CB Insights Report: With U.S. Healthcare Spending at $3 Trillion, Patient-Centricity Emerges as the Key to Success

High-deductible health plans in the United States, coupled with rapidly advancing new technologies, are transforming patients into savvy healthcare consumers. In response to their heightened expectations for services and experiences, companies are implementing various changes.

In recent years, industries ranging from IT enterprises to financial services have shifted toward a consumer-centric model. They have focused on enhancing the user experience of their products and implemented numerous user-oriented policies to attract more potential internet users.

In the healthcare sector, this transformation has progressed relatively slowly. Burdened by stringent regulatory pressures, healthcare companies have failed to recognize the existential threats they face. However, with the enactment of the American Health Care Act, coupled with higher deductibles and advancements in new technologies, user experience has gradually become a core element for healthcare enterprises to redefine their strategic positioning.

From remote wearable devices to telemedicine services, companies are increasingly focusing on the technology itself, exploring how it can enhance patient experience by making it more user-friendly, affordable, and customizable.

This report focuses on analyzing how the healthcare industry adopts a patient-centric approach, the barriers to new models, key players in this field, and development trends in the interactivity between patients and health information systems.

Promoting the Trend of Consumerization in Healthcare

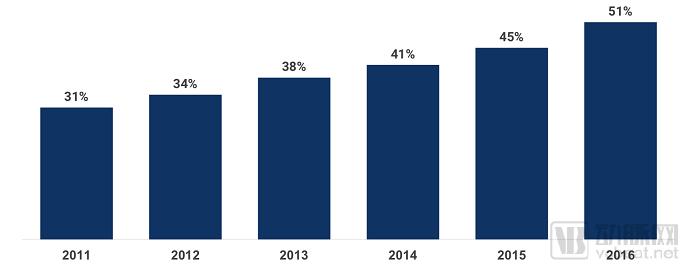

The annual rise in medical costs is no secret. Last year, U.S. healthcare spending reached $3 trillion, accounting for more than 17% of the nation’s GDP. According to the Milliman Medical Index, the average annual medical expenses for a family of four in the United States have been increasing by $1,000 per year, reaching nearly $27,000 in 2016.

Governments, insurers, and enterprises all aim to reduce costs by encouraging patients to consume healthcare services more rationally. To this end, they have introduced high-deductible health plans, which require patients to pay more out-of-pocket before their insurance coverage takes effect. In this scenario, patients become more price-sensitive regarding medical services, carefully evaluating differences among various options based on factors such as price, quality, and convenience, ultimately making more informed and rational choices.

(Figure 1: Annual deductibles exceeding $1,000)

The proliferation of smartphones has also facilitated healthcare consumption. Mobile devices enable individuals to monitor their health status outside of hospital settings, particularly with the widespread adoption of wearable devices. These devices can collect patient data and synchronize it with mobile devices, allowing users to access their health information at any time after tracking and analysis.

Furthermore, mobile devices offer enterprises opportunities to develop new business models. For instance, in telemedicine, users can take out their smartphones anytime and anywhere to communicate with doctors.

