Medical Device Industry Poised for Merger and Acquisition Surge Amid Innovation Breakthroughs and Shifting Target Markets

GAREA

Mobile Medical Solutions Provider

In recent years, the Chinese government has strengthened regulation of the medical device sector through both regulatory oversight and innovation-driven policies, while promoting the domestication of medical devices. In 2017, a substantial number of new regulations and guidelines were introduced, covering multiple areas including accelerated approval processes, encouragement of medical device innovation, improvement of registration procedures, enhancement of clinical management, and advancement of technical capabilities. These measures aim to ensure the high quality and safety of medical devices in China, foster technological development in the industry, and completely move away from the previous reliance on low-end products for profit generation. We are benefiting from institutional dividends and simultaneously entering a fast track of development.

According toVCBeat (WeChat ID: vcbeat)According to incomplete statistics, there were 84 financing events in the medical device sector in 2017. This wave of capital primarily flowed into niche segments such as medical imaging, ultrasound equipment, medical robots, rehabilitation medicine, and home medical devices.

On March 10, 2018, the Future Healthcare: Medical Device Industry Transformation and Upgrading Forum was held at Hall 7 of the Century City New International Convention and Exhibition Center in Chengdu. The event was organized by VCBeat and VCBeat Research Institute, under the guidance of the Chengdu Municipal Health and Family Planning Commission, the Chengdu Municipal Economy and Information Technology Commission, the Chengdu Municipal Civil Affairs Bureau, the Sichuan Hospital Association, and the Sichuan Medical Device Industry Association.

During the morning session, four leading experts in the medical device industry delivered speeches and engaged in on-site discussions on topics including new trends in the development of the medical device industry, the application of disruptive innovative technologies, device-driven pathways within the new ecosystem of tiered diagnosis and treatment, and proactive health in the era of big data.

Guan Yan, Secretary-General of the Smart and Mobile Medical Branch of the China Association for Medical Devices Industry

China's medical device industry is experiencing rapid growth, and a wave of mergers and acquisitions will emerge in the next 5–10 years.

Guan Yan, Secretary-General of the Smart and Mobile Healthcare Branch of the China Medical Device Industry Association

Although the number of companies in the global medical device market is declining, the Chinese enterprise market continues to grow.

