2018: The Great Voyage Era of Healthcare Investment

Healthcare investment in China and the United States has arguably never been as closely intertwined as it is today. China may now be beginning to replicate the two-decade boom of the U.S. biopharmaceutical venture capital market. As we look toward 2018, many are eager to embark on a new age of exploration in healthcare investment. Yet, even amidst surging data and enthusiasm, calm reflection is essential. This new frontier demands not only courage but also professional insight and a sense of reverence.

China Renaissance has been focusing on and deeply cultivating the “Healthcare and Life Sciences” sector since 2008, with in-depth coverage across 29 sub-sectors. To date, its advisory team has served as financial advisor for nearly 50 financing and M&A transactions, with a total transaction value of approximately USD 2.1 billion.

In this article, the healthcare team at China Renaissance interprets four major sectors and 11 subsectors of China’s healthcare investment market in 2017, offering key insights into the venture capital boom in healthcare to cut through the noise and reveal underlying fundamentals.

Funding Side

From the perspective of China’s overall private equity fund industry, a total of 813 funds completed fundraising in 2017, representing a year-on-year increase of approximately 9.4%; the total amount raised by newly established private equity funds disclosed in 2017 was approximately USD 367.1 billion, a year-on-year increase of approximately 65%; and the average amount raised per fund in 2017 was approximately USD 450 million, a year-on-year increase of approximately 51%.

The above indicators demonstrate that the volume and strength of capital flowing into China’s private equity sector are continuously increasing, while funds’ fundraising capabilities have also improved significantly.

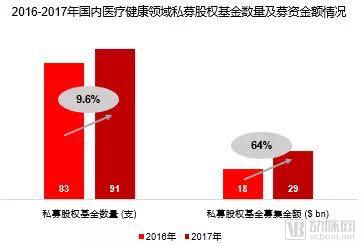

Within the healthcare sector specifically, a total of 91 funds focused on or attentive to healthcare were raised in 2017, representing a year-on-year increase of approximately 9.6%. The total capital raised disclosed in 2017 amounted to approximately USD 29 billion, a year-on-year increase of nearly 64%. The average amount raised per fund in 2017 was approximately USD 320 million, reflecting a year-on-year increase of nearly 50%.

Among them, new funds in the healthcare sector accounted for approximately 11% of the total number of new private equity funds in 2017, while the capital raised by these healthcare-focused new funds represented about 8% of the total capital raised by all new private equity funds.

Compared with the U.S. venture capital market, there is still significant room for growth in the funding side of China’s healthcare sector. With the entry of various “national teams” and “local government-backed funds,” coupled with the reform measures already implemented and those planned by the government in the healthcare field, an increasing amount of capital is expected to flow into this sector in the future.

Asset Side

1. Pharmaceutical and Biotechnology Industry

The pharmaceutical and biotechnology sector has long been a key focus area for the China Renaissance Healthcare team. China Renaissance firmly believes that domestic companies continuously developing first-in-class and best-in-class drugs and therapies will inevitably disrupt the global landscape of the biopharmaceutical industry. Achieving this goal requires an exceptional entrepreneurial team, supportive industrial policies, and capital market momentum—all of which are indispensable.

China Renaissance’s healthcare team has compiled and analyzed transaction data from the pharmaceutical and biotechnology industries in 2017:

There were 67 private equity financing transactions, representing a year-on-year increase of nearly 45%, with total financing amounting to approximately $2.85 billion, up by about 50% year on year; the average financing amount per transaction was around $42 million, showing a slight year-on-year increase. There were 20 initial public offerings (IPOs), marking a year-on-year increase of approximately 150%, with total IPO proceeds reaching about $1.65 billion, down by roughly 33% year on year; the average proceeds per IPO stood at approximately $83 million, reflecting a year-on-year decline of about 73%.

Regardless of growth trends or activity levels, private equity financing remains the primary transaction vehicle in this industry and is expected to maintain this trend over the next three to five years.

Antibodies and CAR-T are two important areas in the pharmaceutical and biotechnology sectors. Tumor immune checkpoint inhibitors represent the largest R&D focus in oncology treatment.