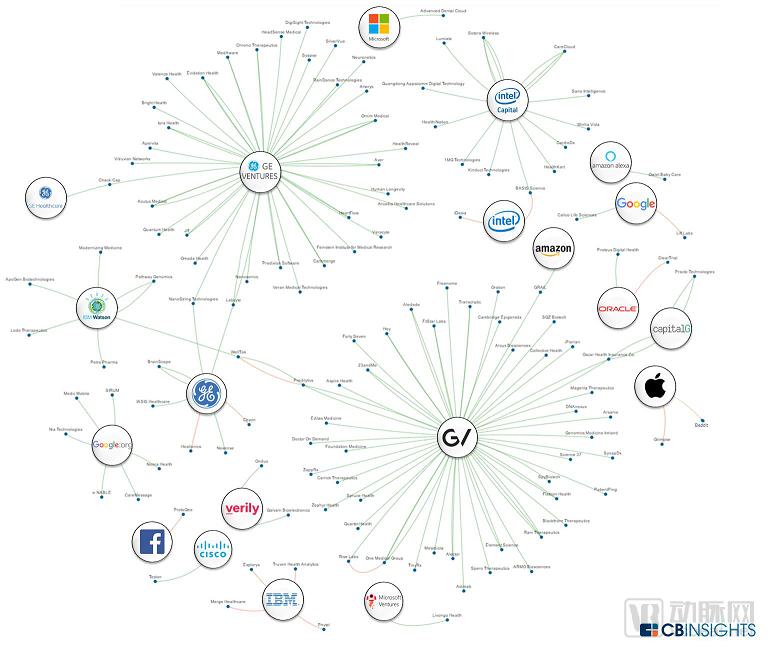

Given their direct connections with patients and robust research and development capabilities, major technology companies such as Apple and Google are seeking opportunities to enter the consumer health market. Companies like Google, Apple, and General Electric have begun investing in healthcare startups or prioritizing strategic initiatives in medical innovation.

(Figure 2: Layout of Tech Giants in the Healthcare Sector)

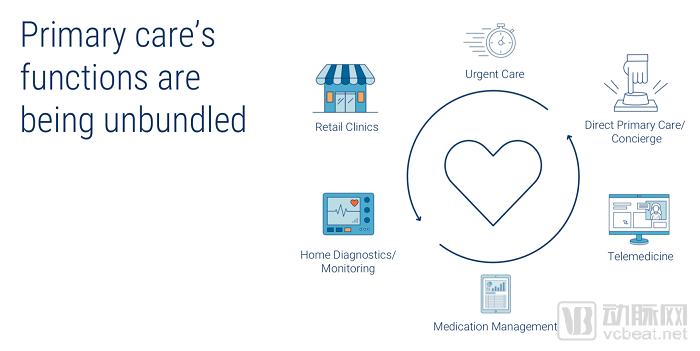

These tech giants and startups, with their focus on user experience, are gradually beginning to use primary care as an entry point into the healthcare market, since primary care serves as the threshold for most consumers accessing health information systems. Meanwhile, primary care services remain significantly scarce, particularly in remote mountainous regions.

These companies view this as an opportunity, aiming to leverage technology to deliver patient-centric services to underserved regions and populations.

(Figure 3: Functional Classification of Primary Care)

Classification of Primary Care

People are beginning to use health information systems in new ways, rather than solely seeking assistance from community physicians at community hospitals or pursuing treatment at hospital emergency and outpatient departments. New patient-facing channels and tools can offer more options based on the severity of patients’ conditions, their ability to pay, and their schedules.

Before seeking medical treatment, individuals should first understand what is wrong with their bodies. Through monitoring and diagnostic tools, users can proactively track their health status and contact their physicians when issues arise.

Patient data may be derived from diagnostic tests, wearable devices, and other sources. By providing more comprehensive health data, users enable healthcare professionals to better assess disease risk and determine the necessary personalized treatment plans.

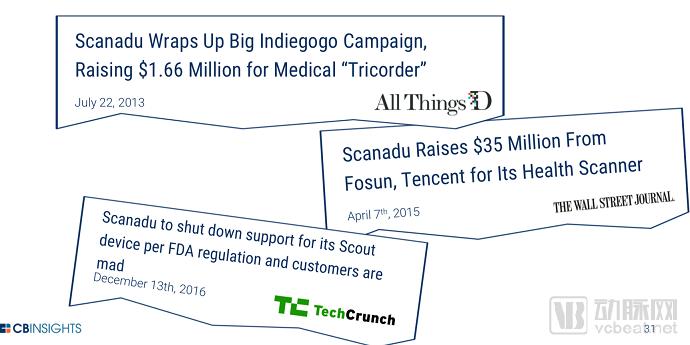

Not all companies have had smooth sailing. Fitbit and Scanadu encountered numerous difficulties in the diagnostics and monitoring sectors. Fitbit’s stock price plummeted because a lack of innovation prevented it from providing patients with more meaningful health data. Meanwhile, Scanadu raised funds to develop a diagnostic device, but contrary to expectations, it ultimately failed to secure FDA approval.

