China's Biologics Industry Report Following the Zero-Tariff Policy on Anti-Cancer Drugs

Sinocare

Rapid Detection of Chronic Disease: Product R&D, Production, and Sales

On the morning of March 20, following the closing session of the First Session of the 13th National People’s Congress, Premier Li Keqiang stated in response to questions from Chinese and foreign journalists that “for certain consumer goods in high market demand, including pharmaceuticals—particularly anti-cancer drugs urgently needed by the public and patients—we will substantially reduce import tariffs, striving to bring the tariff rate on anti-cancer drugs down to zero.” This indicates that the scale of anti-cancer drug imports into China is expected to increase significantly in the future.

According to data from the National Health and Family Planning Commission, the number of cancer patients in China has exceeded 4.5 million, with approximately 2.8 million cancer-related deaths annually. This large patient population has spurred a substantial market for anticancer drugs. According to officials from the Southern Institute of the China Food and Drug Administration (CFDA), the market size for anticancer drugs in China reached RMB 126.8 billion in 2017, with a compound annual growth rate (CAGR) of 14.27% over the previous three years. The anticancer drug market represents a major consumption segment for biological products. The considerable demand for anticancer medications, coupled with the trend toward zero tariffs, will significantly increase imports of related biological products and optimize the supply structure of biological products in China.

Biologics offer advantages such as minimal toxic side effects, low drug resistance, and high specificity, making them favored by healthcare institutions and patients. In 2017, the global biologics industry experienced robust growth, with the number of newly approved drugs returning to historical highs. The market size expanded at a rate significantly higher than that of chemical drugs, particularly with monoclonal antibody-based new drugs emerging as a sales hotspot.

China’s biopharmaceutical industry is generally in an upward trajectory, with a steady increase in the number of newly approved drugs. Sales revenues for both therapeutic and preventive biologics have reached record highs. Looking ahead, the biopharmaceutical sector is expected to maintain its growth momentum, while its industrial structure will undergo further adjustment. Anti-tumor biologics are poised to become the primary driver of growth, with the market size projected to reach RMB 28 billion by 2020.

Report Description:

This report primarily employs a literature review methodology. By analyzing relevant data published by institutions such as the FDA, CFDA, CDE, UpToDate, and Healthcare IT News, it presents the current development status of the biologics industry both domestically and internationally.

Key Findings

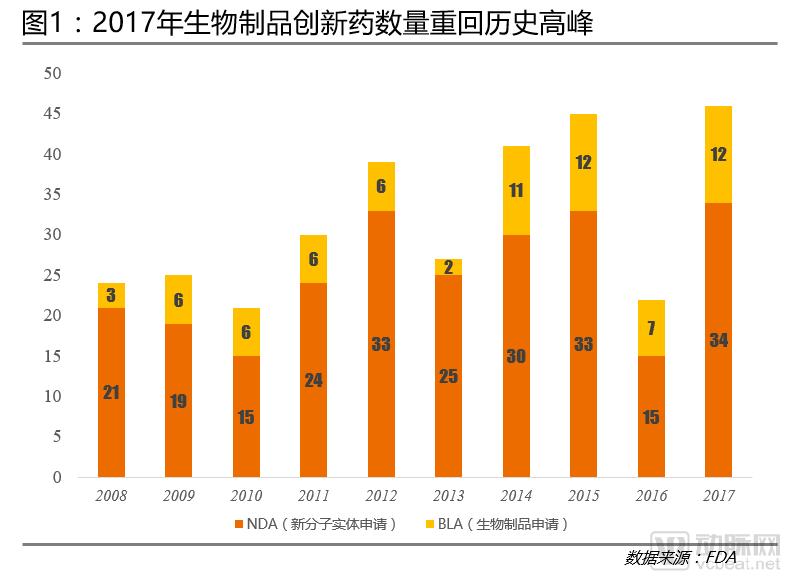

The Number of New Global Biologics Drugs Returned to a Historical Peak in 2017

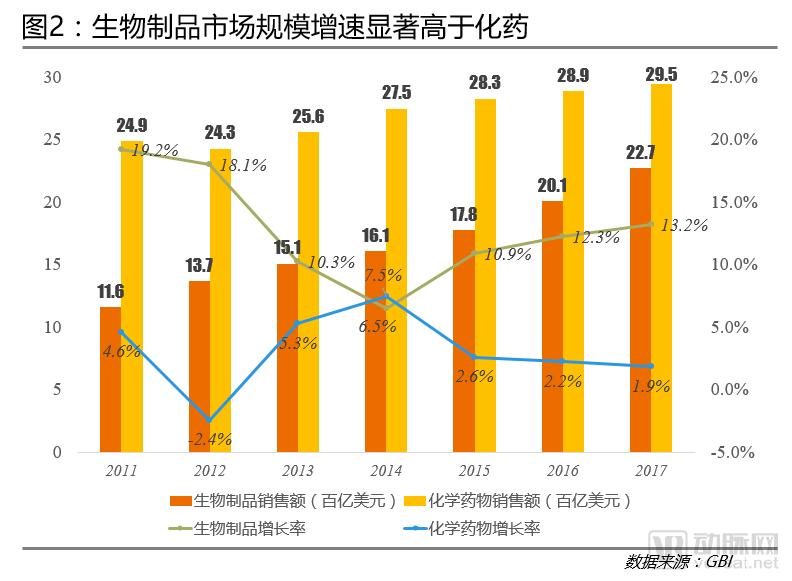

In 2017, the market size of biological products grew by 13.2%, significantly higher than that of chemical drugs.

