Smart Contracts in Blockchain for Healthcare: Bridging Technology and Medical Applications

The key technologies of blockchain mainly consist of four aspects: First, the block-plus-chain structure ensures data rigor and immutability. Second, distributed storage employs a decentralized ledger to ensure the decentralization of accounting responsibility and the integrity of the data system. Third, asymmetric encryption algorithms leverage cryptographic principles to secure data records and establish mutual trust within the blockchain network. Fourth, smart contracts, also known as scripts, enable transactions that meet specific conditions to be executed on the basis of security and mutual trust.

These four technologies form the foundation that has propelled blockchain to become the most prominent IT technology today. In the previous three articles, we introduced blocks, chains, distributed storage, and asymmetric encryption algorithms. Here, we will discuss smart contracts, exploring their role within blockchain technology and examining what challenges they can address in the healthcare sector.

Decoding Key Blockchain Terms (I): “Block” and “Chain”

Blockchain Keywords Explained (4): Smart Contracts

It has been nearly a decade since the emergence of blockchain technology. At its core, blockchain is a distributed database, and the digital currency Bitcoin, which originated alongside it, has become a highly sought-after, high-value digital asset. From its initial application in digital currencies to its current role as the foundational infrastructure of the future internet, blockchain has undergone significant iterations.

However, the value of blockchain technology extends far beyond digital currencies; it has established a decentralized autonomous community. The financial sector is poised to become a major application domain for blockchain, which will also serve as a critical underlying infrastructure for internet finance. Initially imperfect, the technology has undergone continuous iteration over the past decade, laying the groundwork for its commercial deployment.

To date, blockchain technology has been transitioning from version 1.0 to 3.0.

The Blockchain 1.0 Era, known as the Cryptocurrency Era, is represented by Bitcoin and primarily aims to address the decentralized management of currencies and payment methods.

The Blockchain 2.0 era, known as the era of blockchain contracts, is represented by smart contracts and promotes decentralization across the entire internet application market at a macro level, rather than merely facilitating currency circulation. Blockchain technology can be leveraged to enable the conversion of a wider range of digital assets, thereby creating value for these assets. All financial transactions and digital assets can be adapted for use on the blockchain, including financial products such as stocks, private equity, crowdfunding, bonds, hedge funds, futures, and options, as well as digital records such as digital copyrights, certificates, identity records, and patents.

The Blockchain 3.0 Era, known as the era of blockchain governance, is characterized by the integration of blockchain technology with the real economy and physical industries. By combining chain-based ledgering, smart contracts, and real-world applications, it enables decentralized autonomous governance and unlocks the value of blockchain.

Currently, in the nascent stage of Blockchain 2.0, its key technology lies in the application of smart contracts.

The Origin of Smart Contracts

A contract is a binding agreement that both parties are obligated to uphold. For instance, the automatic payment service for water, electricity, and gas bills linked to a savings card at a bank constitutes a contractual arrangement. When specific conditions are met—such as when the gas company transmits the monthly gas bill to the bank—the bank transfers the corresponding amount from the customer’s account to the gas company as agreed. If the account balance is insufficient, notifications are sent via SMS or other means. Prolonged non-payment results in gas supply suspension. Different conditions trigger different outcomes.

Smart Contract (smart contract) was born in1993around the year , long before blockchain technology. It was created by computer scientist and cryptography expert Nick Szabo in1993proposed in the year,1994published the paper “Smart Contracts”.Smart contracts are a set of digital formsDefined Commitments (promises), including an agreement under which the contracting parties can execute these commitments. Smart contracts embed the execution terms and liability for breach of contract by both parties into software and hardware, thereby controlling contract execution through digital means.

Features of Smart Contracts

1. Automation. Smart contracts can automatically execute the corresponding next-step transactions based on trigger conditions, with accurate and timely condition assessment. Traditional contracts require manual determination of trigger conditions, resulting in lower efficiency and accuracy compared to smart contracts.

2. Objective and Subjective Dimensions. Smart contracts are suitable for scenarios involving objective requests, whereas traditional contracts are better suited for indicators requiring subjective judgment. Indicators based on subjective judgment are difficult to incorporate into automated systems for evaluation, thereby hindering the execution of subsequent transactions.

3. Cost. Smart contracts incur low costs, as all conditional judgments, execution, and disposition are performed automatically.

4. Execution Timing. Smart contracts operate on a pre-agreed, preventive execution model, whereas traditional contracts are enforced after the fact.

5. Liability for Breach of Contract. The cost of breaching a smart contract is high; once a breach occurs, collateral such as digital assets and security deposits will be forfeited. In contrast, the enforcement of traditional contracts relies on legal penalties, which entails high execution costs.

