Three Key Questions on the Role of GPO in Pharmaceutical Procurement: Foundations, Platform Construction, and Implementation Models

Since the Third Plenary Session of the 18th Central Committee of the Communist Party of China, reforms in drug procurement and supply have accelerated significantly. Since 2015, the Chinese government has successively introduced a series of landmark policies on drug procurement and supply reform, including the Guiding Opinions on Centralized Drug Procurement, the Guiding Opinions on Drug Price Reform, and the updated National Reimbursement Drug List. Drawing on internationally accepted drug procurement practices has become an important direction for China’s drug procurement and supply reform.

Furthermore, letting the market play a decisive role in the allocation of pharmaceutical resources is the central theme of the National Guidelines on Drug Pricing: actual transaction prices for drugs are formed through full market competition, government intervention in drug pricing is minimized to the greatest extent possible, and the reasonable formation of drug prices is guided by the reimbursement standards of medical insurance.

Drug GPO is an internationally recognized model for pharmaceutical procurement that is garnering increasing attention in China. While some regions are exploring its application, there remains considerable skepticism across various sectors of society. What environmental factors support the implementation of drug GPO? What operational models exist? And how can market-oriented GPOs be effectively applied?

Shanghai, Shenzhen, and Wuhan Take the Lead as Domestic GPOs Get Underway

Since 2015, with the in-depth advancement of healthcare reform and the launch of new rounds of centralized drug bidding across various regions, the national government, after designating 11 provinces and municipalities as pilot areas for healthcare reform, subsequently designated two-thirds of prefecture-level cities as national pilot cities for healthcare reform. It was explicitly stated that pilot cities are permitted to implement volume-based procurement reforms for drugs on a city-wide basis within the provincial framework for winning drug bids. As volume-based drug procurement is fundamentally very similar to Group Purchasing Organization (GPO) models, cities such as Shanghai, Shenzhen, and Wuhan have successively initiated pilot reforms in drug GPO procurement.

Shanghai was the first city in China to propose and implement reforms in Group Purchasing Organization (GPO) procurement of pharmaceuticals. Led by the health authorities, the specific GPO procurement operations are carried out by its subordinate Healthcare Services Center. The primary approach involves the Center establishing a transaction service platform for pharmaceutical GPO, with drug selection criteria determined by relevant experts from participating hospitals. The benefits derived from the GPO are primarily allocated to the individual participating hospitals.

In essence, Shanghai’s Group Purchasing Organization (GPO) procurement reform was government-led. However, the participating hospitals had divergent interests and objectives, leading to significant skepticism regarding the GPO’s operational processes, particularly concerning the transparency of its selection criteria. Furthermore, as not all medical institutions participated in the pharmaceutical GPO procurement, inconsistencies arose in drug retail prices across healthcare facilities in Shanghai, which dampened the enthusiasm of pharmaceutical manufacturers to engage. In 2017, the Shanghai Medical Health Affairs Service Center was even subjected to an antitrust investigation by national industrial and commercial authorities on suspicion of monopolistic practices.

As a frontier region of China’s reform and opening-up, Shenzhen’s drug Group Purchasing Organization (GPO) reform has drawn nationwide attention and received support from both national and Guangdong provincial health authorities. Following a selection process, the Shenzhen municipal competent authorities designated Shenzhen Quanyaowang Pharmaceutical Co., Ltd., a subsidiary of Shenzhen Neptunus Group, as the GPO procurement service provider for public hospitals in Shenzhen.

Unlike Shanghai, GPO service providers in Shenzhen not only offer online drug trading services but also engage in specific drug procurement and supply. After purchasing drugs through the GPO model, these service providers distribute them to relevant drug distribution companies, which then settle drug procurement transactions with hospitals.

Reviewing Shenzhen’s GPO practices, they are essentially led by government departments and have undergone antitrust investigations by national development and reform authorities. Following rectification under the guidance of Shenzhen’s competent authorities, the model has now expanded to Dongguan, while multiple other cities in Guangdong Province, such as Guangzhou and Foshan, are eager to adopt similar approaches. The “Opinions on Improving Policies for Drug Production, Distribution, and Use in Guangdong Province” further explicitly endorse the direction of GPO reform.