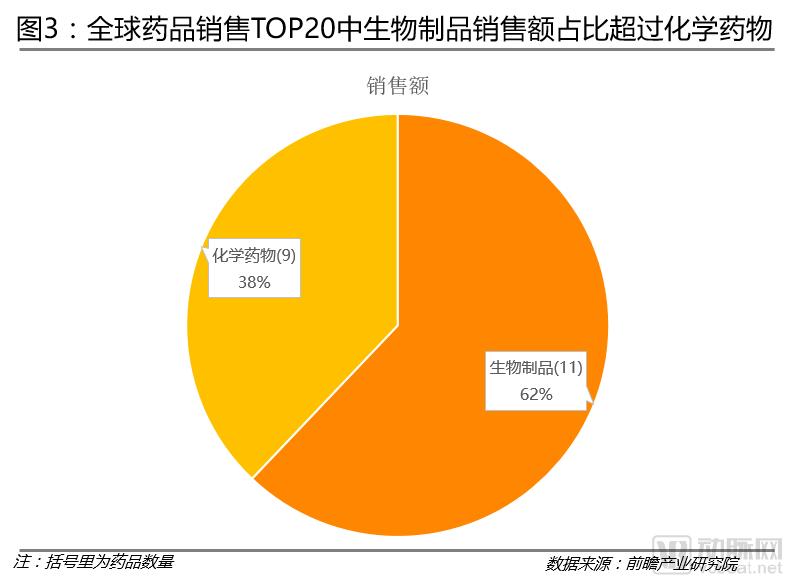

Among the Top 20 Global Pharmaceutical Products by Sales, Biologics Outpace Chemical Drugs in Revenue

Therapeutic biologics dominate, with monoclonal antibodies becoming the hotspot for R&D and sales

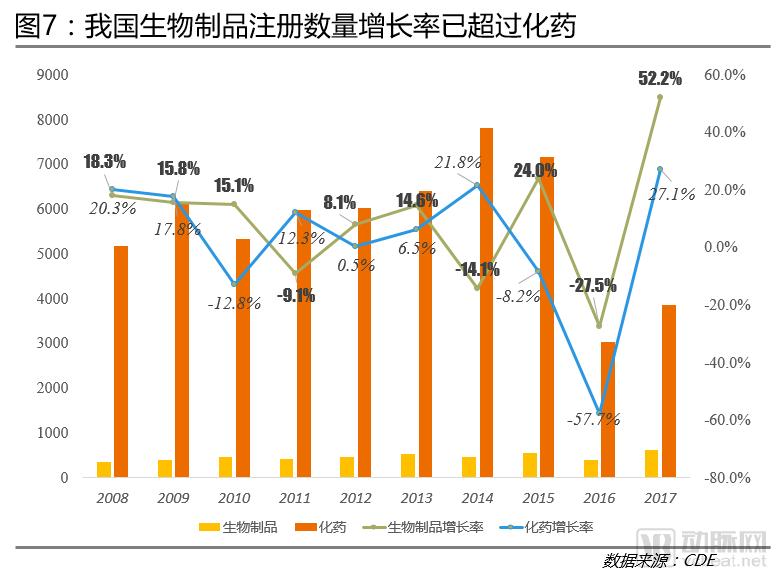

The growth rate of biological product registration in China has surpassed that of chemical drugs.

Biological product manufacturers in Beijing, Shanghai, and Guangzhou account for approximately one-third of the total number of enterprises nationwide.

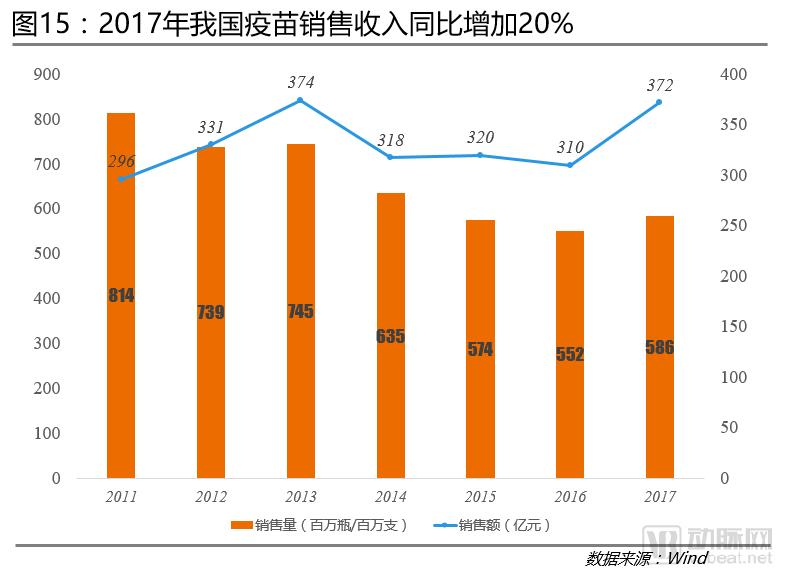

In 2017, China's vaccine sales revenue increased by 20% year-on-year.