Antibody:

The market size of China’s biopharmaceutical industry has currently reached nearly RMB 150 billion, with the compound annual growth rate (CAGR) expected to remain at 13% in the coming years, as an increasing number of pharmaceutical companies enter the biopharmaceutical sector. Among biopharmaceuticals, monoclonal antibodies (mAbs) are experiencing the fastest growth, with a projected CAGR of 24%. Given the low market penetration of mAbs in China, there is substantial room for future growth. However, as the number of competitors increases, domestic enterprises will face an increasingly competitive market environment.

For startups in this field, companies with unique technological platforms for superior target pathway research and robust global multi-center clinical capabilities are more likely to stand out in fierce market competition. In addition to monoclonal antibodies, technologies such as bispecific antibodies and antibody-drug conjugates are also emerging.

CAR-T Cell Therapy:

CAR-T therapy has recently garnered significant market attention. Currently, CAR-T therapy remains primarily focused on the treatment of hematologic malignancies; however, given that long-term relapse rates post-treatment remain unknown and the therapy is costly, it is unlikely to replace conventional treatment modalities in the short term.

In the field of solid tumor therapy, CAR-T still has poor therapeutic effects. Many companies have attempted to upgrade the way CAR-T therapy kills tumors and combine it with other treatment methods such as PD-1/PD-L1 to achieve a breakthrough in therapeutic effects.

With Novartis’ and Kite’s CAR-T therapies, Kymriah and Yescarta, becoming the first to receive FDA approval for market launch, and with Kite and Juno being acquired by Gilead and Celgene, respectively, at sky-high valuations, global capital markets have once again turned their focus to the CAR-T sector in search of the next unicorn.

Among domestic CAR-T companies, those that were the first to file Investigational New Drug (IND) applications—including Carsgen Therapeutics, Legend Biotech, Hengrun Dasheng, Beijing Marino, UCAR-T, Bosheng Ji’anke, and Shanghai Mingju Bio—are poised to emerge as leading enterprises in this field.

Tumor Immunology:

Due to their significant clinical efficacy, continuously expanding indications, and rich combination therapy options, immune checkpoint inhibitors are poised to become the best-selling anti-cancer drugs over the next five years. To date, six immune checkpoint inhibitors have been approved globally. In China, PD-1 and PD-L1 are currently the most prominent targets, while numerous companies have also established pipelines targeting CTLA-4, IDO, A2aR, and other markers.

The innovative drug sector remained highly active in 2017, marking the official upgrade of China’s pharmaceutical industry into the 2.0 era. With the Hong Kong Stock Exchange introducing new listing rules favorable to life sciences companies, another surge in the capital market is expected in 2018. Increasing amounts of venture capital will flow into the innovative drug sector, accelerating the emergence of original novel drugs developed in China from a financial perspective.

2. Medical Device Industry

As another sector that integrates technology, patents, and talent, medical devices are also a key area of focus for the Huaxing Medical team.

Currently, the primary development directions for domestic medical device companies in China remain import substitution, mergers and acquisitions (M&A) for expansion, and digital transformation. Through import substitution, these companies are gaining policy advantages in sectors dominated by international brands, such as cardiovascular, orthopedics, surgery, medical imaging, dentistry, and neurology. Meanwhile, M&A activities enable them to expand their product portfolios and accelerate channel expansion.

Digitalization represents another pathway for the development of medical device enterprises. With continuous advancements in emerging technologies such as artificial intelligence, mobile and telemedicine, big data, and the Internet of Things (IoT), digitalization will facilitate “cross-boundary expansion” for medical device companies, enabling them to accumulate and consolidate big data assets at an early stage and achieve product iteration and upgrading.

