2018 China Sleep Health Industry Trends Report: Traditional Enterprises Undergoing Intelligent Transformation, Creating New Traffic Entrances

Addressing the traditional enterprise model, Lang Xianping proposed the “6+1” industrial chain model, wherein six major segments—product design and development, raw material procurement, product manufacturing, warehousing and logistics, wholesale operations, and retail—collectively constitute a complete manufacturing industry. Currently, participants in the sleep health industry focus primarily on sleep-related home products. Most of these enterprises originate from manufacturing backgrounds and adopt wholesale business models, placing them within the secondary sector. On the production side, they face substantial cost and competitive pressures; on the product side, they contend with significant inventory and branding pressures.

For any industry, development generally follows four stages. After enduring the arduous early entry phase, experiencing rapid growth during the expansion phase, and reaching stability in the maturity phase, an industry with stable products, business models, channels, and demand will inevitably enter a “new normal” of development—a stage characterized by long-term, stable, yet low-level growth rates. With limited room for incremental growth across the industry, corporate opportunities are compressed, and competition primarily revolves around capturing share from the existing market. In this context, industrial trends are unstoppable; the key lies in embracing transformation.

We believe that the intelligentization of devices in the sleep product sector represents not only a qualitative leap for the products themselves but also constitutes a novel demand distinct from traditional home furnishings and textiles. More importantly, smart sleep technology diverges from the “6+1” model characteristic of the secondary industry, establishing a new production relationship centered on services. Therefore, we have reason to believe that if the sleep industry experiences new growth drivers in the future, they are highly likely to emerge from the smart sleep sector.

Therefore, this report centers on sleep intelligence, delving into transformation opportunities for traditional enterprises through macro-environmental analysis, industry competitive landscape assessment, and micro-level case studies of individual companies. It also explores the new products, business models, and insights that technology-driven innovators are bringing to the sleep industry.

This report, jointly produced by Pan-Home Furnishing Network and VCBeat’s Eggshell Research Institute, spans approximately 40 pages and nearly 20,000 Chinese characters. A free download link is provided at the end of the document.

We extend our sincere gratitude to Gao Song, Founder of Snail Sleep; Huang Jinfeng, Founder of Sleepace; and other industry experts for their invaluable support in the preparation of this report!

The following is an excerpt from selected sections of the report.

Table of Contents

I. Changes in the Macro Environment Make Industrial Upgrading Imperative

Residents' Sleep Health Is a Cause for Concern, and the Sleep Health Industry Holds Significant Demand Potential

Sleep Disorders Are Stubborn Yet Controllable

Macro-level Industrial Upgrading: The Inevitability of Business Adjustments for Traditional Enterprises

The Internet of Things Drives the Integration of Products and Services

II. Growth in the Sleep Industry Slows, Smart Sleep Solutions Poised to Become a New Growth Driver

Sleep Products: The Core Component of the Sleep Industry

Traditional sleep industry growth is sluggish; smart sleep solutions have emerged as a new growth driver, unlocking a market worth hundreds of billions.

Sleep Monitoring Becomes the Core Entry Point for the Intelligent Sleep Industry

Sleep Hardware + Sleep Services: The Business Foundation of Smart Sleep Enterprises

III. Traditional Industry Giants Move into the Intelligence Sector, with Industrial Investment Being the Most Popular

Luolai Home Textiles: Leveraging Industrial Investment to Enter the Sleep Monitoring Sector

Mlily: Partnering with Smart Sleep Enterprises to Build the Mlily Smart Sleep System

IV. Smart Sleep Investment Becomes More Rational, Technology-Driven Enterprises Show Strong Performance

Capital Markets Grow More Rational: Gimmicks No Longer Attract Capital

The industry’s overall financing remains at early stages, with the highest round reaching only Series B+.

In the field of technological innovation, financing capabilities are the strongest; in the field of service innovation, it is easier to attract capital attention.

V. Innovative Enterprises Rush to Enter the Market, Cross-Industry Collaboration Becomes a Trend

Leader in Smart Controllers: H&T’s C-Life Smart Platform Strategy, Serving Industry Players

Sleepace: An Industry Leader and a Hot Partner for Cross-Industry Collaboration

Entering the Smart Sleep Industry via an App: Snail Sleep’s Device-Free Sleep Monitoring

Orange Family: Entering Sleep-Related Chronic Respiratory Disease Management Through Blood Oxygen Monitoring

VI. Industry Giants Enter the Sleep Health and Health Management Sectors, Signaling Future Trends

Samsung: SmartThings Enables Intelligent Nighttime Home Control with SleepSense Monitor

Apple: Three “Kits” for Health Strategy

VII. Summary of Report Perspectives and Trends

Residents' Sleep Health Is a Cause for Concern; The Sleep Health Industry Holds Significant Demand Potential

With the improvement in residents' living standards and the emergence of new lifestyles driven by mobile internet, people's sleep quality has been deteriorating. According to Tencent's Big Data Report on Sleep, the proportion of internet users staying up late rose from 13% in 2010 to 20% in 2015, while average daily sleep duration decreased from 8.1 hours in 2010 to 7.05 hours in 2015.