(Figure 4: Major News Events of Scanadu)

If clinical data or health management data are a concern for these companies, they will inevitably be subject to regulation by organizations such as the U.S. Food and Drug Administration (FDA). However, regulatory oversight also serves as a powerful form of endorsement. Once FDA approval is obtained, healthcare professionals are more likely to trust the data generated by patient-side devices. Meanwhile, the FDA’s new regulations continue to expand and adapt to accommodate an increasing array of novel medical devices and tools.

Recently, the United States passed a low-profile yet far-reaching piece of legislation: the Over-the-Counter Hearing Aid Act of 2017. This law will allow hearing aid manufacturers to bypass physicians and sell directly to patients without a prescription.

The FDA is creating a fast track for approving these low-risk wearable devices and tools that can generate clinical data, thereby enabling their products to be sold directly to patients.

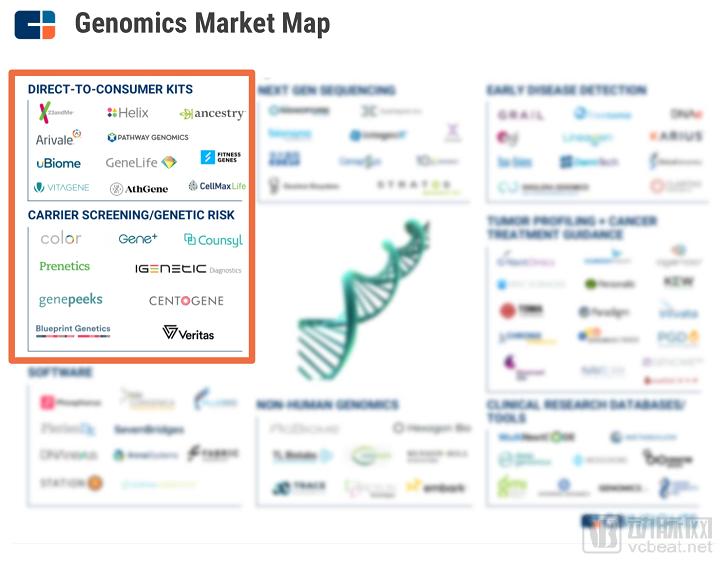

In the realm of diagnostics, 23andMe has launched consumer-grade genetic sequencing products. Many startups in the consumer genetic sequencing space are securing funding, blurring the lines between diagnosis and prediction while establishing direct relationships with patients.

(Figure 5: Gene Market Layout)

Now, we have new genetic information and clinical data from FDA-approved wearable devices, such as Kinsa and Cue, which can predict conditions like influenza and obesity by monitoring changes in temperature and hormone levels. All these tools can be used for prediction, enabling patients and healthcare providers to leverage personalized data to inform medical decisions.

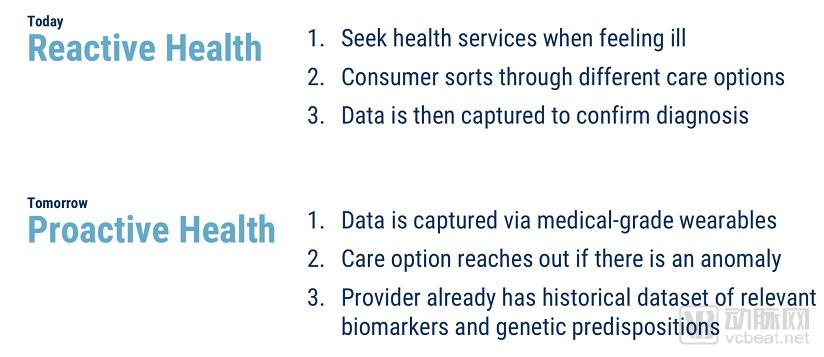

This is the first step toward proactive healthcare and away from passive health management.

Once abnormalities appear in a patient’s health data, the software tool can promptly alert healthcare providers, who then contact the patient to determine whether any physical anomalies have occurred. In contrast, patients typically seek medical attention only after they become ill.