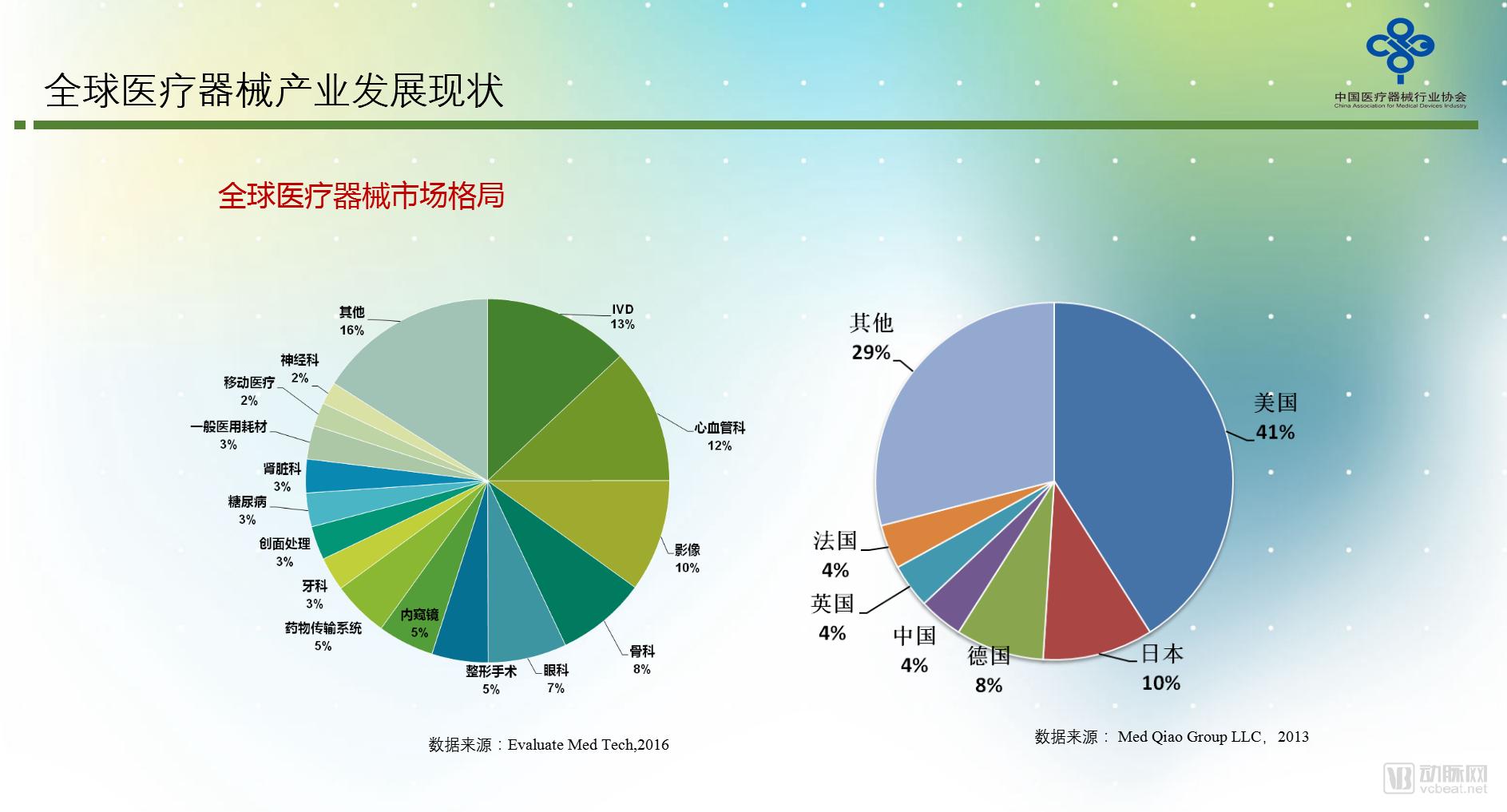

The global medical device market grew from $309 billion in 2009 to $371 billion in 2015, with a growth rate exceeding that of GDP during the same period. The compound annual growth rate averaged 5.2% between 2015 and 2022.

From a global perspective,The Largest Market Share Segment in In Vitro Diagnostics, accounting for approximately 13%, with a market size reaching $50 billion.Second is the cardiovascular field., accounting for 12%. Currently, the Chinese market is gradually aligning with the global market. The in vitro diagnostics (IVD) sector is experiencing a very high growth rate, and the cardiovascular field is also developing rapidly.

Data from 2013 shows that the United States accounted for 41% of the global medical device market, followed by Japan in second place and Germany in third. Currently, China holds the second position, making it the world’s second-largest medical device market.

In general,The global medical device industry maintains a relatively high growth rate of 5% to 6%.。

We have now entered the era of capital, where mergers and acquisitions are taking place. Biopharmaceutical companies are continuously entering the medical device industry, with frequent M&A and investment/financing activities in recent years. A decade ago, the medical device industry was characterized by small but elegant businesses; each operator was a small business owner, achieving annual sales of tens of millions of yuan and maintaining very high net profit margins. They thrived without the need for external investment.

At present, most enterprises aspire to scale up and strengthen their market position. Amid current emerging trends, the increasing regulatory pressure poses a challenge for companies worldwide.China's medical device market is seeing continuous regulatory improvements, yet the pressure on enterprises is actually increasing.

The national output value of the medical device industry for the latest year is announced every June. According to the 2016 data, the value-added of the pharmaceutical industry increased by 9.92% year-on-year in 2016. The Ministry of Industry and Information Technology defines enterprises with annual sales exceeding RMB 5 million as “enterprises above designated size.” After 2010, the threshold was raised to RMB 20 million. Therefore, this dataset actually covers only those medical device companies with annual sales above RMB 20 million, and thus does not truly reflect the overall situation of the industry.

Currently, there are over 2,000 pharmaceutical companies with annual sales of RMB 20 million. China has nearly 16,000 medical device companies; this figure represents only a portion, as the remaining 13,000 are very small enterprises.Industry associations estimated that the total output value of the entire industry exceeded RMB 550 billion in 2016.

Since 2010, China's medical device industry has experienced rapid growth, with an annual growth rate exceeding 15%.

