Jack Ma Strikes Again: iKang Healthcare's Privatization Finalized as Alibaba Builds Its Healthcare Empire

AliHealth

Medical and Health Services Network Service Provider

On the evening of yesterday (March 12), Ikang Guobin, a leading private health checkup provider, announced that it had received an acquisition proposal from Yunfeng Capital and Alibaba. The proposed acquisition price is $20 per ADS (American Depositary Share) or $40 per share.

Following the announcement, Ikang Guobin’s U.S. shares rose more than 11% in pre-market trading, currently quoted at $19.94. The company closed at $17.92 last Friday, implying a premium of approximately 11.6%.

As early as 2016, news emerged that Ikang Guobin had received a privatization proposal letter from Yunfeng Capital. At the time, Ikang Guobin’s M&A journey was fraught with challenges, culminating in Alibaba’s intervention in its acquisition battle with Meinian Onehealth. Now, two years later, what does Yunfeng Capital’s renewed move signify? VCBeat (WeChat ID: vcbeat) offers an analysis.

Ikang Guobin's Path to Privatization

As is well known, in the private health checkup market, which accounts for only 7.5% of the total share, three major players—Ikang Guobin, Meinian Onehealth, and Ciming Health Checkup—had long dominated the landscape. Following Meinian Onehealth’s acquisition of Ciming Health Checkup in 2017, the private health checkup sector entered an era of duopoly.

Between 2015 and 2016, the privatization battle between Ikang Guobin and Meinian Onehealth lasted for nearly seven months. As news emerged on March 12 that Yunfeng Capital had acquired Ikang Guobin, we first take a look back at Ikang Guobin’s path to privatization.

On March 4, 2014, Ikang Guobin filed an IPO application with the U.S. Securities and Exchange Commission (SEC), planning to list on the NASDAQ Global Select Market with a maximum fundraising of $150 million.

On the evening of April 9, 2014, Ikang Guobin officially listed on the NASDAQ in the United States, with the stock ticker symbol KANG.

In August 2015, Zhang Ligang, Chairman and CEO of Ikang Guobin, along with related private equity funds, initiated a privatization offer at a price of $17.8 per ADS, corresponding to a market capitalization of $1.165 billion.

Two months later, Meinian Onehealth Healthcare, through its shell company Jiangsu Sanyou, announced the formation of a buyer consortium with Ping An, Sequoia Capital, Cathay Capital Private Equity, and other firms. The consortium submitted a privatization proposal to the board of directors and its special committee of Ikang Guobin, initially offering US$22 per American Depositary Share (ADS). The offer was subsequently raised twice, reaching US$25 per ADS. The proposal involved an all-cash acquisition of all outstanding Class A ordinary shares, Class C ordinary shares, and American Depositary Shares of Ikang Guobin, countering the privatization offer put forward by Zhang Ligang in late August.

In December 2015, Ikang Guobin launched a “poison pill” plan to block the acquisition by Jiangsu Sanyou, preventing Jiangsu Sanyou from acquiring or purchasing Ikang Guobin’s shares on the secondary market, while simultaneously introducing powerful partners such as Yunfeng Capital and China Life Insurance as strategic backers.

In June 2016, Ikang Guobin announced that the company had received a privatization proposal letter from Yunfeng Capital, which intended to acquire all outstanding shares of Ikang Guobin at a price of $20 to $25 per share.

That month, Zhang Ligang and Meinian Onehealth announced the withdrawal of their privatization offers in succession, and China Life Insurance also withdrew from the bidding war. Yunfeng Capital became the sole bidder for the privatization of Ikang Guobin.

The nearly seven-month-long conflict has temporarily come to an end with Alibaba’s intervention. Media outlets have pointed out that following Yunfeng Capital’s entry, Jack Ma can integrate Ikang Guobin into his AliHealth industrial chain, thereby strengthening Ikang Guobin’s footprint in the healthcare sector. It is precisely this ability to balance the interests of both parties that prompted Zhang Ligang and Meinian Onehealth to make mutual concessions.

How has Ikang Guobin developed in recent years?

As shown in the table, although Ikang Guobin’s overall revenue has been on an upward trend in recent years, its growth rate has declined year by year.

As of March 31, 2017, Ikang Guobin’s fiscal year 2016 report showed full-year revenue of $435 million, nearly RMB 3 billion, representing a 17.5% year-on-year increase compared to the same period in 2015.

