Premier's Endorsement Signals New Growth Phase for 'Internet + Healthcare' Amid IPO Filing

Sophmind

Internet Medical Examination Platform

During the ongoing Two Sessions, Premier Li Keqiang, while participating in the deliberation of the government work report with the Ningxia delegation, called on relevant departments to accelerate the development of “Internet + Healthcare.” The Premier’s remarks have brought “Internet + Healthcare,” which had previously lost momentum, back into the spotlight of public discourse.

The first phase of “Internet + Healthcare” was characterized by numerous internet healthcare companies burning cash to acquire users. Due to shifts in the capital market and policy orientation, “Internet + Healthcare” entered a cold period starting in 2016. The greatest value of the internet lies in connecting demand with supply; it can play a role in reshaping industry structure in sectors where supply exceeds demand. However, the biggest obstacle in healthcare is the shortage of qualified medical supply, making it difficult for the internet to disrupt the industry landscape. The Premier’s formal statement helps eliminate uncertainty in policy direction, paving the way for the second phase of development in “Internet + Healthcare.”

The second phase will be characterized by transforming the internet into a foundational capability for all healthcare services, pharmaceuticals, and health insurance. Internet healthcare companies are deeply integrating with offline physical medical institutions, and even establishing their own brick-and-mortar facilities. As reforms such as medical consortia and family doctor systems advance, traditional medical institutions will also enhance their adoption of internet applications to improve operational and management efficiency. The boundary between internet healthcare enterprises and traditional medical institutions will become increasingly blurred, paving the way for “Internet + Healthcare” to enter its third phase.

