Investment Insights on Medical Imaging AI: Applications, Trends, Key Investment Considerations, and Product Landscape

Author: Yang Chengkui, Tongdu Capital

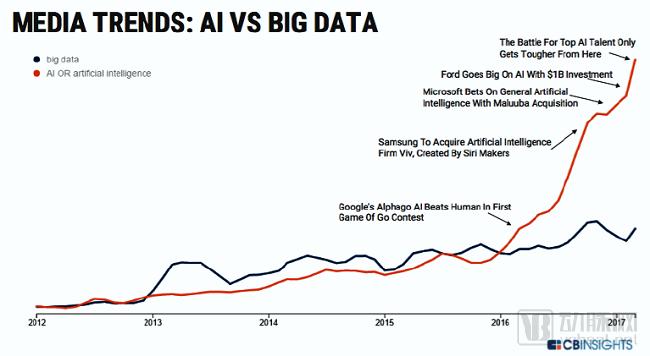

The AI boom in China’s healthcare sector began in the field of medical imaging. Early companies were established around 2016 and, within approximately two years, rapidly completed three rounds of financing, reaching Series B funding amounts in the hundreds of millions of RMB, thereby becoming benchmarks leading industry development. In contrast, startups in overseas markets such as the United States and Israel were mostly founded between 2013 and 2014, about two years earlier than their Chinese counterparts, with some benchmark enterprises having been established for more than five years. However, investment and financing activities in this sector have been relatively less active abroad than in China. Although foreign countries do not hold advantages over China in terms of data volume, market size, policy support, or application potential, their practices in research and market exploration are still a step ahead, making their approaches worthy of reference.

Practical Applications of AI in Medical Imaging:

Among more than 130 overseas medical AI companies collected from public sources, over 20 are specialized in medical imaging AI. These can be broadly categorized into comprehensive medical imaging AI companies and disease-specific medical imaging AI companies.

Comprehensive medical imaging AI companies include Arterys, Zebra Medical Vision, Lunit, Enlitic, AIdoc, and Predible Health. These companies currently apply AI technologies across multiple disease domains. Due to variations in diagnostic approaches and equipment for different conditions, their solutions involve diverse imaging data types, such as X-ray, CT, and MRI, covering diseases of the lungs, liver, bones, breasts, and cardiovascular system.

Arterys stands out as a leader in the field. Founded in 2011, it initially focused on cardiovascular diseases and gradually expanded into pulmonary and hepatic applications. In February 2018, Arterys’ deep learning-based Liver AI and Lung AI oncology imaging suites received FDA clearance for the first time. These tools enable clinicians to rapidly measure and track lesions and nodules in MRI and CT scans, and this FDA clearance covers all solid tumors.

As early as the beginning of 2017, Arterys’ product, Arterys Cardio DL, received FDA approval for analyzing cardiac MRI images. This was the first cloud-based, deep learning–powered analytical software approved by the FDA for clinical use, enabling physicians to perform fully automated yet editable ventricular segmentation and providing accurate calculations of ventricular function. It

The accuracy is comparable to manual segmentation performed by experienced physicians. Based on Arterys’ product offerings, it does not directly provide diagnostic results; instead, it leverages deep learning technology to assist physicians in conducting more precise and efficient intelligent image analysis. Arterys has also demonstrated strong performance in fundraising, completing a $30 million Series B financing round in November 2017 from investors including Temasek Holdings.

Specialty-focused medical imaging AI companies include: HeartFlow, IDx, MedyMatch, Viz, CureMetrix, Bay Labs, Maxwell MRI, and Manchester Imaging.

Numerous companies have emerged in the field of cardiovascular disease, among which HeartFlow is the longest-established. Founded in 2007, its primary product is a hemodynamic simulation software for assisted diagnosis that calculates Fractional Flow Reserve (FFR) using three-dimensional models of the aorta and heart derived from CT scans, representing a breakthrough in the medical diagnosis of coronary artery disease.

This technology received FDA approval as early as 2014; however, in the past two years, HeartFlow has incorporated deep learning techniques, enabling physicians to more accurately assess coronary blockages and blood flow dynamics, thereby facilitating faster and more precise diagnoses. The clinical significance of this solution lies in its ability to reduce unnecessary invasive procedures, thus lowering healthcare costs and patient burden.

HeartFlow also announced in late 2017 that it had secured $150 million in Series E financing. Another company, Bay Labs, applies deep learning to assist in the diagnostic interpretation of cardiac ultrasound images.

In addition to AI applications in cardiovascular disease, Viz and MedyMatch assist physicians in diagnosing stroke from the perspectives of cerebral infarction and intracerebral hemorrhage, respectively. Viz employs deep learning algorithms to automatically analyze brain CTA images for identifying suspected large vessel occlusion strokes; this solution received FDA approval in February 2018. MedyMatch, based on standard non-contrast brain CT scans, utilizes deep learning technology to perform highly sensitive automatic detection of intracranial hemorrhage (ICH) and alerts attending physicians when ICH is detected. Currently, this solution has entered the FDA’s Breakthrough Devices Program.