In early 2017, the "China Sleep Quality Report" released by Huawei Health revealed that the sleep quality of Chinese residents was a cause for concern. The average bedtime was after 12:00 AM, and the average sleep duration was less than 7 hours. Among the respondents, 64% considered themselves sleep-deprived, 27% reported being prone to waking up easily, and over 12% indicated experiencing poor breathing during sleep.

According to relevant data, poor sleep quality can directly or indirectly contribute to more than 90 diseases, including neurasthenia, Alzheimer’s disease, hyperlipidemia, obesity, diabetes, coronary heart disease, and cardiovascular diseases. Improving sleep quality can enhance residents’ quality of life and physical health from an individual perspective, while reducing the number of patients and alleviating pressure on the healthcare system from a societal perspective.

The traditional approach to building national health in China has centered on enhancing disease treatment capabilities. However, under the influence of various societal pressures—such as population aging, increased life expectancy, a shortage of medical professionals, and a significant rise in the incidence of chronic diseases—improving residents’ health solely from the perspective of “disease treatment” is no longer sufficient to address the increasingly prominent supply-demand imbalance in the healthcare sector. Disease prevention centered on health management can reduce disease incidence at its source and alleviate the supply-demand mismatch in the healthcare industry.

In 2016, the State Council issued the Outline of the “Healthy China 2030” Plan, which pointed out that we should “implement the principle of prevention first and promote healthy lifestyles.” The strategic core of building a Healthy China is to center on people’s health, adhere to a focus on primary care, take reform and innovation as the driving force, prioritize prevention, place equal emphasis on traditional Chinese medicine and Western medicine, integrate health into all policies, and follow the health work guideline of joint construction and shared benefits by the people. Addressing health determinants such as lifestyle behaviors, production and living environments, and medical and health services, we must combine government leadership with mobilizing the enthusiasm of society and individuals, promote participation, contribution, and benefit for all, implement the principle of prevention first, promote healthy lifestyles, reduce disease incidence, strengthen early diagnosis, early treatment, and early rehabilitation, and achieve health for all.

Sleep Disorders: A Stubborn Yet Controllable Condition

The causes of poor sleep are complex and varied; any factor that increases the excitability of the central nervous system can contribute to sleep disturbances. These factors can be categorized into six types: environmental, behavioral, disease-related, psychological, and those related to medication and alcohol consumption. Insomnia in patients is often multifactorial; in real-world settings, psychological factors are a common trigger for insomnia. In fact, while these six categories of factors primarily stem from objective environmental conditions and are difficult to avoid entirely, they can be mitigated through human intervention to improve sleep quality. This potential for improvement constitutes the fundamental demand underpinning the existence of the sleep health industry.

Most diseases can be alleviated to some extent, or even completely cured, through treatments such as medication, psychotherapy, surgery, and medical devices. The demand within the sleep health industry is universal, and there are multiple effective ways to meet consumer needs. This means that the sleep health industry not only holds enormous consumption potential but also offers diverse entry points. Whether engaged in products, services, medical devices, or broader industrial operations, companies can find their own strategic niche within this vast industry.

# Macro Industrial Upgrading Makes Business Adjustments Inevitable for Traditional Enterprises

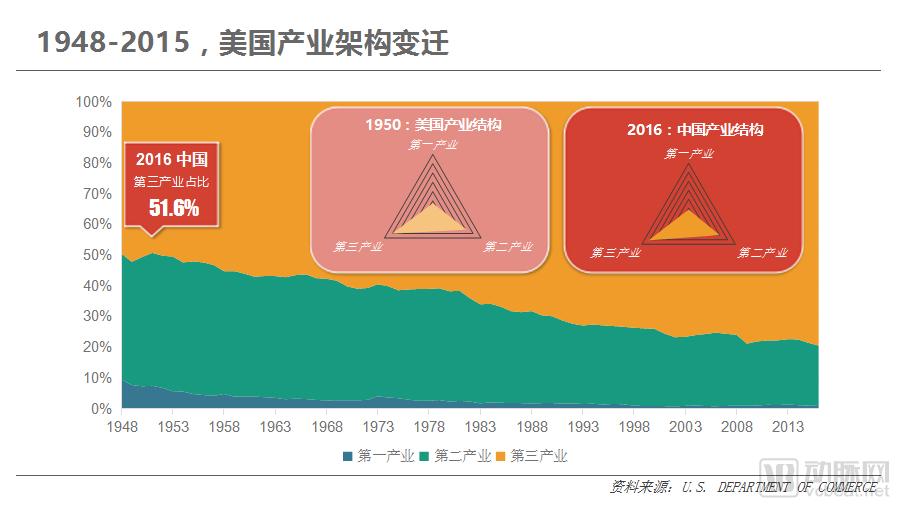

Insufficient endogenous growth drivers, rising manufacturing costs, and intense industrial competition, coupled with the booming tertiary sector, have led to a year-on-year decline in the influence of the manufacturing-centric secondary sector on China’s economic development. However, from an industrial trend perspective, such development exhibits a certain degree of inevitability.

