China's Medical Device Industry in 2017: Entering a Golden Era, More Thrilling Than Imagined

2017 was a remarkable year for China’s medical device industry! It saw the publication of the industry’s first blue book, the “China Medical Device Industry Development Report (2017).” That year, 13 companies successfully went public, with prominent players emerging across various subsectors, signaling the rise of future market leaders.

We are both grateful and honored to document the development of this industry as a media outlet. In 2017, VCBeat published 149 articles related to the medical device industry and conducted exclusive interviews with more than 20 experts, entrepreneurs, and investors in the field. Through their real-world case studies, they have demonstrated that innovation will become the primary driver of rapid growth in the future medical device market, and that China’s medical device innovation has entered its “golden decade.”

We have found that, with the penetration of new technologies such as artificial intelligence, big data, and the Internet of Things, innovation in China’s medical device industry is primarily reflected in technological and business model innovations, most notably in segmented fields such as in vitro diagnostics, imaging equipment, and smart hardware.

Policy: Fully Encourage Innovation and Achieve Import Substitution at the Earliest Opportunity

2017 was a year of rapid updates to medical device regulations. During this period, the China Food and Drug Administration (CFDA) and the Center for Medical Device Evaluation (CMDE) issued a substantial number of new regulations and guidelines covering multiple areas, including expedited approval processes, encouragement of medical device innovation, improvement of registration procedures, strengthened clinical trial management, and enhancement of technical capabilities.

Overall, the state has primarily focused on regulation and innovation to encourage the localization of medical devices and achieve standardized development.

In terms of regulation, regulatory authorities have continuously issued new regulations aimed at establishing a sound medical device regulatory framework, eliminating non-compliant enterprises and low-quality medical devices, ensuring the high quality and safety of medical devices in China. Industry concentration continues to rise, with a positive long-term trend.

The main new regulations related to regulatory affairs in 2017 are as follows:

● Amendment to the Administrative Measures for the Registration of In Vitro Diagnostic Reagents

● Decision on Adjusting the Approval Procedures for Certain Administrative Approval Matters Concerning Medical Devices

● Public Consultation on the Amendment to the Regulations on the Supervision and Administration of Medical Devices (Draft for Comments)

● Basic Requirements for Clinical Evaluation Data of In Vitro Diagnostic Reagents Exempt from Clinical Trials (Trial)

In terms of innovation, in recent years, the state has consistently encouraged the medical device industry to pursue technological innovation, thoroughly shedding its former position at the bottom of the industrial chain, which relied on low-end products for meager profits.

The new regulations related to innovation in 2017 are mainly as follows:

● Guidelines for the Preparation of Application Materials for Priority Review of Medical Devices (Trial)

● Policies on Encouraging Innovation in Drugs and Medical Devices and Reforming Clinical Trial Management (Draft for Comments)

● Opinions on Deepening the Reform of the Review and Approval System to Encourage Innovation in Drugs and Medical Devices

Capital: Favorable Investor Sentiment, Accelerated Industry Consolidation

Domestic medical devices are enjoying substantial policy dividends, while capital favor has enabled the industry to enter a fast track of development through resource integration.

According to incomplete statistics from VCBeat, the medical device industry witnessed a total of 84 financing events (including 8 IPOs) in 2017, with a cumulative amount of nearly $1.6 billion (approximately RMB 10 billion). This wave of capital primarily flowed into subsectors such as in vitro diagnostics, radiation medicine, medical imaging, ultrasound equipment, medical robots, endoscopic minimally invasive devices, rehabilitation medicine, and home medical equipment.

Among them, the medical imaging equipment sector is flourishing across the board, with a wave of positive financing news.

On September 4, 2017, Sinovision Technologies, a dark horse in China’s domestically produced CT scanner market, announced that it had secured RMB 200 million in joint investment from Yili Fuyi Daohe, Huagai Capital, and Qiming Venture Partners.

