EY Life Sciences 4.0 Report: When the Human Body Becomes the Largest Database, Who Will Take the Lead?

The core of Life Sciences 4.0 lies in capturing value through data-driven platforms. In EY’s newly launched Progressio article series, we explore how advancements in science and technology are reshaping and enhancing consumers’ perceptions of health.

In this dynamic landscape, every data company is aligning itself with the tech sector by continuously developing medical products and providing related services; likewise, every tech company is gradually transforming into a health-focused entity, striving to acquire consumer-generated health information and other health-related data.

Meanwhile, ubiquitous peer-to-peer sharing tools—such as smartphones and wearable devices—are transforming consumers into “super consumers.” These super consumers expect high-quality services from the health ecosystem that rival those they receive in other areas of their lives. Consumers are gaining greater voice and gradually displacing enterprises as the leading force in this market.

The rise in the number of super-consumers, coupled with the emergence of related technologies, has provided new insights for other stakeholders, such as those involved in artificial intelligence and the Internet of Things. This trend is causing life sciences companies to gradually lose their market control. To regain their influence, these companies must make strategic and differentiated changes, focusing on the future: not only improving patients' health outcomes but also meeting their highly personalized needs.

In this era, products are no longer the core driver of value. Life sciences companies must innovate their business models by focusing on outcomes and personalization. Meanwhile, to create future value, life sciences companies must also develop their own systems to facilitate value sharing. This means that biopharmaceutical and medical technology companies must strengthen communication with upstream and downstream partners, actively solicit feedback, and cultivate more talent with specialized expertise.

Life Sciences 4.0 is both an urgent global imperative and an opportunity rich in value. Companies that can build platforms and curate their proprietary data will position themselves at the forefront of the era, unlocking boundless future value.

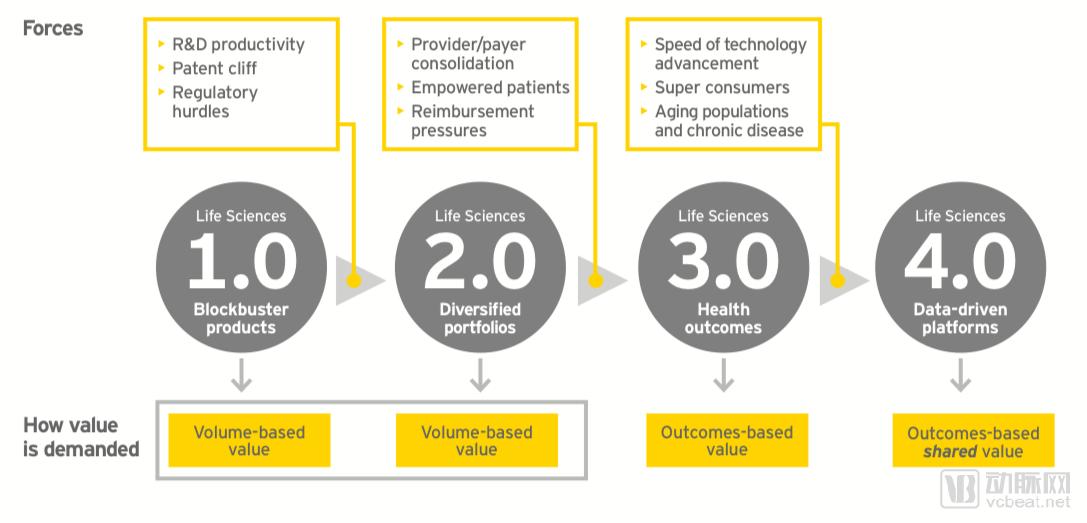

As time passes and technology evolves, the market changes rapidly. Life sciences companies are under unprecedented pressure; they must transform their business models and personalize their products and services to avoid being swept away by the tide.

To create more value, life sciences companies should consider participating in data-centric platforms to improve business performance and reduce costs.

In this environment, the platform will provide enterprises with a framework to create future value while strengthening their capabilities in connectivity, data integration, and data sharing.