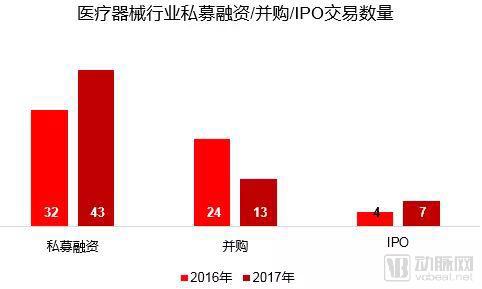

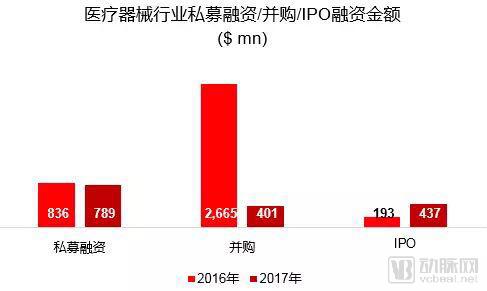

In mid-2017, the medical device industry recorded 43 private equity financing transactions, a year-on-year increase of approximately 34%. The total financing amount reached nearly $800 million, with an average of about $18 million per transaction, both representing a slight year-on-year decline. There were 13 mergers and acquisitions (M&A) deals, a year-on-year decrease of approximately 50%. The total transaction value was around $400 million, with an average deal size of about $31 million, both showing year-on-year declines. Meanwhile, there were 7 initial public offerings (IPOs), a year-on-year increase of approximately 75%. The total IPO proceeds amounted to roughly $440 million, up by about 126% year-on-year, while the average IPO proceeds per company reached approximately $62 million, marking a year-on-year increase of nearly 30%.

Data indicates that in 2017, as regulatory authorities tightened their review of mergers and acquisitions (M&A) and restructuring, China’s M&A market adopted a more cautious stance, leading to declines in both the number and value of transactions. However, given the narrow yet high-barrier nature of individual medical device sectors, we maintain that M&A will remain one of the primary exit channels for investment institutions in the foreseeable future.

Orthopedic Instruments:

The three most important segments in orthopedic devices are trauma, spine, and joints. Considering factors such as technological barriers to entry, the difficulty of obtaining regulatory approvals, and the establishment of distribution networks, the joint segment will emerge as the subsector with the greatest growth potential in the future and will accelerate the pace of import substitution.

From the perspective of China Renaissance, the key technological development directions in the joint field include 3D printing, trabecular bone structures, and new materials. At the policy level, the future implementation of the two-invoice system will have a significant impact on orthopedic implant companies.

Medical Imaging AI:

The massive growth of medical data is severely mismatched with the number of physicians. In 2017, the rapid development of AI technology made AI-assisted imaging diagnosis a reality.

Domestic startups in this field have entered the medical imaging AI industry by leveraging their unique resources and advantages, primarily falling into three categories: internet/AI giants with strengths in AI resources and algorithms, such as Tencent Miying, Alibaba Cloud, and iFlytek; startups with advantages in algorithms and medical resources, such as QED Technique, TomoDeep, and Bigwei; and third-party imaging centers with strengths in data and medical resources, such as Yizhan Technology and Huiyi Huiying.

The integration of AI technology with medical imaging will usher in a new era of “intelligent healthcare.” While an increasing number of startups are entering this field, the focus of capital markets will center on how to achieve commercial implementation of these technologies and rapidly establish sustainable profit models. AI-assisted diagnosis has initially taken root in areas such as pulmonary nodule detection, and is expected to expand further into more challenging disease domains, including liver cancer.

3. Healthcare Services Industry

The domestic healthcare services sector is profoundly influenced by national healthcare system reforms, particularly public hospitals, which command 80% of China’s medical resources. Meanwhile, the private healthcare services landscape comprises enterprises with diverse backgrounds and business models. The Huaxing Healthcare team maintains close monitoring of leading companies across major sub-sectors.

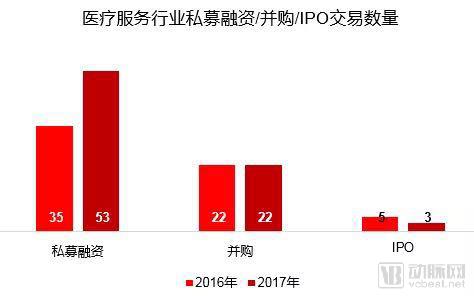

In 2017, the healthcare services sector saw 53 private equity financing deals, a year-on-year increase of approximately 50%, with total funding reaching nearly $900 million, up by about 86% year on year. The average deal size was approximately $17 million, representing a year-on-year increase of around 23%. There were 22 mergers and acquisitions (M&A) transactions, remaining flat compared to the previous year, with a total transaction value of nearly $1 billion, down by approximately 58% year on year. The average M&A deal size was about $45 million, also decreasing by roughly 58% year on year. Additionally, there were 3 initial public offerings (IPOs), a 40% decline from the prior year, raising approximately $210 million in total, a drop of about 44% year on year. The average IPO raise amounted to around $70 million, showing a slight year-on-year decrease.