Revenues in 2015 and 2014 were RMB 370 million and RMB 290 million, respectively, representing a year-on-year growth of 27% in 2015 and 45% in 2014.

In terms of gross profit, Ikang Guobin’s gross profit in 2016 was $170 million, representing a year-on-year increase of 8.6%. While both total revenue and gross profit grew year by year, the company’s gross profit margin continued to decline.

Furthermore, among the data from the past four years, Ikang Guobin incurred a loss of RMB 11 million in 2016. According to the table, the loss was primarily attributable to increased operating expenses, higher total costs, and a decline in gross profit margin.

In 2016, Ikang Guobin entered a period of rapid expansion, with its number of clinics increasing from 73 to 90 in the first quarter alone. Its management remained committed to executing a dual-expansion strategy: continuing to build its own network while also expanding through acquisitions and investments (in health examination centers), resulting in cash outflows exceeding inflows.

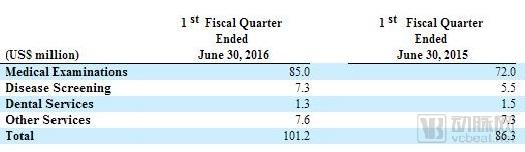

Ikang Guobin Q1 2016 Financial Report (Source: SEC.gov)

Ikang Guobin is primarily positioned in the mid-to-high-end market, providing corporate clients with health checkups, disease screening, dental services, and more. It is a direct competitor to Meizhao Health Checkup and Ciming Health Checkup, both under Meinian Onehealth.

State-owned enterprises, government agencies, and private companies account for 80% of Ikang Guobin’s current revenue. Data from the first quarter of 2016 indicates that its disease screening services targeting high-end clients are on an upward trend.

In recent years, Ikang Guobin has not been content with its traditional health examination business, but has made its own explorations in internet healthcare, disease screening, and artificial intelligence.

In 2015, Ikang Guobin launched the Daoyitong APP and Tijianbao APP. It explored a service model that integrates IT technology with traditional medical services, aiming to strengthen its presence in the internet healthcare sector.

“Daoyitong” is an independent company, with Zhang Ligang personally holding a 20% equity stake, Ikang Guobin holding 70%, and the management team holding 10%. “Ikang Tijiianbao” is an upgraded application product developed by Ikang Guobin over five years, evolving from a PC-based platform to a mobile app. This app enables users to rapidly generate personalized health examination plans by completing questionnaires covering family genetic history, past medical history, lifestyle, and other relevant information within the “Tijiianbao” platform.

Ikang Guobin aims to leverage its mobile health platform as an entry point to integrate a wide range of preventive and medical services—including health check-ups, disease screening, dental care, private physician services, expatriate medical support, anti-aging treatments, and vaccinations—thereby establishing a comprehensive health management platform.

In addition to exploring the various possibilities of integrating internet-based healthcare with traditional physical examinations, Ikang Guobin has also intensified its efforts in precision health management over the past year. At Ikang Group’s strategic upgrade press conference held on June 23, 2017, the group innovatively introduced the concept of “managed” physical examinations, along with the iKangCare+ and iKangPartners+ programs.

By integrating DNA testing technologies, Ikang has upgraded its health checkup packages to offer the “Ikang Anti-Cancer Trio.” For early screening of gastric and colorectal cancers, Ikang’s “Gastrointestinal Care” introduces China’s first fecal Helicobacter pylori genotyping test, along with fecal DNA testing for early colorectal cancer screening. For early lung cancer screening—addressing the most prevalent cancer in China—Ikang’s “Lung Protection” includes liquid biopsy capable of detecting ultra-early-stage lung cancer, low-dose computed tomography (CT) of the lungs, and genetic testing. For more comprehensive early cancer screening and disease risk assessment, Ikang’s “Jun Kang Bao” features a full panel of genetic tests (197 items for men and 202 items for women), liquid biopsies for 18 high-incidence cancers, and lung CT scans.

Furthermore, on August 1, 2017, Ikang Group and Baiyang Pharmaceutical Group jointly announced that they would collaborate to establish IBM Watson for Oncology consultation centers at 108 health examination and medical centers under the Ikang Group by introducing the IBM Watson for Oncology cognitive computing solution.

All of these explorations demonstrate Ikang Guobin’s determination to expand beyond its traditional health checkup business and develop in the field of precision prevention.

