Third-Party Medical Imaging in China: Market Overview, Challenges, Core Competencies, and Future Outlook

In August 2016, the National Health and Family Planning Commission (NHFPC) issued the *Basic Standards for Medical Imaging Diagnostic Centers (Trial)*, giving a green light to third-party medical imaging centers from the perspective of national policy. Encouraged by this policy, various capital players rushed into this market, hoping to carve out their territories and seize market share. However, this field has high barriers to entry; without strong operational capabilities, heavy asset investments may lead to significant difficulties.

If you want to enter the third-party medical imaging sector, there are five important questions to clarify from the outset:

I. How Large Is China’s Medical Imaging Market?

Market size estimates vary, but accurate data is lacking. By analyzing data from the China Health Statistics Yearbook and the National Bureau of Statistics, it can be estimated that the total annual revenue from hospital examination fees (primarily comprising imaging and laboratory tests) in 2017 was approximately RMB 300 billion. Based on general industry experience where imaging and laboratory tests each account for half of these fees, hospital imaging examination fees amounted to roughly RMB 150 billion. Including the market share of primary healthcare institutions, the overall medical imaging market should be around RMB 200 billion. It is projected to grow to approximately RMB 250 billion by 2020.

The growth of the medical imaging market is often attributed to hospitals’ practices of prescribing excessive medications and ordering unnecessary diagnostic tests. However, this characterization is inaccurate:

(1)"Before the advent of MRI and CT, doctors still diagnosed and treated patients.". Conditions that were previously diagnosed using X-rays are now assessed with CT scans—is this over-testing? The answer is not clear-cut. With advancements in medical equipment, declining examination costs, and the increasingly widespread use of large-scale medical devices, clinical guidelines need to keep pace with the times. Therefore, demand in the imaging market is driven not only by patient diagnostic needs as outlined in clinical guidelines but also by patients’ income levels and the cost of examinations.

(2)With the advancement of medical technology, it is an inevitable trend for doctors to increasingly rely on modern diagnostic equipment.. It is no longer realistic to expect modern physicians to rely solely on inspection, palpation, percussion, and auscultation, or on the traditional Chinese medical diagnostic methods of observation, listening and smelling, inquiry, and pulse-taking.

(3)Tense Doctor-Patient Relations Turn Comprehensive Examinations into Physicians’ Self-Protection. Who can guarantee that a fever is due to ordinary influenza rather than the Ebola virus?

Coupled with the impact of an aging population, the demand for medical imaging examinations will continue to rise in the long term.

II. How Large Is the Third-Party Medical Imaging Market?

China originally lacked third-party medical imaging services, with each hospital purchasing its own equipment. Constrained by the existing system, public hospitals have favored acquiring large-scale medical equipment, particularly high-end devices. This practice not only enhances the hospital’s image but also provides tangible benefits to relevant personnel. As a result, imaging equipment in most regions of China is overallocated (i.e., the majority of devices in a given area remain idle and fail to operate at full capacity). Also due to systemic constraints, these underutilized devices cannot be accessed by third-party providers, leading to significant waste of resources.

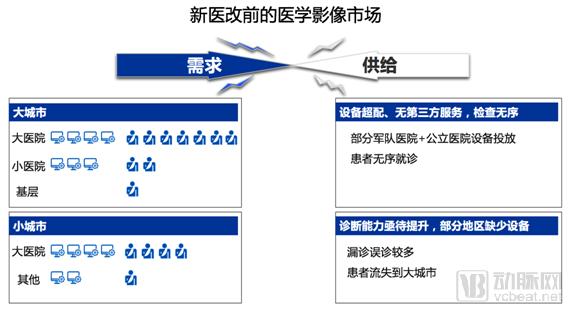

A Distinctive Feature of the Healthcare Market Prior to the New Healthcare Reform:

(1) In major cities, renowned hospitals are equipped with abundant medical devices; however, the high patient volume results in prolonged waiting times. Mid-tier hospitals (e.g., secondary hospitals) also possess considerable equipment but suffer from significant underutilization due to lower patient volumes. Primary healthcare institutions, while serving a smaller patient base, lack adequate medical equipment. Patients whose diagnostic needs remain unmet are partially accommodated through medical devices deployed via the socialization initiatives of certain military and public hospitals.

