How Can Chain Rehabilitation Clinics Expand Rapidly Despite High Single-Store Costs Exceeding RMB 1 Million? Marketing, Talent, and Standardization Remain Key Challenges

*Header image provided by Jingyiwei

Compared to sports rehabilitation, which is still in the market education phase, rehabilitation institutions focusing on neck, waist, shoulder, and spinal pain appear to be faring much better. The increasingly younger demographic has injected vitality into this market, which was traditionally associated with age-related conditions.

The sports injury market is skewed toward the high-end segment, and public awareness of rehabilitation remains limited. Even Hongdao Sports Medicine Clinic, a top-tier player in the market, stated in an interview with a reporter from VCBeat (WeChat ID: vcbeat) that it took four years to reach break-even.

In contrast, treatment and rehabilitation institutions specializing in spinal and musculoskeletal pain cater to a larger customer base, with consumer spending power above the market median.

Recently, VCBeat interviewed several companies in the niche market of pain management to explore their perspectives on how to build small yet exquisite rehabilitation chains and examine the distinct development paths they are pursuing.

From the perspectives of the existing stock market and the incremental market, the current rehabilitation market comprises three categories of existing populations:

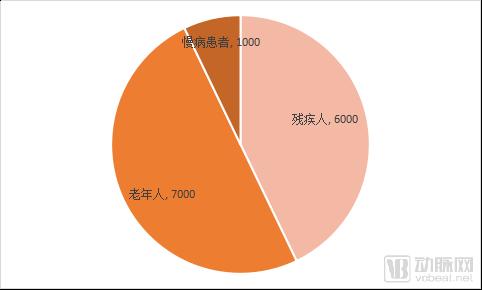

Target Population and Size for Rehabilitation Needs (Unit: 10,000 people)

1. Population with disabilities: over 59.5 million;

2. Elderly population: over 70 million;

3. Population of patients with chronic diseases: over 10 million.

According to a PwC survey, the primary rehabilitation needs in China currently stem from postoperative rehabilitation for conditions treated in neurology and neurosurgery, orthopedics, cardiology and pulmonology, pediatrics, and obstetrics and gynecology. This represents the existing market within the rehabilitation industry, served by 3,800 rehabilitation departments in general hospitals and specialized rehabilitation institutions, as well as approximately 4,500 tier-II-and-above hospitals that have established rehabilitation departments.

Relatively speaking, hospitals provide generalized services and exist as public infrastructure. Within hospitals, however, the development of rehabilitation departments faces significant challenges due to constraints imposed by the existing system, resulting in their marginalization. Consequently, patients often receive suboptimal treatment and have a poor care experience.

In sectors open to private capital, beyond specialized hospitals that must secure a Medical Institution Practice License by meeting a series of environmental impact assessment requirements and staffing configurations, there is also a cohort of small yet refined specialized rehabilitation institutions actively operating at the intersection of capital and services, seeking opportunities in niche market segments.

Beyond the existing market, the incremental market encompasses niche segments such as pediatric rehabilitation, geriatric rehabilitation, psychiatric rehabilitation, cardiac rehabilitation, and sports rehabilitation. With societal development and an accelerating pace of life, coupled with the widespread adoption and increased frequency of use of smart devices, a specific demographic has emerged at the intersection of sports rehabilitation, pain management, and orthopedics. Their health concerns are primarily focused on cervical spine, lumbar spine, spinal column, and musculoskeletal pain. The vast majority of this group shares a common identity: office workers.

According to observations and research analysis by Ning You, founder and CEO of Jing Yi Wei, there are as many as 200 million patients with cervical and lumbar spine disorders in China, with the peak onset age dropping from 55 to 38 years—a trend closely linked to the rising incidence among office workers. Jing Yi Wei’s core customer base is positioned between the ages of 30 and 50, and in 2017, it provided cervical and lumbar spine care services to a total of 25,000 patient visits.

Ji Jin Wan Mei stores primarily offer four core services: spinal pain management, sports injury rehabilitation, postpartum pelvic floor recovery, and posture correction. Among these, patients with spinal pain account for 50%, while those with sports injuries make up 25%. Zhu Guomiao, the founder, describes the target customer profile as individuals aged 25–55 who engage in long-term sedentary work.

