WuXi AppTec Completes 'One-to-Three' Spin-off Strategy with Combined Market Cap Exceeding RMB 150 Billion

Following Foxconn’s record of securing regulatory approval in just 36 days, another noteworthy medical “unicorn” is poised for a rapid IPO.

According to insiders, at the 51st working meeting of the Issuance Review Committee of the China Securities Regulatory Commission (CSRC) in 2018 held on March 27, WuXi AppTec successfully passed the review.

WuXi AppTec is hailed as the “Huawei” and “Foxconn” of the pharmaceutical industry, ranking 11th globally among pharmaceutical R&D outsourcing service providers. Its successful regulatory approval also marks the smooth completion of its “one-into-three” listing on the capital markets following its delisting from U.S. stocks. The combined market capitalization of the three companies in the WuXi AppTec group may exceed RMB 150 billion.

Niche Markets Breed “Unicorns”

WuXi AppTec operates in the CRO and CMO/CDMO sectors—contract research, contract manufacturing, and contract development and manufacturing services—which constitute a relatively niche and specialized market within the pharmaceutical industry.

CRO services encompass preclinical research, clinical trials, technology transfer, and consulting, covering the entire process from new drug discovery and clinical development to regulatory registration. As the CRO market matures, it has given rise to diverse business models such as contract manufacturing and industry-academia collaborations, making CROs an increasingly vital segment of the pharmaceutical and biotechnology industry.

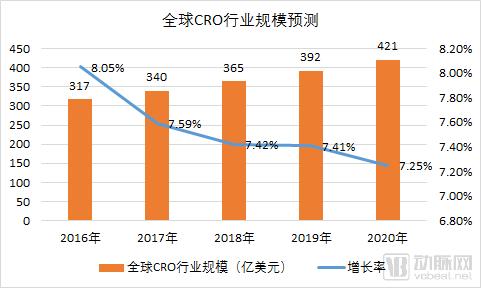

CRO Business Scope

According to data from the Southern Institute, the global CRO market is only around $30 billion.

Data Source: Southern Institute of Pharmaceutical Economics

From the perspective of competitive landscape, the global leaders are primarily U.S.-based companies. From the mid-1980s to the 1990s, companies such as Parexel, PPD, ICON, and Covance were successively established and went public, marking a period of rapid growth for the U.S. CRO market. After 2000, these leading U.S. CRO firms began expanding globally and pursuing mergers and acquisitions within the industry, gradually diversifying their service offerings to cover the entire continuum from new drug discovery to post-marketing consulting.

China’s CRO industry developed relatively late and was similarly introduced by foreign enterprises. In 1996, MDS Pharma Services invested in establishing the first true CRO company in China, primarily engaged in clinical research services, marking the nascent stage of China’s CRO industry. In 2000, WuXi AppTec was founded, followed by the establishment of companies such as Shanghua Pharmaceutical, BJC Pharma, and Tigermed, ushering China’s domestic CRO industry into a period of growth.

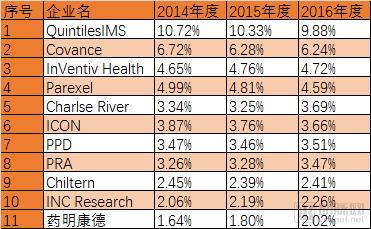

The global CRO market is highly concentrated, with the top ten service providers accounting for approximately 50% of the market share. WuXi AppTec ranks as the 11th largest CRO provider globally, with a market share of around 2%.

Leading Global CRO Companies and Their Market Share

Data Source: Southern Medical Economic Research Institute

As the only Chinese company ranked among the top, WuXi AppTec truly deserves the acclaim. Pharmaceutical giants such as Pfizer, Johnson & Johnson, Roche, Eli Lilly, and Merck are all its key clients. After significantly expanding its market share, WuXi AppTec went public on the New York Stock Exchange on August 9, 2007.

“Split into Three” Successfully Completed

After many years in the United States, WuXi AppTec has come to feel that “Wall Street’s excessive focus on short-term performance makes large-scale strategic investments increasingly difficult.” Consequently, the company began planning its return to China.

In April 2015, WuXi AppTec’s contract manufacturing and research organization, STA Pharmaceuticals, was listed on the National Equities Exchange and Quotations (NEEQ), marking the first step in WuXi AppTec’s return to China.