The 21st century is the century of biology. With the rapid development of bioengineering, immunology, cytology, and other fields, the biopharmaceutical industry has entered a golden age of growth. As a crucial component of this industry, biological products are also embracing significant opportunities for development.

Biological products are primarily derived from microorganisms, cells, and various animal- and human-derived tissues or fluids obtained through genetic engineering, cell engineering, protein engineering, and other biotechnological methods. Unlike conventional pharmaceuticals in their mechanism of action, biological products mainly enhance the body’s immune competence by stimulating the human immune system to produce immune effectors, thereby effectively combating various diseases.

Based on their intended uses, biological products are primarily categorized into therapeutic biological products, prophylactic biological products, and diagnostic biological products, with the first two categories accounting for more than 95% of the entire market. Therapeutic biological products are mainly used for disease treatment and include various antibody-based drugs and blood products; prophylactic biological products are primarily used for the prevention of various infectious diseases, consisting mainly of vaccines.

In 2017, the entire biological products industry experienced rapid development. The number of newly approved biological products worldwide returned to a historical peak, with the market size increasing by 13.2% year-on-year, significantly higher than the growth rate of chemical drugs during the same period. The composition of biological products underwent adjustments, with preventive biological products growing rapidly and narrowing the gap in market share compared to therapeutic biological products. Meanwhile, China's biological products industry as a whole was also on an upward trajectory, with the number of new drug approvals gradually increasing. The growth rate of biological product registrations surpassed that of chemical drugs, and sales revenues for both therapeutic and preventive biological products reached record highs. Among these, monoclonal antibody-based drugs became the best-selling biological products.

This report provides a comprehensive analysis of the current characteristics of the biologics industry, both domestically and internationally, covering market size, number of new drug applications, structural changes, and therapeutic areas. Based on the current industry landscape, it also forecasts the future development of the biologics sector.

The Number of New Biologics Hits a Historic High Again, with Monoclonal Antibodies Becoming the Focus of R&D and Sales

Biologics Volume Returns to Historic Peak:An analysis of FDA new drug approval data over the past decade reveals an overall upward trend in the number of new drugs. According to official FDA announcements, the Center for Drug Evaluation and Research (CDER) approved 12 innovative biological products in 2017, returning to a historical peak. This surge is primarily attributed to technological advancements that have improved the extraction quality of bioactive substances and optimized the synthesis of biological organic compounds, enabling the production of a wider variety of biological products to meet the therapeutic needs of different diseases. Furthermore, compared with chemical drugs, biological products are associated with lower patient drug resistance and fewer toxic side effects, making them more favored by patients.