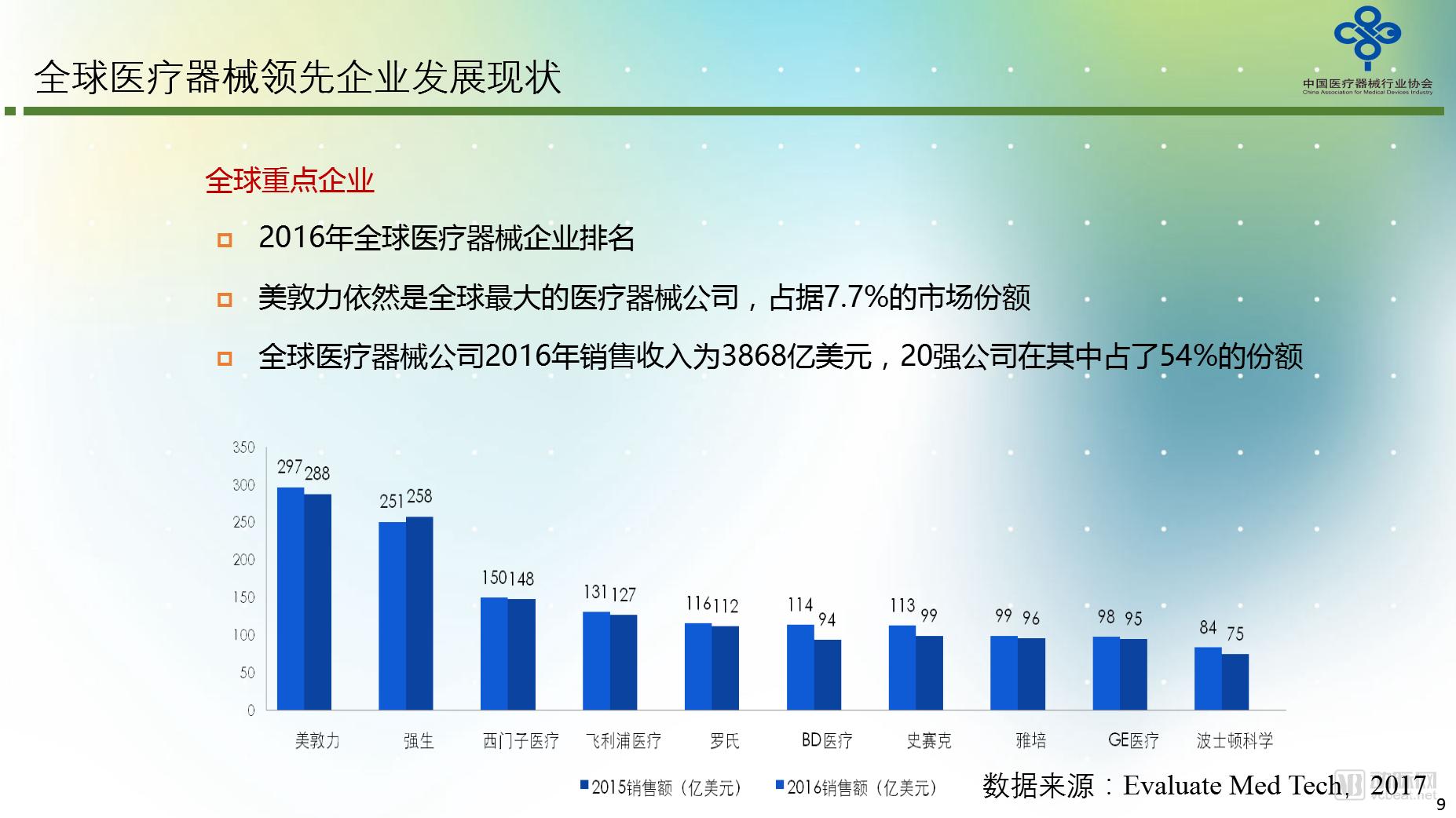

In contrast, international data reveals a very high level of concentration in this industry.Medtronic remains the world’s largest medical device company, holding a 7.7% market share. The global medical device industry generated $386.8 billion in sales revenue in 2016, with the top 20 companies accounting for 54% of that total.

It is predictable that in the next five to ten years, a large number of medical device companies will be acquired, and many enterprises may disappear due to intense competition. Of course, this also presents opportunities for the capital market and the entire industry.