Xie Chunqing, CEO of Beijing Kangfu Zhijia Hospital Management Co., Ltd., stated that elderly customers actually constitute a smaller demographic at Kangfu Zhijia stores, with the majority of rehabilitation service recipients being younger individuals. This trend is closely linked to the growing public emphasis on addressing and improving suboptimal health conditions.

This demographic is characterized by advanced consumption concepts, a strong emphasis on health, and a willingness to pay for health-related services. At its core, this group rejects the inefficient and time-consuming services offered by public hospitals.

In China’s rehabilitation market, specialized branches are becoming increasingly refined. Institutions focused on cervical and lumbar spine and spinal rehabilitation range from large chain rehabilitation centers to small-scale blind massage parlors, resulting in a highly heterogeneous market. However, regarding the prospects of specialized rehabilitation institutions, as the target population expands and the market becomes more regulated, a blue ocean awaits exploitation by incoming players. These players share a common characteristic: close integration with rehabilitation medicine.

In the pain management market, chain institutions can be divided into two categories: one is pain specialty clinics holding a medical practice license, and the other is rehabilitation institutions with professional rehabilitation physicians on staff.

Pain specialty outpatient clinics have evolved from hospital-based pain departments. There has been limited entry of private capital into this sector; to date, VCBeat is aware of only one player, Hepu Medical, whose first pain specialty clinic in China officially opened in January 2018. In addition to providing rehabilitation services, it offers minimally invasive surgical procedures for pain management. Consequently, beyond specialized hospitals and clinics, the market is predominantly populated by chain institutions focused on rehabilitation.

In an interview with VCBeat, Feng Feng, co-founder of Jijin Wanmei, stated that the greatest advantage of establishing Jijin Wanmei and specializing in in-depth spinal rehabilitation lies in mastering “core technologies.”

So, what exactly is the “core technology” they refer to? To answer this, we must start with the pain points in the market.

When most people experience discomfort in their cervical spine or muscles, they do not immediately seek evaluation at a medical institution. Instead, their first stop is typically a massage parlor. What exactly is a massage parlor? Accurately speaking, it is an establishment where services are provided by technicians, and its scientific basis and professionalism are often not guaranteed.

In an interview with VCBeat, Ning You stated that individuals seeking massage therapy for muscle or spinal issues often encounter one of two outcomes: either the treatment is ineffective, or it causes further harm. The varying quality of wellness establishments in the market poses challenges to standardizing pain management practices. However, the prevalence of such businesses, large and small, on city streets underscores the existing market size and demand for pain-relief services.

As rehabilitation medicine gains momentum, specialized institutions are seizing market opportunities, with professional diagnostic and therapeutic methods backed by medical expertise becoming the “core technology” for rehabilitation centers targeting pain management.

Based on observations of the cervical and lumbar spine rehabilitation and pain management markets, most rehabilitation institutions currently adopt physical therapy as their primary treatment modality. This approach also serves as the core method in sports rehabilitation, combining exercise training with manual therapy corrections, or utilizing rehabilitation equipment for assessments and therapeutic exercises.

Such institutions typically earn a reputation among patients through their professionalism. The individual professionalism of the physicians and the standardization of their clinics constitute the primary distinctions from the myriad of “hourly tui na,” “blind massage,” and “wellness centers” prevalent in the market.

Ning You is a postdoctoral fellow at Huashan Hospital, Fudan University, specializing in acupuncture and tuina (Chinese therapeutic massage) and spinal aging. He previously established a specialized outpatient clinic for acupuncture and tuina at Huashan Hospital. On Dianping, one of the promotional platforms for Jing Yi Wei, the most frequent comment about Jing Yi Wei is “professional.” His team includes PhDs and master’s degree holders in rehabilitation medicine, as well as professionals specializing in physical therapy.

Coincidentally, Zhu Guomiao, Master’s and Doctoral degree holder and founder of Jijin Perfect, studied successively under Professor Fang Min, Chief Scientist of China’s 973 Program, and Professor Yan Juntao, the country’s first doctoral supervisor in Tuina (Chinese therapeutic massage). As the sixth-generation inheritor of Ding’s Tuina, he possesses a rigorous and solid theoretical foundation and has authored more than 500 professional articles.