6. Scope of Application. Smart contract technology can be adopted globally, whereas traditional contracts are heavily influenced by geographic factors; legal and cultural differences across regions can impact the enforcement process.

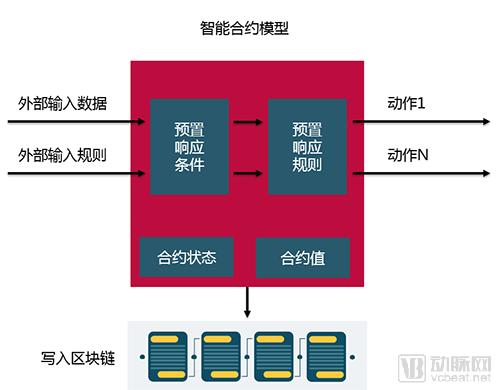

In essence, smart contracts function like if-then statements in computer programming languages; once predefined conditions are triggered, the contract executes automatically to facilitate the exchange of digital assets. The widespread adoption of smart contracts has been hindered by the need for underlying protocol support and the lack of digital systems and technologies inherently capable of supporting programmable contracts.

The emergence of blockchain not only supports programmable contracts but also offers advantages such as decentralization, immutability, and transparent, traceable processes, making it inherently suitable for smart contracts. Data cannot be deleted or modified, eliminating concerns about tampering with contract content. Contract execution is timely and effective, ensuring that the system will execute the contract when conditions are met. Meanwhile, network-wide backups maintain complete records, enabling post-event audits and historical traceability.

How Smart Contracts Work

Blockchain-based smart contracts handle both transaction storage and state processing entirely on the blockchain. Transactions primarily consist of the data to be transmitted, while events serve as descriptive metadata for this data. Once transaction and event information are input into the smart contract, the resource states within the contract’s resource set are updated, thereby triggering the smart contract to perform state machine evaluations. If the event actions meet the predefined trigger conditions, the state machine automatically and correctly executes the corresponding contract actions based on the participants’ preset configurations.

Ethereum and Smart Contracts

Ethereum is an innovative blockchain platform. Its innovation lies in encapsulating code and data within the blockchain, allowing anyone to build and use decentralized applications (dApps) powered by blockchain technology on the platform. It not only adopts the principles of blockchain but also adds the functionality to create smart contracts on the blockchain.

Ethereum originated in December 2013, when its founders—Vitalik Buterin, Gavin Wood, and Jeffrey Wilcke—began researching blockchain technology, attracting numerous technical experts worldwide to join their effort to build a smart contract platform that operates entirely on a trustless basis. In July 2015, Ethereum released its first version as an open-source blockchain project. Unlike Bitcoin, Ethereum is designed with significant flexibility and high adaptability.

Although Bitcoin represents a significant innovation in the technology sector, it has numerous limitations. Consequently, Ethereum established a programmable, Turing-complete blockchain. Turing completeness implies that the virtual machine and programming language possess the computational capability to solve any computable problem, performing all tasks achievable by a Turing machine.

On this blockchain, developers can create new digital assets by writing code, and they can also implement transfer functions for non-digital assets by coding smart contracts. As a Turing-complete blockchain infrastructure that supports programmability, it enables the management of a broader range of non-digital assets through such coding capabilities.This means that blockchain transactions involve far more than just buying and selling currencies; a wider range of application instructions will be embedded into the blockchain.Therefore, creating new applications on the Ethereum platformThe scenario becomes significantly simplified.

Application Cases of Smart Contracts in the Healthcare Sector

Smart contracts are a key feature that integrates blockchain with real-world application scenarios. They are also the primary reason blockchain is regarded as a disruptive technology and serve as the technological foundation for programmable finance and programmable currency. Smart contracts facilitate the transition of blockchain from theory to practice and may bring about significant transformations to human social structures in the future.

Smart contracts may become the fundamental building blocks of the global economy in the future, allowing anyone to access this global economy without prior censorship or upfront costs. Smart contracts do not require users to trust each other, as they are not only defined by code but also enforced by code, operating fully automatically and without interference. This is the concept of “code is law.”

In finance,Smart contracts can play a significant role in areas such as auctions, lending, wills, registration, crowdfunding, equity, voting, and insurance. Here, we select the representative application of medical insurance claims for description.

In the field of medical insurance, patients, healthcare institutions, and insurance providers form a triangular relationship. Inefficiencies and service complexities exist in every interaction.

