China's Medical Unicorns Poised for IPO Fast Track Amid Capital Market Reforms

Ping An Healthcare

One-stop Solution Provider for Health Management

"Fragrant tidings arrive; the apricot tips turn red."

This spring, the news that A-shares are embracing “unicorns” has undoubtedly brought a wave of warmth to innovative enterprises and the capital market.

To support the listing and financing of high-quality innovative enterprises, and to attract “BATJ” companies already listed overseas to return to the A-share capital market, the China Securities Regulatory Commission (CSRC), the Shanghai Stock Exchange (SSE), and the Shenzhen Stock Exchange (SZSE) have taken proactive measures. By drawing on international capital market experience, reforming listing regulations, and enhancing institutional inclusiveness, these initiatives have been steadily advanced, creating a “green channel” for unicorn enterprises to list on the A-share capital market.

Why Is There a Surge in Embracing Unicorns Now? What Measures Will Be Taken to Support Them? Which Unicorns Will Enter the IPO Fast Lane? VCBeat (WeChat ID: vcbeat) Aims to Answer These Questions.

It’s Time for China to Fulfill Its “BATJ Dream”

The current round of discussions on the A-share market embracing unicorns originated on February 27, when Xinhua News Agency published an article titled “It Is Time to Fulfill the ‘BATJ Dream’ in China’s Capital Markets.” The article stated that over the past decade, China’s internet and high-tech companies represented by Baidu, Alibaba, Tencent, and JD.com (collectively known as BATJ) have listed in the United States or Hong Kong, invariably adopting a model of “generating profits domestically while distributing dividends overseas.” Watching these outstanding enterprises go abroad without being able to retain them has become a “pain point” for the A-share market.

This list could be quite extensive. Apart from BATJ, well-known internet companies such as NetEase, Weibo, Ctrip, Vipshop, 58.com, and Autohome have all chosen to list overseas, resulting in the long-term “absence” of new-economy companies in China’s A-share market.

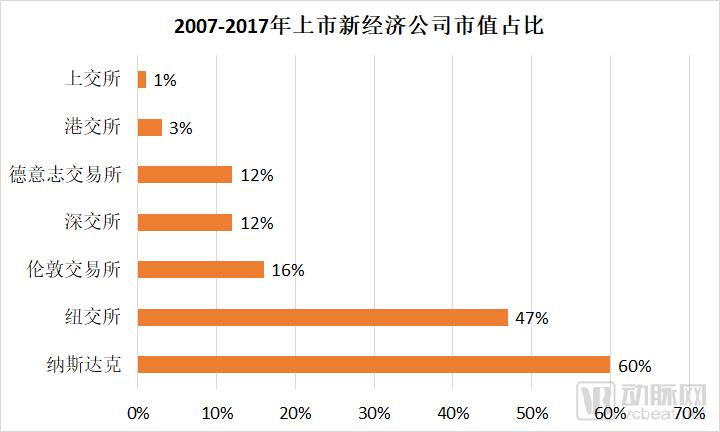

Data shows that “new economy” companies, represented by internet technology, biotechnology, and healthcare, account for only 12% of the total market capitalization of companies listed on the Shenzhen Stock Exchange (SZSE) and merely 1% on the Shanghai Stock Exchange (SSE). This reflects the A-share market’s lack of appeal to new economy companies and the current reality of obstructed pathways for such companies to access the A-share capital market.

New economy companies are “bypassing nearby opportunities to seek distant ones” by going all the way to the U.S. market, primarily for three reasons: First, the A-share market operates under an approval-based system, resulting in a large backlog of companies and lengthy waiting periods. Second, the A-share market imposes stringent requirements on the eligibility, corporate governance, and financial metrics of prospective listed companies, which new economy firms often struggle to meet simultaneously. Third, past domestic innovation largely consisted of “me-too” products benchmarked against Europe and the United States; in the U.S. market, new economy companies can find comparable peers, enabling investors to more easily understand their business models, form expectations about their future development, assign higher valuations, and thus facilitate capital raising.