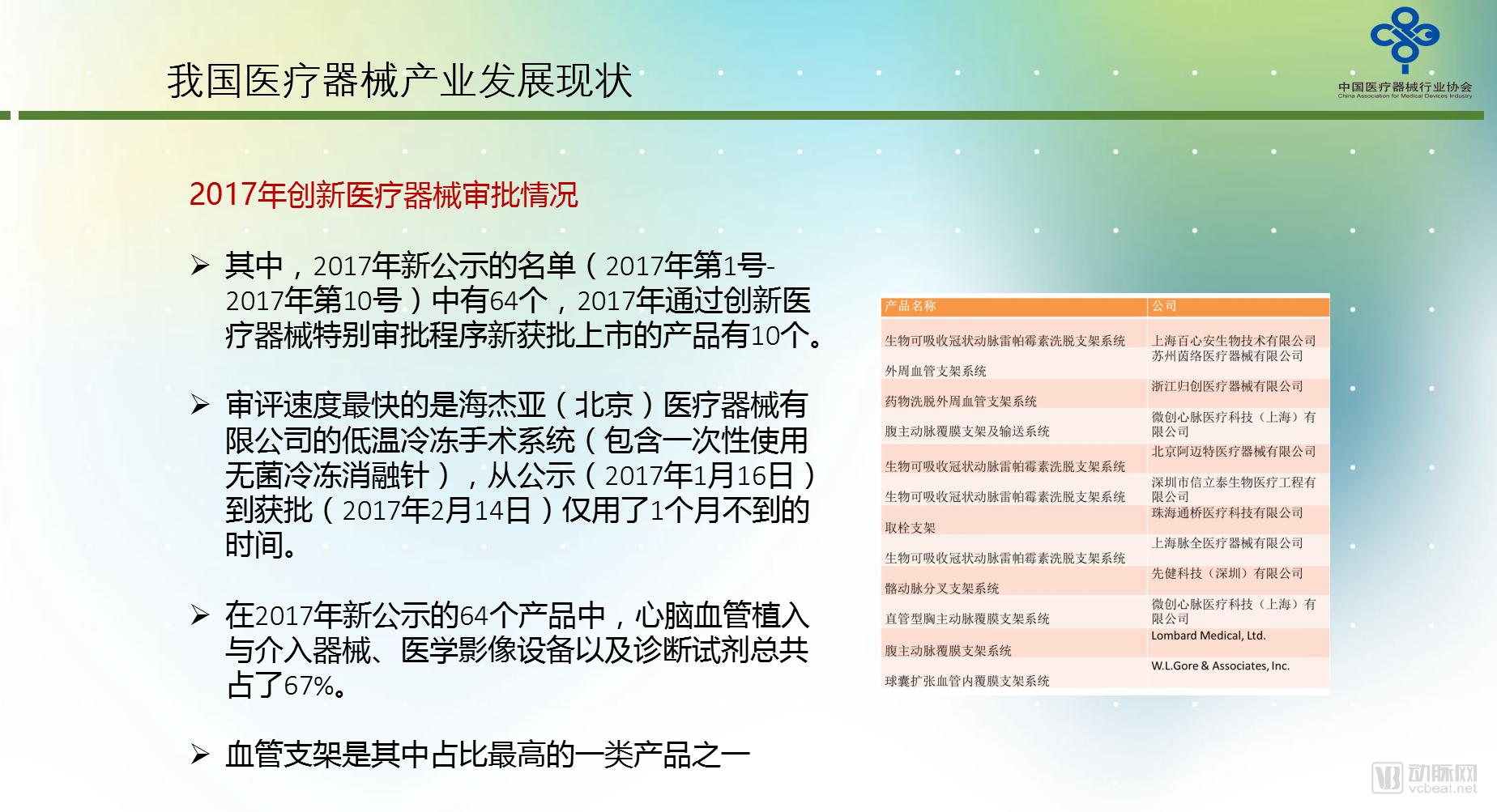

In 2014, the China Food and Drug Administration issued the Special Examination and Approval Procedures for Innovative Medical Devices (Trial), featuring a streamlined approval process.First, it possesses core product technologies and invention patents in China; second, its product performance and safety are improved compared to similar products; third, it has reached an internationally leading level; and fourth, it demonstrates clinical application value."In principle, this applies more to Class III medical devices; however, provinces such as Jiangsu and Shanghai have also established innovation pathways for Class II devices."

However, obtaining approval through the Green Channel does not mean that certification can be obtained immediately; clinical evaluations and inspections are still required. The only difference is that there is no need to wait in line. According to the 2017 approval data, the 64 products announced in 2017 took approximately one month to obtain certification.Cardiovascular and cerebrovascular products accounted for 67%, with vascular stents being the product category with the highest share.In 2017, 12 vascular stents were approved through the fast-track channel.

Co-founder of Anhan Medical, Huan Dandan

What is the Approach to Technological Innovation at Anhan Medical?

Huan Dandan, Co-founder of Anhan Medical

First, let us review our overall technical approach, with the capsule gastric robot as the central theme. In his book The Innovator’s Dilemma, management guru Clayton M. Christensen argues thatSome once-perfect business moves—precisely investing in and conducting R&D for products that meet mainstream customer needs and deliver the strongest profitability—may well destroy an excellent company.

For instance, in the hard disk drive market, corporate iteration does not depend on conventional metrics such as capacity, cost, and access speed—improvements in these incremental performance areas—but rather on the physical size of the drives themselves. This leads to the conclusion that certain breakthrough technologies gradually evolve into disruptive innovations that dominate new markets.

Anhan’s capsule gastroscopy for precise gastric examination exemplifies the typical characteristics of innovation. As an original, disruptive innovation with fully independent intellectual property rights in China, it was featured in the Five-Year Achievements Exhibition. It is a great honor to showcase our nation’s independent innovation achievements alongside high-speed rail.

There are three main reasons for developing such a product:

First, the situation of gastrointestinal health in China is very severe. Among the top five digestive cancers in China, except for lung cancer, the others are all gastric cancer;

Second, awareness of gastric health is generally weak, and the discomfort associated with electronic gastroscopy is difficult to tolerate.

Third, China’s medical resources face bottlenecks and are far from meeting the population’s needs for universal healthcare access. The low screening rate for digestive diseases in China has contributed to persistently high incidence rates. Moreover, there are only 26,203 physicians in China qualified to perform gastrointestinal endoscopy, which is insufficient to meet the demand for universal health screenings.

Our capsule robot can perform precise movements in millimeters under the control of a control device, rotate according to the doctor's instructions, and provide an accurate and comprehensive view of the stomach.

This capsule contains over 300 internal components, representing a multidisciplinary integration. It is a product with fully independent intellectual property rights, holding more than 100 patents domestically and internationally. The examination is performed simply by swallowing the capsule with water. The procedure takes only 15 minutes to complete, after which the capsule is naturally excreted from the body. It poses no risks, eliminates the risk of cross-infection, and provides comprehensive 360-degree visualization without blind spots.