Currently, China’s industrial structure is roughly comparable to that of the United States in the 1950s. During that period, post-war economic recovery spurred the release of consumer and service demand in the U.S. In 1949, the tertiary sector’s share of national income surpassed the combined shares of the primary and secondary sectors for the first time, subsequently embarking on a sustained, fluctuating upward trend. According to data from the U.S. Department of Commerce, by the end of 2016, the tertiary sector accounted for more than 79% of U.S. national income. This inevitable trend suggests that China’s secondary sector may face a prolonged and persistent period of uncertainty in the future.

The tide of history is unstoppable; embracing change is the key. The most renowned theory on traditional business models is Lang Xianping’s “6+1” industrial chain model, which posits that six major segments—product design and development, raw material procurement, manufacturing, warehousing and logistics, wholesale operations, and retail—combine to create one complete manufacturing industry.

Current participants in the sleep health industry are primarily centered on sleep-related home products. Most of these enterprises originate from manufacturing backgrounds, operate through wholesale models, and belong to the secondary sector. On the production side, they face substantial cost and competitive pressures; on the product side, they contend with significant inventory and branding challenges.

The secondary industry has encountered significant challenges; therefore, while these enterprises are enhancing their manufacturing capabilities through lean production, they are also actively expanding into the tertiary sector, achieving a strategic shift in their core business model from “product” to “product + service + ecosystem.”

In the early stages of industry competition, immense domestic consumer demand fostered a seller’s market, prompting enterprises to prioritize increases in output and efficiency given the abundance of demand. As the market evolved, this seller’s market gradually transitioned into a buyer’s market. Such enterprises found that robust production capacity, coupled with rising demand uncertainty, instead resulted in significant inventory pressures. The reform approach centered on mass production, exemplified by lean manufacturing, aims fundamentally to improve capacity utilization and maximize the production potential of limited resources. However, capacity utilization is driven by end-user demand; while improving capacity utilization on the supply side is a necessary condition for the recovery of manufacturing investment, the continuous expansion of end-user demand is the sufficient condition. Consequently, shifting the strategic focus from the production end to the consumption end has become the core of these enterprises’ reforms in recent years.

The reform directions are mainly divided into the following points.

On the product development front: intensify technological R&D to enhance product value-added; drive product development based on market demand; and improve product customizability.

On the raw material procurement side: Introduce a comprehensive supplier management system to provide stable material support for a flexible supply chain.

On the production side: Implement a flexible manufacturing model characterized by small-batch, high-frequency production runs, striving even for ultra-flexible, individual order-driven manufacturing; promote intelligent manufacturing to reduce labor costs.

Warehousing and Transportation: Implement an intelligent warehouse management system to enhance inventory controllability and management efficiency; develop smart warehousing capabilities to provide service support for small-batch orders associated with flexible production.

Wholesale Operations: Streamline distribution channels, develop direct sales channels, and enhance the controllability of distributors and channel service capabilities.

Retail Terminal Strategy: Implement comprehensive terminal reforms to enhance brand image, open more high-end and specialized terminals, and build an omni-channel, intelligent terminal network.

Supply Chain Management: Transforming traditional push-based supply chains into demand-driven pull-based supply chains.

The fundamental purpose of this reform is to leverage information technology, new material technology, and other advanced technologies to facilitate a transformation from a product manufacturer into a consumer-centric brand with robust product research, development, and manufacturing capabilities. By abandoning low-margin production-based profit models, the company aims to anchor its core profitability in products and services, thereby achieving a complete business model transition that aligns with contemporary demands and industrial development trends.

IoT Drives the Integration of Products and Services

Currently, the accumulation of human disease data primarily relies on real-time monitoring data provided by patients during their hospital stays. However, due to the significant lack of vital signs data during nighttime hours, the etiologies of many diseases cannot be defined or traced. Therefore, focusing on the sleep process not only alleviates the direct suffering caused by insomnia but also enables disease etiology tracing through the real-time acquisition of sleep-related physiological signals, thereby supporting disease prevention and treatment.

Imagine if, by leveraging extensive nocturnal physiological data from a large user base and integrating it with other datasets—such as dietary information, ambient temperature and humidity levels, physical activity metrics, medical history, and prior treatment experiences—we could establish more precise probabilistic models for disease prediction and recommendation models for therapeutic regimens. This would significantly enhance the controllability of disease onset and the precision of disease treatment. Such application scenarios constitute a key driver behind the rapid development of sleep data monitoring in recent years.