Click for details:Sinovision Announces RMB 200 Million in Joint Investment to Accelerate Clinical Development and Application of Multi-Disciplinary CT Projects

On September 15, 2017, United Imaging Healthcare successfully completed a Series A financing round of RMB 3.333 billion, setting a record for the largest single private equity financing in China’s medical device industry to date. As a provider of high-end medical equipment and healthcare informatics solutions, United Imaging Healthcare’s successful fundraising not only raised its valuation to RMB 33.333 billion but also highlighted the promise of domestically produced high-end medical equipment in China.

Click for details:United Imaging Healthcare Completes RMB 3.333 Billion Series A Financing, Reaching a Post-Money Valuation of RMB 33.333 Billion

On October 20, 2017, two domestic medical imaging equipment manufacturers simultaneously announced the completion of a new round of financing.

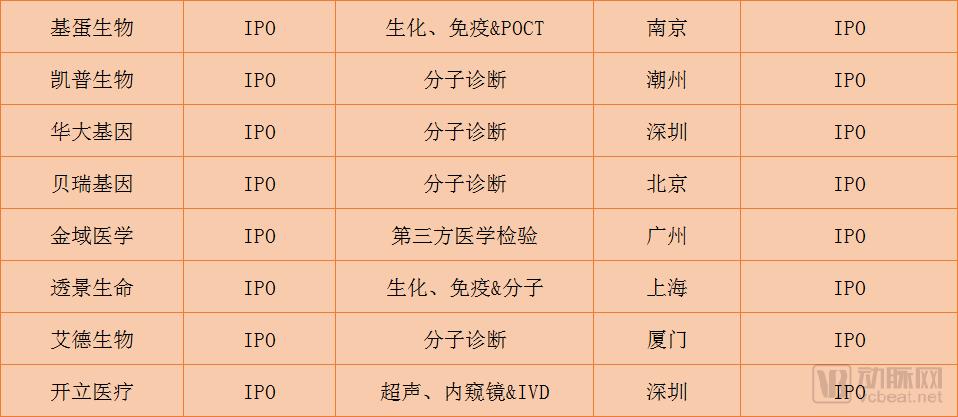

According to incomplete statistics from VCBeat, approximately 13 medical device companies successfully went public in 2017, spanning multiple sub-sectors such as in vitro diagnostics (IVD), imaging equipment, medical consumables, and device leasing. Among these, eight companies were in the IVD sector, underscoring that the IVD market remains the most favored segment by capital markets.

In 2017, Eight IVD Companies Successfully Went Public

Among these, molecular diagnostics was arguably the hottest topic in the IVD sector last year, with BGI Genomics, Berry Genomics, AmoyDx, and Hybribio going public one after another. In addition, KingMed Diagnostics, a leading third-party medical laboratory service provider, also listed on the capital market in September 2017.

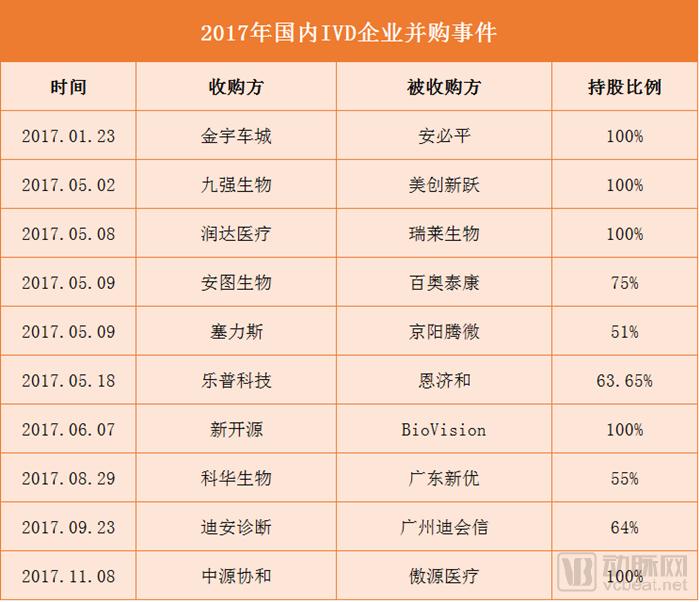

For the medical device industry, 2017 was a year of frequent mergers and acquisitions, characterized by a “big fish eating small fish” dynamic. Both Chinese and international companies spared no expense in their aggressive acquisition sprees, with each M&A deal signaling either a shift or a major transformation in the industry landscape.