(Figure 6: Proactive Healthcare and Reactive Healthcare)

Some retail clinics have gradually expanded their operations from selling health products to providing medical services. These services include STD testing, vaccinations, microbial culture tests, and other preventive health screenings.

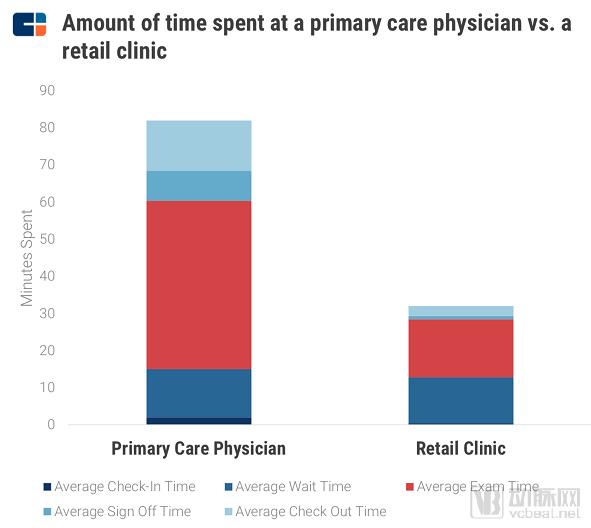

Patients spend significantly less time visiting clinics than community hospitals, as most individuals are already aware of the reason for their visit or the specific tests they require. Retail clinics provide targeted medical services that enable rapid testing, thereby reducing the time spent on each visit.

(Figure 7: Comparison of Time Spent by Patients in Primary Care and Retail Clinics)

Nowadays, retail clinics are becoming increasingly prevalent, such as CVS’s “MinuteClinic” locations housed within Walgreens, Kroger, and Walmart stores. This business model signifies that these traditional retailers are beginning to explore new operational frameworks and seek fresh avenues for growth, with the healthcare industry emerging as a newly identified market opportunity.

An increasing number of companies are viewing these retail clinics as new sales channels and are seeking ways to expand the types of care patients can access at local pharmacies. This includes introducing telehealth kiosks and additional diagnostic tools to measure patients’ temperature, weight, and biometric indicators.

However, this is a difficult market to penetrate, as it involves high venue rental and maintenance costs, while companies must also figure out how to ensure these services truly attract consumers.

Some well-funded clinics have been forced to close, such as HealthSpot. However, there have also been more successful cases, such as Pursuant Health and Higi.

(Figure 8: Introduction to Selected Companies)

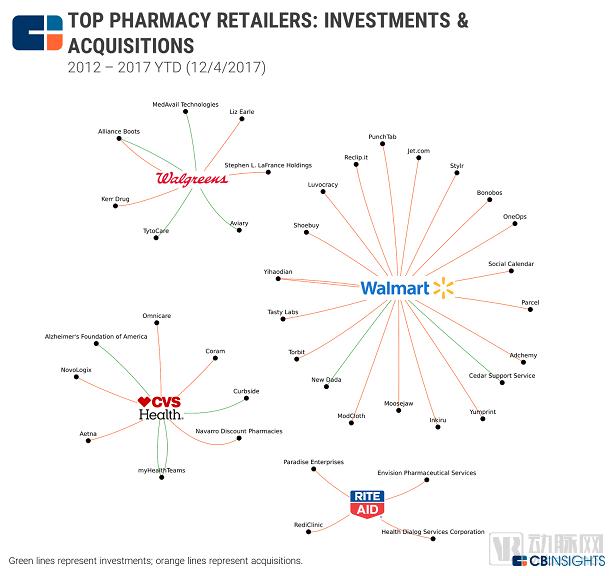

On December 3, 2017, CVS Health, the U.S. retail pharmacy giant, announced its $69 billion acquisition of Aetna, the third-largest health insurer in the United States. This move has drawn attention to the development of retail clinics within the healthcare sector. CVS has stated that its vision is to leverage digital tools, such as mobile apps and medication adherence solutions, to help patients improve their health outcomes. With this acquisition, the combined CVS-Aetna entity will be better positioned to expand in this area.