I. The Development of “Internet + Healthcare” Has Fluctuated with Policy Trends

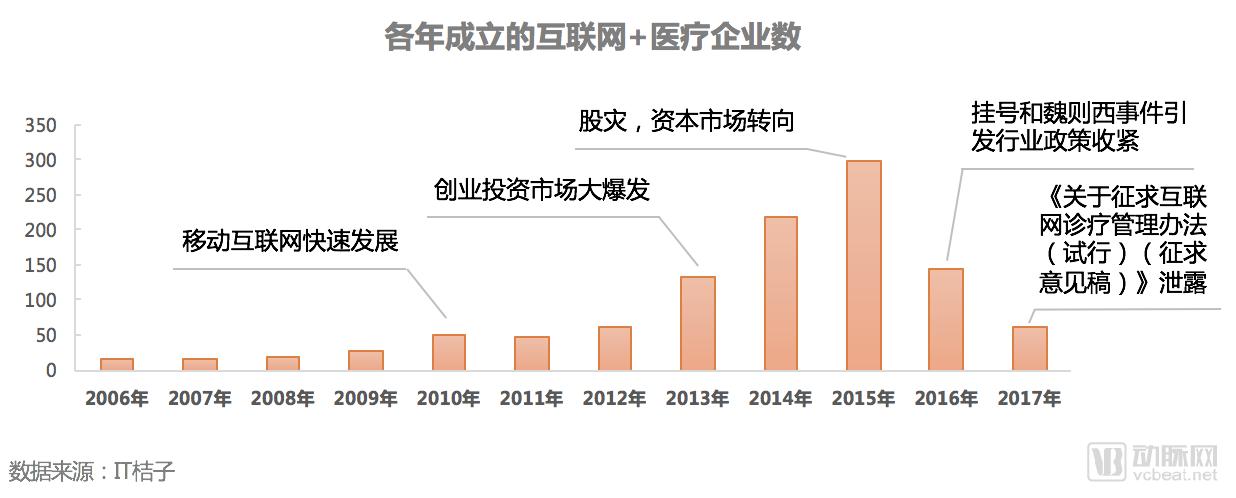

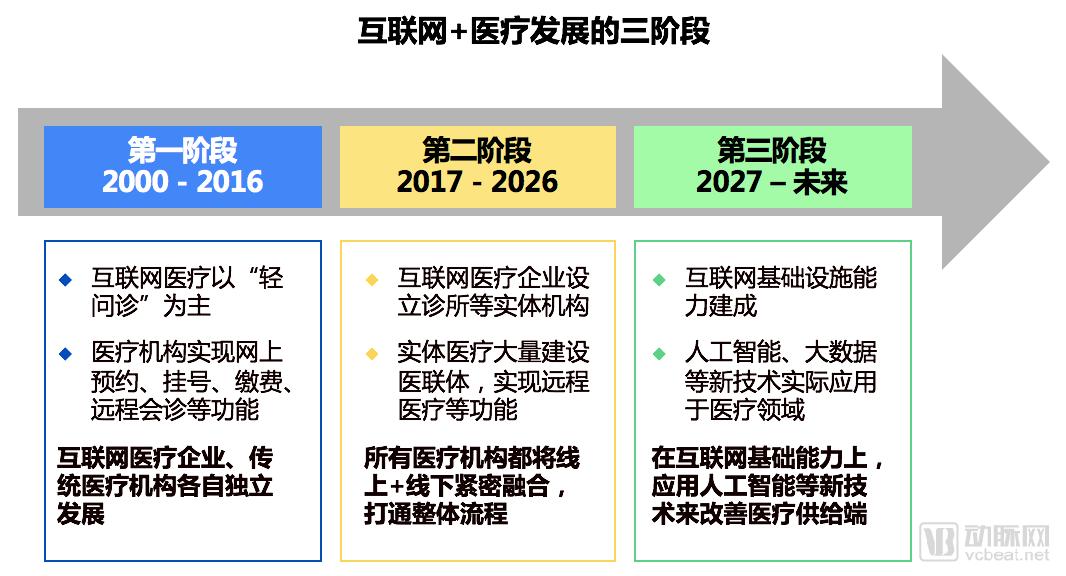

From 2000 to 2017, Internet Plus Healthcare was in its first stage of development. The concept of Internet Plus Healthcare emerged during the 2000 Nasdaq bubble and subsequently experienced slow growth. It was not until the explosion of mobile internet around 2010 that Internet Plus Healthcare entered a period of rapid development. Particularly after 2013, buoyed by a surge in venture capital investment, numerous Internet Plus Healthcare companies emerged. These enterprises sought to replicate the proven strategies of the mobile internet sector within the healthcare industry, aiming to become transaction platforms connecting supply and demand by acquiring a large base of consumer-end (C-end) users.

However, in practice, the healthcare industry is characterized by low-frequency demand, high professional barriers, stringent policy thresholds, and a lack of clear payers, rendering this classic strategy ineffective. In particular, as dominance in the sector remains firmly in the hands of renowned hospitals and top-tier experts, the connective role of internet companies is quite limited. In 2015, sentiment in the capital markets began to reverse, with investors no longer endorsing cash-burning strategies aimed at scaling up. Meanwhile, efforts by internet healthcare companies to capture high-quality medical resources from the traditional healthcare system faced backlash. Triggered by incidents such as the “registration gate” scandal and the Wei Zexi case, regulatory authorities and major hospitals significantly tightened external collaborations. To cope with this situation, many internet healthcare companies pivoted toward establishing internet hospitals, hoping to gain recognition from regulators and industry experts through legitimate licenses. However, the “accidental leak” of the Draft for Comments on the Administrative Measures for Internet Diagnosis and Treatment (Trial) revealed the regulators’ cautious stance toward internet healthcare. Consequently, internet healthcare companies fell from grace, hitting rock bottom as the sector cooled down comprehensively.

II. In the first phase, internet healthcare companies primarily focused on the incremental market of “light consultation” services

During the first phase of “Internet + Healthcare,” traditional medical institutions’ digital transformation and internet healthcare companies developed largely independently, like two parallel lines.

Traditional healthcare institutions have primarily focused their internet applications on appointment scheduling, payment processing, and remote consultations. In some regions, healthcare institutions have taken the lead in establishing internet hospitals, such as the Online Hospital of Guangdong Second Provincial General Hospital and the Internet Hospital of The First Affiliated Hospital, Zhejiang University School of Medicine; however, their scope of application remains limited.

Internet healthcare companies primarily focus on services such as light consultations, online counseling, and appointment slot additions. Their main offerings are value-added services centered around the core processes of diagnosis and treatment. However, the mainstream demographic for medical services tends to be older, making it difficult to establish consistent usage habits. Consequently, the conversion rate from online interactions to actual offline clinical care is very low, and effective collaborations with physical medical institutions remain scarce.

