2017 In Vitro Diagnostics Data Report: Over RMB 5.03 Billion in Financing, Molecular Diagnostics Companies Gain Strongest Investor Favor

In early 2017, in vitro diagnostic (IVD) instruments were officially included in the “Guidance Catalog of Key Products and Services for Strategic Emerging Industries (2016 Edition)” issued by the National Development and Reform Commission. In 2017 alone, there were as many as 42 national-level policies related to IVD. Why has policy attention toward the IVD industry increased significantly in recent years? With total financing in the IVD sector exceeding RMB 5.03 billion in 2017, why has capital shown such strong preference for this industry? How has the IVD industry developed in recent years? To gain insight into the development status of the IVD industry, VCBeat has conducted a comprehensive, multi-dimensional analysis of the sector.

This report will address this issue from the following aspects:

(1) How do policy, macroeconomic conditions, and social development exert a trend-driven impetus on the growth of the in vitro diagnostics industry?

(2) What is the industrial distribution, technological breakthroughs, and market size of the in vitro diagnostics industry?

(3) How is capital positioned within the in vitro diagnostics industry?

These questions will be addressed individually in the report. Below are excerpts from the report.

174 National Policies Comprehensively Promote Industry Development

In the four years following 2008, the number of national-level policies issued for in vitro diagnostics (IVD) remained at a low level, indicating insufficient national attention to this field at that time. After 2012, the volume of relevant policy releases increased significantly and maintained a high level of activity. In 2017, the number of national-level IVD policies reached a peak of 42, demonstrating a rapid rise in policy emphasis on the IVD sector.

On October 10, 2010, the State Council issued the Decision on Accelerating the Cultivation and Development of Strategic Emerging Industries, designating the bio-industry as one of the seven strategic emerging industries. It emphasized the need to vigorously develop major innovative drug categories, including biotechnological drugs, novel vaccines and diagnostic reagents, chemical drugs, and modern traditional Chinese medicines for the prevention and treatment of major diseases, thereby enhancing the level of the biopharmaceutical industry. On the 21st, the Ministry of Science and Technology released the Application Guidelines for Major Projects in In Vitro Diagnostic Technology and Product Development under the National High-Tech R&D Program (863 Program) in the Fields of Biology and Medicine. This initiative established a major project focused on “In Vitro Diagnostic Technology and Product Development,” aiming to achieve breakthroughs in key technologies for in vitro diagnostic instruments, equipment, and reagents, and to develop a series of innovative products with independent intellectual property rights and high-quality products with international competitiveness.

In January 2017, the National Development and Reform Commission (NDRC) issued the “Guidance Catalogue of Key Products and Services for Strategic Emerging Industries (2016 Edition),” which formally included in vitro diagnostic (IVD) instruments. Specifically, this encompasses “high-precision, high-throughput (rapid), fully automated analytical instruments for biochemistry, electrolytes, blood gases, urine, body fluids, feces, vaginal secretions, hemoglobin, glycated hemoglobin, specific proteins, blood cells, microbiology, metabolism, nutrition, coagulation, etc. (including dry chemistry systems), as well as their associated disease diagnosis and screening information systems.”

Key Policy Overview

The Demand for In Vitro Diagnostic Services Continues to Increase

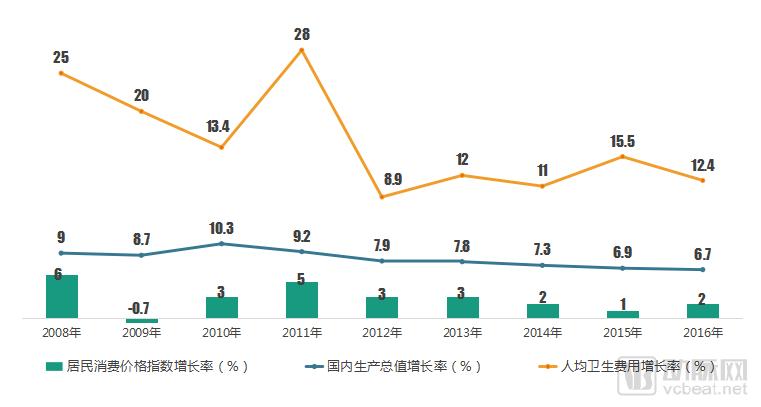

From the perspective of the growth rate of per capita health expenditure among residents, the growth rate of per capita health expenditure is significantly higher than both the gross domestic product (GDP) growth rate and the consumer price index (CPI) growth rate. This indicates that the proportion of healthcare consumption within the national economic structure has been increasing year by year.