For insurance service providers, insurance costs are high, particularly administrative costs. Significant effort is devoted to contract execution and management, database maintenance, payment and collection of funds, claims verification, and documentation review. One data point shows that in 2018, U.S. billing and insurance-related (BIR) The cost of activities will reach $315 billion, an increase of more than 100% compared to 2007.

For patients, most of them and their families are filled with uncertainty and fear when facing medical bills and third-party reimbursement processes. The complexity of insurance reimbursement makes the process lengthy, and patients have many questions that are difficult to resolve: Can it be reimbursed? How to reimburse? When will the reimbursement be processed?

For healthcare institutions, a significant amount of time each year is also spent on insurance reimbursement processes, organizing medical records, and undergoing audits by insurance service providers and government agencies.

Claims payment and adjudication is a highly complex process, involving substantial administrative costs and manual procedures to verify that all stakeholders comply with the agreed-upon terms in the contract. The vast majority of claims are not complex and can be processed using relatively simple logic within a fully automated workflow. Leveraging blockchain-based smart contract technology makes it feasible to achieve a fully automated process for insurance claims.

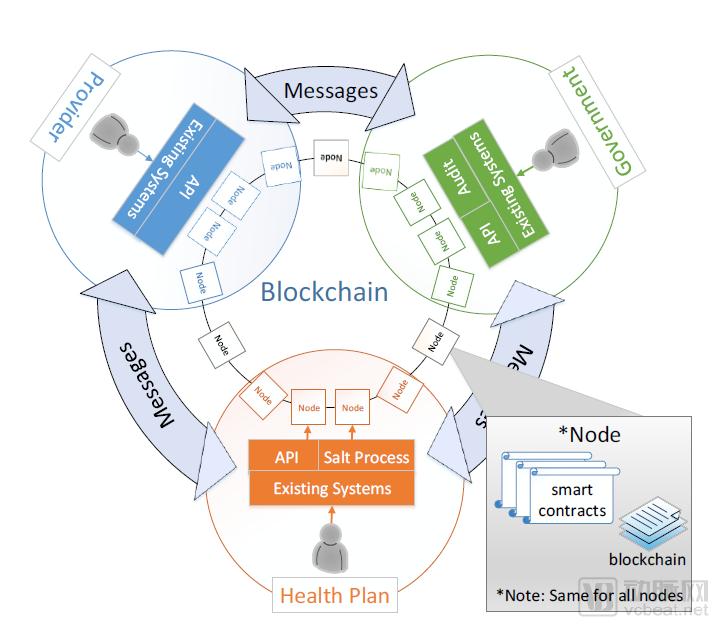

In this type of blockchain project, two types of data are processed: electronic health records (EHRs) and insurance contracts. Due to the high sensitivity of EHR data security and the current immaturity of blockchain technology, it remains highly challenging to store EHRs directly on the blockchain. Therefore, an interface-based approach can be adopted to integrate the two systems.

For instance, by integrating blockchain with Fast Healthcare Interoperability Resources (FHIR) API interfaces, data output can be restricted to only the information necessary for smart contract execution. Clinical care details associated with each claim can be stored on the blockchain as reference addresses, while being delivered via FHIR-compliant APIs. By storing URL links to clinical information on the blockchain rather than the actual clinical medical data, sensitive data shared among nodes is minimized, while still achieving interoperability and leveraging the advantages of blockchain technology.

Methods for Insurance Stakeholders to Provide Data and Join the Blockchain

From the perspective of understanding the term “contract,” the intelligent execution of insurance contracts is the most easily comprehensible application. However, in reality, nearly all blockchain applications utilize smart contracts. Here, “contract” is not limited to the execution of legal agreements but refers to automated execution triggered upon the fulfillment of specific conditions.

For example, addressing the issue of medical data flow.Protected by smart contracts, medical data can be shared with other hospitals, where users with physician credentials are granted one-time read access. The data is automatically destroyed after use, alleviating hospitals’ concerns about data security. Additionally, continuous medical data uploaded by patients with chronic diseases can be monitored; once indicators exceed predefined thresholds, both physicians and patients are alerted, and automated actions such as appointment scheduling are executed. All processes adhere to pre-established agreements that specify the events triggered upon meeting defined conditions.

Smart contracts offer immense potential, which is the primary reason blockchain technology has the capacity to disrupt our existing industries. Although smart contract technology holds great promise for automation, high efficiency, and low cost, it still has certain limitations. For instance, publicly accessible code may be inappropriate in some industries, necessitating gradual functional improvements in future developments.

References:

Blockchain Technologies: A whitepaper discussing how the claims process can be improved

Chang Jia, Han Feng, et al., *Blockchain: From Digital Currency to Credit Society*