He/She has worked for nearly 20 years at top-tier (Grade A Tertiary) traditional Chinese medicine hospitals, including Anhui Provincial Hospital of Traditional Chinese Medicine, Shanghai Shuguang Hospital, and Shanghai Seventh People’s Hospital, accumulating extensive clinical experience.

Even the rehabilitation centers under Family of Health, which were just launched in January 2018, are equipped with a professional team of physicians. This team features multidisciplinary collaboration among specialists in sports medicine, rehabilitative medicine, pain management, and physical therapists.

From offering a single product to providing disease-specific solutions for conditions such as respiratory disorders, hypertension, stroke, and pain, the transformation and practices of Family of Health have delivered strong operational results for its stores, with the average transaction value increasing by 20%.

Generally, in the outlets of such rehabilitation chains, the equipment used for rehabilitation services mainly includes therapeutic devices, assessment devices, and others, with functions primarily focused on physical therapy. Due to differing positioning among various providers, there is a distinct emphasis on the types of equipment employed. Based on extensive interviews and research conducted by VCBeat, the following devices are most commonly found in rehabilitation chain institutions:

In each category of stores, different assessment instruments are available for different symptoms. For instance, Jing Yi Wei, which focuses on cervical spine care, is equipped with a specialized cervical spine tester to evaluate and assess functional issues of the cervical spine (such as those involving muscles, tendons, and ligaments).

The Neck, Shoulder, Waist, and Back Conditioning Center of Family of Health has introduced an infrared thermal imaging somatosensory assessment system, which scans and images the whole body and local areas to visually present muscle strain points from the images.

Similarly, Ji Jin Wan Mei’s stores are also equipped with infrared thermal imaging body assessment devices for posture evaluation. In addition, the stores feature the “Posture-Screen” body measurement system, which employs precise imaging and data analysis to quantitatively assess abnormal postures such as shoulder tilt, spinal curvature, pelvic tilt, leg alignment abnormalities, foot and ankle anomalies, rounded shoulders, kyphosis, and forward head posture. This system serves as an effective complement to conventional orthopedic examinations such as X-rays and CT scans.

Shockwave therapy devices are physical therapy equipment capable of generating precise shockwaves and transmitting them into the patient’s body through a coupling medium. The clinical application of this technology has ushered in the “era of non-invasive treatment” in the history of rehabilitation and physiotherapy. Compared with traditional invasive treatments such as acupuncture, acupotomy, and minimally invasive procedures, shockwave pain therapy is not only non-invasive but also stands out as the most rapid, safe, and effective pain management technique in physical rehabilitation, owing to its finely adjustable dosage range, diverse treatment modalities, and unrestricted treatment locations.

The underlying principle involves utilizing shockwaves generated by the device, which are coupled into the human body through a water balloon or other methods, and focused on the lesion to achieve therapeutic effects. Market prices vary significantly, with shockwave therapy devices of different models and functions ranging from several thousand to tens of thousands of yuan.

S-E-T is the English abbreviation for Sling Exercise Therapy. The so-called SET suspension training system involves suspending part of the patient's body from fixed ropes. Through active intervention techniques, it aims to early stimulate neural networks to establish correct functional control areas, restore balance function, coordination ability, control ability, and dominance ability, thereby progressively addressing abnormal force application and abnormal postures resulting from impaired brain control.

The SET Sling Exercise System is a comprehensive conceptual framework aimed at achieving long-term improvement in musculoskeletal disorders through the application of active therapy and training. With active exercise and rehabilitative treatment as its core components, this approach encompasses diagnosis, therapeutic intervention, and standardized, prescription-guided exercise programs for pediatric patients. It emphasizes the activation and mobilization of the body’s latent functional capacities under unstable conditions to achieve therapeutic outcomes. The system is widely utilized by institutions specializing in motor rehabilitation and providing solutions for muscle pain.

According to Ning You, the instruments used by Jing Yi Wei are common “acoustic, optical, and electrical” physical therapy devices in rehabilitation equipment. Such devices mainly include medium- and low-frequency therapeutic apparatuses, DMS deep muscle stimulators, ultrasonic therapy devices, electromagnetic wave therapy devices, interferential current pain therapy devices, and polarized light pain therapy devices.