In 2013, Anhan Medical’s capsule gastroscopy robot received the CFDA Class III medical device registration certificate and was launched on the market.

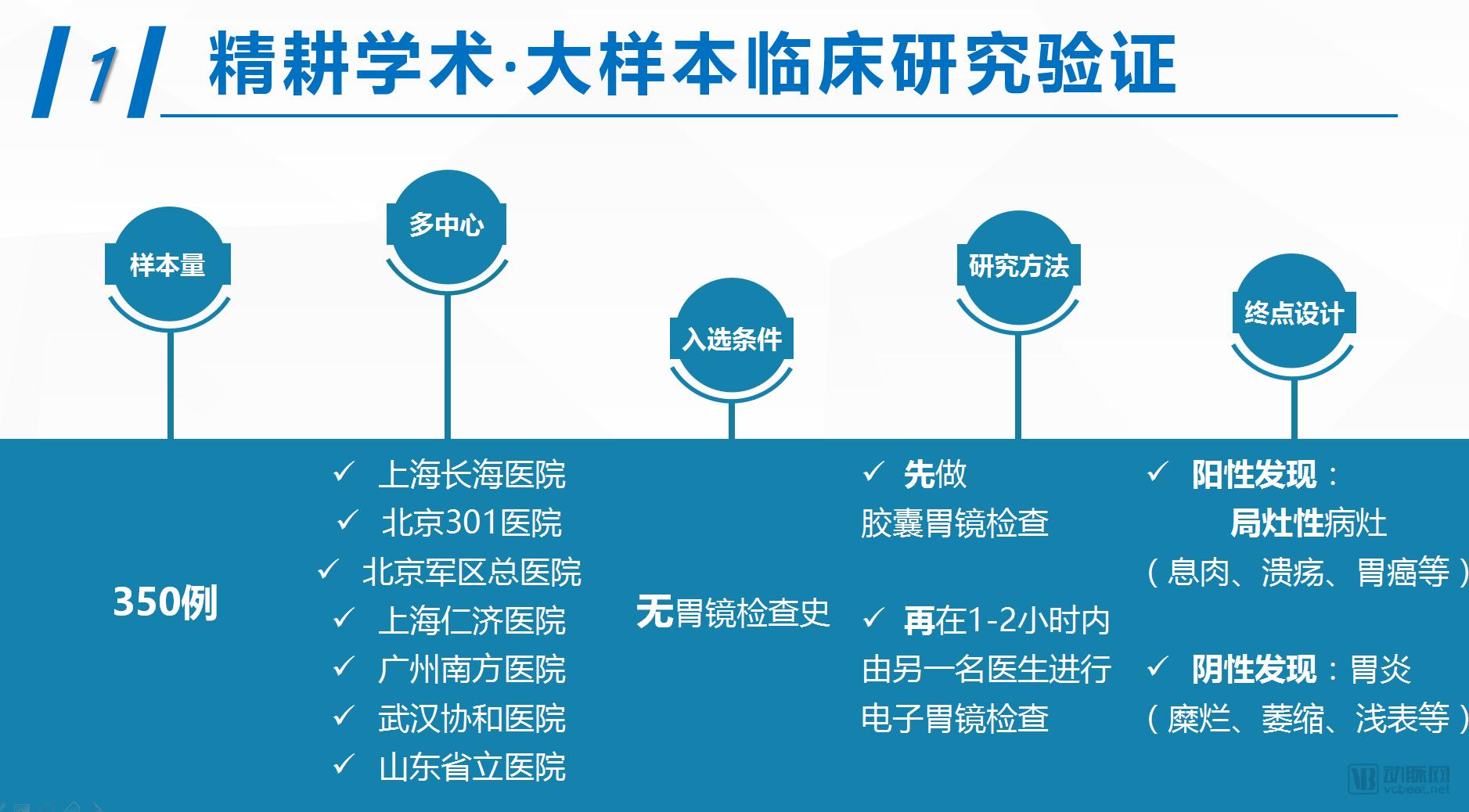

Based on large-sample, multi-center studies conducted at Shanghai Changhai Hospital, Beijing 301 Hospital, the General Hospital of the Beijing Military Region, and Shanghai Renji Hospital, the diagnostic accuracy of capsule gastroscopy was found to be 93.4% when compared with conventional gastroscopy.

High-risk medical devices necessitate reliance on specialized physicians, making them highly suitable for promotion within health checkup institutions. We analyzed data from health screenings conducted at several public Grade 3A hospitals in Shanghai between March and August 2016. The study included 4,688 asymptomatic individuals undergoing routine health examinations, with a mean age of 47 years; 62% were male and 38% were female. Strikingly, typical pathological lesions were identified in 24.6% of these ostensibly healthy, symptom-free participants. Furthermore, the detection rate for gastric cancer reached 6.3 per 1,000 individuals.