This acquisition will compel other retail pharmacies to take action. While some of them are already active investors in the personalized medicine market, this move may prompt them to pursue larger and more ambitious initiatives. CVS Health itself is focusing on the consumer market to strengthen its core pharmacy business, while also placing greater emphasis on telemedicine, health analytics, and medication delivery tools to help manage patients’ health outcomes.

(Figure 9: Layout of Pharmaceutical Retailers)

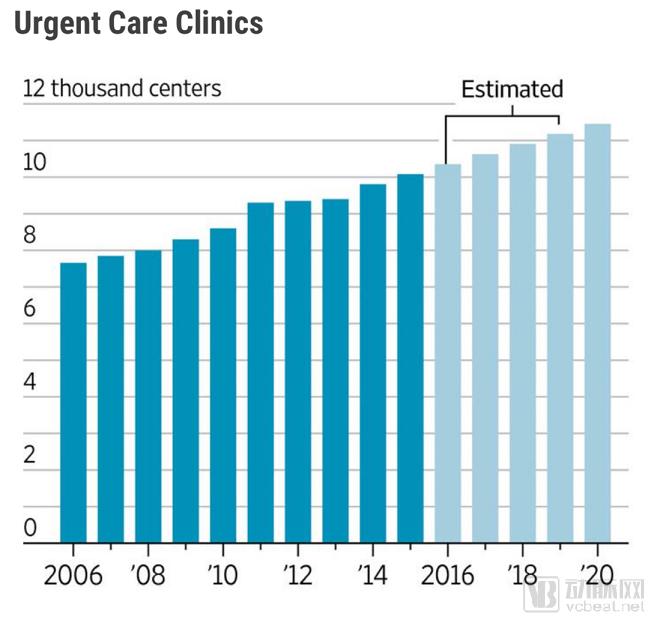

Urgent care clinics may serve as a middle ground between traditional community hospitals and costly emergency departments. These clinics can treat urgent but non-life-threatening conditions, typically without incurring the high costs associated with emergency room visits. Moreover, in most cases, urgent care clinics enable patients to see a physician more quickly than going directly to a hospital.

Meanwhile, urgent care clinics are much smaller than emergency departments; their operation typically does not require costly investments in medical equipment and staffing, and they may refuse to treat uninsured patients (unlike emergency departments).

Nowadays, driven by growing patient demand and the convenience they offer, the number of urgent care clinics is steadily increasing. This trend aligns with government objectives, which aim to encourage individuals to seek emergency department services only when truly necessary. As more urgent care clinics emerge, they are increasingly competing on price, convenience, and user experience.

(Figure 10: Number of Urgent Care Clinics)

For some investment firms, urgent care clinics have long been an attractive investment target, as they recognize the opportunities presented by streamlined operations, interconnected clinic networks, and improved efficiency through standardized processes and tools. Recently, Warburg Pincus acquired CityMD at a $600 million valuation.

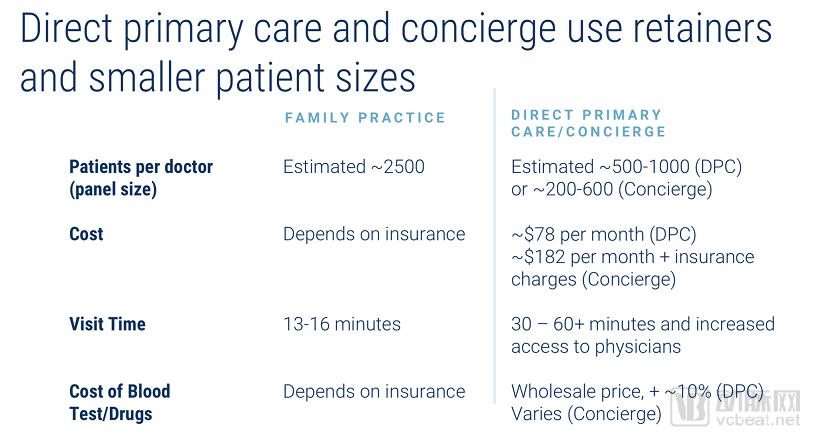

Direct Primary Care (DPC) and Concierge Medicine operate on a fixed-fee basis, charged monthly or annually, enabling patients to establish a dedicated relationship with a specific physician or clinic. Both models cater to a small patient panel under a fixed-fee structure, distinguishing them from traditional family practice.