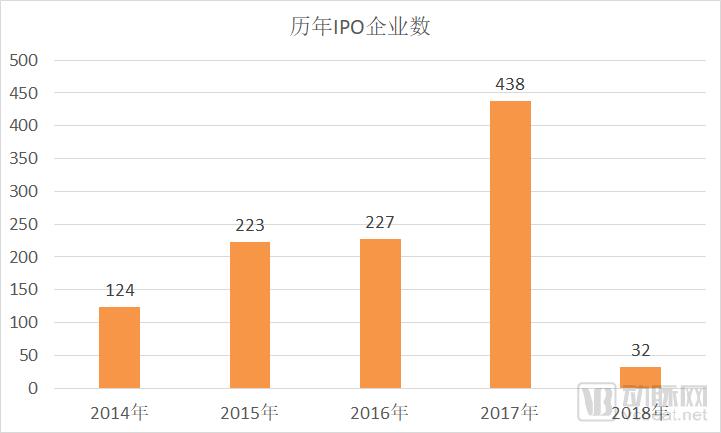

According to data released by the China Securities Regulatory Commission (CSRC), nearly 600 companies were still waiting in line for approval as of the end of 2017, resulting in a severe “backlog” phenomenon in initial public offerings (IPOs). At the existing pace of review and approval, it would take two to three years to clear this backlog. In contrast, markets such as the New York Stock Exchange (NYSE) and NASDAQ operate under a registration-based system, whereby issuers can raise capital in the capital markets promptly as long as their information disclosure complies with regulatory requirements.

From the perspective of listing requirements, A-share IPOs entail more stringent conditions. For instance, regarding the principle of "equal rights for equal shares," innovative enterprises typically undergo multiple rounds of fundraising prior to going public. To ensure founders retain control over the company, they often implement a dual-class share structure (Class A and Class B shares), whereby founders’ shares and investors’ shares carry different voting rights. However, the A-share market does not accept such disparities in voting rights. Other requirements, such as achieving consecutive profitability over the three years preceding the listing, maintaining operating cash flows exceeding RMB 50 million or generating revenues surpassing RMB 300 million, and meeting specific pre-issuance share capital thresholds, effectively bar a cohort of companies that continuously "burn cash" and lack profitability from accessing the A-share market.

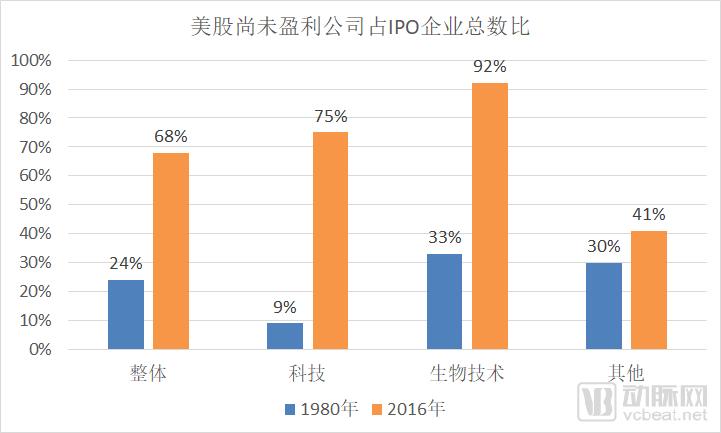

Relevant reports indicate that in recent decades, technological innovation and global integration have fundamentally transformed the landscape of many industries. In particular, driven by the “Internet economy,” new-economy companies have prioritized market share over profitability, often sacrificing profits to gain market presence. Investors in capital markets have clearly supported this trend. Taking the U.S. capital market as an example, statistics show that the proportion of companies permitted to list despite being “not yet profitable” rose from 24% in 1980 to 68% in 2016, serving as clear evidence of this trend.

There is a particularly large number of unprofitable biotechnology companies that have been approved for listing in the United States; among the biotech firms that entered the U.S. capital markets in 2016, 92% were “unprofitable.”