Since its market launch, the product has been deployed in nearly 1,000 medical institutions across 29 provinces and municipalities in China, including renowned centers such as Peking Union Medical College Hospital, the PLA General Hospital (301), and Meinian Onehealth. It has also expanded overseas, with adoption in countries including the United Kingdom, Germany, and other European nations. Our innovation has thus shifted from imitation to leadership; rather than being educated by foreign entities on the Chinese market, we are now leading international education.

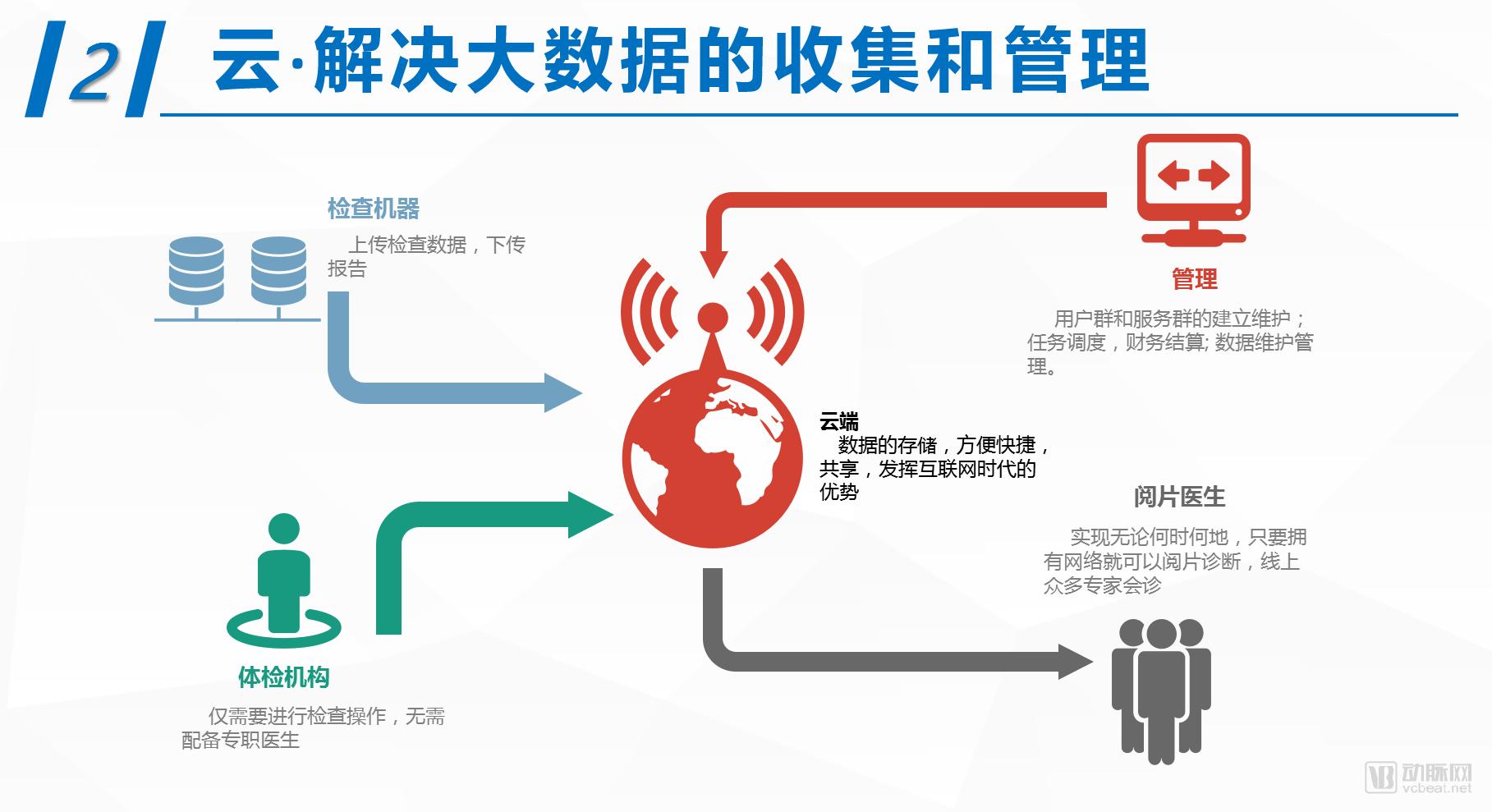

We also hope to expand it through cloud platforms and artificial intelligence.

The Internet is the most efficient means for data transmission and sharing. Anhan has established its own cloud platform, uploading all examination data to the cloud. Our physicians can access and review images anytime via the cloud platform as long as they have an internet connection, facilitating online consultations with a broader pool of specialist resources and transforming patient data into flowing data assets.