Traditional sleep product manufacturers (primarily referring to home textile and home furnishing companies) can engage in industrial collaboration with technology firms by integrating detection sensors into traditional sleep aids or compact monitoring devices, thereby achieving the goals of sleep monitoring and data collection. This approach not only enhances product value-added but also enables these manufacturers to enter the sleep services industry. By collaborating with backend big data companies and medical institutions, they can integrate industry resources and establish a sleep health service platform centered on sleep products. This development strategy has become the primary pathway for traditional sleep product manufacturers to transform their industrial roles in recent years. Within this industrial framework, products and services are inseparable, allowing manufacturing enterprises to break through the profitability bottlenecks of traditional product sales models and identify new revenue opportunities. On a macro level, this aligns with the trend of industrial evolution; on a micro level, it strengthens the core competitiveness of enterprises.

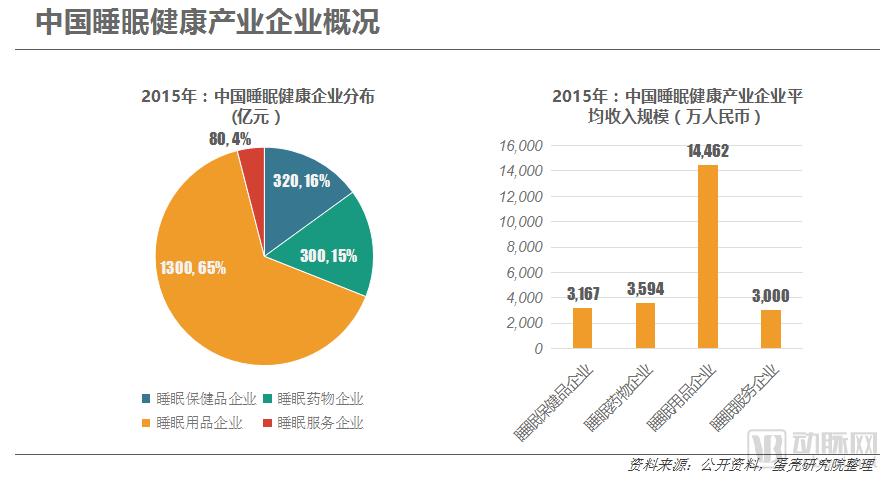

Sleep Products Become a Core Component of the Sleep Health Industry

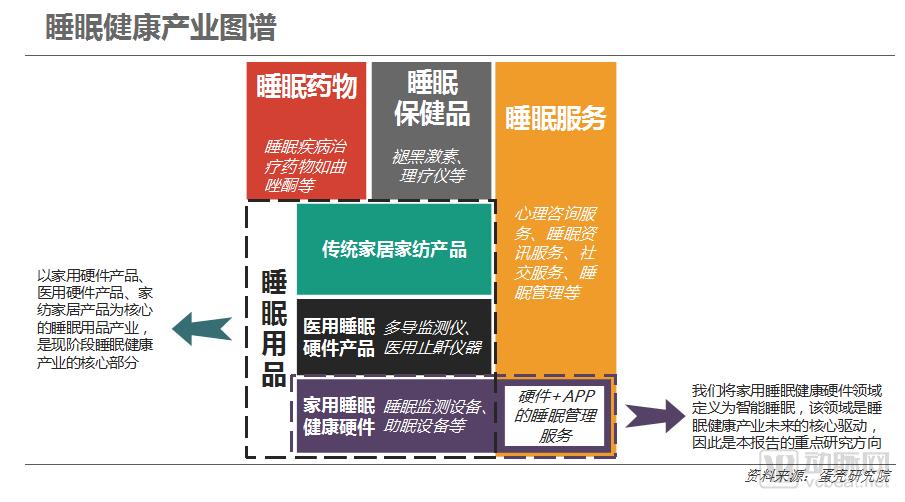

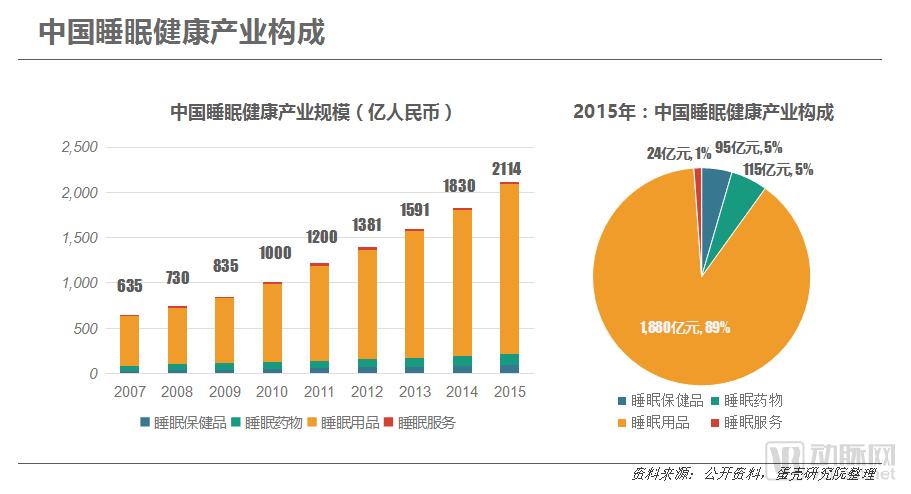

The sleep health industry can be divided into four major categories: sleep supplements, sleep medications, sleep products, and sleep services. According to public data, by 2015, the scale of China's sleep health industry had reached RMB 211.4 billion, with a compound annual growth rate exceeding 16%.