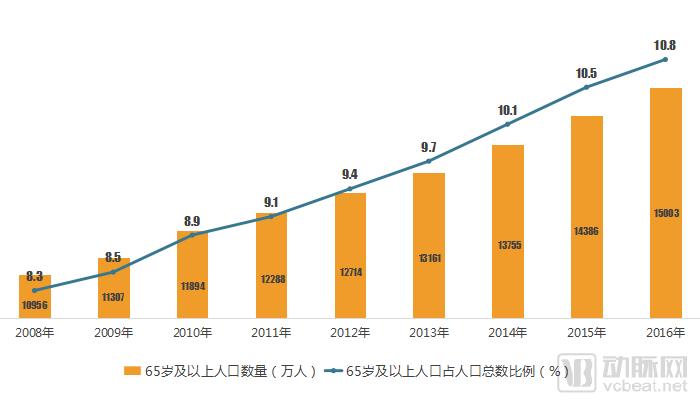

China’s population aging issue is becoming increasingly severe, with the proportion of individuals aged 65 and above rising from 8.3% in 2008 to 10.8% in 2016. Old age is a period characterized by a high prevalence of chronic diseases, many of which require in vitro diagnostic (IVD) products for diagnosis, thereby objectively driving up the demand for IVD products.

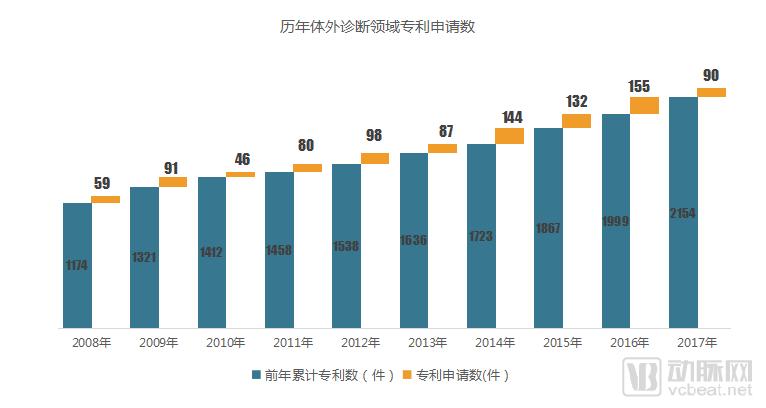

2,244 Cumulative Patent Applications: Continuous Technological Breakthroughs in the In Vitro Diagnostics Industry

Since 2008, the number of patent applications in China’s in vitro diagnostics (IVD) field has shown a rapid growth trend. By 2017, the cumulative number of IVD-related patent applications had exceeded 2,244. Continuous technological breakthroughs have laid the foundation for the development of the IVD industry.

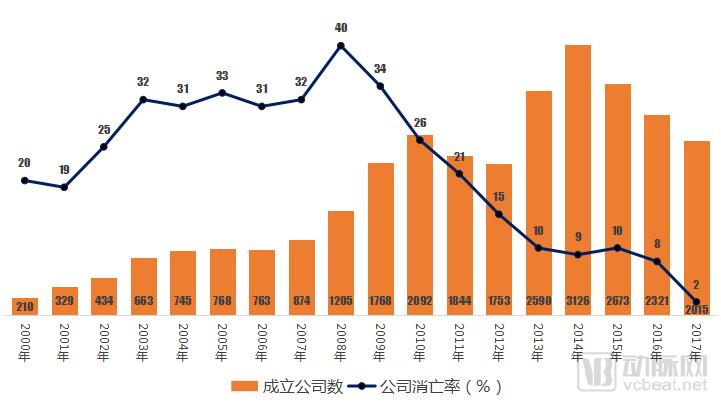

2% Company Attrition Rate: Industry Enters Maturity Stage

From 2000 to 2008, the number of in vitro diagnostic (IVD) companies established was relatively low, and the company failure rate was high, indicating that the industry was in its early stages of development.

Between 2009 and 2014, the number of in vitro diagnostic (IVD) companies established experienced explosive growth, while their survival rate increased significantly, marking the entry of the IVD industry into a period of rapid development.

Since 2015, the number of newly established in vitro diagnostic (IVD) companies has declined year by year, while the survival rate of these companies has further improved. This trend is attributed to the industry’s maturation, the establishment of mature business models, and the emergence of industry giants, which have raised the barriers to entry for new enterprises.