Yunfeng Capital’s acquisition of Ikang Guobin is driven not only by the value of its offline network of over 100 clinics, but also by the strategic imperative to capture the traffic gateway represented by its corporate client base, which accounts for 80% of its customers.

In the current landscape, after two years of relative quiet, Ikang Guobin has returned to the spotlight. The rivalry is no longer just between Ikang Guobin and Meinian Onehealth; it may well evolve into a contest between Alibaba and Tencent. After all, in the internet sector, no company can afford to bypass either Alibaba or Tencent. Competition for offline entry points has become a key strategic focus for both tech giants in recent years, particularly in targeting B-end users and expanding into new retail.

What is Alibaba seizing in the offline market?

The offline entry points currently contested by Alibaba and Tencent in the new retail sector are also embroiled in fierce competition. The two giants are leveraging capital ties to accelerate their land-grab strategies in new retail, injecting both financial resources and technological capabilities into the previously fragmented regional offline retail market.

Examining the trajectory of Alibaba, the earliest proponent of New Retail: it began acquiring stakes in Intime Department Store in 2014; partnered with Suning in 2015; launched Hema Fresh and acquired a stake in Sanjiang Shopping Club in 2016; and in 2017, privatized Intime, acquired stakes in Lianhua Supermarket and Yiguo Shengxian, invested in Xinhua Du, and pioneered new retail formats such as unmanned stores and pop-up shops. Meanwhile, Alibaba accelerated the development of its foundational logistics infrastructure by establishing Cainiao Network and investing in express delivery companies including YTO Express, Best Inc., RRS Logistics, and Sudiyi, thereby enhancing the velocity of product circulation.

In February 2018, Alibaba Group announced the signing of a strategic investment agreement with Easyhome Group, investing RMB 5.453 billion to acquire a 15.0% stake in Easyhome. This move was aimed at leveraging Easyhome’s resources across its 223 offline stores nationwide. Based on its previous layout, Alibaba’s offline resources have become relatively solid.

Nor has Tencent shown any weakness, as it firmly seized the opportunities presented by new retail. In 2017, Tencent successively invested in Missfresh, Meituan-Dianping, Yonghui Superstores, JD.com, Super Species, and Vipshop, among other retail and e-commerce ventures. In 2018, it further invested in Carrefour, Wanda Commercial, and Heilan Home, while also increasing its stake in JD.com.

Following reports that Yunfeng Capital plans to acquire Ikang Guobin, some sources suggest that Ikang Guobin’s network of over 100 health examination centers across more than 30 cities represents Alibaba’s initial move into offline medical entities.

In the era of oligopoly, the emergence of new internet industries or new IPs ultimately seems to boil down to a rivalry between two giants: Alibaba and Tencent. Whether in the realm of new retail or healthcare, any move by either company draws widespread attention from the industry.

Over the past year, rumors have been rife about “Ma Huateng planning to open hospitals” and “Jack Ma investing in shared clinics in Hangzhou.” However, apart from their strategic layouts in the internet healthcare sector, both companies have made relatively little noise in the offline space. Tencent has only invested in one physical entity, Penguin Doctor. Although Wang Shirui, CEO of Penguin Doctor, has expressed grand ambitions to open 100 shared clinics across China, the project is still in its early stages and cannot yet be compared with the scale of Ikang Guobin Health Physical Examination Management Group Co., Ltd.

Looking again at Alibaba’s strategic layout in the healthcare sector, three lines of business stand out as particularly significant:

AliHealth is Alibaba’s flagship business in the internet healthcare sector and represents its largest investment and acquisition to date in this field.