Concierge medical practices typically charge both patients and health insurance companies, thereby ensuring compliance with health insurance regulations. In contrast, direct primary care requires only a single upfront payment and completely avoids insurance-related requirements.

Both direct primary care and concierge medicine utilize fixed fees to secure a defined patient panel for clinics and generate a recurring, predictable revenue stream. Patients are afforded ample time to interact with physicians during visits, except in special circumstances. The fixed fee typically covers consultation charges, although some clinics offer an all-inclusive package price with no additional fees.

(Figure 11: Comparison of Directed Primary Care/Contracted Medical Services and Home-Based Diagnosis and Treatment)

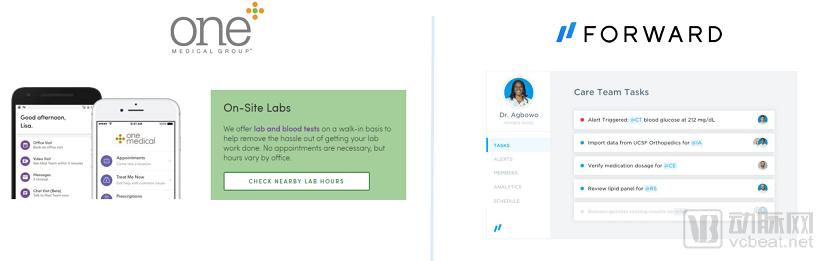

These new types of clinics are starting from the grassroots level, relying on third-party services to enhance user experience. Companies like One Medical and Forward have their own electronic medical record systems and mobile apps. By leveraging these tools, physicians can better manage their patients.

Additionally, they also promote and sell clinic subscription services through enterprises as employee benefits.

(Figure 12: One Medical and Forward)

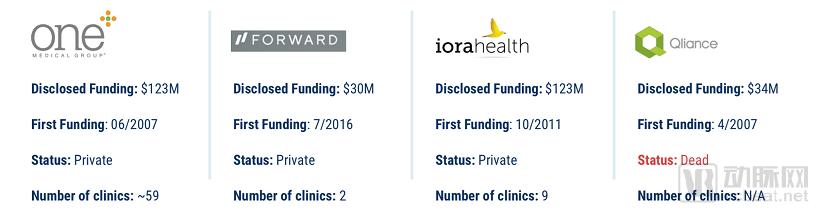

Both direct primary care and concierge medicine are based on small patient panels, enabling them to deliver consistent, high-quality, and highly personalized medical services. However, this model also makes it difficult to scale up. Some well-funded companies have gone bankrupt, such as Qliance, while other medical practices have remained highly successful after more than a decade in operation.

(Figure 13: Overview of Targeted Primary Care Companies)

In some remote areas, telemedicine can help physicians expand their reach of care. Telemedicine enables doctors to conduct postoperative monitoring to prevent patient readmissions. Furthermore, it facilitates remote follow-up consultations.

In the United States, an increasing number of regions have enacted telemedicine-related laws to ensure that telemedicine is as effective as in-person initial consultations.

In 2014, telemedicine companies experienced a surge in financing, but growth stagnated by 2017. This may be partly attributed to uncertainties surrounding business models. Even well-funded telemedicine companies have struggled to reverse this trend.

Teladoc is one of the early startups in this field. After struggling in its first few years, its business began to gradually climb. Teladoc is attracting more people to access telemedicine services, but the actual usage rate has never exceeded 5% (although it continues to grow steadily).