Furthermore, there is value alignment. The star internet company models mentioned above all originated in Europe and the United States, such as Baidu in relation to Google, Alibaba and JD.com in relation to Amazon, and Weibo in relation to Twitter. Similar business models help investors quickly assess the growth potential and long-term value of new-economy companies, rather than being confined to short-term interests.

“Green Channel, CDR, Investor Protection”: The Three-Pronged Strategy

To retain new-economy unicorns and attract listed high-tech companies back to the A-share market, the China Securities Regulatory Commission (CSRC), along with the Shanghai and Shenzhen stock exchanges, has intensively rolled out institutional reforms and innovative measures, which can be summarized as the “three-pronged approach” of green channels, Chinese Depository Receipts (CDRs), and investor protection.

Regarding the "green channel," the Issuance Department of the China Securities Regulatory Commission (CSRC) recently provided guidance to relevant securities firms. For clients classified as "unicorns" in four specific industries—biotechnology, cloud computing, intelligent manufacturing, and artificial intelligence—firms can report them to the Issuance Department immediately. Those meeting the relevant regulations will be subject to immediate review upon submission, bypassing the standard queue. Furthermore, for these enterprises seeking an initial public offering (IPO), not only are profitability requirements relaxed, but they are also exempt from dismantling their Variable Interest Entity (VIE) structures. The review process is expected to be completed within two to three months.

Foxconn’s “lightning-fast” approval serves as the best example: from submitting its IPO materials on February 1 to passing the review on March 8, Foxconn took only 20 working days, whereas the previous IPO cycle—from queuing to approval—lasted nearly 700 days. Foxconn has become the fastest company in the history of China’s A-share market to complete an IPO.

The market views Foxconn’s “lightning-fast” IPO approval as confirmation of rumors that regulators have opened a fast-track channel for initial public offerings (IPOs) by new-economy enterprises. The 2018 Government Work Report explicitly stated support for the listing and financing of high-quality innovative enterprises. In a previous interview on “how the capital market can serve the new economy,” Jiang Yang, Vice Chairman of the China Securities Regulatory Commission (CSRC), clearly indicated that the CSRC would align with national strategies and give preferential treatment in IPO reviews to industries characterized by “four new elements”—new technologies, new industries, new business formats, and new models—while prioritizing support for the listing and financing of innovative, leading, and demonstrative enterprises.

CDR is a financial instrument designed to facilitate the “return” of companies already listed overseas. Its full name is Chinese Depository Receipt. A Depository Receipt (DR) is a negotiable certificate circulating in one country that represents securities of a foreign company.

Depending on the place of issuance or trading, depository receipts are often given different names; for instance, those traded in the U.S. market are known as American Depositary Receipts (ADRs). In fact, many Chinese concept stocks listed in the United States have adopted the ADR model, including Baidu, JD.com, and NetEase.

The operational model of ADRs involves listed companies depositing a portion of their shares with domestic banks, which then issue depositary receipts for public trading on the stock market. Investors who purchase these depositary receipts effectively hold equity in the listed company, thereby enabling cross-border share trading.

Currently, the China Securities Regulatory Commission (CSRC) has established a dedicated working group to fully advance matters related to Chinese Depository Receipts (CDRs). It is reported that the first batch of companies shortlisted for CDR issuance has been announced, including BATJ (Baidu, Alibaba, Tencent, and JD.com), Ctrip, Weibo, NetEase, and Sunny Optical Technology, which is listed in Hong Kong.

At the corporate attitude level, founders of companies such as Tencent, Baidu, JD.com, NetEase, and Sogou have all stated in recent media interviews that they are “very willing to return to the A-share market, provided that regulatory policies permit.”

The Shanghai Stock Exchange stated that as early as 2001, prior to the establishment of the Strategic Emerging Industries Board, it had begun researching issues related to the domestic issuance of stocks or Chinese Depository Receipts (CDRs) by red-chip companies and the listing of enterprises in strategic emerging industries. This laid a solid foundation in terms of scheme design, institutional research, and technical implementation for the domestic listing of high-quality innovative enterprises.