(2) In small cities, the largest local central hospitals or people’s hospitals generally have equipment capacity that is well matched to patient volume, resulting in minimal waiting times. Other hospitals may be equipped with imaging devices but serve very few patients. The primary challenges in small cities are the low standardization of image acquisition and limited diagnostic capabilities. In some economically underdeveloped regions, equipment infrastructure remains inadequate and offers room for improvement.

Following the new healthcare reforms, the state has been vigorously promoting a tiered diagnosis and treatment system, aiming to keep patients at primary care institutions in grassroots cities for initial consultations, with referrals to large hospitals reserved only for complex and critical cases. In the medical imaging market, the government has implemented four major reforms:

(1) Military hospital reforms and the cessation of paid services have led to the termination of all imaging equipment placement projects, rendering them no longer operational;

(2) A significant drop in examination fees has transformed radiology departments from highly profitable units into low-margin or even loss-making departments (under full-cost hospital accounting);

(3) Reclassify large-scale medical equipment from “non-administrative licensing items” to “administrative licensing items,” and strengthen the approval process for public hospitals’ acquisition of equipment configuration permits;

(4) Introduce measures to encourage socialized medical services, such as independent imaging centers and shared imaging resources.

The national strategy is clear: promoting tiered diagnosis and treatment necessarily entails supporting third-party imaging services, reducing government investment, controlling medical costs, and increasing social investment.

However, the original market structure cannot be changed overnight. It is quite challenging for the emerging field of third-party medical imaging to grow out of the existing industry landscape. At present, the third-party medical imaging market consists of only two segments:

(1) The market void left by the withdrawal of military hospitals and public hospitals accounts for 5%-33% of the imaging market in major cities, with significant variations across different cities;

(2) The demand for upgrading imaging equipment in county-level and prefecture-level cities has transformed the traditional model of equipment sales into partnerships with third-party imaging centers. The size of this market is difficult to estimate, as it depends on specific regional demands and opportunities, and more critically, on whether the operator can integrate local resources and persuade hospitals to forgo independent equipment purchases in favor of collaborating with third-party providers.

These two market segments are estimated to be valued at approximately RMB 15–20 billion.

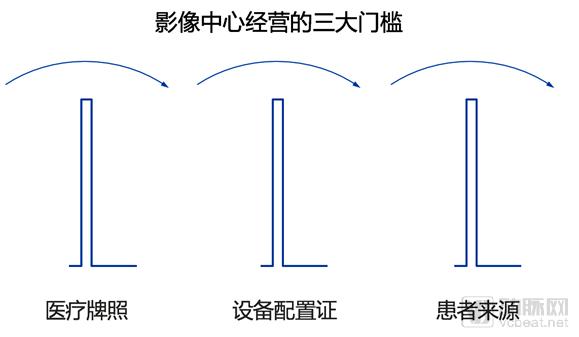

III. What Are the Challenges of Investing in Third-Party Imaging Centers?

Investing in imaging centers currently requires clearing three major hurdles: medical practice licenses, equipment configuration permits, and patient acquisition.。

Although national standards for imaging centers were issued in 2016, the pace and intensity of implementation vary significantly across different regions in China. Applications for imaging centers must follow the standard procedure for establishing medical institutions, which involves a lengthy cycle. As imaging centers require numerous large-scale medical devices, they are subject to stricter environmental impact assessment requirements, making site selection more challenging than for general medical institutions. Furthermore, the application process for medical institutions is unreasonable; applicants are required to lease premises before approval. The application process can take anywhere from six months to a year, and if the application is ultimately rejected, all upfront leasing costs are lost.

After obtaining approval for the imaging center setup, the key step is to apply for configuration permits for large-scale medical equipment, including Class A devices such as PET-CT scanners and Class B devices such as MRI and CT scanners. While the national government is tightening equipment approval for public hospitals and relaxing restrictions on private medical institutions purchasing medical equipment, the implementation of this policy has been slow, and its full rollout will require a considerable period.

Compared to the first two barriers, patient acquisition represents the most significant hurdle for independent imaging centers. Regarding the current market for third-party imaging services:

(1) To address the market gap left by the withdrawal of military and public hospitals, strong patient acquisition capabilities are required;

(2) To meet the demand for equipment upgrades in primary care hospitals, patient volume can be leveraged from the existing patient base of these hospitals. However, persuading hospitals to opt for third-party imaging centers rather than purchasing equipment independently requires extensive engagement with government authorities and public hospitals.