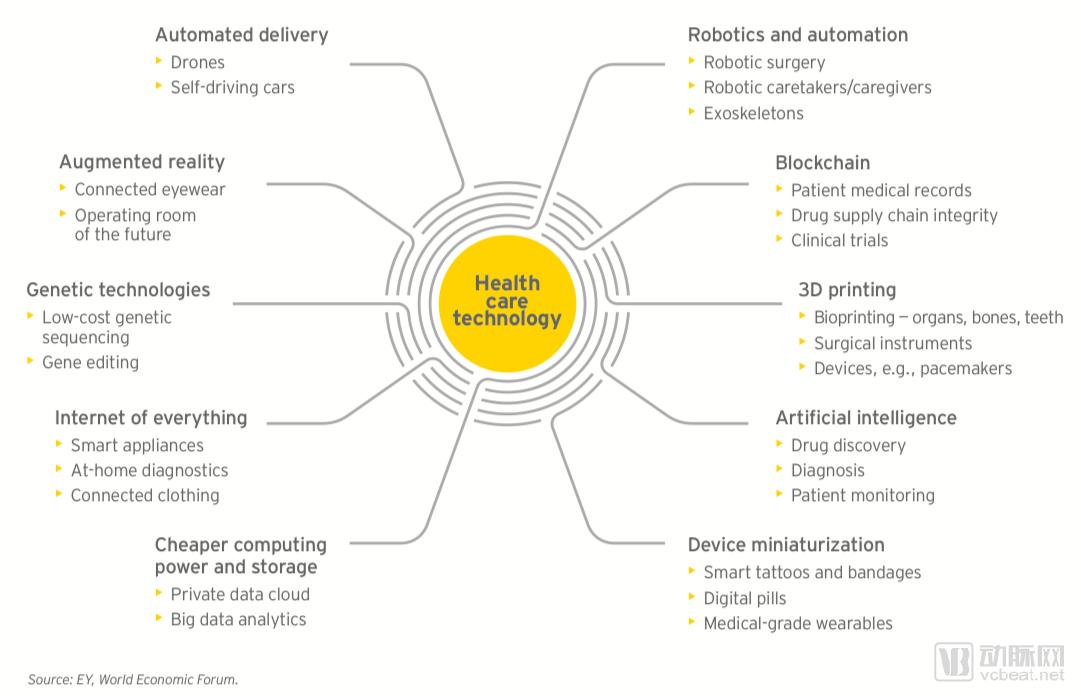

We are entering the Fourth Industrial Revolution. Affordable storage and increasingly powerful microprocessors are driving the development of emerging technologies such as 3D printing, blockchain, and artificial intelligence (AI), leading to “the fusion of the physical, digital, and biological worlds.”

In this context, super consumers are placing higher demands on the healthcare system, significantly reshaping the landscape of healthcare services. Consumers are regaining their bargaining power.

Advances in new technologies and devices have fueled a growing willingness among individuals to view and share their health data, as consumers strive to have a say in their lifelong health journeys. These demands are not only reshaping the patient–physician relationship but also encouraging patients to take a more proactive role in managing their own healthcare. All stakeholders urgently need to integrate existing disease-related data and solutions into comprehensive, data-driven platforms.

The seamless sharing of data has invisibly raised consumers’ expectations for healthcare quality and created opportunities for more precision medicine research. Consequently, the healthcare services sector is undergoing a profound transformation.

This means that innovation is no longer solely product-centric.Companies need to focus on a range of services, including customer engagement, personalized treatment, and data integration. The blockbuster therapies of tomorrow are likely to be algorithms that synthesize scientific, behavioral, economic, and financial forecasts to treat, or even prevent, diseases. Therefore, life sciences companies must consider how and when to engage with emerging data platforms to seamlessly collect, integrate, and share diverse health data in real time. We refer to these platform-based business models as Life Sciences 4.0.

New Health Technologies Spawned by the Mobile Internet

A hyper-liquid market refers to a market in which frictions among economic agents are eliminated. The healthcare market has not yet achieved this state of hyper-liquidity. As patients move among multiple caregivers, the overall experience remains disappointing; the absence or restriction of legal frameworks makes it difficult for physicians to easily share the information necessary to optimize care. However, the situation is inevitably shifting in a positive direction.