In addition, the Shanghai Stock Exchange (SSE) has developed a service framework tailored for “BATJ”-type companies and “unicorn” enterprises. This includes compiling a list of high-quality innovative enterprises; adopting an integrated approach combining equity financing, debt financing, and corporate training to provide comprehensive services to promising new businesses; implementing a “bring in, go out” strategy to address specific issues related to accessing capital markets for high-quality enterprises; and establishing collaborative mechanisms with relevant national ministries, local government departments, high-tech industrial parks, leading securities firms, and investment institutions, thereby comprehensively enhancing the SSE’s capacity to serve enterprises.

The Shenzhen Stock Exchange also stated that it “has the foundational conditions to embrace the new economy.”

Of course, new-economy companies, by virtue of their “newness,” carry certain risks. For investors in the A-share market, it is particularly crucial to assess and identify these risks. In this regard, according to a recent announcement by the China Securities Regulatory Commission (CSRC), special arrangements have been made for investor protection concerning unicorn companies, and relevant indicators are being expedited for research and development.

"Green Channel," CDR, and Investor Protection: The Three Key Measures of A-Share Reform to Ensure Unicorn Companies "Stay Put," Overseas-Listed Companies "Come Back," and Investors' Rights Are "Secured."

Which Medical “Unicorns” Can Enter the IPO Fast Lane?

Under U.S. capital market standards, a “unicorn” refers to a company with a valuation exceeding $1 billion, while those valued at over $10 billion are termed “super unicorns.” According to research conducted by the China Securities Regulatory Commission (CSRC), there are currently around 100 unlisted companies in China with valuations of $1 billion, and no more than 50 with valuations reaching $2 billion.

This provides an overview of unicorns. Based on these criteria, which companies in the healthcare sector qualify as “unicorns”? Drawing on data from VCBeat and publicly available information, we have compiled a list of pre-IPO medical unicorn enterprises in China, as follows:

Note: Compiled based on official information from relevant companies and public reports. Every effort has been made to ensure the completeness and accuracy of the information. Should there be any discrepancies, corrections are welcome.

Among the aforementioned companies, some have already disclosed their IPO prospectuses, while others have seen rumors of their impending listings surface. For instance, Mindray Bio-Medical swiftly restarted its listing plans after withdrawing its initial application, and WuXi AppTec is currently in the queue. Ping An Healthcare has disclosed its Hong Kong IPO prospectus, while WeDoctor, Henlius, and Shanghai Tasly have successively sparked rumors of planning Hong Kong listings. These developments indicate that it is not only the market embracing unicorns, but also that these unicorn enterprises themselves possess a strong willingness to go public and raise capital.

Notably, several medical unicorns have chosen to list on the Hong Kong Stock Exchange (HKEX), hinting at emerging competition between the HKEX and China’s A-share market. In terms of listing rule reforms, the HKEX appears to be moving faster. On February 23, the HKEX released a consultation paper proposing to allow three types of companies to list in Hong Kong: a) biotechnology companies that fail to meet the financial eligibility tests, including those without revenue or profit records; b) high-growth and innovative industry companies with weighted voting rights structures; and c) eligible issuers seeking secondary listings on the Stock Exchange of Hong Kong.

A comparison shows that the Hong Kong Stock Exchange (HKEX) and the Shenzhen Stock Exchange (SZSE) have roughly equivalent numbers of listed companies, yet the total market capitalization of Hong Kong stocks exceeds that of the Shenzhen market. In terms of trading volume, however, Hong Kong stocks are less active than those in Shenzhen. Both markets have opened IPO channels; while the number of companies going public surged significantly in 2017 for both exchanges, the amount of capital raised through IPOs on the HKEX declined, whereas the SZSE saw a substantial increase. The reform of the Hong Kong stock market has served as an important catalyst for the reform of China’s A-share market.

Returning to the unicorn list, differences in listing requirements, investor profiles, exit conditions, and fundraising capabilities among A-shares, Hong Kong stocks, and U.S. stocks determine their choice of exchange. Given that these conditions are largely similar, medical unicorns are highly likely to choose to list on the A-share market.