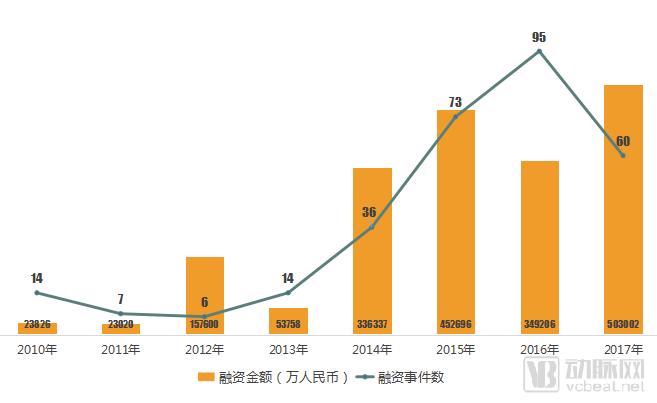

Number of Financing Events Declines, While Total Financing Amount Surges

In 2017, there were 60 financing events in the in vitro diagnostics (IVD) industry, a 37% decrease from 2016, with total funding amounting to RMB 5.03 billion, a 44% increase from 2016.

Since 2014, the financing scale in the in vitro diagnostics (IVD) industry has seen significant growth. However, the average amount per financing round gradually decreased between 2014 and 2016, a trend driven by the continuous entry of new projects. In 2017, the average financing amount per round rose sharply, reflecting the maturation of early-stage projects.

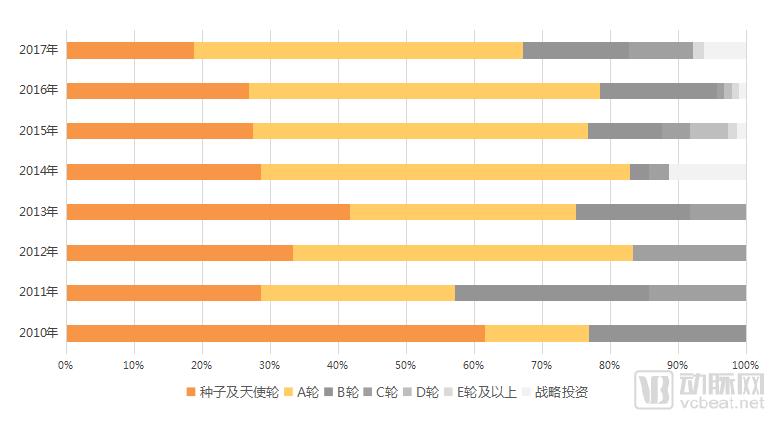

Financing Shifts Toward Maturity

From the perspective of the historical structure of financing rounds, the distribution of financing rounds in the in vitro diagnostics (IVD) industry in 2017 was more balanced compared to previous years, with a shift toward later-stage investments.

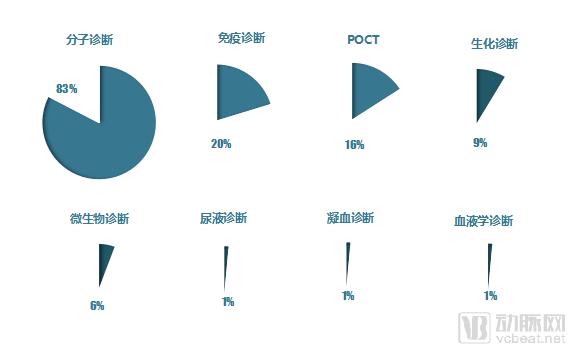

Molecular Diagnostics Companies Are Most Favored

In 2017, the companies in the in vitro diagnostics (IVD) industry that received investment were primarily molecular diagnostics companies, immunoassay diagnostics companies, point-of-care testing (POCT) companies, and clinical chemistry diagnostics companies. Among them, molecular diagnostics companies accounted for 83% of the invested companies.