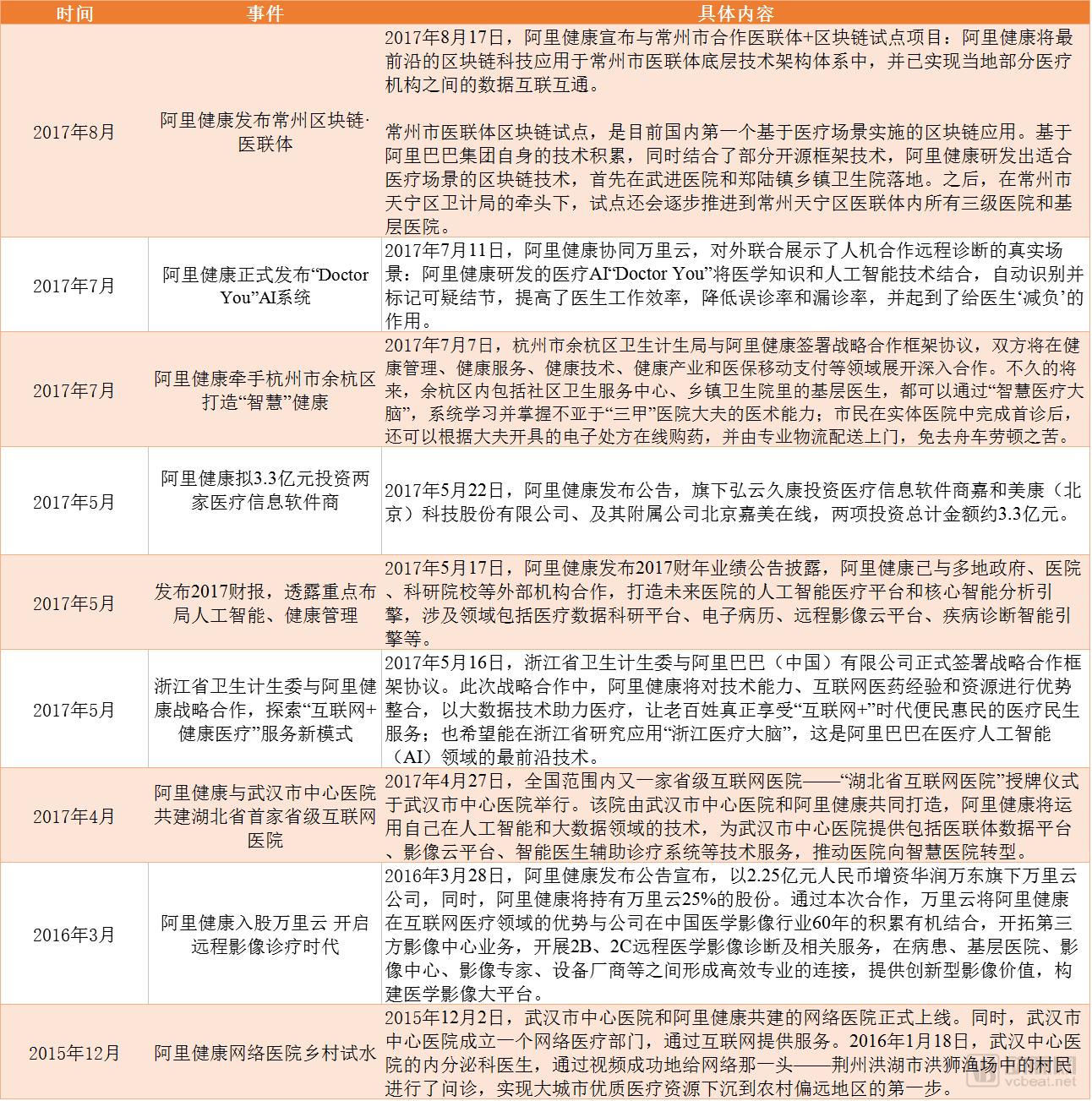

Over the past year, Alibaba’s initiatives in the healthcare sector have been widely recognized. As a flagship healthcare platform under Alibaba Group, AliHealth’s developments have drawn particular attention within the internet healthcare industry.

VCBeat had previously compiled a timeline of AliHealth’s major milestones in smart healthcare in 2017:

AliHealth has become a key strategic initiative for Alibaba in exploring the fields of pharmaceutical O2O, AI, prescription outflow, and informatization. Over the three years since its establishment, AliHealth has gradually adjusted its business model, ultimately forming stable business lines in pharmaceutical e-commerce, smart healthcare, product traceability, and health management.

In addition to smart healthcare supported by technologies such as artificial intelligence and big data, future hospitals centered around payment scenarios are also part of Jack Ma’s healthcare blueprint.

On May 28, 2014, Alipay Wallet officially announced the launch of its “Future Hospital” initiative. Under this plan, Alipay Wallet will open up its platform capabilities to healthcare institutions in the future, including its account system, mobile platform, payment and financial solutions, cloud computing capabilities, and big data platform, with the aim of helping hospitals become more efficient in the era of mobile internet.