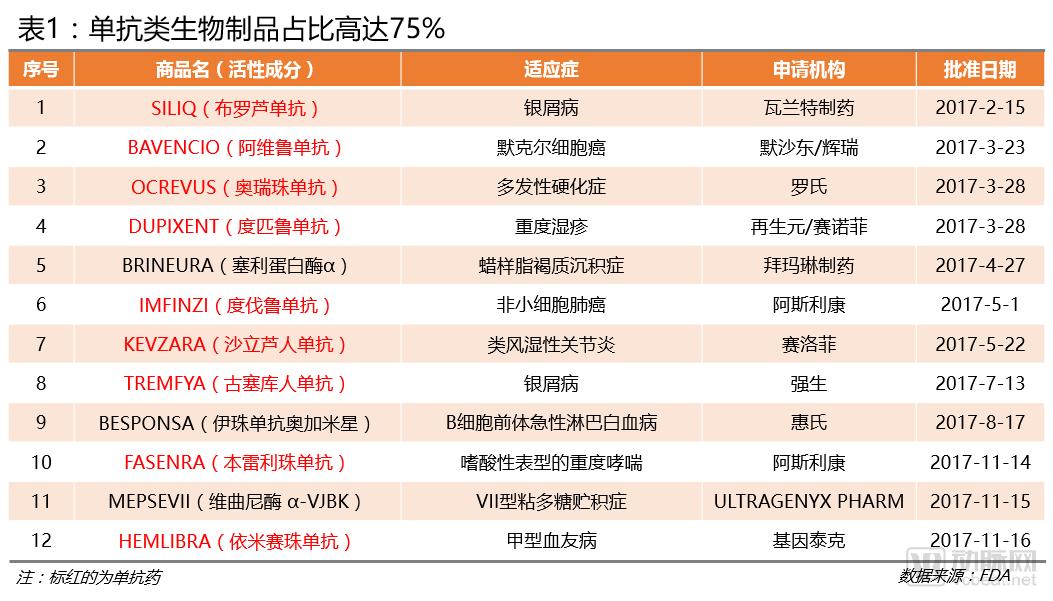

Monoclonal Antibody New Drugs Are the Most Numerous:According to the list of biologics approved by the FDA in 2017, there were nine monoclonal antibody drugs, accounting for as high as 75%. SILIQ (brodalumab), manufactured by Valeant Pharmaceuticals of Canada, became the first new monoclonal antibody drug to receive FDA approval in 2017. Brodalumab is a novel fully human monoclonal antibody that binds to the interleukin (IL)-17 receptor, blocking the binding of multiple IL-17 cytokines to their receptors and inhibiting inflammatory signal transduction. It is primarily indicated for the treatment of psoriasis, an autoimmune skin disease. According to data published by the WHO, the prevalence of psoriasis among the global adult population is 2%–4%, with plaque psoriasis being the most common form, accounting for up to 90% of cases.

From the perspective of applicant companies, Sanofi and AstraZeneca each had two new drugs approved for market launch in 2017. Sanofi’s DUPIXENT (dupilumab) and KEVZARA (sarilumab) are indicated for the treatment of severe eczema and rheumatoid arthritis, respectively. Rheumatoid arthritis is a chronic autoimmune disease in which the patient’s immune system attacks joint tissues, causing inflammation and pain, and ultimately leading to joint damage. GBI, a globally renowned research firm, predicts that the global market for rheumatoid arthritis treatments will reach $19.3 billion by 2023, indicating broad market prospects for KEVZARA in the future.

The market size of biological products is growing significantly faster than that of chemical drugs:From 2011 to 2017, the global biological products market grew at a significantly faster rate than the chemical drug market. In 2017, sales of biological products increased by 13.2%, reaching $227 billion. In contrast, the sales growth rate for chemical drugs was only 1.9%, representing a 17.3% decline. This trend was primarily driven by major pharmaceutical companies increasing their R&D investment in biological products, thereby boosting market supply, while healthcare institutions also increased their utilization of these products.

Biologics Sales Surpass Chemical Drugs:In 2017, among the top 20 global pharmaceutical products by sales, 11 were biologics, accounting for 62% of total sales. Humira (Adalimumab), ranked first, is a monoclonal antibody biologic with annual sales of $18.427 billion, representing 14.3% of the total sales of the top 20 drugs. Developed by AbbVie Inc. in the United States, this drug is a dimer composed of humanized monoclonal D2E7 heavy and light chains linked by disulfide bonds, and is primarily used to treat rheumatoid arthritis.

Humira was first approved by the FDA for market launch in December 2002, and subsequently received marketing authorization in Germany, the United Kingdom, and Ireland. In November 2011, the China Food and Drug Administration (CFDA) granted its initial approval for Humira for the treatment of two indications: rheumatoid arthritis and ankylosing spondylitis. By 2017, the market for rheumatoid arthritis treatments in China had reached RMB 18 billion, with a compound annual growth rate (CAGR) of 3.9% over the preceding five years.

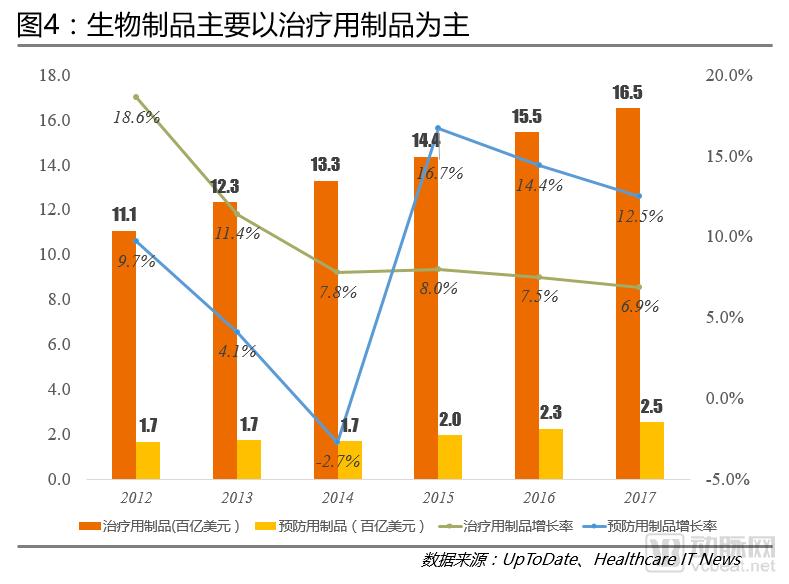

Therapeutic biologics dominate:In terms of sales within the biopharmaceutical subsectors, therapeutic biologics dominate, far surpassing preventive biologics. In 2017, sales of therapeutic biologics reached $165 billion, accounting for 72.7% of total biopharmaceutical sales.

