery through third-party managed services.

The siphon effect of large hospitals has led to patient volumes exceeding capacity. Meanwhile, certain personalized needs of clinicians are not being adequately met. The involvement of third-party enterprises in providing service support offers hope for changing this status quo, with Tongxin Medical Alliance being one such company.

Another scenario is gene sequencing.

Currently, the turnaround time and analytical speed of gene sequencing are significant bottlenecks. Deploying large-scale distributed computing clusters on-premises imposes excessive pressure on gene sequencing companies, with prohibitive costs rendering them unaffordable for many enterprises.

The annual sequencing data volume of domestic gene companies has reached tens of petabytes (PB). This massive amount of data places severe strain on corporate data centers. Companies are forced to continuously increase investment and expand storage capacity, resulting in persistently high costs.

To address the challenges of gene sequencing, domestic public cloud providers such as Alibaba Cloud have launched data processing services. These public cloud providers typically charge genomics companies a fee, yet their pricing remains significantly more cost-effective than building in-house infrastructure.

Besides medical cloud, another interesting topic in 2017 was blockchain.

Last year, blockchain was the subject of intense speculation, but not for positive reasons. In September, seven government agencies—including the People’s Bank of China, the Cyberspace Administration of China, the Ministry of Industry and Information Technology, the State Administration for Industry and Commerce, the China Banking Regulatory Commission, the China Securities Regulatory Commission, and the China Insurance Regulatory Commission—jointly intervened to officially ban initial coin offerings (ICOs).

Following that incident, Sheng Songcheng, Counselor to the People’s Bank of China and Executive Vice President of the China Europe International Financial Institute at Lujiazui, stated to the media: “A large number of projects with no prospects, or even outright fraudulent schemes, not only expose investors to significant risks but also draw considerable complaints from genuine blockchain startup teams. This has effectively resulted in the adverse consequence of bad money driving out good. Nevertheless, China should continue to encourage blockchain technology.”

At the time, I consulted a practitioner in the medical blockchain sector (when companies specializing in medical blockchain were still few and far between). He told me, “The ICO incident had no impact on us, as we did not conduct public initial coin offerings. This has allowed everyone to focus with greater confidence on applying blockchain technology.”

As recently as January this year, Borderless Intelligence, a medical blockchain company I covered, secured tens of millions of RMB in Pre-A financing from Fosun Tonghao. This is undoubtedly encouraging news for the development of blockchain in healthcare. It is no exaggeration to predict that many blockchain companies will secure funding in 2018.

The peer-to-peer (P2P) nature of blockchain makes it a double-edged sword. The choice between its positive and negative implications ultimately rests with the users of the technology.

What I Have in Mind

I have categorized the key terms of healthcare informatization in 2017 into two types: one is technology-oriented, and the other is mechanism-oriented. The technology-oriented category includes artificial intelligence, blockchain, cloud computing, big data, and the Internet of Things (IoT); the mechanism-oriented category includes medical consortia, family doctor services, Diagnosis-Related Groups (DRGs), and cross-regional medical expense settlement.

From the perspective of public perception, cross-regional medical expense settlement, big data, the Internet of Things (IoT), and artificial intelligence are inevitably ranked among the top.

Healthcare informatics is an industry characterized by the coexistence of the slow pace of healthcare system reform and the rapid advancement of new technologies. Through the dynamic interplay between these two contrasting forces, it continuously grows, evolves, and enhances efficiency.

Practicing in such an industry hones not only one’s professional expertise but also one’s character and mindset.

As one of the observers in the field of healthcare informatization, I should also possess both fast and slow thinking. When it comes to grasping new technology trends, one needs to be sensitive (fast), while in implementing these new technologies, patience and tolerance are essential (slow).

The following “betting agreement” was the 2018 weight-loss plan of a promising heartthrob weighing over 200 jin at VCBeat. I won’t name names (sorry, I couldn’t resist exposing him; if you’ve got a problem with that, come and try to stop me...).

In 2018, I will also strive to become a better version of myself, just like that colleague, in every aspect...