In 2017, Wuhan’s volume-based drug procurement adopted the services of the Central China Drug Trading Platform. At that time, volume-based drug procurement initiatives were emerging across China. Whether this signaled a strategic shift for the Central China Drug Trading Center—from its initial role as a Group Purchasing Organization (GPO) platform to a more clearly defined public drug trading platform—remains unclear. Publicly available information indicates that Wuhan’s approach differed from those of Shanghai and Shenzhen. Wuhan likely started with a very limited number of drug categories characterized by high consumption volumes and intense competition, rather than implementing broad-based reforms as seen in Shanghai and Shenzhen. However, there has been scant media coverage or commentary on the effectiveness of Wuhan’s volume-based drug procurement.

GPO Procurement Helps Lower Drug Prices and Reduce Healthcare Costs

Although pharmaceuticals are special commodities, they remain commodities at their core and inevitably share many characteristics with bulk goods. Long-standing administrative controls over drug procurement and supply in China have led to a series of anomalies, including artificially inflated and depressed drug prices. These distortions have not only strained medical insurance funds but also compromised public access to essential medications, fostered widespread misconduct within the industry, and ultimately undermined the government’s image in governance.

As a market-oriented procurement and supply model, Group Purchasing Organizations (GPOs) for pharmaceuticals undoubtedly contribute to establishing a unified, open, competitive, and orderly market in the healthcare sector. Furthermore, GPOs are prevalent across various industries, where exchanging volume for price and linking volume with pricing are universal principles applicable to all commodities, including pharmaceuticals. Therefore, the adoption of market-driven pharmaceutical GPOs will inevitably become a natural outcome as healthcare reform deepens.

Reforms in pharmaceutical procurement and supply cannot be advanced without the coordinated promotion of reforms in the medical insurance system and the healthcare delivery system, particularly given that public hospitals currently account for the majority of pharmaceutical consumption. At present, as China comprehensively deepens its reforms, supply-side structural reform has been established as the primary direction, a principle that equally applies to the reform of the medical and healthcare systems.

Although the supply-side reform in the pharmaceutical and healthcare sector involves reforms to the national administrative system, particularly in the areas of medical insurance administration and modern healthcare management systems, the Third Plenary Session of the 19th Central Committee of the Communist Party of China has clearly stated that direct government allocation of market resources and direct government intervention in market activities should be minimized.

Therefore, the healthcare and pharmaceutical system reform is poised to receive support from a framework aligned with the objectives of health fiscal allocation, volume, and effectiveness. This involves progressively transitioning to a model where commercially insured companies with professional qualifications are commissioned by the government to manage various medical insurance services through service procurement, thereby establishing payment mechanisms based on price negotiations and service purchasing between medical insurance agencies, healthcare providers, and pharmaceutical suppliers.

The establishment of payment standards for medicines covered by medical insurance is a central link in the pharmaceutical supply chain. As part of the supply-side reform in the healthcare sector, the formulation of these payment standards must be based on the fund’s affordability, the assurance of rational medication use for patients, and the healthy development of the pharmaceutical industry.

Moreover, the continuous adjustment and optimization of payment standards, particularly with the accelerated advancement of the national consistency evaluation for generic drugs, will normalize the practice of establishing drug payment standards based on generic names. Meanwhile, the medical insurance policy of bearing costs exceeding the budget while retaining surpluses will encourage various healthcare institutions to engage in consortium-based drug procurement to reduce purchasing costs.

Currently, many regions in China are undergoing integrated reforms of the drug tendering and bidding system and the mechanism for establishing medical insurance drug payment standards. Following the completion of its integration, Fujian Province has explicitly discontinued drug tendering and bidding, instead adopting a drug procurement and supply model based on medical insurance drug payment standards (using the generic name model). Under this approach, all medical institutions and retail pharmacies in Fujian settle payments uniformly according to the established payment standards. Guided by policies that hold entities accountable for overspending while allowing them to retain surpluses, these institutions and pharmacies are employing diverse strategies to reduce drug procurement costs, thereby enhancing drug-related revenues and institutional competitiveness.

Pharmaceutical Group Purchasing Organizations (GPOs) have undoubtedly become a significant option for medical institutions and retail pharmacies across Fujian Province. Consequently, there is an emerging and urgent market demand for GPO-based pharmaceutical procurement services, necessitating engagement with institutions that possess mature pharmaceutical GPO management systems. Meanwhile, regions such as Guangdong, Zhejiang, and Gansu are also advancing integration reforms to introduce payment standard reforms primarily based on generic drug names. Therefore, the advent of market-oriented pharmaceutical GPOs is imminent.