Since 2017, multiple organizations have joined forces to develop new healthcare services and products, guided by the core principles of enhancing convenience and adopting a customer-centric approach. These services and products will empower future consumers with the right to choose when and where to receive medical care, as well as control over their own health data.

The convergence of artificial intelligence, robotics, and 3D printing is creating opportunities for consumers and physicians to transform health data into actionable insights. With the advancement of wearable devices, consumers are empowered to make better decisions regarding their health and lifestyle. Ultimately, instead of consumers seeking out healthcare services, numerous companies will begin competing for their attention.

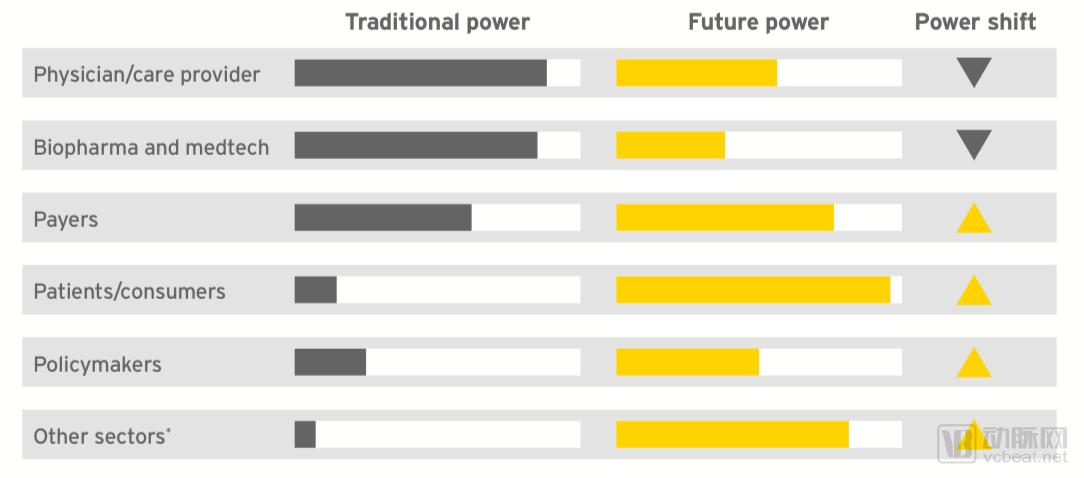

Value Distribution Among Future Healthcare Market Participants

Historically, innovation will continue to be a core component of value creation for life sciences companies. However, these innovations will be based on the comprehensive efforts made by enterprises in achieving goals related to personalization, quality of health, and cost. In other words, to create future value, life sciences companies must develop systems to adjust objectives and share value among stakeholders.

In certain therapeutic areas, particularly in the management of chronic diseases, digital infrastructure oriented toward patients will play an increasingly important role in care-related ancillary services, such as transportation and physician appointment scheduling. Indeed, innovation will be driven by more diverse data streams originating outside the traditional healthcare ecosystem. Life sciences companies need to find ways to securely and rapidly leverage these disparate data sources and integrate them with deep scientific and clinical data.

In healthcare, platforms have become a means of connecting patients, physicians, payers, policymakers, and product manufacturers. Once connected, these stakeholders can combine the strengths of their respective roles with shared data, thereby transforming the currently fragmented approach to care. Companies will develop software centered on individuals to capture data that helps people diagnose and treat health conditions.

Although life sciences companies currently possess only limited cost-related data, they have access to a wealth of clinical data. By integrating this clinical data with environmental, behavioral, and financial analyses, these companies have the opportunity to become key drivers of future value.

In doing so, life sciences companies can strengthen their position as leading medical technology providers within the broader ecosystem, operating healthcare sector networks to facilitate the exchange of information and services, thereby delivering greater benefits to individuals, physicians, governments, and insurance companies.