Growth Rate of Prophylactic Biological Products Exceeds That of Therapeutic Biological Products:In terms of sales growth rate, the sales growth rate of preventive biological products exceeded that of therapeutic biological products in 2015, with the growth rate consistently remaining above 10%. This was mainly due to the emergence of many new types of diseases caused by environmental pollution, the increase of emerging pathogens, and the frequent occurrence of epidemics, which increased the demand for disease prevention and boosted the sales volume of preventive biological products.

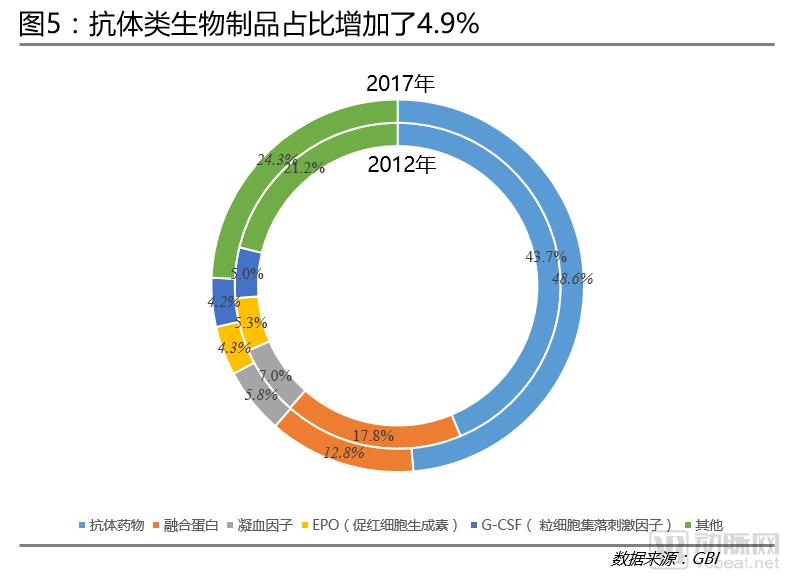

Antibody Drugs Stand Out:In terms of biological products, only antibody drugs registered growth, with a 4.9 percentage point increase, while all other categories experienced varying degrees of decline. This is primarily because oncology has become the main therapeutic area for antibody drugs. According to authoritative pharmaceutical industry reports released by EvaluatePharma and IQVIA (formerly IMS Health) in 2017, the global market size for anti-tumor drugs is projected to reach $192.2 billion in 2022, with a compound annual growth rate (CAGR) of 12.7%.

The growth rate of biological product registrations in China has surpassed that of chemical drugs, with anti-tumor biological products accounting for the largest number.

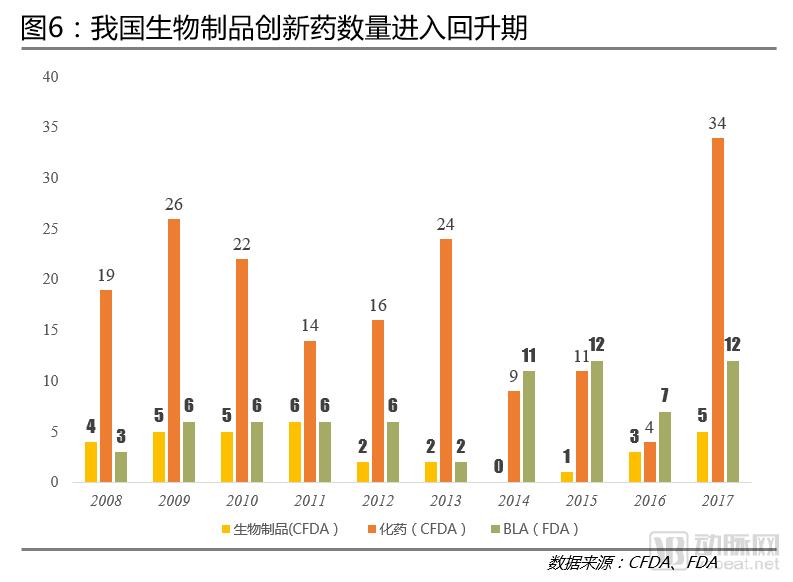

Number of New Biological Products Enters a Recovery Phase:An analysis of the CFDA’s new drug approvals over the years reveals that the number of approved innovative biological products (including imported original research drugs) in China has entered a period of recovery. In 2017, the number of approved biological products reached five, marking a six-year high. This indicates that while China is introducing foreign original research drugs, it is also strengthening its independent innovation capabilities and enhancing its R&D capacity for biological products.

The Growth Rate of Biologics Registrations Exceeds That of Chemical Drugs:According to the new drug registration data released by the Center for Drug Evaluation (CDE), the growth rate in the number of biological product registrations has surpassed that of chemical drugs. In 2017, the number of biological product registration applications in China reached 627, an increase of 272 compared with 2008, with a compound annual growth rate (CAGR) of 6.5% over the past decade. In contrast, the CAGR for chemical drugs during the same period was -3.2%. This further demonstrates that Chinese pharmaceutical companies have strengthened their research, development, and production of biological products.