Currently, the sleep health industry is dominated by sleep-related products (including home textiles, medical devices, and smart hardware), with over 89% of the market held by companies in these sectors. As of 2015, the market size exceeded RMB 188 billion.

From 2007 to 2015, the annual average growth rate of China’s sleep health industry reached 16.2%. Among various sub-sectors, the sleep services sector, including psychological counseling, experienced the fastest growth, with a compound annual growth rate of 25%. However, due to its relatively small overall scale, this sector currently has a very limited impact on driving the development of the industry as a whole.

In the field of sleep products, not only is the market size substantial, but the rapid growth of this segment has also become the primary driver of growth for the sleep health industry. Between 2007 and 2015, the compound annual growth rate (CAGR) of the sleep products industry reached 16.7%. In 2015, growth in this segment accounted for 92% of the industry’s incremental expansion. It is evident that the sleep products sector serves as a main pillar of the sleep health industry, both in terms of market scale and growth momentum.

In terms of corporate distribution, sleep product companies constitute the largest group, accounting for 65% of the total. However, the number of these enterprises is disproportionate to the scale of this specific segment. This discrepancy is primarily attributable to the high maturity of the industry, where companies in this niche tend to be larger in overall size. We have observed that among the four sectors within the sleep health industry, aside from sleep products, the average annual revenue of companies in the other sectors hovers around RMB 30 million. In contrast, the average annual revenue for sleep product companies reaches RMB 144.62 million. The higher average revenue in the sleep products sector stems from the well-established nature of traditional industries such as home textiles, home furnishings, and medical devices, which are dominated by large enterprises, thereby compressing the competitive space for smaller players. It should be noted, however, that vertical smart hardware companies belonging to this sector, due to their later entry into the market, have not yet reached this level of revenue.

Traditional Sleep Industry Sees Sluggish Growth, While Smart Sleep Emerges as a New Growth Driver, Unlocking a Market Worth Hundreds of Billions

Based on application scenarios, the sleep health industry can be divided into three major sectors.

Sleep Quality and Health: Traditional sleep products, represented by conventional home furnishings and home textiles, that enhance sleep comfort.

Sleep Health and Medical Care: Medical products for the treatment of sleep disorders, represented by sleep medical devices and sleep medications

Sleep Intelligence: Leveraging smart home textiles, smart home systems, intelligent devices, and smartphones, with the aim of safeguarding physical health, this approach relies on technologies such as sensors, the Internet of Things (IoT), mobile internet, and big data to deliver intelligent products and services—including data monitoring, health management, smart home integration, and personalized sleep solutions. This article focuses its research on sleep intelligence innovations primarily within the household sector.

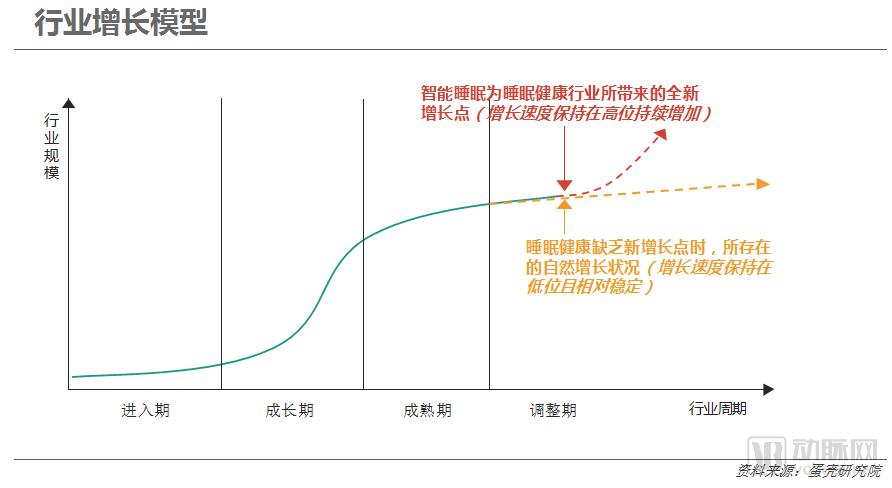

Industry development can generally be summarized into four stages. After experiencing the arduous development of the entry phase, the rapid growth of the expansion phase, and the stabilization of the maturity phase, an industry with stable products, business models, channels, and demand will inevitably enter a “new normal” of development—a stage characterized by long-term stability and low-level growth rates. With limited room for incremental growth across the industry, corporate opportunities are compressed, and competition primarily revolves around vying for share in the existing market.