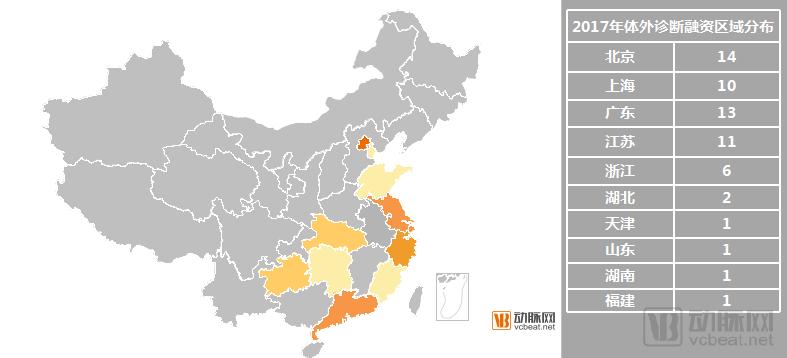

Vibrant Financing Activity in Economically Developed Regions

From financingIn terms of geographic distribution, Beijing, Shanghai, Guangdong, Jiangsu, and Zhejiang recorded higher levels of activity; in 2017, these five regions accounted for 87.5% of the total number of financing events.

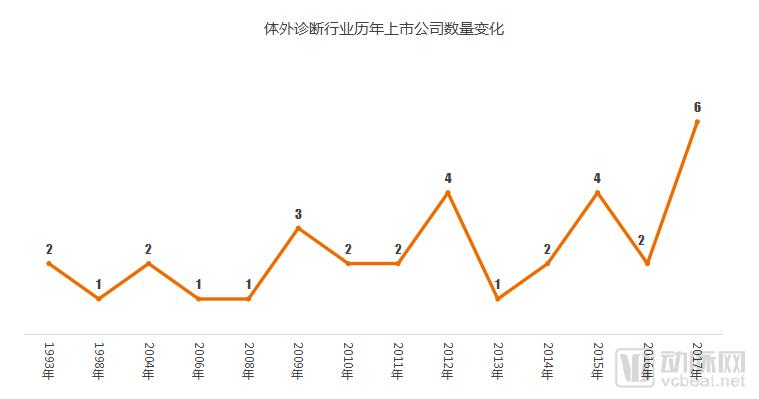

Surging IPO Enthusiasm in the In Vitro Diagnostics Sector

Public listings of companies in the in vitro diagnostics (IVD) industry began in 1993. By the end of 2017, the cumulative number of listed companies had reached 33, with six new listings that year, accounting for 18% of the total number of listed companies in the IVD industry.

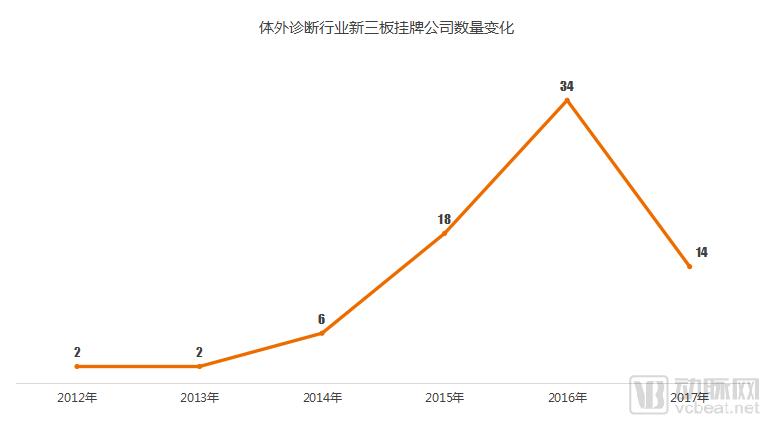

Significant Cooling in IVD Companies’ Listings on the NEEQ

From 2012 to 2014, the number of in vitro diagnostic (IVD) companies listed on the National Equities Exchange and Quotations (NEEQ) was relatively low. However, with the recovery of the equity trading market in 2015 and continuous policy support for the NEEQ, the number of IVD companies listed on the NEEQ surged significantly during 2015 and 2016. In 2017, as the listing thresholds for the NEEQ were raised, the number of IVD companies listed on the NEEQ declined to 14.。

12 M&A Deals, with Transaction Value Reaching RMB 8.23 Billion

In 2017, a total of 12 mergers and acquisitions (M&A) transactions occurred in the in vitro diagnostics (IVD) sector, with a total transaction value of RMB 8.23 billion. Notably, 75% of these M&A deals exceeded RMB 100 million each. It is worth mentioning that Jinyu Checheng invested RMB 1.32 billion to enter the IVD field.

This report, totaling 65 pages, covers policy landscape, macroeconomic factors, industrial distribution, technological breakthroughs, market size, capital allocation, and the VB Quadrant analysis for in vitro diagnostics.analysis, and more. To access additional content, please scan the QR code below to become an official VCBeat member and obtain the full version of the "2017 In Vitro Diagnostics Data Report."

(Scan the QR code to purchase a membership)