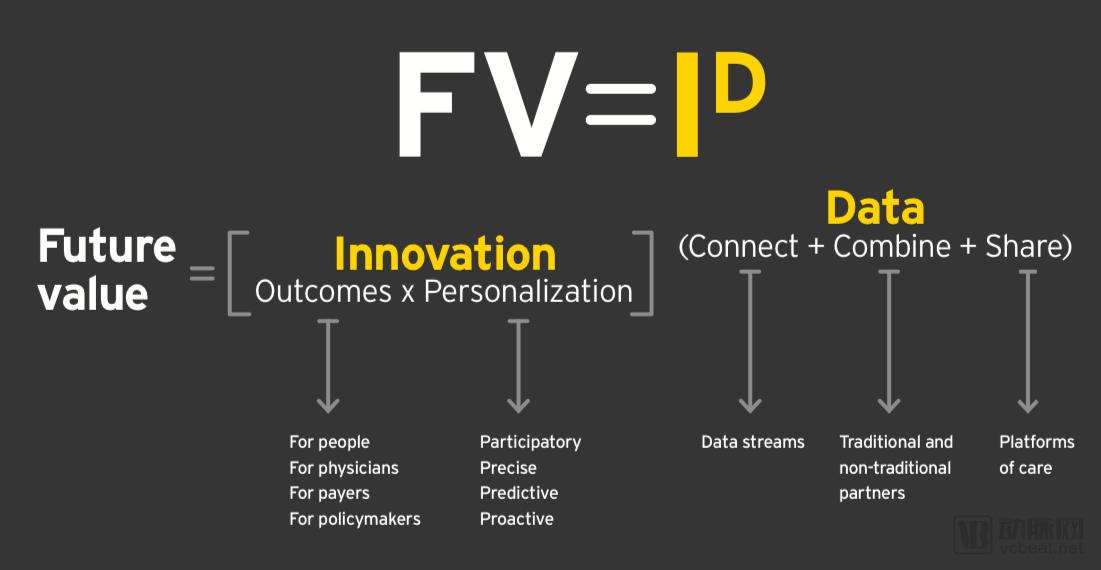

The New Equation for Value Innovation: Future Value = Innovation + Data

By engaging with emerging nursing platforms, life sciences companies can build relationships with healthcare stakeholders, thereby developing new products that meet their customers’ needs.

If life sciences companies fail to engage with care platforms, they risk being marginalized by emerging technologies and digital players that will fill the gaps with their own products.

Success in the emerging platform environment requires the launch of new features, such as personalized services and data integration.

Digital health startups and established tech companies are already leveraging their expertise in engineering skills and data analytics to serve consumers, physicians, and payers. These efforts have now gone beyond sleep tracking and cloud-based data storage services; indeed, new technologies have arguably surpassed all core product offerings historically provided by life sciences companies.

Many life sciences companies view these developments as an existential threat. In the October 2017 EY Global Capital Confidence Barometer survey, respondents identified intensified competition from companies outside the industry as the greatest risk to maintaining their market position.