For specialized chain service providers, the key lies in a business model that can be rapidly scaled. The chain model for pain management institutions has not yet taken shape in the market. Even well-regarded players in this niche, such as Jijin Wanmei and Jingyiwei, have not expanded on a large scale; they remain in the startup phase, exploring mature business models.

The spine, cervical vertebrae, and other such structures are akin to “consumable” assets; treatment primarily focuses on rehabilitation and conditioning, meaning that a single session is often insufficient to alleviate chronic pain. Consequently, compared with the diagnosis and treatment of common ailments like colds and fevers, pain management services are characterized by longer treatment cycles and higher repurchase rates. In terms of consumption models, they are typically divided into course-based billing and single-session payment.

Ji Jin Wan Mei currently operates three clinics in Shanghai, each ranging from 200 to 400 square meters. The average daily patient volume is approximately 30. Its fee structure comprises two categories: single-session visits and comprehensive treatment packages. The consultation fee for a one-hour single session ranges from RMB 600 to RMB 1,000.

Jing Yi Wei, also based in Shanghai, has established three offline stores, each with an area of approximately 200 square meters. In terms of its business model, Jing Yi Wei adopts a “front-store, back-clinic” approach. In addition to receiving therapeutic and maintenance services on-site, customers can also purchase rehabilitation-related products available in the store.

Rehabilitation Home’s Neck, Shoulder, Waist, and Back Conditioning Center is located in Wuxi and opened in January 2018. It was incubated from rehabilitation experience services offered within medical device retail stores. The store covers an area of approximately 150 square meters. Thanks to years of deep engagement in the medical device sector, nearly all equipment procured for the store is acquired at the lowest possible prices. Additionally, by avoiding establishment in first-tier cities, the initial investment per store is kept around RMB 800,000. With an average transaction value of approximately RMB 200, the center primarily serves residents in nearby communities and areas surrounding hospitals.

According to Xie Chunqing, the Rehabilitation Home Neck, Shoulder, Waist and Back Conditioning Center was not in a hurry to expand in 2018, and currently has chosen to set up locations in three cities: Beijing, Shanghai, and Wuxi.

Characterized by low costs, high repurchase rates, and substantial demand, such chain institutions often achieve break-even within six months to a year. Those capable of rapid expansion and possessing mature business models are also more likely to attract capital investment.

Compared with sports rehabilitation, which targets a narrower demographic and occupies a higher-end market position, mass-market content and products typically incur lower market education costs. Meanwhile, as public health awareness continues to rise, they also boast a larger potential audience.

In terms of marketing, each company has its own strategies.

Conventional online marketing includes setting up traffic diversion entry points on O2O platforms such as Dianping and Meituan. Beyond that, it hinges on leveraging brand equity.

In the field of pain management, brand building and word-of-mouth dissemination are crucial; “treating one patient often brings in a whole group of others.”

In addition to online methods, offline science popularization and market education activities are indispensable. Such broad-reach initiatives typically serve as a means to reduce customer acquisition costs.

In this regard, Ningyou has targeted corporate clients, promoting its brand through a series of experiential lectures. Backed by the expertise of its postdoctoral team, the company’s public welfare health lectures and on-site free clinics have proven effective in attracting clients, educating the market, and achieving high conversion rates.

For specialized rehabilitation, the challenge has always been that “even fine wine fears a deep alley.” Acquiring end-users (C-side) involves significant market education hurdles, whereas shifting this model to the business side (B-side) may offer a cost-saving approach and serve as one pathway toward diversifying business models.

Given that the core target audience is positioned as office workers, enterprises are inevitably the key “point” that Jing Yi Wei must penetrate. According to Ning You, since the second half of 2017, Jing Yi Wei’s B-end clients have gradually increased. The company has currently established partnerships with enterprises such as the Shanghai headquarters of Siemens, Nike, and Lenovo, with revenue from B-end services accounting for 10% of its total.

Regarding marketing and customer acquisition, Zhu Guomiao humbly admitted that his efforts were “not very effective,” with a low conversion rate from lectures to new clients. “We lack mature marketing and sales strategies; Ji Jin Wan Mei still relies primarily on its brand equity and word-of-mouth reputation.”