Data indicates an upward trend in the number of private equity financing transactions, total financing amount, and average deal size.

Chain Clinics:

Chain-operated private clinics can address some of the shortcomings of traditional community healthcare. In the future, new types of chain clinics with strong technical capabilities, high service quality, and standardized management will experience rapid development.

Among these, the three most typical models of new chain community clinics are: mid-to-high-end private clinics (representative enterprises: Jonsen Medical, Xinkang Medical, Zhuozheng Medical), internet healthcare companies with offline clinic operations (representative enterprises: Chunyu Doctor, DXY Clinic), and platform-based enterprise chain community clinics (representative enterprises: Wanfang Development, AliHealth).

In addition, new business models such as capital-favored pediatric chain clinics and ambulatory surgery centers have also emerged.

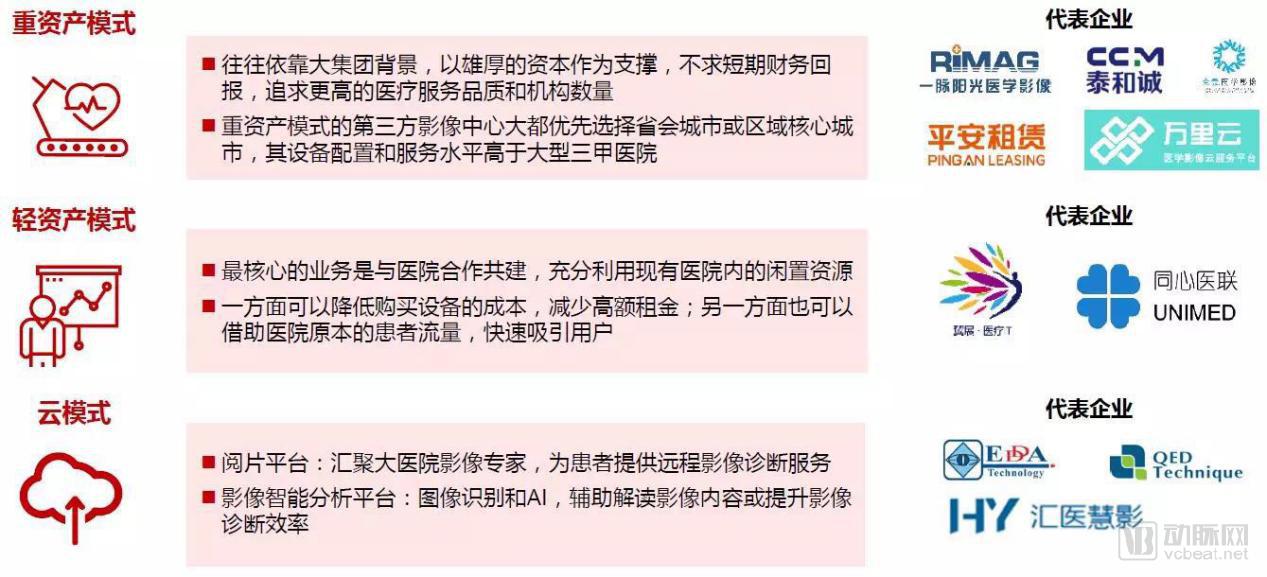

Independent Imaging Centers among Third-Party Services:

The state has clearly expressed its encouragement of third-party services across ten key sectors, with the medical imaging field experiencing the most rapid growth in recent times. Compared to in-hospital imaging examinations, independent imaging centers offer lower costs and higher-quality services. However, the development of independent medical imaging centers in China remains in its early stages. With the continued advancement of tiered diagnosis and treatment, restrictions on new equipment acquisitions by large public hospitals, and the relaxation of policy constraints on independent imaging centers, the future market size is projected to exceed RMB 50 billion.

Currently, there are three main models for independent medical imaging centers in China: the asset-heavy model, the asset-light model, and the cloud-based model.