Our community hospitals, physical examination centers, prefecture- and county-level hospitals, tertiary Grade A hospitals, and international medical institutions have all been integrated into this cloud platform, addressing the imbalance in medical resource distribution. If local prefecture- or county-level hospitals or physical examination centers lack certain diagnostic resources, we can share examinations and data by simply uploading them to the cloud. Physicians from tertiary Grade A hospitals or international hospitals can then issue reports, providing remote support and pioneering a new model for gastrointestinal examinations.

Wei Xing, Sales Director at GAREA Medical

New Opportunities for Medical Devices Emerge Amid the Development of Medical Consortia, Family Doctor Contract Services, and Integrated Medical and Elderly Care Systems

Wei Xing, Sales Director of Garea Medical

Apart from Grade A tertiary hospitals, all other healthcare facilities are referred to as the grassroots out-of-hospital market. The current strategic pathway focuses on three key initiatives: establishing medical consortia, implementing family doctor contract services, and integrating medical care with elderly care. These three pillars constitute the healthcare reform agenda outlined at the 18th National Congress of the Communist Party of China: first, build medical consortia; second, develop family doctor services to serve as health gatekeepers; ultimately, these measures aim to reduce societal operational costs and address the challenges of an aging population.

In the tiered diagnosis and treatment system, it is still most common for Grade A tertiary hospitals to take the lead in establishing medical consortiums. However, the current state of this mechanism is characterized by “physical integration without genuine cohesion.”Medical institutions can be upgraded from secondary to tertiary hospitals, but how can tertiary hospitals be downgraded to secondary ones? We have broken down information silos through informatization.Once this channel is established, many of our innovative products can reach primary care institutions from hospitals, and data can be transmitted back to hospitals from the grassroots level.

GAREA Healthcare’s partnerships across China cover a substantial number of leading regional enterprises, with estimated collaboration scales ranging from RMB 20 million to over RMB 100 million. These companies are increasingly grappling with the pressing need to identify strategic pathways for breakthrough growth.Many medical devices have a limited market when used in hospitals, but once deployed to primary care facilities in alignment with policy directives, they effectively gain the support of all local grassroots healthcare providers.With primary care physicians prescribing and diagnosing, business volume increases, which naturally drives the use of medical devices and consumables.However, a critical prerequisite for entering the primary care market is inclusion in the national medical insurance reimbursement list.

We previously believed that it was impossible for medical device manufacturers to participate in the construction of healthcare systems. However, we are now collaborating with certain regions and local partners to engage in building county-level healthcare systems, encompassing counties, towns, and townships. This includes the initiative of decentralizing medical resources, which has created opportunities for enterprises. Companies can evolve into service providers supplying solutions for healthcare system construction at the county level, thereby enhancing their influence locally and effectively establishing a monopolistic position in the market.

Furthermore, community-level medical institutions represent a more significant tier. Both community physicians and residents possess strong health awareness and substantial purchasing power, leading to high consumption of medical devices for testing at these grassroots healthcare facilities.

GAREA has been engaged in marketing for two years and has observed several shifts in the strategic directions of our partners:

First, the traditional hospital system: whereas we were previously regarded as a trading vendor, we are now recognized for our participation in the construction of hospital systems. By engaging in the development of new markets, our revenue model has shifted from sales-based profits to service-based income.

Second is the shift in target markets. Previously, medical device manufacturers, including those producing consumables and pharmaceuticals, primarily served hospitals. Since most medical institutions are located at the primary care level, companies historically focused on Tier-3 Grade-A hospitals due to their higher profit margins. Today, as the hospital system has become largely well-established, adopting the same approach in the primary care market—characterized by numerous scattered sites, broad coverage, and the goal of universal access—is no longer cost-effective. It is not feasible for individual enterprises to operate independently in this segment. Instead, medical device companies should engage in household contracting and align with the development of Medical Consortiums (Yi Lian Ti). This strategy reveals an alternative channel that can be leveraged to reach every primary care institution directly.

Third, GAREA’s shift from serving hospitals to serving the entire Health and Family Planning Commission—effectively serving the whole community and all residents—has naturally led to changes in its business model and marketing approach due to the change in target market, thereby creating new opportunities.