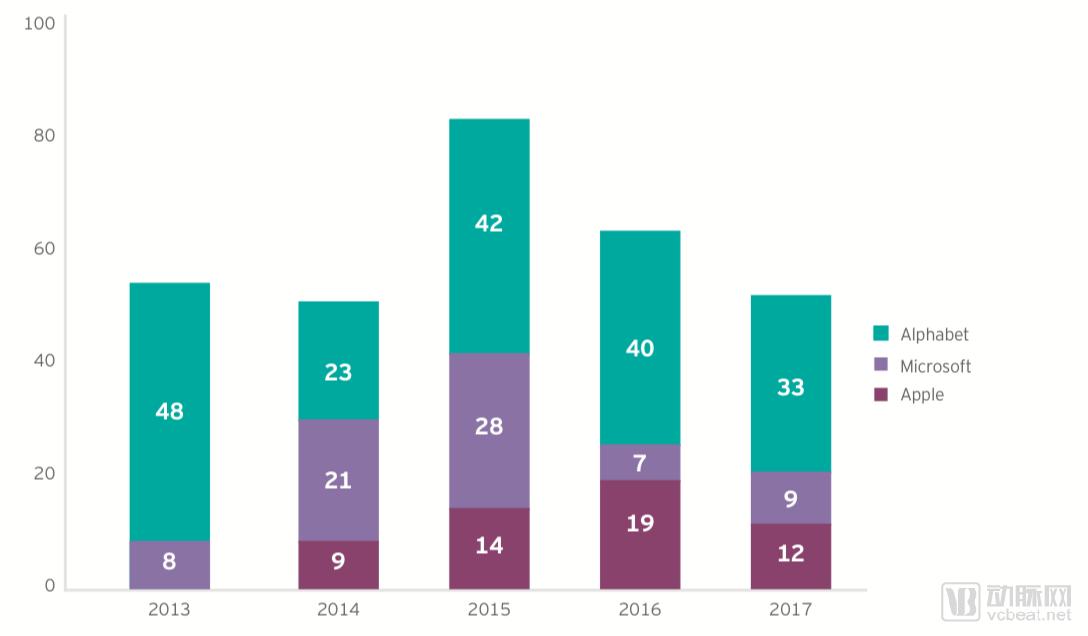

EY’s analysis of health-related patents held by major technology players such as Alphabet, Apple, and Microsoft reveals that these tech giants are making significant inroads into the healthcare sector. For instance, Alphabet has a portfolio of projects under DeepMind and Verily Life Sciences, including joint ventures focused on diabetes management (Onduo), bioelectronics (Galvani Bioelectronics), and smart operating rooms (Verb Surgical).

Statistics on the Number of Patents Applied for by Tech Giants in the United States

Medical technology companies and biopharmaceutical companies have responded by partnering with digital collaborators and launching corresponding exploratory initiatives. For instance, in the biopharmaceutical sector, we have witnessed numerous emerging digital innovations, such as the sensor embedded in Abilify (developed by Proteus Digital Health and Otsuka). In the medical technology field, Philips has developed an automated medication ordering service for the elderly, which is part of its cloud-based digital platform, HealthSuite.

These efforts are important, but they cannot completely eliminate risks. Current plans typically focus on developing key products, but do not necessarily place new connectivity technologies at the core of their strategic business objectives. Furthermore, because current investments are made in isolation across the entire portfolio, companies face the risk of underinvestment, even though new technologies will transform their business models and generate significant future returns.

Most major life sciences companies are vertically integrated business structures, organized around one of the following four broad business models:

1. Breakthrough Innovators: Develop top-tier products with higher prices, primarily covered by health insurance.

2. Disease Managers: Develop products and solutions for managing chronic diseases.

3. Efficient manufacturers: developing low-cost products.

4. Product Manager: A product developer who sells products directly to consumers, focusing on prevention and overall health maintenance.

Regardless of the business model, a key characteristic of platforms is their ability to create positive feedback loops that ultimately drive sustained customer engagement. In the healthcare sector, platforms offering products and services that monitor patient conditions and provide medication adherence coaching may hold inherent advantages.

As the number of users and frequency of use increase, the platform itself becomes more valuable due to newly generated data.

The fact that Facebook and Alibaba have been able to dominate their respective markets demonstrates the significant first-mover advantage enjoyed by companies that establish platforms early. By 2017, Facebook’s user base had surpassed 2 billion. In China, Alibaba dominates e-commerce; by the end of 2017, its platform boasted over 450 million annual active buyers. In both cases, robust platform growth created a positive feedback loop, ultimately leading to market dominance.

How do network effects operate in the healthcare sector? Let us take diabetes management as an example. Consider the development of two distinct diabetes platforms. Platform A integrates a suite of services, including cloud-based storage for HbA1c measurements, real-time messaging alerts, insulin level management, and tools for tracking and analyzing activity levels and nutritional intake. In contrast, Platform B offers fewer services, potentially limited to routine metric monitoring. As more patients with diabetes congregate on Platform A, its growing popularity will attract even more registrations. Furthermore, as the user base expands, service providers may prioritize participation in Platform A due to its greater influence. The ultimate outcome is that Platform A becomes increasingly dominant, while Platform B fades into obsolescence.

To transform their business models, life sciences companies must begin designing a broader range of personalized services. These offerings should incorporate novel approaches to studying individual behaviors, engagement styles, and risk management.

Intuitively, the revenue generated by enterprises building platforms in specific disease areas is not difficult to imagine. Some life sciences companies may choose to develop their own platforms, while others will find other ways to participate in digital platforms.

The healthcare sector is witnessing a continuous emergence of services and products for chronic disease management, but early market performance has been lackluster.