Furthermore, IDx focuses on AI solutions for ophthalmic diseases such as diabetic retinopathy, glaucoma, and age-related macular degeneration; the FDA has expedited the review process for its AI system for diabetic retinopathy. Manchester Imaging’s AI software can automatically detect early signs of enamel caries that are difficult for dentists to identify with the naked eye, thereby providing timely guidance to prevent subsequent tooth decay. CureMetrix and Maxwell MRI focus respectively on X-ray-based computer-aided diagnosis of breast cancer and MRI-based computer-aided diagnosis of prostate cancer.

In addition to the aforementioned practices, the author has observed that Imagia, a company based in Canada, is attempting to leverage deep learning techniques to mine radiomic biomarkers from routine clinical imaging data that can predict cancer patient prognosis, thereby enabling clinicians and pharmaceutical companies to forecast individualized disease progression and treatment response.

In contrast, within China, several companies have emerged in this field. Initially, early screening for lung cancer and diabetic retinopathy were the most common applications. As the industry has evolved, so too have the strategic directions and focal points of these companies. For instance, after launching its lung cancer early-screening product, Deepwise Medical successively expanded its R&D efforts into thoracic diseases, neurological disorders, and breast cancer, moving toward the development of a comprehensive AI-powered medical imaging platform.

After more than two years of development, leading startups in the industry have gradually emerged, with capital converging toward these top players. Most companies have basically completed their Series B financing rounds, securing cash reserves exceeding RMB 100 million and establishing advantages in accessing medical resources, data accumulation, and brand building. Furthermore, as powerful comprehensive entities such as Tencent and iFlytek continue to intensify their efforts in this field, the medical imaging AI sector has become exceptionally crowded, with increasingly fierce competition. New entrants, if in terms of direction,

Without distinct product differentiation, it will be difficult to gain recognition from users and investors. However, the appeal of the healthcare sector lies in the fact that a “winner-takes-all” outcome is rare, leaving many new opportunities for startups to explore.

2018 Forecast on the Development Trends of AI in Medical Imaging:

1. Regulatory approval in China will accelerate, and a quality evaluation system for imaging AI products prior to market launch is gradually taking shape.

The United States has been navigating the regulatory approval landscape, engaging extensively with industry stakeholders. Its foundational preparations for regulatory approval predated those in China by many years, leading to the successive approvals of AI products from companies such as Arterys, Viz, and Cognoa. In 2017, both the U.S. Food and Drug Administration (FDA) and the China Food and Drug Administration (CFDA) established dedicated review departments specifically for medical AI, underscoring their high level of attention and open stance toward this field. Currently, the National Institutes for Food and Drug Control (NIFDC) has convened meetings on the development of standard test datasets for fundus imaging and lung cancer, publicly soliciting contributions to establish these datasets and objective evaluation methods, thereby advancing pre-market quality assessment of AI-based medical products.

2. Leading companies in the industry will engage in comprehensive competition across medical resources, medical data, talent, and products. With the acceleration of CFDA registration for products, they must consider advancing the commercialization process of their first product.

Over the past two years, the field of medical imaging AI has witnessed remarkable prosperity. Beyond the widely reported victories in human-versus-AI competitions, capital market enthusiasm has surged, driving enterprise valuations steadily upward. If, over the previous two years, the industry’s overall understanding remained confined to speculative perceptions of AI’s potential in healthcare, then this year, investors—particularly those participating in Series C rounds—are likely to prioritize several critical questions: Can visible products withstand public scrutiny? Can they be genuinely integrated into clinical workflows? And what forms will their commercialization take? Failure to address these issues raises serious concerns about how companies can justify their elevated valuations.

If the entire industry fails to deliver, will it trigger a phase of pessimism, and will the legendary “bubble burst” scenario play out once again? The author holds a somewhat more optimistic view. Unlike mobile health, medical AI is distinguished by both technological and business model innovation. This wave of development in medical AI is driven by technology and data, featuring high entry barriers. Its impact on healthcare lies primarily in enhancing productivity—a resource that is particularly scarce in the medical sector—thereby making AI’s value proposition for healthcare even more significant.

Mobile healthcare, by contrast, focuses more on optimizing production relations. Since these relations are constrained by institutional frameworks, they cannot be resolved through technology alone. Another key difference lies in the broader macroeconomic environment. The previous downturn in mobile healthcare was triggered by a stock market crash, tighter capital conditions, and a lack of favorable policy developments. In contrast, the current landscape is characterized by the advancement of artificial intelligence as a national strategy, new supportive policies for strategic industries such as AI in the A-share market, and ample, active capital—including state-owned funds. Overall, the macro environment remains conducive to the development of medical AI in the short to medium term.