In his early career, Zhu Guomiao amassed a large patient following on the “Haodafu” platform by writing popular science articles. He was also among the first physicians to actively use Sina Weibo and WeChat Official Accounts. Currently, the “Ji Jin Wan Mei” WeChat Official Account has been in operation for four years, with over 60,000 followers.

On Zhihu, Zhu Guomiao has answered 180 questions, amassed 1,900 followers, and received nearly 5,000 upvotes. He has also published 152 popular science articles on the Haodf platform. Followers from these channels, along with some of his former hospital patients, became the early clients of Jijin Wanmei.

For Rehabilitation Home, which has just entered the cervical, lumbar, and shoulder rehabilitation service sector, there are three channels for patient acquisition:

First, walk-in customers from the vicinity of Family of Health stores, covering the target population in surrounding communities; second, patient referrals from hospital pain management or rehabilitation departments, directing non-surgical patients to the stores; and third, educational presentations for schools and other enterprises and institutions. Xie Chunqing stated, “The primary purpose of these presentations is to popularize Family of Health’s relatively new technologies and treatment modalities within these organizations, with a greater focus on facilitating corporate employee health management services, as well as collaborating with primary and secondary schools to conduct postural assessments and corrections for students.”

In the healthcare services industry, talent has long been a perennial topic. Within the rehabilitation sector, nearly all entrepreneurs unanimously cite a shortage of skilled professionals. Given that each rehabilitation facility typically staffs 10–12 employees per location, labor costs often account for 50%–60% of total operating expenses.

Why Spinal Pain Rehabilitation Centers Are “Small but Beautiful”: First, the nature of high-frequency, long-cycle rehabilitation services ensures stable market demand; second, to address the pain point of a shortage of rehabilitation professionals, many companies have chosen to build their own training systems.

Zhu Guomiao believes that one of the advantages of Ji Jin Wan Mei is its relatively comprehensive training business system.

According to previous reports by Lanxiong Sports, Jijin Wanmei’s revenue in 2017 reached the tens of millions of yuan, with 40% derived from its training business. If the company can maintain its 2017 levels of 25–30 participants per course and an average transaction value of RMB 4,000–5,000, supplemented by income from online courses, its training segment alone is projected to reach tens of millions of yuan in 2018.

Starting from borrowing venues for training, Spine Near Perfect has now established a comprehensive online and offline training curriculum. In addition to courses taught by internal instructors, it also features lectures from domestic experts and international instructors.

Jijin Perfect’s technical training programs have earned a strong reputation in the industry, thanks to their high quality. Feng Feng once stated, “Jijin Perfect invites only the best instructors.” As a result, its training services have attracted doctors and rehabilitation therapists from hospitals across China to pay for enrollment, with further expansion driven by word-of-mouth referrals from participants.

Ning You believes that the advantage of Jing Yi Wei lies not in isolated “points of strength,” but in the self-constructed “advantage chain.” This advantage chain refers to the competitive barriers Jing Yi Wei has established in the market, ranging from a team with strong medical expertise and extensive operational experience to a comprehensive talent training system, as well as its libraries of manual therapy techniques and treatment protocols based on user therapeutic data.

In the process of rapid expansion, Ning You believes there are two key factors:

First, the establishment of a training system; second, the improvement of corporate culture and management systems, including compensation and performance mechanisms.

He also stated, “Jing Yi Wei’s core business model is ‘front-store, back-clinic.’ While the model is relatively straightforward, executing simple tasks is not necessarily easy. As healthcare services are, to some extent, non-standardized, flexible standardization is required.”

Xie Chunqing believes that if the rehabilitation centers under Family of Health wish to establish a chain operation, they need to address two issues. The first is the talent training system, which many entrepreneurs agree is essential, such as their own “Rehabilitation Academy.” “This is the core system that enables the introduction of more rehabilitation professionals to ensure technological R&D and the training of rehabilitation therapists.”

The second aspect is the establishment of standardization, including the construction of a rehabilitation archive database. The focus shifts from relying on star therapists to build reputation toward leveraging a robust treatment system. “The performance of a clinic should not depend on any single rehabilitation therapist. We aim to ensure that patients receive consistent treatment outcomes and experiences regardless of which therapist they see at any of our locations.”