Among the four elements mentioned above, if one or more factors are disrupted, the industry may discover entirely new growth drivers, thereby entering a new growth cycle. The prerequisite for such development is often a qualitative transformation in one or more of these four elements, which unlocks novel consumer demand and, to some extent, restructures the industry. We believe that the intelligentization of sleep-related devices represents not only a qualitative leap in products but also constitutes a new type of demand distinct from traditional home furnishings and textiles. More importantly, unlike the “6+1” model characteristic of the secondary industry, smart sleep solutions establish a new production relationship centered on services. Therefore, we have reason to believe that if new growth drivers emerge in the future sleep health industry, they are highly likely to originate from the field of smart sleep technology.

For smart sleep technology, the direct reason for the slow industry development at this stage is that consumer habits have not yet been established.

Innovative tech products such as smart sleep solutions are typically adopted first by innovators, then by early adopters, followed by the early majority, the late majority, and finally laggards. After years of rapid development in mobile internet and smart hardware, the smart sleep health industry has currently entered the early adopter stage. Users at this stage are predominantly industry-specific clients. The current bottleneck for the industry lies in the lack of effective comprehensive solutions for insomnia; most products suffer from low accuracy, a lack of open collaboration among upstream and downstream entities, and insufficient market maturity. Key market challenges include the need for more precise monitoring technologies, more open collaborations across the supply chain and with cross-industry partners, and continued efforts in market education.

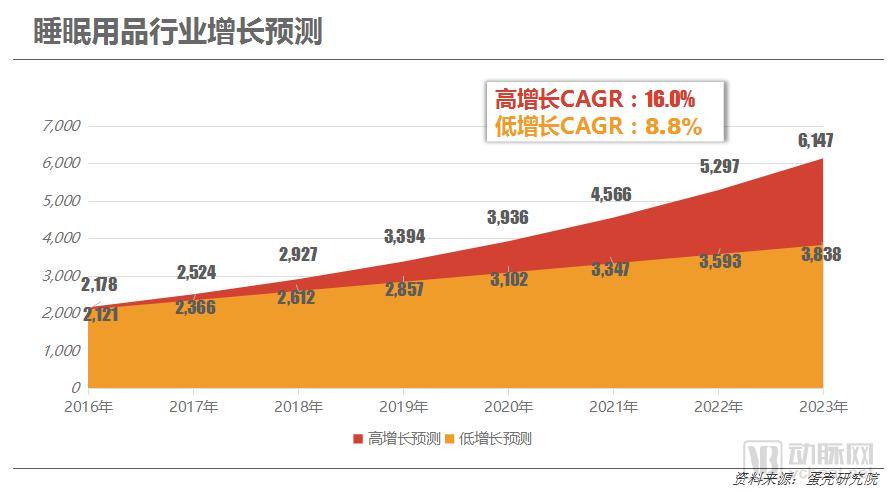

Based on historical industry data and analytical models, we have projected the scale of industry development. A high-growth forecast indicates that intelligent products and technological innovations centered on sleep intelligence have gained market recognition based on past performance. This has introduced new growth drivers to the sector, initiating a phase of rapid expansion with an accelerating growth rate, thereby reflecting a broadly anticipated increase in overall market size.

Low-growth projections indicate that, based on historical data, traditional products and upgraded offerings centered on sleep quality and health are experiencing stable market demand, resulting in a forecast of gradually declining growth rates.

While growth in the sleep industry driven by traditional channel reforms, enhanced product comfort, and brand upgrades is necessary to some extent, it is short-lived and unsustainable against the backdrop of saturated overall consumer demand. In contrast, smart sleep solutions, which build upon traditional sleep products while offering additional intelligent services, can stimulate new consumer demands and create fresh growth opportunities.

Sleep Monitoring Becomes the Core Entry Point for the Smart Sleep Industry

The Smart Sleep Industry Can Be Divided into Four Major Sectors

Hardware: Upstream hardware material enterprises primarily focused on product components such as sensors and chips.

Equipment: Smart sleep devices, represented by sleep monitors and smart sleep aids

Data: Data Management and Report Analysis for Sleep Monitoring Data

Application: Apply sleep monitoring data to various fields, including medical care, sleep improvement, and health assessment.

It is clearly evident that the current smart sleep industry centers on sleep monitoring, leveraging sleep monitoring data to deliver related health management services. Sleep monitoring can be regarded as a key entry point into the sleep health industry. By utilizing data derived from sleep monitoring, companies can offer a range of medical and healthcare services, including health assessments, thereby creating new opportunities for the transformation of traditional enterprises and the growth of innovative companies.