TCM Chain Clinics:

The Law on Traditional Chinese Medicine officially adopted the provision to change the regulatory model for TCM clinics from a licensing system to a filing system, which came into effect on July 1, 2017, ushering in a new era of growth for TCM services. Currently, the TCM clinic industry is highly fragmented. The “asset-light + standardized branding” model of chain clinics facilitates market share expansion. However, as the growth rate of total TCM patient visits slows, building corporate brands and enhancing customer stickiness will become critical.

From the perspective of revenue composition, pharmaceutical sales account for more than 70% of the income generated by TCM outpatient clinics. We believe that enterprises with unique core advantages—such as high-quality TCM decoction pieces backed by a fully integrated industry chain, or those adopting the traditional “front-shop, back-clinic” model (represented by Heshuntang)—will rapidly gain a competitive edge in regional markets. These companies will quickly build reputation and customer loyalty during the early stages of expansion, thereby gradually achieving nationwide presence across China.

4. Diagnostics and Genetic Testing Industry

The gene sequencing industry is another niche sector that the Huaxing Medical team strategically focused on in 2017.

China’s current industry landscape is characterized by an oligopoly in the upstream sector and intense competition in the midstream segment. The midstream sector primarily focuses on the diversified applications of genomic data, where Chinese unicorn companies are expected to emerge in areas such as research sequencing services, oncology genetic testing, reproductive health sequencing, and consumer-grade sequencing. The industry will undergo a transition from technology-driven growth to business model-driven expansion, ultimately achieving large-scale consolidation, making its future prospects highly promising.

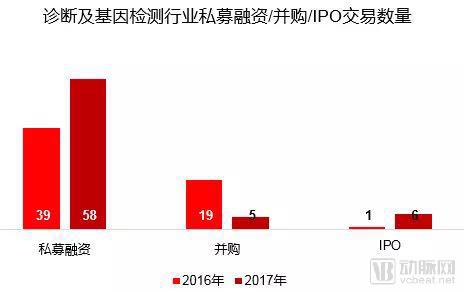

2017, the diagnostics and genetic testing industryThere were 58 private equity financing transactions, representing a year-on-year increase of nearly 50%, with total financing amounting to approximately $1 billion, a year-on-year increase of about 26%. The average financing amount per transaction was approximately $17 million, showing a slight year-on-year decline. There were 5 mergers and acquisitions (M&A) transactions, a year-on-year decrease of about 74%, with a total transaction value of approximately $60 million, down about 85% year-on-year. The average deal size was approximately $12 million, a year-on-year decrease of about 42%. There were 6 initial public offerings (IPOs), a year-on-year increase of 500%, with total IPO proceeds reaching approximately $440 million, up about 380% year-on-year. The average IPO proceeds per transaction were approximately $74 million, a year-on-year decrease of about 20%.

Over the next three to five years, a large number of midstream genetic testing companies in China will enter a critical life-or-death phase characterized by product regulatory approval and market development. Consequently, they will remain heavily reliant on capital from private equity financing to achieve technological upgrades and business expansion. Companies with strong R&D capabilities and robust commercialization prowess are highly likely to survive and gradually usher in an oligopolistic landscape, akin to China’s internet industry more than a decade ago.

Liquid Biopsy for Tumors:

Grail, a liquid biopsy company focused on early cancer screening, completed a $900 million funding round in 2017, marking the largest private financing in the global oncology liquid biopsy sector.

Turning to the domestic market, driven by factors such as patient population size, treatment demand, technological advancements, and willingness to pay, China’s tumor liquid biopsy market is poised for explosive growth. The market size is projected to reach RMB 90 billion (covering both cancer early screening and treatment).

Currently, companies in China engaged in tumor liquid biopsy primarily employ two major technical approaches: PCR and NGS. Representative enterprises in the PCR field include Amoy Diagnostics, Boer Cheng, and New Horizon Health, while those in the NGS field include BGI Genomics, Genetron Health, Burning Rock Biotech, Kangsoo Gene, and AnchorDx.

Third-Party Medical Laboratory Testing:

China’s third-party medical laboratory industry has maintained rapid growth in recent years, with a compound annual growth rate exceeding 30%. However, its market penetration remains low compared to developed markets such as the United States. The market size is projected to reach RMB 25 billion by 2020. The primary care market is bound to expand, and new business collaboration models—such as Group Purchasing Organizations (GPOs), co-developed laboratories, and regional testing centers—will emerge. The proportion of specialized testing will increase significantly, unlocking a vast blue-ocean market for incremental growth.