For the general public, apart from professional physicians, medical qualifications serve as another key criterion for assessing legitimacy. The market advantage of specialized rehabilitation institutions lies in their lower entry barriers; relevant authorities have not explicitly prohibited non-medical entities from providing rehabilitation services, but rather have streamlined the approval process for such institutions to obtain medical institution status.

On August 10, 2017, Jiao Yahui, Deputy Director of the Bureau of Medical Administration and Hospital Management under the National Health and Family Planning Commission (now the “National Health Commission”), announced at a regular press conference that five additional types of independently established institutions would be added: rehabilitation medical centers, nursing centers, sterile supply centers, small and medium-sized ophthalmic hospitals, and health examination centers.

On November 8, 2017, the National Health and Family Planning Commission (now the “National Health Commission”) officially issued the “Notice on Printing and Distributing the Basic Standards and Management Specifications for Rehabilitation Medical Centers and Nursing Centers (Trial),” which stipulated the basic standards and management specifications for rehabilitation medical centers. Compared with the previous requirement that only clinics could apply for a medical practice license, the conditions have been significantly relaxed.

Under the provision that “institutions not providing inpatient rehabilitation medical services are not required to establish inpatient rehabilitation beds, but must set up no fewer than 10 day-care rehabilitation beds,” small specialized chain institutions find it easier to meet regulatory requirements compared with the previous rule, which stipulated that “medical institutions with no beds or fewer than 100 beds must apply to the local county-level health administrative department.” At the very least, the requirements for floor space are not excessively stringent.

Furthermore, in November 2017, the National Health and Family Planning Commission issued Order No. 14, promulgating the Interim Measures for the Record-filing Administration of Traditional Chinese Medicine (TCM) Clinics (hereinafter referred to as the “Measures”). The Measures explicitly shifted the regulatory framework for TCM clinics from a licensing system to a record-filing system. Entities establishing TCM clinics may commence practice activities upon filing with the county-level administrative department of traditional Chinese medicine in the locality where the clinic is to be established. The Measures came into effect on December 1, 2017.

Based on current policies, there are two pathways to address the medical qualification issues for specialized rehabilitation institutions: one is to apply for qualification as a Rehabilitation Medical Center, and the other is to apply for a Medical Practice License for a Traditional Chinese Medicine (TCM) Clinic.

Having just completed a tens-of-millions RMB Series A financing round in March, Ji Jin Wan Mei plans to open two additional outpatient clinics and three to four community rehabilitation centers in 2018, followed by three new outpatient clinics and five to six community rehabilitation centers in 2019.

Beijing Family of Health Medical Treatment Devices Chain Business Co., Ltd. is also planning its layout and in-depth development in Beijing, Shanghai, and Wuxi.

Meanwhile, Jingyiwei is engaged in brand building and product R&D, including planning activities such as data collection.

Xie Chunqing believes that the service pain points of large hospitals mean that a portion of patients seeking care in rehabilitation or pain management departments will inevitably turn to the broader market for high-quality rehabilitation services that can effectively address their needs. “Judging by today’s market, small yet specialized and high-quality rehabilitation institutions are poised for significant growth over the next five years.”

In 2014, when emerging sports rehabilitation institutions were still burdened with the significant task of educating the market and popularizing awareness and consumption habits, many small yet specialized rehabilitation clinics adopted a chain model. By focusing on more practical areas such as occupational diseases among office workers, postural correction, postpartum recovery for women, and weight loss, and by delivering “professional and effective” results unmatched by traditional massage parlors, these clinics were able to achieve healthy revenue streams and rapid expansion in their early stages.

According to VCBeat’s observations, institutions that offer concentrated and more precisely targeted services for four specific demographics—spinal rehabilitation and neck, waist, and shoulder care for younger populations; prenatal and postpartum rehabilitation for women; pediatric posture correction for school-age children; and exercise-based rehabilitation for functional recovery in the elderly—are likely to expand rapidly in the market through a community-store model. However, whether these institutions can achieve rapid growth will depend on their ability to deliver differentiated experiences and establish competitive barriers in the market.