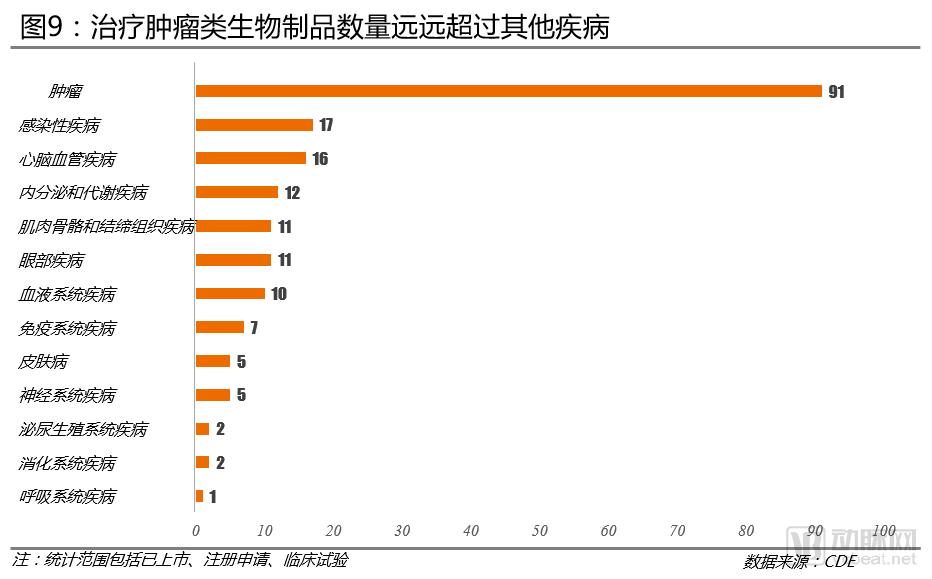

Oncology Therapeutic Biologics Are the Most Numerous:In terms of the distribution of indications for various biological products, there are as many as 91 oncology-focused biological products, far exceeding those for other diseases. This is primarily because cancer has become a major disease burden in China, with lung cancer and breast cancer being the most prevalent cancers among men and women, respectively. As a result, anti-tumor biological products have become the preferred choice in the oncology drug market.

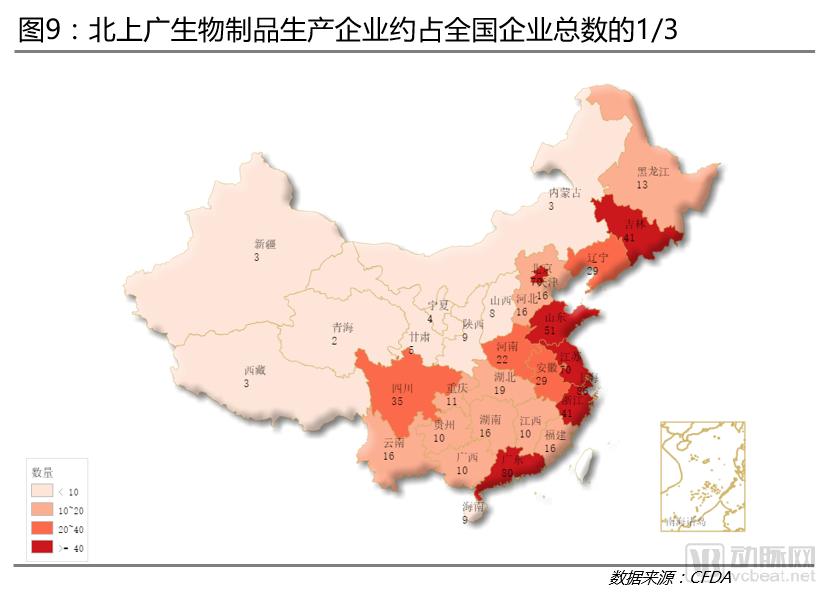

Imbalanced Distribution of Biologics Companies: Beijing, Shanghai, and Guangzhou Emerge as Primary Hubs

Imbalanced Distribution of Biologics Companies:China currently has a total of 752 biopharmaceutical companies. In terms of registration location, they are mainly concentrated in coastal areas, with fewer distributed in the northwest, which is closely related to China's economic level and population distribution. The number of biopharmaceutical companies in Beijing, Shanghai, and Guangzhou reaches as high as 236, accounting for about one-third of the total number of biopharmaceutical companies in China. From the perspective of the number of companies in individual provinces, Shanghai has the largest number, with 86 companies.