Industry giants are rapidly expanding their business scopes through different models. Dian Diagnostics adopts a model centered on “products + services + operational management,” leveraging horizontal M&A to expand its ecosystem, while KingMed Diagnostics focuses on vertical deepening of services and R&D, building industry barriers through economies of scale. Which business model is superior remains to be seen over time, but one thing is certain: this niche sector continues to severely test a team’s commercial execution capabilities.

As gene sequencing startups gradually mature, it is worth consideration for established IVD (in vitro diagnostics) public companies on how to embrace this industry. On one hand, they can expand their business lines and product portfolios; on the other hand, they need to meet the market capitalization expectations of secondary market investors in China’s A-share market. This issue deserves reflection from both the industrial and investment communities.

Companion Diagnostics:

Co-development and bundled approval of new drugs with companion diagnostics will become the major trend in the future, ushering in an explosive growth for companion diagnostics.

Companion diagnostics can effectively screen for patients who respond to targeted therapies in clinical trials, significantly improving the success rate of these trials. Collaboration between innovative drug companies and companion diagnostic firms is deepening. The FDA has also endorsed the "targeted therapy + companion diagnostic" model and introduced multiple policies to standardize it.

In the future, companies that master diagnostic technologies with high sensitivity and high specificity, and can deliver greater clinical service value, will emerge as winners in this sector. This outcome will also depend on continued regulatory refinement of the companion diagnostics market.

1. Healthcare Opportunities Amid Capital Frenzy

Modern venture capital originated in the United States after World War II. Initially, the annual scale of venture capital investment in the Silicon Valley region was only a few million U.S. dollars, but due to high returns, the investment amount increased year by year.

In 2000, U.S. venture capital investment peaked at $100 billion, coinciding with the burst of the dot-com bubble. Over the past decade-plus, annual U.S. venture capital investment has ranged between $30 billion and $50 billion, rising to $70 billion in 2016 but never surpassing the 2000 record.

According to statistics, the average quarterly fundraising amount for early- and mid-stage venture capital funds in China exceeded $60 billion in 2017, with the annual total surpassing $240 billion. Although the growth rate of M2 dropped to 8.2% by the end of 2017, investment opportunities in the real estate market have vanished, and the volatility of the A-share market remains daunting. Consequently, idle disposable capital has naturally flowed into the venture capital sector, despite its uncertain depths.

Xinhua News Agency once reported that from 1990 to 2015, China experienced 55 bull-and-bear market cycles, a frequency more than six times that of the S&P 500 Index. Frequent fluctuations imply high risks; coupled with the generally poor quality of listed companies and the outflow of some high-quality enterprises to overseas markets, the scarcity of investment channels has long plagued domestic investors.

Even within the venture capital community, smart money is flowing from valuation peaks to underexplored industries. It seems that in 2016, everyone was still discussing the “capital winter.” However, this may have merely represented a shift in capital interest, turning away from relatively overheated sectors to seek new directions. As we entered 2017, it was hardly surprising that outstanding startups in the biopharmaceutical and biotechnology fields within China’s healthcare sector continued to emerge, becoming hot targets for venture capital investment.

2. Capital and Industry Diverge in Tandem

Compared with 2016, the number of private equity financing transactions in China’s healthcare industry rose steadily in 2017. Except for medical devices, the average transaction size increased significantly in the pharmaceuticals and biotechnology, diagnostics and gene sequencing, and healthcare services sectors. This trend was particularly pronounced in the biopharmaceutical field, where the total transaction value accounted for more than half of the market share.

Venture capital is also a market governed by supply and demand. When there is an influx of venture capital, the emergence of new technologies does not necessarily keep pace with the surge in capital. Projects that should not receive funding end up securing investments, and companies valued at $100 million are suddenly valued at $200 million. However, the greatest distinction—and allure—of venture capital compared to private equity (PE) investment lies in its pursuit of returns that are several-fold or even dozens of times higher. A valuation deviation of 50%–100% is not a major concern; but if you bet on the wrong team, you risk losing your entire investment.