Overseas, the medical device industry saw 10 major mergers and acquisitions in 2017, with a total transaction value reaching an astonishing $73.5 billion.

BD’s core businesses include medical and genomic research, diagnosis of infectious diseases and cancer, medication management, infection prevention, interventional therapy, and diabetes management. Bard’s core businesses focus on peripheral vascular, specialized surgery, oncology, urology, and electrophysiology. The merger of the two companies will enable complementary advantages and foster development across a broader spectrum of fields.

On April 24, 2017, Becton Dickinson (BD), one of the world’s largest medical technology and medical device companies, announced that it would acquire C. R. Bard, Inc. for $24 billion in a cash-and-stock transaction.

Click for details:BD to Acquire Bard Medical for $24 Billion; Both Boards of Directors Have Approved

Abbott Laboratories also made significant moves in 2017. At the end of 2016, it announced the $25 billion acquisition of St. Jude Medical, challenging Medtronic in the cardiovascular sector. Six months after acquiring St. Jude Medical, Abbott further announced the acquisition of Alere, a leading company in point-of-care testing (POCT).

Click for details:Abbott Claims $5.3 Billion Acquisition of POCT Leader Again After 14 Months: How Many Stories Are Hidden Behind It?

On June 28, 2017, Philips announced that it would acquire Spectranetics Corp., a U.S. manufacturer of minimally invasive surgical medical devices, for €1.9 billion (approximately $2.16 billion), to expand its leading position in the global image-guided therapy market and accelerate the expansion of image-guided therapy devices for the treatment of cardiac and peripheral vascular diseases.

Click for details:Philips Acquires Medical Device Maker Spectranetics for €1.9 Billion to Accelerate Expansion of Image-Guided Therapy Devices

On December 26, 2017, PerkinElmer officially announced the completion of its acquisition of EUROIMMUN Medizinische Labordiagnostika AG, with a total transaction value of approximately $1.3 billion (equivalent to RMB 8.5 billion).

Click to view details:$8.5 Billion! PerkinElmer Acquires EUROIMMUN Medizinische Labordiagnostika AG, Possibly the Final M&A Deal in the IVD Sector in 2017

Compared with foreign markets, China’s medical device industry remains in a growth phase, characterized by high growth rates, low entry barriers, and intensifying competition. However, with the acceleration of A-share initial public offerings (IPOs), several mergers and acquisitions took place in China’s medical device industry in 2017, primarily concentrated in the in vitro diagnostics (IVD) sector, involving well-known companies such as Runda Medical and Dian Diagnostics.

In addition to integrating domestic resources, Chinese medical device companies are also accelerating the acquisition of high-quality overseas enterprises to introduce more advanced technologies.

In September 2017, Weigao Group acquired U.S.-based Argon Medical Devices for RMB 5.6 billion. Argon Medical Devices is primarily engaged in the research and development, manufacturing, sales, and distribution of medical devices for oncology and vascular interventional procedures. Such a substantial overseas acquisition by Weigao is uncommon in recent years, indicating that the company has begun to strategize its presence in the global market.

Among the three leading domestic medical consumables manufacturers—Weigao, Lepu Medical, and MicroPort—MicroPort has achieved the most successful international expansion. Its 2017 semi-annual financial report showed that 96% of its revenue came from overseas markets.

In November 2017, MicroPort Medical signed an agreement with LivaNova PLC, announcing the acquisition of LivaNova’s cardiac rhythm management business for $190 million in cash.

Click to view details:MicroPort Medical to Acquire LivaNova’s Cardiac Rhythm Management Business for $190 Million, Targeting the Global $10 Billion CRM Market

In addition to consumables, medical imaging equipment represents a relatively specialized segment within China’s medical device industry. Wandong has long been a leading player in the broad field of medical imaging, but it lacks ultrasound products.