Sleep Hardware + Sleep Services: The Business Foundation of Intelligent Sleep Enterprises

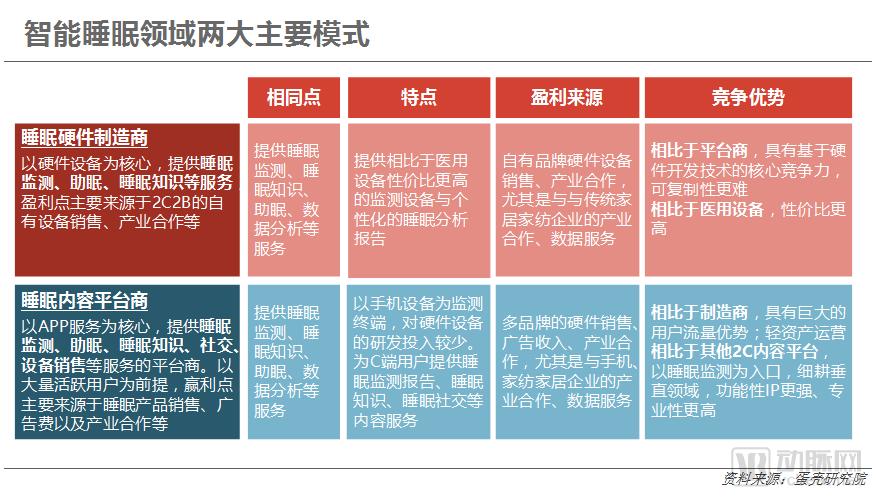

Companies in the field of intelligent sleep health can be categorized into two types:

A category of sleep hardware manufacturers that integrate smart hardware with mobile applications to provide services such as sleep monitoring, sleep improvement, and sleep data analysis, generating revenue through product sales and industrial collaborations. We refer to them as integrated product-and-service sleep hardware manufacturers. Taking Sleepace, a representative company in this sector, as an example, its monitoring devices analyze sleep status using Heart Rate Variability (HRV) technology along with indicators such as respiration and body movement; this technology has been widely recognized by the academic community.

A category of services centered on software applications, offering sleep data analysis, sleep education, and sleep improvement solutions, with revenue generated through platform-based e-commerce device sales, advertising, data monetization, and industry partnerships. We refer to these as sleep content platforms that use sleep monitoring as an entry point. In the Apple App Store, there are more than 10 sleep-aid apps represented by Snail Sleep, Firefly Sleep, Little Sleep, and White Noise. Some of these apps also provide basic monitoring functions, such as measuring sleep duration and distinguishing between deep and light sleep stages, by leveraging technologies like audio capture and body temperature collection.

The former focuses on the sales of its proprietary branded hardware devices, with app-based sleep reports and sleep education serving as value-added services. Such companies typically possess strong R&D capabilities, hold multiple technical patents, and offer products with high technological sophistication, excellent industrial design, and accurate monitoring mechanisms. Compared to medical-grade equipment, their devices provide better cost-performance ratios. These companies can establish competitive moats through technology and patents.

The latter approach leverages mobile sensor-based sleep monitoring as an entry point, with software services such as sleep tracking and sleep education at its core. Due to its heavy reliance on user traffic, it often incorporates social features to enhance user stickiness and facilitate viral dissemination. Monetization strategies primarily revolve around the sales of sleep-themed products, advertising, and industrial partnerships. Such companies typically invest little or nothing in hardware development; instead, their core competitiveness must be built upon a strong brand IP established through first-mover advantage, coupled with the continuous provision of vertical content highly relevant to sleep. Meanwhile, they strive to forge close collaborations with smartphone manufacturers to secure more user access points and consolidate their traffic advantages.

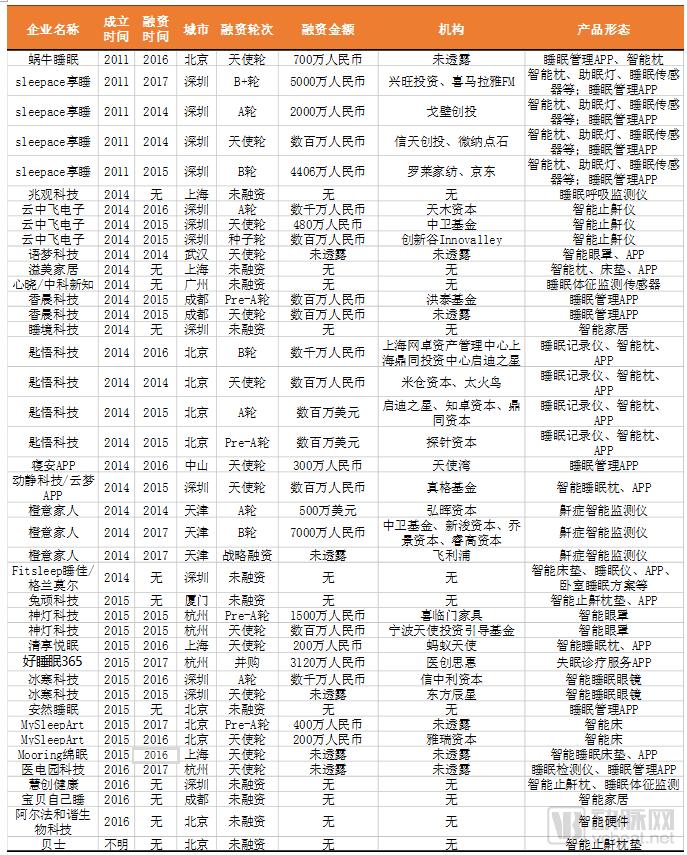

According to incomplete statistics from VCBeat, there are currently more than 30 companies in the smart sleep sector, with over half having secured financing. The funding amounts primarily range from several million to tens of millions of RMB. Among them, Orange Family’s Series B round was the largest, reaching RMB 70 million. Overall industry financing is concentrated in the early angel stage; even Sleepace, which has completed the most funding rounds, has only reached Series B+. The industry as a whole remains relatively immature, indicating substantial room for future growth.