The core competency of venture capital lies in accurately assessing technologies and anticipating future technological trends. Encouragingly, a number of leading VC firms in China have gradually established specialized teams with clear divisions of labor, successfully attracting a portfolio of outstanding investee companies through their efforts. Entrepreneurial teams with strong track records and unique technological barriers have enabled companies in the biopharmaceutical and gene technology sectors to stand out, emerging as rising stars.

In contrast, within the more traditional segments of the medical device industry—namely equipment and consumables—average deal sizes in both private equity and M&A transactions have declined significantly. Companies lacking core competitiveness are gradually fading from the radar of investors, and industry consolidation has entered its second half.

Overall, talent, capital, and resources are increasingly concentrating in emerging startups with high barriers to entry, while most outstanding companies are included in the investment portfolios of approximately 10 leading venture capital firms in China.

3. Risks and Opportunities Coexist: Only Those Involved Truly Know the Reality

The common perception is that high risk brings high reward, but this does not imply a causal relationship between the two. In Silicon Valley, 48% of venture capital funds incur losses, while Dr. Jun Wu, founding partner of Yuanjing Capital, estimates that only 5% of venture capital firms in China are profitable.

In terms of funding sources, venture capital (VC) funds are also a type of private equity fund. However, because they typically invest only in startups or even pre-incorporation ventures, they require teams to have keen judgment regarding technology and markets. In contrast, another category known as private equity (PE) funds primarily invests in relatively mature companies, aiming to transform them through operational improvements and capital restructuring before seeking an exit opportunity.

In the emerging healthcare sector, companies are far from reaching maturity, making them unsuitable for private equity (PE) funds. However, an increasing amount of capital with limited risk tolerance and shorter investment horizons is flowing into the venture capital stage. This trend has not only driven up valuations for early-stage and growth-stage assets to some extent but also imposed numerous restrictions on portfolio companies due to investors’ lack of discernment. For instance, if a company fails to meet the requirements for a qualified initial public offering (IPO) within a few years, it must pay annual interest rates of 8%–12%. Such venture capital practices compel entrepreneurs to divert significant time and energy toward short- to medium-term goals, thereby prematurely eroding future investment returns.

Entrepreneurs are increasingly deliberate in their choices regarding capital sources and the strategic resources they require, setting higher thresholds for institutional investment enthusiasm. For private equity (PE) firms, the key to success lies in patiently awaiting future industry consolidation opportunities while leveraging their strengths in resource allocation.

At this point, readers are undoubtedly eager for a discussion on whether there is a “bubble” in China’s healthcare investment sector. In response, we recommend cutting through the haze to uncover the essence:

Venture capital is inherently a high-risk industry. Even for industry experts who accurately assess technological and market trends, the probability of successfully guiding portfolio companies to an IPO exit remains low. If the majority of companies are destined to be eliminated, focusing on average market valuation levels holds little significance.

In a favorable macroeconomic environment, leading companies with superior capabilities across all dimensions exhibit a pronounced Matthew effect, becoming the focus of capital and market attention. These firms have the potential to evolve into platform companies and spearhead future industry consolidation; an excessive focus on valuation will result in missed investment opportunities.

Enterprises that secure financing first in niche sectors are more likely to maintain a sustained lead in their subsequent development, reinforcing the “strong get stronger” dynamic; whereas companies that miss the golden window for fundraising due to various hesitations may fall into developmental difficulties.

Due to its high-tech nature and stringent regulatory environment, the healthcare sector has effectively barred capital lacking professional judgment from entry. The misalignment of capital and asset risks could deliver a fatal blow to investors and undermine the overall development of the industry.

Conclusion

Some joke that Christopher Columbus was the earliest entrepreneur, in which case Queen Isabella of Spain was undoubtedly an investor with unique insight. She recognized the prospects and potential of Columbus’s business plan and provided him with funding. The young Columbus discovered the New World, securing 10% of the expedition’s proceeds, while the Queen reaped returns hundreds of times greater. This can be regarded as the earliest form of venture capital.

As we face 2018, many are eager to embark on the "Age of Discovery" in healthcare venture capital. This endeavor requires not only courage but also professional insight and a sense of reverence. What does reverence entail? We borrow the term "Pragmatism," highlighted in China Renaissance’s 2017 Year-in-Review: As China’s healthcare investment industry is still in its early stages, it demands a pragmatic spirit from both entrepreneurs and investors to drive the sector’s comprehensive development.