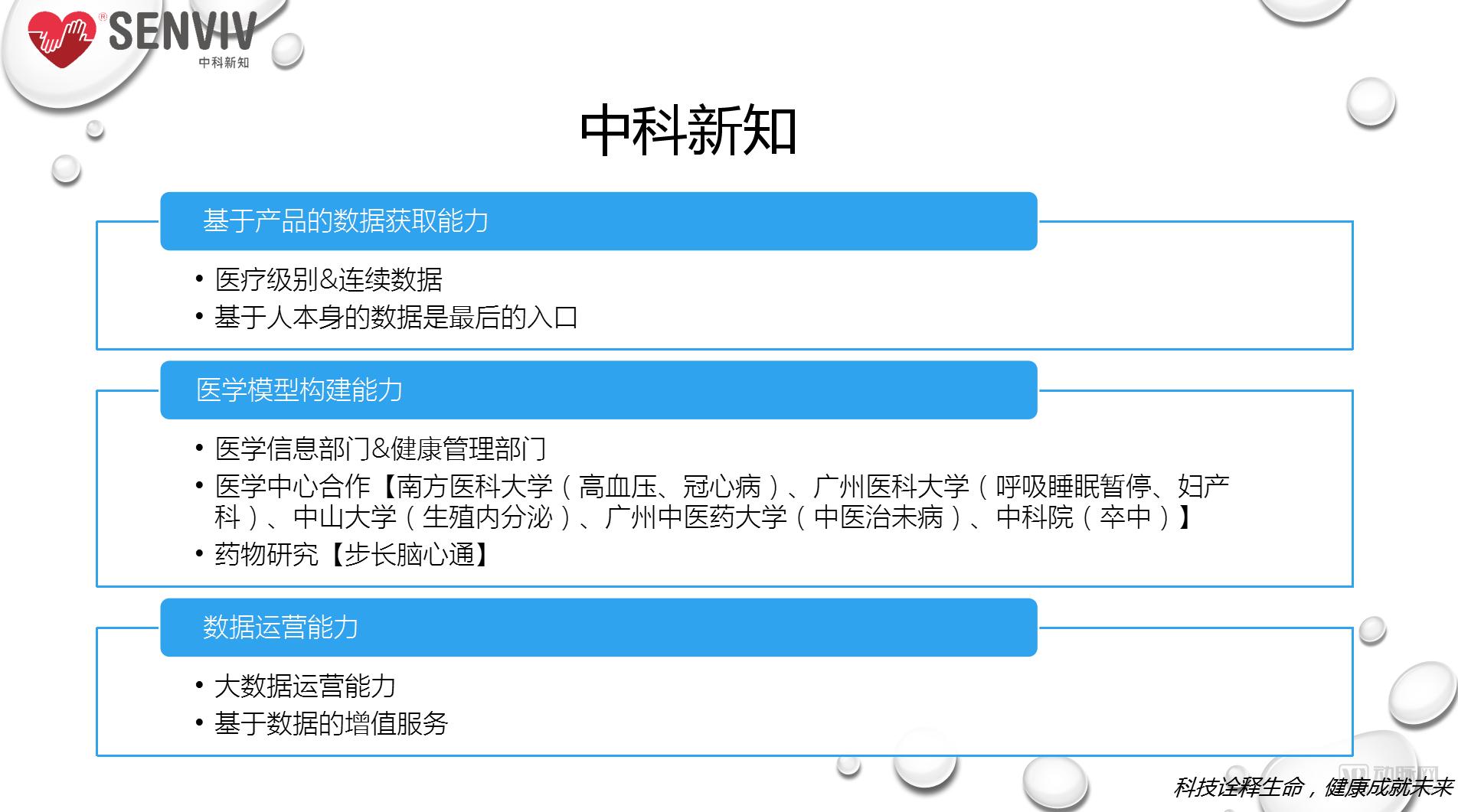

Co-founder of Zhongke Xinzhi, Cui Caimei

How Data Is Changing Human Cognition?

"Proactive Health" is a concept I quote from President Xi Jinping, who explicitly stated at the National Conference on Hygiene and Health in August 2016 that the focus must shift from disease treatment to people’s health, with attention paid to the entire life cycle and the full process of health management.

From our perspective, proactive health encompasses elements at both the technological and even the scenario-based levels. First, there is the transition from standardization to personalization. In traditional medical practice or evidence-based medicine, we rely on standardized reference values or criteria to guide all our work.

Driven by the demand for proactive health, our data applications have become more diversified. First, we also require standardized population data. As we currently engage in big data analytics, how many individuals do we need to include?

As Professor Guan just mentioned, while we deploy 1,000 personnel for Class III medical devices, the same number of people in big data represents merely a single unit; in reality, it may require hundreds of thousands or even millions of individuals to establish more robust standards.

Zhongke Xinzhi has established a public model based on standardized data from such populations. Starting from our own data, we can categorize individuals into at least hundreds of trillions of distinct states. As individuals may transition between these states from day to day or even within different time periods, we focus on the phased changes associated with their transitions from one state to another.

Zhongke Xinzhi monitors an individual’s physiological signs throughout the night. Over a period of seven to eight hours, we collect more than 600 MB of data. The accumulation of such personal data constitutes a valuable asset that can accurately reflect your health conditions.

In light of this trend,"We believe that only through precise, continuous, and non-intrusive monitoring can true personalization be achieved; this is fundamental to our technology."

What Zhongke Xinzhi can currently do falls into two categories: artificial intelligence and sensing technology. Sensing technology serves as the source of data acquisition. We position ourselves as a data company. Why does a data company need to develop its own hardware and sensors? Because if we want to obtain the specific data we desire, we must develop it ourselves. Currently, there is no device available worldwide that can provide us with the ideal data, which is why we are developing our own sensing technology.