In December 2015, WuXi AppTec announced the completion of its privatization, a transaction involving $3.3 billion. On March 23, 2017, WuXi AppTec posted an announcement on its official website regarding listing tutoring; in June 2017, WuXi Biologics listed in Hong Kong, successfully completing the second step of its spin-off and return.

In July 2017, WuXi AppTec filed its IPO prospectus, officially kicking off the third act of its “one-into-three” split. On February 6 this year, WuXi AppTec released its pre-disclosure information for listing on the Shanghai Stock Exchange. The application was approved by March 27, taking only 50 days in total—another record for IPO queue processing time, following Foxconn’s 36-day “lightning” approval.

As of now, the total market capitalization of WuXi STA is RMB 20.274 billion, while that of WuXi Biologics is HKD 93.984 billion—approximately equivalent to RMB 75.2 billion (market capitalization calculated based on the closing price as of March 27).

According to WuXi AppTec’s prospectus, the company plans to issue 104 million shares, accounting for no less than 10% of its total share capital, and raise RMB 5.741 billion. Based on this estimate, the company’s market capitalization at the time of its listing would be approximately RMB 57 billion.

202.74 + 752 + 570 = 1,524.74. This means that if WuXi AppTec successfully completes its IPO fundraising, the combined market capitalization of the three companies resulting from the “one-into-three” split will exceed RMB 150 billion. Compared to the USD 3.3 billion valuation at the time of its return, this represents a more than sixfold increase in market capitalization over three years.

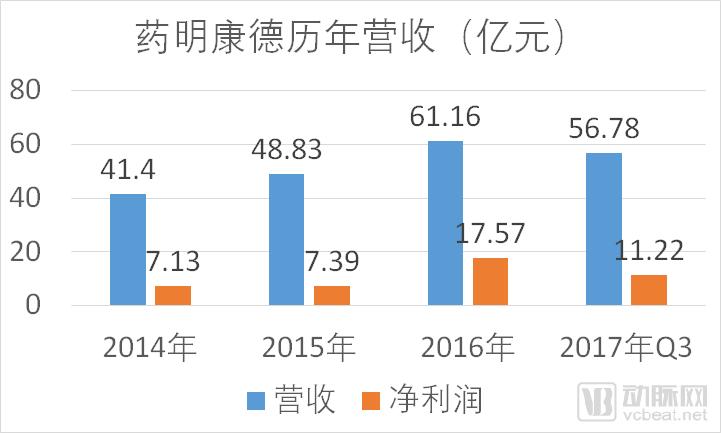

Additionally, WuXi AppTec’s post-IPO growth potential can be assessed based on its revenue data. According to the prospectus, from 2014 to September 30, 2017, WuXi AppTec reported operating revenues of RMB 4.14 billion, RMB 4.883 billion, RMB 6.116 billion, and RMB 5.678 billion, respectively; net profit attributable to shareholders after deducting non-recurring gains and losses amounted to RMB 213 million, RMB 180 million, RMB 878 million, and RMB 859 million, respectively; net cash flows from operating activities were RMB 713 million, RMB 739 million, RMB 1.757 billion, and RMB 1.122 billion, respectively; and gross profit margins stood at 36.78%, 34.55%, 40.76%, and 42.76%, respectively.

Based on its 2016 net profit, WuXi AppTec’s issuance price-to-earnings (P/E) ratio was approximately 32x. In contrast, the average P/E ratio for the A-share pharmaceutical sector stood at around 80x, while that of its peer Joinn Laboratories exceeded 78x on a trailing basis. This suggests that WuXi AppTec had significant room for market capitalization growth following its listing.

However, WuXi AppTec’s planned fundraising amount is the highest among this year’s IPOs. The next two largest are Huaxi Securities (RMB 5 billion) and Jiangsu Financial Leasing (RMB 4 billion). The substantial fundraising target also poses certain challenges to WuXi AppTec’s smooth listing.

WuXi AppTec’s IPO benefited from favorable timing, as A-share markets embraced “unicorns”; geographic advantage, with access to capital markets on its doorstep; and human resources, leveraging a professional team with pharmaceutical expertise and capital operation capabilities. Following its listing, WuXi AppTec may leverage the resource agglomeration effects of being a public company to enhance its competitiveness in the global market and drive domestic pharmaceutical innovation.