Our statistical analysis of companies in the smart sleep sector focuses primarily on innovative enterprises centered on sleep health. Industry giants such as Philips and Samsung also manufacture sleep monitoring products and provide related services; however, due to the complexity of their business operations, which could impair our assessment of the capabilities of innovative firms, this report does not include an analysis or study of these companies and their products.

In terms of sleep monitoring products, they are mainly divided into three categories: medical polysomnography monitors, wearable monitoring devices, and non-wearable monitoring devices.

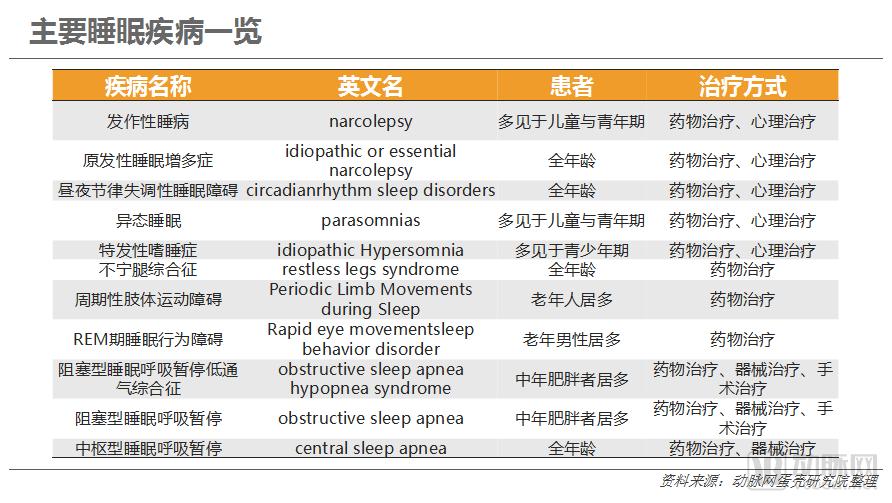

Polysomnography (PSG) Monitor: Currently the most professional device in the field of sleep monitoring, it can detect various sleep disorders such as snoring, narcolepsy, pediatric obstructive sleep apnea, Kleine-Levin syndrome, hypersomnia, and insomnia. By continuously monitoring indicators such as respiration, arterial oxygen saturation, electroencephalogram (EEG), electrocardiogram (ECG), and heart rate throughout the night, it can determine whether a snorer experiences apnea, the frequency and duration of apneic events, the lowest arterial oxygen saturation levels during these events, and the extent of their impact on physical health. It is internationally recognized as the gold standard for diagnosing sleep apnea-hypopnea syndrome (SAHS). The polysomnography monitor is currently the most commonly used method for sleep monitoring and the most critical examination for diagnosing snoring, serving as the internationally accepted gold standard for the diagnosis of sleep apnea-hypopnea syndrome.

In terms of home-use hardware, devices are primarily categorized into sleep-aid devices and monitoring devices, with the latter further divided into wearable and non-wearable types.

Representative Wearable Monitoring Device: Smart BandsSmart bands analyze sleep status using actigraphy. Specifically, they assess sleep patterns by monitoring the wearer’s body movement frequency via built-in gravity sensors and three-axis accelerometers. During light sleep, body movements are more frequent, whereas during deep sleep, they are less frequent. Although these devices are affordable, they offer lower accuracy and lack heart rate monitoring capabilities.

Representative Non-Wearable Monitoring Device: Sleep Belt. Featuring a strip-like design embedded with sensors, it is laid flat on the bed to analyze nighttime sleep patterns. It can measure total sleep duration, resting heart rate, respiratory rate, sleep latency, number of awakenings, and total time spent in deep sleep, as well as monitor snoring. This device offers high accuracy and entails higher manufacturing costs, while exerting minimal impact on the user’s sleep.

Representative Non-Wearable Monitoring Device: The Monitoring Button. Placed beside the pillow, it enables monitoring. Button-shaped, it detects sleep status through body movement. It can only monitor sleep cycles, sleep efficiency, body movement, and humidity/temperature, with limited monitoring accuracy.

This report is a collaborative production by VCBeat and Pan-Home Furnishing Network.

The above is an excerpt from this report. To obtain the full report, PC users can click to access the VCBeat Report Download Center (http://vcbeat.top/Report/reportIndex) to view or download the full report; WeChat users need to follow the official WeChat account and click on "Knowledge Base - View Report" below to access or download the complete version.