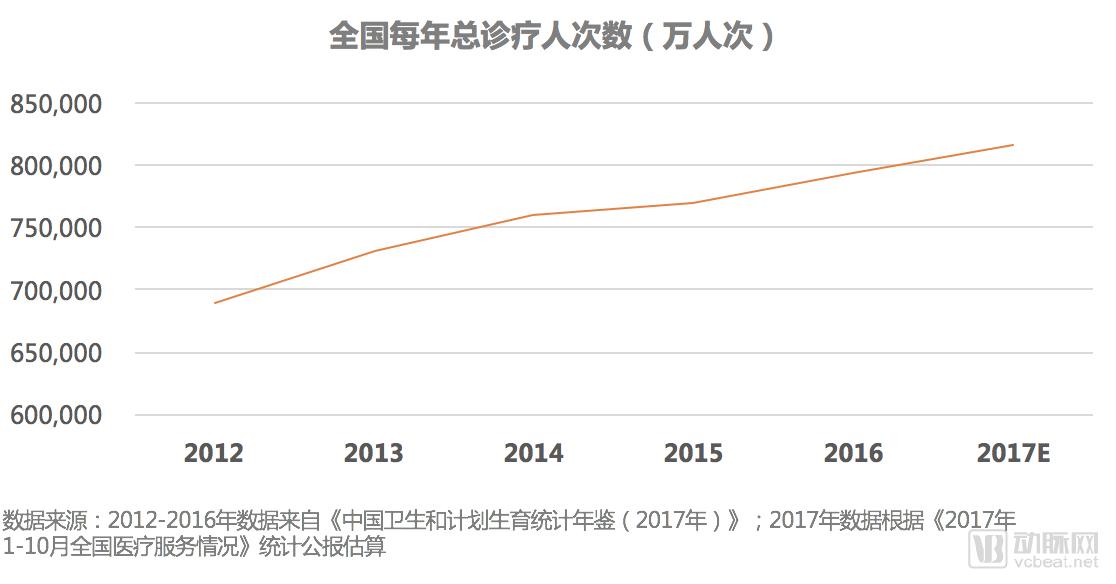

As disclosed in the prospectus of Ping An Good Doctor, by the end of 2017, its monthly active users reached 32.9 million, more than five times that of the second-largest competitor, with an average of approximately 370,000 online consultations per day. Based on this, the total volume of online consultations nationwide in 2017 was estimated at around 200 million. Meanwhile, the number of visits to physical medical institutions across China continued to rise steadily, reaching approximately 8.2 billion in 2017. This indicates that the service volume of physical medical institutions has not been significantly affected by internet healthcare. Instead, internet healthcare has provided the public with a new channel to address their needs for medical and health consultations, coexisting harmoniously with traditional in-person visits.