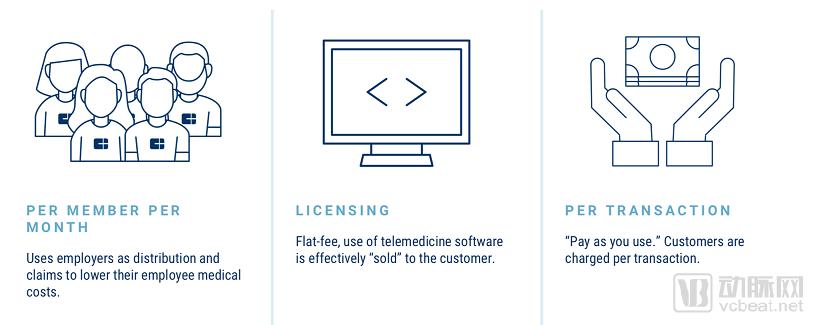

During the first wave of the telemedicine boom, these companies’ revenue models fell into three main categories:

First, by having enterprises subscribe to telemedicine services and claiming that this can reduce employees' medical expenses; second, by charging for hardware, selling devices such as tablets to users when they use telemedicine software; and third, by charging a fee for each telemedicine consultation.

However, this model is not sustainable in the long run, as its target users are primarily healthy individuals, and the enterprise-facing market is already saturated with lengthy sales cycles. For consumers, physicians’ advice remains crucial, so they are less sensitive to service costs.

(Figure 14: Service Model of the First Wave of Telemedicine)

Now, a new wave of telemedicine is gaining momentum.

Digital healthcare encompasses a suite of tools, including wearable devices, chat applications, and online portals. As an integral component of digital healthcare, telemedicine is seeing a growing number of products enter the market.

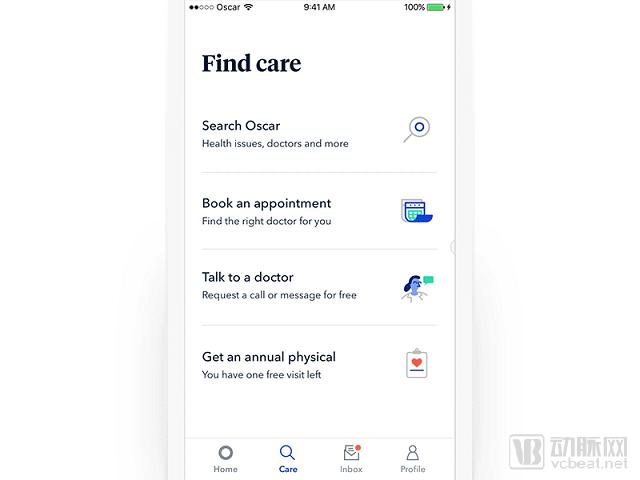

Meanwhile, the FDA has also begun to support digital therapeutics companies. On October 6, 2017, the FDA issued the first prescription-based regulatory framework for digital therapeutics. As telemedicine is covered under insurance plans, Oscar and other insurers assume the financial risk of providing telemedicine services to their enrollees.

However, with the widespread adoption of value-based care models and the growing popularity of Accountable Care Organizations (ACOs), telemedicine has become a strategic wager, exposing hospitals to greater risk. Yet, alongside this risk, telemedicine has helped hospitals attract more physicians and better manage patients’ chronic conditions.

(Figure 15: Oscar Company)

Currently, an increasing number of companies are attempting to streamline the process for consumers to obtain prescriptions and secure physician renewals by offering last-mile delivery services and contracted medical consultations.

Some virtual pharmacies also offer medication consultation services, with dedicated service teams responsible for dispensing medications, handling insurance claims, and managing packaging to simplify the use of complex drug regimens. Some companies attract more consumers to their platforms by reducing medication costs while maintaining full transparency in the dispensing process. Others adopt different approaches, such as smart pillboxes and bottles, leveraging smartphones and machine sensing technologies, and developing ingestible sensors to monitor patients’ medication adherence.

However, relying solely on smart devices to remind patients to take their medication may not be sufficient, so many hardware companies bundle this service with their products for sale.