Alipay will also provide technical support within hospitals, including free Wi-Fi services and indoor navigation, to guide users to locations for medical consultations, examinations, payment, and medication pickup. Reportedly, this is a long-term plan spanning five to ten years.

As of May 2017, more than 1,500 public hospitals had joined Alipay’s “Future Hospital” initiative, covering 30 provinces, autonomous regions, and municipalities across China, as well as nearly 200 cities. The platform had provided over 300 million instances of convenient services—such as real-name appointment registration, mobile payments, and medical report inquiries—via Alipay. Additionally, more than 80,000 pharmacies supported Alipay payments.

The "Future Hospital" has always been an idealized healthcare model in Jack Ma’s vision. Alibaba aims to realize the scenarios of the Future Hospital built around Alipay through a three-phase approach:

Phase I: Assisting Hospitals in Establishing Mobile Healthcare Services

By leveraging Alipay’s mobile platform capabilities, payment and financial solutions, and data analytics, and partnering with various Independent Software Vendors (ISVs), we collaborate with hospitals to build patient-centric smart healthcare platforms. These platforms enable end-to-end mobile healthcare services—from appointment registration, waiting, in-hospital navigation, and payment, to report retrieval and doctor-patient interaction—thereby enhancing the patient experience.

Phase II: Activating the Full Healthcare Ecosystem Services

In conjunction with the advancement of healthcare reform, all processes—including online electronic prescriptions, localized medication delivery, patient referrals, real-time medical insurance reimbursement, and instant commercial insurance claims—are completed via the internet, thereby revitalizing the entire social healthcare ecosystem.

Phase III: Co-building a Big Data-Based Health Management Platform to Enable the Shift from Treatment to Prevention

By opening up its big data platform and leveraging cloud computing capabilities, we collaborate with wearable device manufacturers, healthcare institutions, government health departments, and other partners to jointly build a big data-driven health management platform, facilitating a shift from treatment to prevention.

Some Companies Invested in by Yunfeng Capital in Recent Years (Data Source: VCBeat Knowledge Base)

Since its establishment in 2010, Yunfeng Capital has achieved remarkable results in investment and acquisitions within the healthcare sector.

In addition to the companies involved in investments and mergers and acquisitions listed in the table, Alibaba has partnered with Yuwell Medical in the field of smart mobile medical devices, taken an equity stake in China Resources Wandong in the medical imaging sector, and entered into a strategic cooperation with Dian Diagnostics in the health examination and testing sector.

According to our statistics, Alibaba’s footprint now spans multiple healthcare sectors, including smart medical devices, pharmaceutical O2O services, hospitals, and health management.

For health management enterprises, especially physical examination companies that serve as entry points, the hundreds of millions of health big data records they hold will undoubtedly bring immeasurable value to medical services and technological development. The selection of Ikang Guobin Health Physical Examination Management Group Co., Ltd. as the acquisition target precisely reflects Alibaba’s emphasis on this critical entry point into health management.

Similar to Alibaba Group’s investments in logistics, finance, retail, and mobility—sectors that permeate various aspects of daily life—the acquisition of Ikang Guobin signals that Alibaba may be moving toward establishing a closed-loop healthcare ecosystem. By integrating preventive medicine (pre-diagnosis), future hospitals and smart healthcare solutions (during diagnosis), and pharmaceutical services, Alibaba aims to build its own comprehensive medical ecosystem.

Based on the proposals from last week’s Two Sessions, Ma Huateng’s focus remains on digital technology. (See details:Ma Huateng’s Medical Proposal at the Two Sessions Becomes Increasingly “Tech-Focused”: A Look into Tencent’s 2018 Healthcare Strategy)

Thus, judging from AliHealth’s recent moves, Alibaba has also made significant strides in AI, healthcare informatization, and internet-based medical services. With this foray into offline physical entities, Alibaba’s accumulated online service capabilities and information technology expertise are poised to extend to the offline realm. Meanwhile, Ikang Guobin’s network of over 100 stores serves as Alibaba’s key offline entry point into the healthcare sector and a crucial channel for expanding its B-end user base.

For Tencent, which has not yet made significant inroads into the physical sector, some media outlets have commented that Alibaba’s move effectively “kicks the ball to Tencent.”

How will Tencent respond? Will Alibaba encounter management issues inherent in the operation of physical medical institutions? Time will tell.