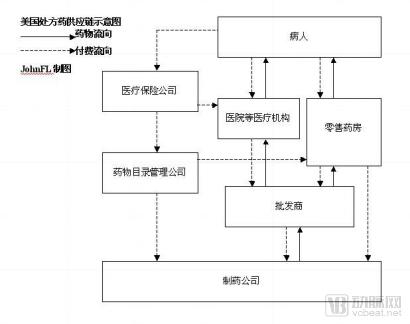

Implementation and Reference of U.S. Pharmaceutical GPOs

Unlike in China, the U.S. pharmaceutical market is primarily concentrated in the retail sector. Similar to healthcare institutions in the United States, the vast majority of retail pharmacies also adopt the Group Purchasing Organization (GPO) model for drug procurement; however, many organizations in China have focused exclusively on GPO purchasing within U.S. healthcare institutions.

Due to the strict implementation of tiered diagnosis and treatment systems in the United States, medication usage in U.S. healthcare institutions differs significantly from that in China. It primarily focuses on critically ill patients, complex and refractory diseases, and medical research. Most hospitals participate in procurement through two or more Group Purchasing Organization (GPO) service providers. Furthermore, these GPOs are typically established by participating hospitals or purely non-profit organizations. Such GPOs generally do not engage in the production or distribution of pharmaceuticals; instead, they provide only price negotiation and transaction services, generating revenue by charging transaction service fees or management fees to upstream pharmaceutical manufacturers.

Separation of prescribing and dispensing, tiered diagnosis and treatment, and control of the drug-to-revenue ratio are key components of China’s healthcare reform. As these reforms deepen, hospitals funded by social capital and retail pharmacies are poised for further development. Consequently, the Group Purchasing Organization (GPO) procurement model in the U.S. retail pharmaceutical market warrants close attention from many Chinese enterprises.

Pharmacy Benefit Management (PBM) companies in the United States offer services such as prescription review, chronic disease management, and payment administration; however, their primary revenue streams are derived from Group Purchasing Organization (GPO) services for retail pharmaceuticals, as well as mail-order and online pharmacy services. In 2016, for instance, the three largest specialized pharmaceutical retailers in the U.S. accounted for only half of the retail market share, yet nearly all pharmaceutical retailers adopted the GPO model. Therefore, studying the GPO services provided by U.S. PBM companies is more conducive to the development and application of GPOs in China and better aligns with China’s national conditions.

Source: A Detailed Explanation of the U.S. Healthcare Management System, by JOHNFL

U.S. Pharmacy Benefit Managers (PBMs), also known as formulary management companies, center their Group Purchasing Organization (GPO) procurement services on big data analytics of drug formularies. Grounded in health insurance reimbursement standards for pharmaceuticals, these PBMs leverage a suite of big data models—including drug formulary classification, dosage form grouping, quality stratification, price differential and ratio analysis, comprehensive drug selection, price collection, and group purchasing revenue simulation—to facilitate consolidated volume-based procurement for retail pharmacies while generating their own revenue. The operational scale of major U.S. PBM firms such as Express Scripts (ESI), CVS Health, and UnitedHealth Group exemplifies this business model.

U.S. Drug GPOs Offer Significant Insights for China’s Drug GPOs: Drug GPOs are the outcome of marketization. In contrast, most drug GPOs in China are led by government authorities rather than driven by hospitals’ own proactive market demands. Therefore, without market-oriented leadership, drug GPOs in China’s public hospitals remain fraught with uncertainty.

The reform of payment standards for medical insurance-covered drugs is a key factor in pharmaceutical GPO services, particularly the establishment of payment standards based primarily on generic drug names. With the deepening advancement of national administrative systems and healthcare reforms, pharmaceutical GPO is poised for significant development.

Beyond mere drug transaction services, formulary management capability is also a key competency in market-oriented GPO services for pharmaceuticals. Numerous domestic institutions aspiring to engage in pharmaceutical PBM and GPO businesses need to conduct in-depth research into the GPO services offered by U.S. PBM companies.

Author: Yingji Changkong, Renowned Pharmaceutical Consulting Expert