(Figure 16: Selected Medication Management Devices)

Pharmacy benefit management (PBM) firms have viewed medication adherence as a promising opportunity. Express Scripts recently invested in Mango Health, a startup focused on medication adherence. This marks the company’s first investment since 2012. Additionally, it has entered into a partnership with Propeller Health, a company specializing in smart inhalers for asthma.

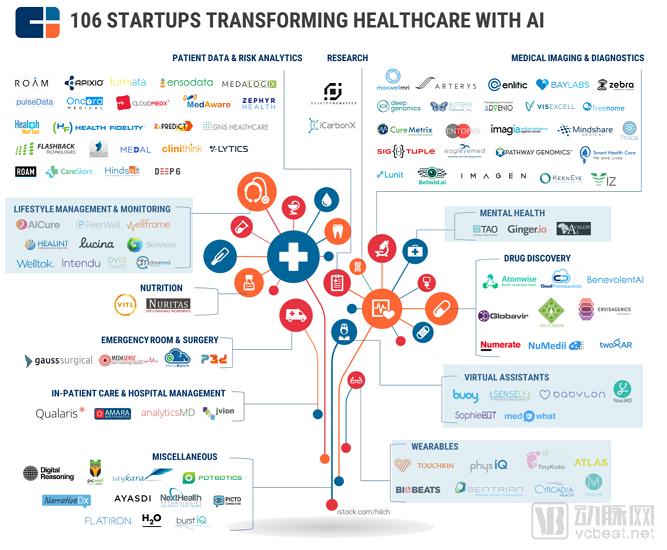

AI startups are delving into various segments of healthcare, ranging from preventive care to virtual assistants. These startups aim to shape new patterns of interaction between patients and the healthcare system.

For example, they leverage home robots to assist patients with Alzheimer’s disease in medication management and even provide long-term companionship services. Their chatbots guide patients to the appropriate care settings through conversational interfaces, although this depends on the ease with which patients can formulate their questions.

Artificial intelligence builds bridges between data, while wearable devices provide physicians with actionable information; their integration enables physicians to deliver proactive care.

Currently, both Google and Apple have conducted in-depth explorations in this area. Google has developed an algorithm that yielded conclusions largely consistent with those of eight ophthalmology experts who screened for diabetic retinopathy based on more than 9,000 images.

Apple aims to build a health platform in users’ pockets by integrating devices, personal health records, and applications.

(Figure 17: Overview of Companies in the AI Healthcare Sector)

Looking Ahead

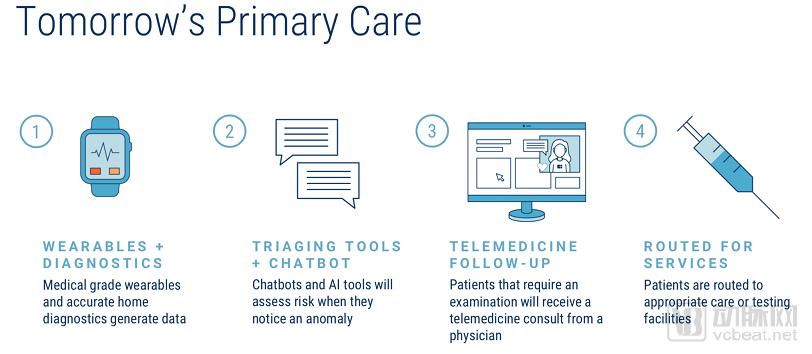

In the future, primary care may adopt the following models:

1. Wearable Devices + Diagnostics: Medical-grade wearables and precise home diagnostic data.

2. Tools and Chatbots: Chatbots and artificial intelligence tools assess risk when patients experience abnormalities.

3. Telemedicine Follow-up: Patients requiring examination receive telemedicine consultations from physicians.

4. Allocation of Medical Services: Patients are assigned to appropriate care or undergo corresponding examinations.

(Figure 18: Future Primary Care Model)

Original Report: VBInsights - "CONSUMERIZATION OF HEALTHCARE"

Download link: https://www.cbinsights.com/research/consumer-healthcare-relationship-expert-intelligence/