In December 2017, Wandong Medical joined forces with Yunfeng Capital, Tianyi Investment, Yuyue Medical, the Shanghai Free Trade Zone Fund, and Kangda to form the “Strongest Medical Investment Consortium in China,” planning to acquire Esaote S.p.A., a top Italian medical equipment manufacturer, for €248 million (approximately RMB 1.937 billion).

Click for details:Breaking: Jack Ma’s Fund Leads Top-Tier Investment Consortium, Including Wandong Medical, in €190 Million Acquisition of Italy’s Esaote

Technical Upgrades, Role Transitions

Driven by national policies and capital investment, domestic innovation has emerged as the most significant theme in the development of the medical device industry in recent years. The year 2017 was hailed as a landmark year for the convergence of technologies represented by artificial intelligence, big data, and 3D printing. Under the guidance of these emerging technologies, technological iterations have intensified competition within the medical device sector.

The most significant emerging technology in 2017 was undoubtedly artificial intelligence (AI). Traditional medical device manufacturers have also targeted this trend, devoting substantial resources to the research and development of AI-powered products, or partnering with AI companies to intelligently upgrade their existing offerings. Among these, industry giants such as GE, Siemens, and United Imaging Healthcare have demonstrated particularly outstanding performance, as detailed in reports by VCBeat.

Click for details:How These 8 Top Medical Device Companies Are Embracing AI Through Intelligent Solutions?

Furthermore, the development of big data has further stimulated the construction of healthcare informatization. Informatization has gradually played a crucial role in the procurement management, maintenance management, and asset management of medical devices. This has ushered in development opportunities for third-party service providers in the medical device sector. VCBeat has also conducted interviews and published reports on relevant companies.

Click for details:In the field of third-party medical equipment services, how does Kunya Medical break the “monopoly” of industry giants?

In addition to technological innovation, major equipment manufacturers are also seeking business model innovation, transitioning from their traditional role as equipment manufacturers to providers of comprehensive equipment solutions.

Companies have gradually evolved from initially manufacturing devices for treating a single type of disease, to producing a range of devices for that same condition, then investing in other medical institutions related to the disease, and finally perfecting their product lines to become comprehensive solution providers for treatment equipment targeting that specific disease.

Among them, manufacturers of smart wearable devices stand out the most. They have gradually evolved from being purely hardware manufacturers into providers of comprehensive smart wearable solutions that integrate “hardware + software + cloud services.”

Moreover, product-dependent manufacturers have also begun to transition toward service-oriented models. Medical device manufacturers previously relied on the production and sale of medical devices, resulting in a singular business model with limited value-added potential. As China’s healthcare system reforms continue to advance, various unreasonable policy restrictions on healthcare institutions and medical services are being gradually lifted.

It has become possible for manufacturing enterprises to provide services leveraging the medical devices they produce, which will effectively enhance the value-added of their business operations and diversify their business lines. For instance, companies can build chronic disease management platforms based on blood glucose meters to provide long-term services to patients; or establish independent diagnostic centers and health examination centers based on diagnostic equipment, thereby alleviating pressure on hospitals and improving patients’ healthcare experience.

Identifying New Growth Points in Each Subsector

As the largest segment of the medical device industry, the in vitro diagnostics (IVD) sector comprises numerous subsegments, each exhibiting significant differences in life cycle, market size, growth rate, technological barriers, and marketing channels.

In 2017 alone,Immunodiagnostics, molecular diagnostics, and POCT are experiencing the most rapid growth, with chemiluminescence emerging as a new growth driver.

In addition, the IVD sector has consistently remained a hot spot for capital investment. According to incomplete statistics from VCBeat, there were 38 financing and investment events in China’s IVD industry in 2017, with a cumulative amount exceeding USD 400 million; among these, the molecular diagnostics segment (particularly gene sequencing) attracted the most funding.