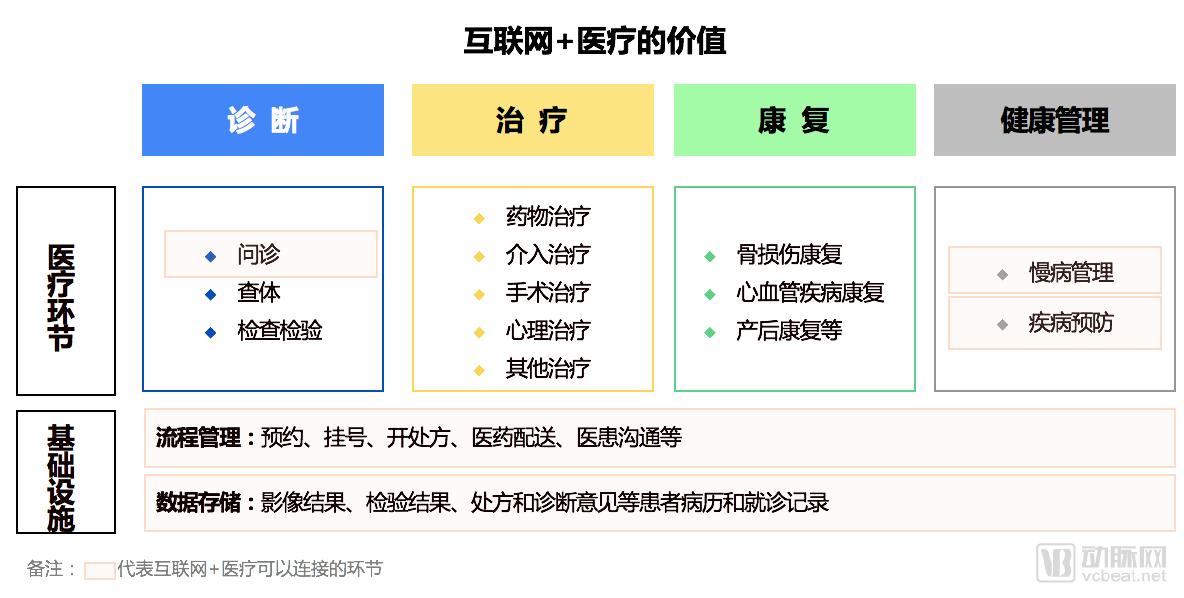

III. Core Value and Development Barriers of Internet+ Healthcare

“Internet + Healthcare” does not alter the essence of medical care. The greatest value of the internet lies in connectivity, which to some extent decouples doctors, patients, and hospitals from physical location constraints. It enables certain processes to be handled online and facilitates the storage and retrieval of medical data throughout the service journey. This helps eliminate information asymmetry and improve overall efficiency.

The development of "Internet + Healthcare" is constrained by insufficient supply-side resources and the inherent characteristics of healthcare itself:

(1) Policy restrictions: While existing macro-level policies strongly encourage physicians’ multi-site practice, the development of medical consortia, and family doctor services, implementation at the operational level remains rooted in traditional models. There are numerous restrictions on the establishment of new medical institutions and the mobility of medical resources. Internet-based medical services have not been integrated into the public hospital-led medical consortium framework, thereby lacking support for formal referral systems and health insurance reimbursement.

(2) Insufficient Resources: Constrained by the lagging state of medical education in China and the dim career prospects for physicians, the scarcity of high-quality medical resources remains unchanged and is even worsening. The number of outstanding physicians attracted to “Internet + Healthcare” platforms is limited, with a significant proportion of senior physicians from major hospitals not having joined these online platforms.

(3) Inherent Characteristics: Healthcare is a heavily offline, practice-oriented service, and core diagnostic and treatment functions are difficult to deliver remotely. While simple patient consultations can be conducted online, formal diagnosis and treatment still require visits to physical medical institutions. Furthermore, the current mainstream patient population has limited familiarity with internet usage. These factors have led to a disconnect between online consultations and actual medical care, resulting in low conversion rates.

(4) Information Security: For existing medical institutions, the transition from hospital information system construction to “Internet Plus” healthcare requires hospitals to evolve from closed internal networks to open networks, shift from physical isolation to integrated internal-external connectivity, and expand from wired-only infrastructure to a combination of wired and wireless systems. This imposes significant demands and requires substantial investment from traditional medical institutions. Without sufficient driving forces, these institutions tend to prefer conservative approaches; therefore, the adoption of internet technologies remains a long and arduous task.

IV. Where Should Internet+ Healthcare Head in the Next Phase?

Based on the development experience in the United States, internet healthcare that is not integrated with offline physical entities has limited growth potential at the current stage. For example, Teladoc, a leading telemedicine company in the U.S., went public in 2015. Its 2016 financial report showed that it had 7,500 corporate and insurance clients, 17.5 million members, and revenue of $120 million, still far from achieving break-even.

The integration of online and offline models will occur across all industries, and the healthcare sector is no exception. After an initial phase characterized by the relatively independent development of online and offline channels, “Internet + Healthcare” is now entering a second phase marked by their mutual integration. Only by making internet capabilities foundational to all healthcare-related entities can the industry advance to a third phase, where technological innovations such as artificial intelligence will substantially improve healthcare delivery.

(1) For internet healthcare enterprises, increasing the supply of qualified medical resources is the leverage point that truly addresses systemic healthcare issues. Whether through deep integration with existing medical institutions or participation in the development of offline medical facilities, this represents an inevitable trend in the second phase.

(2) For traditional medical institutions, the development directions advocated by the state, such as tiered diagnosis and treatment, the construction of medical consortiums, and the family doctor system, all require internet technology as support to achieve effective connection between supply and demand sides, thereby realizing efficient tiered diagnosis and treatment.

“Past the sunken boat, a thousand sails glide by; beyond the diseased tree, ten thousand saplings spring anew.” After navigating the ups and downs of its initial phase, Internet Plus Healthcare has once again garnered endorsement from top-level leadership, ushering in a second, more pragmatic stage. While its progression may not be as rapid as that of other industries, its developmental trajectory is unquestionable. What this process demands is pragmatism, patience, and perseverance.