Unicorn IPOs: Which Investment Firms Will Benefit?

As the proverb goes, “Fine horses are common, but good judges of them are rare.” In the venture capital and startup ecosystem, however, this saying should be reversed: good investors are plentiful, but truly exceptional startups are scarce. Entrepreneurship carries far greater uncertainty than horse racing; even star projects face the risk of early failure. Guiding a startup onto the right path and supporting it through its initial journey constitutes a milestone victory only when the company successfully enters the capital markets. Capital providers and innovative enterprises share both risks and rewards, while streamlined listing channels also offer investors clear exit pathways.

If the aforementioned medical unicorns successfully go public, which institutions stand to reap substantial returns? Several scenarios are possible, including self-incubated subsidiaries, industry funds, investment firms, and state-backed entities.

Regarding subsidiaries, the portfolio includes Ping An Good Doctor, Henlius, Shanghai Tasly, and I-Mab Biopharma. Ping An Good Doctor has disclosed its IPO prospectus and is expected to list as early as the second quarter of this year. Henlius is currently valued at over RMB 10 billion; compared with GenScript, a peer listed on the Hong Kong Stock Exchange with a market capitalization exceeding HKD 46.5 billion, Henlius’s market value could rise significantly post-listing. Shanghai Tasly and I-Mab Biopharma have strong ties to Tasly. Under the “parent benefits from child’s success” dynamic, their listings on either the Hong Kong Stock Exchange or the A-share market would provide a substantial boost to Tasly.

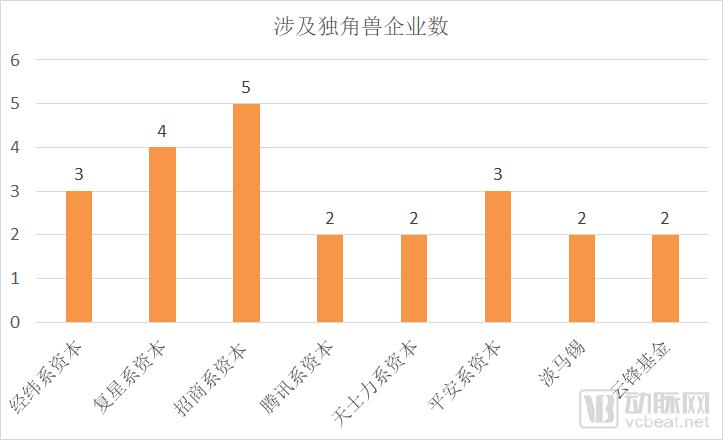

Regarding industrial funds, Matrix Partners-affiliated capital, Fosun International-affiliated capital, China Merchants Group-affiliated capital, and Ping An Group-affiliated capital have all participated in multiple projects. Below is the data on industrial investors with significant project participation:

The ability to identify unicorn companies is closely tied to investors’ familiarity with the healthcare market and their capacity for resource synergy. The more sustained and long-term the cultivation efforts, the greater the non-capital resources that can be delivered to portfolio companies, thereby supporting their continuous development and growth into unicorns.

It is also worth noting the entry of state-backed investors. For instance, the list of Series A investors for United Imaging Healthcare is almost exclusively composed of entities with “Guo” (National) or “Zhong” (China) in their names. The investor rosters of companies such as WeDoctor, Novogene, Gushengtang, and iCarbonX also feature numerous state-owned enterprises and local government funds. These state-backed investors typically enter at later stages through strategic investments. Their participation signifies, to a certain extent, capital market recognition of the commercial value of unicorn companies and may also facilitate their initial public offerings.

Unicorn companies symbolize the vitality of a thriving economy, and their role in driving economic growth is self-evident. In the capital market, they also exert a resource-agglomeration effect, serving as a “source of living water” for the market. The China Securities Regulatory Commission (CSRC), along with the Shanghai and Shenzhen stock exchanges, has implemented a series of measures to actively embrace unicorn companies. The healthcare industry has produced more than 20 unicorns. Under the A-share market’s “new policy,” these unicorn companies may rapidly list on the capital market and achieve leapfrog development.