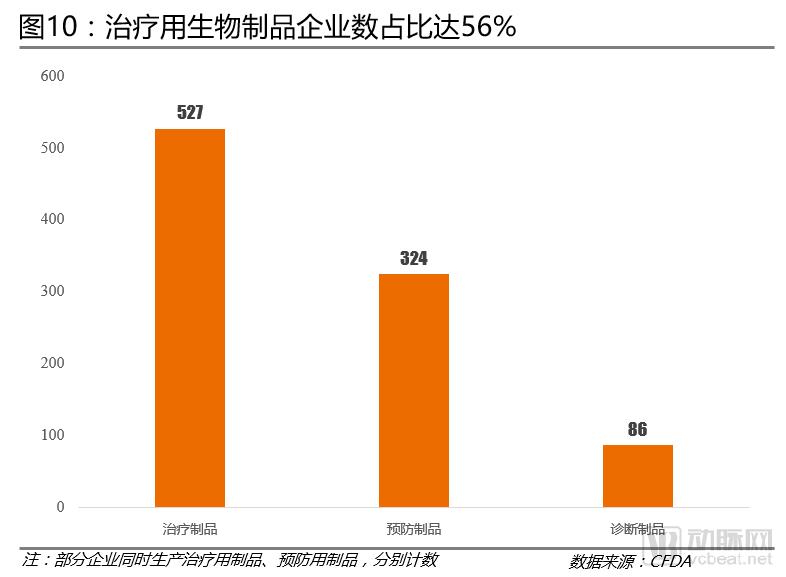

Therapeutic Biological Products: Highest Number of EnterprisesBased on the main products manufactured by major biopharmaceutical companies, there are 527 manufacturers of therapeutic biological products, accounting for 70% of the total number of enterprises. Monoclonal antibodies and blood-derived products have become the two major categories of therapeutic biological products.

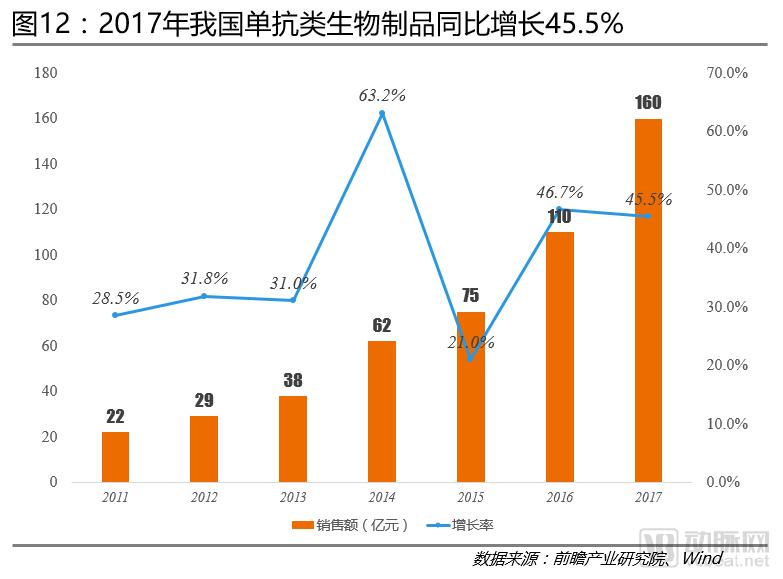

Monoclonal antibody-based biologics recorded a sales growth rate of 45.5%, while the number of vaccine types approved for lot release reached 56.

Monoclonal antibody biologics have achieved an average annual growth rate of 39.2%:From 2011 to 2017, the sales volume of blood products and monoclonal antibody biologics in China continued to expand, with compound annual growth rates (CAGR) of 15.0% and 39.2%, respectively. In terms of market size, blood products exceeded monoclonal antibody biologics; however, in terms of sales growth rate, monoclonal antibody biologics far outpaced blood products. This indicates that the market prospects for monoclonal antibody biologics are promising in the future.

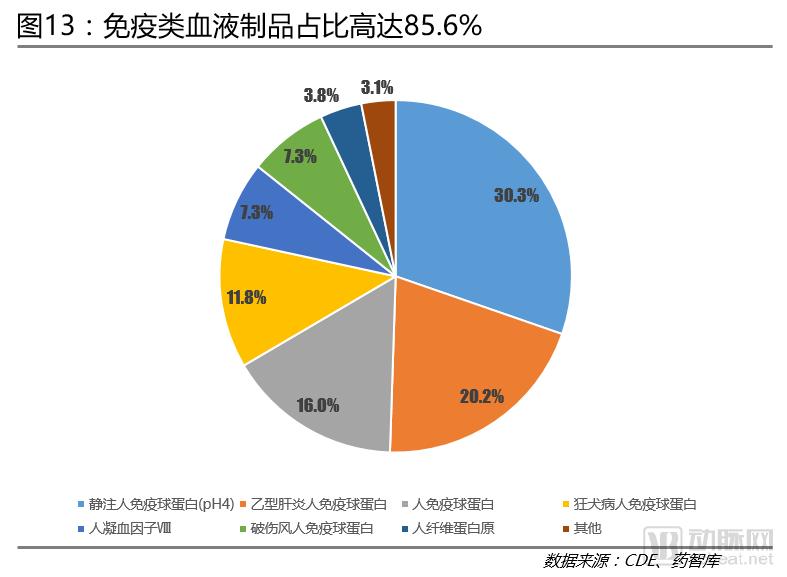

Immunological Blood Products Become Best-Selling Drugs:From the perspective of subcategories of blood products, immunological blood products account for as high as 85.6%. Among them, Intravenous Human Immunoglobulin (pH4) generates the highest sales revenue, reaching 30.3%. This product is primarily indicated for primary and secondary immunoglobulin deficiencies. Such deficiencies can lead to severe infections and neonatal sepsis, with children and the elderly constituting the main patient populations, thereby driving product sales.