3. New startups will emerge in more niche sectors, with deep vertical specialization likely to become the primary strategic choice

In the early stages, when AI was first applied to medical imaging, acceptance among physicians was low, with some maintaining skeptical or resistant attitudes. However, as AI’s clinical performance continues to improve, high-quality academic research on AI by physicians keeps emerging, and broader environmental factors come into play, an increasing number of doctors will shift from passive adoption to actively embracing AI. This transition will unlock greater clinical demand and create more opportunities in specialized subfields.

However, high demand is not necessarily a boon for startups. If a startup merely seeks to leverage AI technology to address numerous clinical needs by attempting to tackle them all, without developing products or services that constitute a distinct competitive advantage, it will remain confined to the role of a technical service provider, making it difficult to generate substantial commercial value. In the face of competition from industry leaders and internet giants, only by carving out differentiated new domains and deepening expertise to establish a strong advantage can a company respond with greater ease.

Competition. Due to the complexity of diseases, different diagnostic modalities are often required in clinical practice for the same disease. Conversely, a single diagnostic modality may be applicable to multiple distinct diseases. Therefore, from the perspective of AI application implementation, there are two strategic approaches. One approach is disease-centric, such as developing an integrated AI solution for breast cancer diagnosis by combining mammography, ultrasound, and MRI. The other approach is modality-centric, such as leveraging CT imaging to diagnose various conditions affecting the lungs, liver, brain, and other organs. Regardless of the chosen entry point, it is essential to comprehensively consider factors such as pain points, data infrastructure, and commercial potential.

Practical Applications of AI in Medical Imaging:

In addition to AI applications in medical imaging, there is another category of data applications in the healthcare field that can be collectively referred to as medical image-based applications. Although these data do not constitute structural or functional images directly acquired by imaging equipment, they can be converted into digital images interpretable by computers. For instance, digitized microscopic fields of view from clinical laboratory and pathology departments, as well as images derived from electrophysiological signals such as electrocardiograms (ECG) and electroencephalograms (EEG), all present opportunities for intelligent analysis and interpretation powered by AI.

For instance, Paige.AI, which secured $25 million in funding in February 2018, leverages AI to assist in the diagnosis of breast and prostate cancer through digital pathology images. However, there is a significant gap between China and other countries in the development of pathology. Abroad, pathologists enjoy the prestigious status of “doctors’ doctors,” whereas in China, pathology departments are often at a disadvantage compared to other specialties in terms of staffing, informatization, and institutional priority. Some hospitals even have pathology departments established but lack the capability to perform relevant diagnostic services. Although pathology serves as the gold standard—highlighting its critical importance—the complexity of pathological diagnosis and the scarcity of pathologists present areas where AI can demonstrate distinct advantages. Nevertheless, companies must still explore viable implementation pathways; integrating models such as government-promoted third-party services and telepathology may offer one potential approach.SigTuple, an Indian company backed by Accel Partners, applies deep learning to the intelligent analysis of peripheral blood smears, urine, and semen samples in hospital laboratories. In contrast to SigTuple, which serves healthcare institutions, the U.S.-based company Athelas targets patients directly by providing home-based blood testing services. Using a device provided by Athelas, patients need only collect a single drop of capillary blood from a fingertip to receive laboratory-grade blood analysis results within 60 seconds. This solution enables cancer patients to monitor their recovery at home, allowing physicians to optimize treatment plans and promptly identify increased infection risks associated with chemotherapy.

Athelas has optimized cancer therapies through deep learning technology and secured funding from investors such as Sequoia. The ECG Analysis Platform, developed by the French company Cardilogs, leverages neural network technology to analyze Holter monitor data, enabling cardiologists to rapidly and accurately diagnose heart conditions. Having obtained both FDA and CE certifications, the platform is poised to accelerate its commercialization in the United States and Europe. In China, Lepu Medical’s “AI-ECG Platform,” an AI-based automated ECG analysis and diagnostic system, has had its medical device registration application accepted by the FDA for review. This platform utilized approximately 25 million ECG data samples derived from 300,000 patient ECG examinations to train its deep convolutional neural network models.

In light of developments in this field both domestically and internationally, this analysis focuses on cardiovascular and cerebrovascular diseases from a disease perspective, and on ultrasound diagnosis and digestive endoscopy from a diagnostic modality perspective. Cardiovascular and cerebrovascular diseases affect a large patient population with high incidence rates, pose significant diagnostic challenges, and require timely diagnosis after onset, with medical imaging serving as the primary auxiliary diagnostic tool. Ultrasound, being non-invasive and radiation-free, is seeing increasingly broad application; however, there remains a scarcity of highly skilled sonographers. While AI has the potential to address this shortage, the lack of standardization in ultrasound imaging increases the difficulty of AI implementation, posing greater challenges for startups. Endoscopy is the gold standard for diagnosing digestive system diseases. With the development and application of capsule endoscopy, the volume of data has surged, increasing the difficulty and time pressure associated with manual diagnosis. AI may help alleviate this situation. Additionally, attention is maintained on AI applications in the fields of pathology, laboratory testing, and physiological signal analysis.

QR Code for Offline Salon Registration