In addition to the three major barriers, imaging centers face high costs. Initial investments include equipment costs (ranging from RMB 20 million to RMB 50 million, depending on equipment tier and services offered), rent during the preparatory phase, and start-up expenses. Major operational costs include rent, patient acquisition costs, and compensation and benefits for operational staff. If patient volume fails to exceed the break-even point, the center faces the risk of losses.

IV. What Core Competencies Are Required to Operate a Successful Imaging Center?

To successfully operate an imaging center, or even establish a chain-based imaging center service system, four core competencies are required:

(1)Financial Strength: Capable of providing long-term financial support, which is a fundamental capability.

(2)Operational Capabilities: Possess the ability to acquire patient traffic through market-oriented means, or establish close cooperative relationships with public hospitals that already have existing patient traffic. An imaging center must possess at least one of these two capabilities to ensure its sustainable survival.

(3)Expert Resources: Imaging centers should be able to bring together China's top imaging examination technologies and diagnostic experts, improve the quality of imaging examinations, and extend high-quality diagnostic capabilities to primary healthcare institutions through internet and artificial intelligence technologies, thereby highlighting the advantages of third-party imaging services.

(4)Chain Management: Traditional medical imaging service providers, despite having numerous projects across China, operate in silos with a lack of unified and standardized management capabilities, resulting in no synergistic effects. The radiology departments within large hospitals and third-party imaging centers follow two entirely different management models. Radiology managers from public hospitals are often unable to adapt to market demands, and there is currently a shortage of talent skilled in managing chain medical institutions. With the rise of private medical institutions, this has become a challenging issue across various specialized sectors of healthcare.

V. What Does the Future of Third-Party Medical Imaging Look Like?

The market size of independent third-party imaging centers in the United States is approximately $17 billion, accounting for about 40% of the entire imaging services market. Drawing on U.S. development experience, the imaging center market is relatively fragmented due to high asset intensity, strong regional characteristics, and limited service radii; the largest player, RadNet, holds only about 5% of the total market. In recent years, imaging centers have primarily relied on mergers and acquisitions to expand their scale, and amid mounting insurance reimbursement pressures, many are seeking partnerships with hospitals. These development trends are also expected to emerge in China.

However, China’s healthcare environment differs significantly from that of the United States. Currently, the scale and pace of development in third-party medical imaging are more constrained by the speed and intensity of national policy implementation, particularly regarding tiered diagnosis and treatment. The deeper and faster the implementation of tiered diagnosis and treatment, the more rapidly third-party imaging services will develop. If large hospitals were to truly eliminate outpatient services and accept only referred and emergency patients, third-party imaging would undoubtedly experience explosive growth. Domestic existing imaging equipment is already over-supplied, resulting in substantial waste due to large-scale redundant investments. Furthermore, patient visits exhibit strong seasonal and cyclical fluctuations. By integrating imaging resources through medical consortiums to provide unified patient services, and by allocating examination schedules based on patient needs and physicians’ requirements, healthcare efficiency and quality could be significantly improved while overall costs are reduced.

About the Author: Liu Weiqi (Founder and CEO of Tongxin Medical Alliance; Research Fellow at the School of Economics and Management, Tsinghua University)

Bachelor of Science in Civil Engineering and Finance from Shanghai Jiao Tong University; Master of Science in Management Science and Engineering from Stanford University, USA; Master of Laws in Administrative Law from the Party School of the Central Committee of the Communist Party of China. A seasoned expert in the healthcare and financial sectors, he previously served as Managing Director at Huakang Tongbang Technology Co., Ltd., and as Chief Operating Officer of Emerging Markets Securities Operations and Head of China Project Development for UBS Group’s Asia-Pacific region. He has been honored with the titles of “Zhongguancun Entrepreneurial Leading Talent” and “Haidian District Entrepreneurial Leading Talent.” The company he founded, Tongxin Yilian, was recognized by the Zhongguancun Administrative Committee as a “Zhongguancun Golden Seed Enterprise” and a “Zhongguancun High-Tech Enterprise.” Currently, the company has completed its fourth round of financing, led by CICC Kangrui.