Therapeutic biological products in China have demonstrated strong sales performance, with monoclonal antibody drugs experiencing the most rapid growth and achieving record-high sales revenue. During the same period, preventive biological products, primarily vaccines, have also undergone new changes.

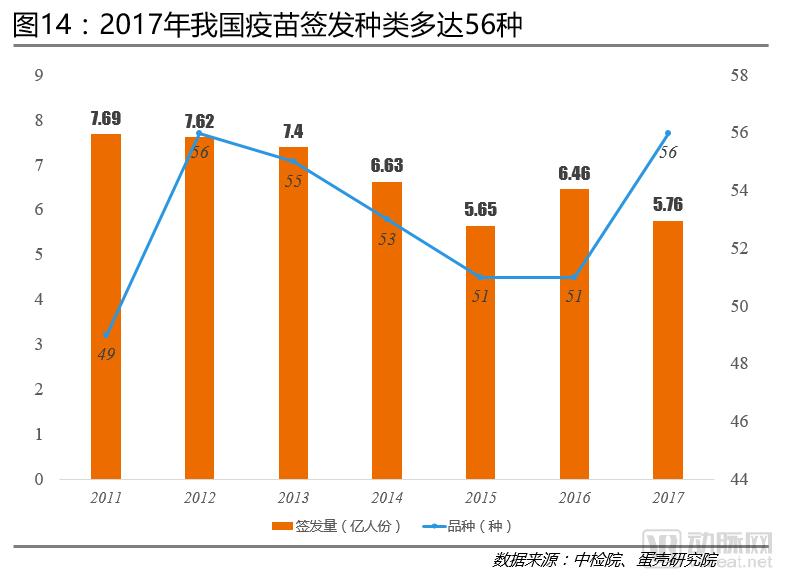

Vaccine Lot Release Volume Hits New Record High:In 2017, the number of vaccine types approved for release in China reached 56, marking the highest level since 2012. However, from 2011 to 2017, the overall volume of vaccines approved for release showed a gradual downward trend. This is primarily because China implements a lot-release system for vaccine approval, whereby each batch of vaccines must undergo review and release by the National Institutes for Food and Drug Control (NIFDC) and can only be marketed after passing quality testing. Stringent regulatory oversight has imposed high requirements on vaccine product innovation. The rebound in the number of vaccine types indicates that the R&D capabilities of Chinese vaccine manufacturers are strengthening.

Vaccine Sales Show a Moderate Increase:Over the past seven years, while the total sales volume of vaccines in China has declined, sales revenue has increased. This indicates that the improved quality and efficacy of Chinese vaccines have gained market recognition, leading to higher vaccine prices and an overall increase in sales revenue for vaccine manufacturers.

Rabies and meningitis vaccines dominate:In 2017, the best-selling vaccine in China was the freeze-dried human rabies vaccine (Vero cell vaccine), with sales reaching 6.55 million doses, accounting for 23.47% of total vaccine sales. Among the top 10 best-selling vaccines, rabies vaccines and meningitis vaccines each occupied three spots, indicating that rabies and meningitis were the primary diseases targeted for prevention in 2017.

Based on an analysis and comparison of data regarding the market launch status, sales volume, and composition structure of new biopharmaceutical products both domestically and internationally, the overall situation of the biopharmaceutical industry in 2017 is as follows:

(1) The number of new biological products launched globally has returned to a historical peak, with the growth rate of the biological products market significantly higher than that of chemical drugs.

(2) Monoclonal antibody-based biologics have become a global hotspot for new drug development, with top-tier market sales.

(3) Therapeutic biological products dominate market sales, while prophylactic biological products are experiencing rapid growth.

(4) The number of newly marketed biological products in China is gradually increasing, but it still lags far behind that of the United States.

(5) The distribution of biopharmaceutical companies in China is uneven, with Beijing, Shanghai, and Guangzhou emerging as the primary hubs.

(6) Antineoplastic biologics and immunological blood products have become best-selling drugs in China.

Given the development of the domestic and international biologics industry in 2017 and the government’s policy incentives favoring the import of anticancer drugs, the structure of the biologics sector will undergo further adjustment. Antineoplastic biologics will lead industry growth and become a key innovation driving improvements in cancer treatment. According to projections by the China Investment Advisory Industry Research Center, the market size for monoclonal antibodies in China is expected to reach RMB 28 billion by 2020, with a compound annual growth rate of 30%. Currently, monoclonal antibody-based biologics in China are predominantly imported. Companies should increase R&D investment in this area to boost the market share of domestically developed original drugs, with the aim of achieving import substitution.

Scan the QR code below now to becomeVCBeat Official Member, you will have unrestricted access to the complete content over the next yearIndustry Trend Report, timely grasp the latest globalInvestment and Financing Information, boasting a comprehensive range ofMedical Enterprise Database, andMassive Resource Integration。