In 2017, the number of publicly listed in vitro diagnostics (IVD) companies also increased rapidly, with seven companies going public (Hybribio, Tumor Vision, BGI, Getein, KingMed, AmoyDx, and Sonoscape) and one completing a backdoor listing (Berry Genomics). To date, the roster of publicly listed IVD companies in China has expanded to 21.

At the end of 2017, VCBeat conducted a detailed year-end review of this niche sector.Click for details:10 Major M&A Deals, 8 IPOs: Immune and Molecular Diagnostics See Fastest Growth; 4 Sectors Most Worthy of Investment

The field of medical robotics has long been regarded as the “crown jewel” of both the broader robotics sector and the medical device industry. Due to its reliance on complex, cutting-edge multidisciplinary technologies and its profound impact on public welfare and industrial transformation, this high-barrier, high-value domain is often referred to as the “space program” of the healthcare industry.

In 2017, the most appropriate keyword for the medical robotics industry should be “domestic robots”Implementation and R&D”。

In its year-end review of the medical robotics sector, VCBeat found that certain surgical and service robots are gradually being deployed in clinical settings, expanding from laboratories in major hospitals in Beijing, Shanghai, and Guangzhou to markets across China, including Sichuan, Karamay in Xinjiang, and Foshan. Meanwhile, aided by artificial intelligence, triage robots, medication dispensing robots, and intelligent consultation robots are also being implemented in various Grade 3A hospitals and rural hospitals.

In terms of financing, medical robotics companies experienced rapid growth in 2017. The seven companies that secured funding, together with Tinavi Medical Technologies, raised approximately RMB 1.5 billion. Even excluding the large financing rounds of Tinavi Medical Technologies, Anhan Medical, and CloudMinds, the total financing amount for the medical robotics sector still exceeded RMB 100 million.

These funded companies operate in fields including surgical robots, service robots, and rehabilitation robots (exoskeleton robots). Notably, in the rehabilitation robotics sector, three companies announced financing rounds this year: MaiBu Robotics’ angel round, Ruihan’s angel round, and Jianjiao Technology’s Pre-A round.

In the first half of 2017, VCBeat conducted a large-scale scan of the medical robotics sector and published a year-end review at the end of the year.

Click for details:China’s Medical Robotics Industry Landscape: 2 Publicly Listed, 12 Funded, and Nearly One-Third of Teams from Harbin Institute of Technology

Click for details:Annual Financing Reaches ¥1.5 Billion; Surgical, Service, and Rehabilitation Robots See Steady Growth, with “Commercial Deployment” as the Key Theme

With the advancement of technologies such as sensors and microfluidics, the trend toward miniaturization and intelligence in the medical device industry is becoming increasingly prominent. Smart home-use medical devices have emerged as a new growth hotspot in China’s medical device sector.

Smart home medical devices represent an organic integration of healthcare and technology. Designed primarily for home use, these devices leverage technologies such as the Internet, big data, and cloud computing to enable intelligent functions, including remote connectivity for the monitoring of daily physiological indicators.

In recent years, the global market size for home-use medical devices has continued to expand steadily. From 2011 to 2016, the global market size grew from USD 19.2 billion to USD 26.2 billion, with a growth rate consistently maintained between 5% and 8%, demonstrating a relatively robust development trend.

Lifesense Medical, as a leading enterprise in China’s smart home medical device sector, also partnered with multiple well-known industry companies in 2017 to jointly lay out its presence in the broader health industry.

On December 22, 2017, Lifesense Medical announced the joint establishment of the Guangzhou Lifesense Yuhong Healthcare Industry Investment Fund with Yuhong Investment, aiming to achieve its strategic goal of extending the industrial chain. The fund has a total size of approximately RMB 50 million and is dedicated to investing in areas aligned with Lifesense Medical’s core business, including medical services, medical devices, healthcare information technology and services, pharmaceuticals, and the broader health and wellness sector.

Click to view details:LifeSense Medical and Yuhong Investment Establish RMB 50 Million Industrial Investment Fund to Cover the Entire Medical Industry Chain