Most life sciences companies lack the capability to build platforms and do not have the resources to develop comprehensive care platforms from scratch, making “deal-making” essential.

EY’s analysis indicates that life sciences companies are leveraging “transactions” to develop new products or enhance existing products and services, while simultaneously collecting and building real-world data.

Few life sciences companies possess the financial resources to compete with a well-capitalized technology player in the realm of platform creation.

The reason tech companies are drawn to the healthcare sector is that, while they have developed data solutions, they have failed to address the health concerns that matter most to end users. Life sciences companies, by contrast, understand consumers’ medical needs and know how to develop products within existing regulatory frameworks. Tech companies now have an opportunity to assume a leading role in shaping primary care platforms.

At the outset, multiple platforms may compete for the same customer base. However, over time, leading platforms specializing in specific disease categories are likely to emerge, prompting customers to gradually concentrate around these focused players.

Founded in 2015, Helix is a platform dedicated to personal genomics that provides genetic sequencing services to customers and allows them to access their data. Helix also offers a suite of applications delivering genomic interpretations, as well as entertainment, family, fashion, health, and nutrition insights. Partners can leverage Helix’s API to develop new products on the platform, enabling direct utilization of data within the genomic ecosystem. All products launched on Helix must undergo its internal Scientific Evidence Evaluation (SEE).

According to Ernst & Young statistics, among nearly 90 companies with clearly defined partnerships, 50% are involved in the diabetes or respiratory sectors, while 14% focus on oncology-related products or services.

Similarly, among patients with diabetes, the three major insulin suppliers have established partnerships to provide consumers with better services.

Sanofi and Alphabet’s Verily Life Sciences have established the joint venture Onduo; Eli Lilly has partnered with Livongo to conduct trials aimed at better understanding consumer health behaviors; Novo Nordisk has collaborated with Glooko to launch a free mobile application for diabetes management; Roche took a step toward building a patient-centric digital health service platform by acquiring mySugr in 2017; and Johnson & Johnson has continued to expand its business scope through agreements with Qualcomm and WellDoc.

The first step for a health platform is to provide health management and chronic disease management.

The landscape of cancer treatment has undergone significant changes. First, certain cancers, such as multiple myeloma, are no longer considered acute diseases but rather chronic conditions that can be managed over several years. Second, as patient demand for treatments based on molecular profiling and other clinical trials continues to grow, platforms can optimize individualized therapeutic pathways. Third, with an increasing number of biopharmaceutical companies racing to launch targeted drugs in the market, competition among biosimilars is intensifying; platforms can help first-movers stand out in this crowded marketplace.

Due to cost constraints, minor adjustments to the payment model are insufficient to meet future demands. The entire payment model requires a more thorough overhaul.

Life sciences companies must move beyond product-centric operating models to create complex, data-driven partnerships that share value with other healthcare stakeholders.

Support for simple, transparent data-sharing platforms is crucial to the development of these partnerships.

In the Life Sciences 4.0 era, value is transmitted among all stakeholders within the ecosystem

In recent years, life sciences companies have implemented patient education initiatives to strengthen their position within the health ecosystem. Nevertheless, a significant trust gap persists.

As health platforms become a critical component in capturing future value, life sciences companies can leverage data to deepen existing relationships. They can help stakeholders achieve value-based goals, including improving the quality of care, reducing the total cost of care, and, most importantly, enhancing overall long-term health outcomes.

Payers: A small number of life sciences companies have begun collaborating directly with payers, linking product reimbursement to improved health outcomes. Many such contracts focus on reimbursing diabetes or cardiovascular products, as their outcomes are easier to standardize and measure. The emergence of more complex and costly cell and gene therapies is now prompting life sciences companies and payers to revisit approaches to pricing these treatments.

Pharmaceutical Manufacturers: Governments around the world are seeking to digitize healthcare and transition it to lower-cost environments. Efforts to date have focused primarily on building the necessary infrastructure, including electronic health records (EHRs), online procurement and regulatory submission systems, as well as systems for tracking product movement throughout the supply chain.

Life sciences companies strive to build trusted relationships with stakeholders and create more innovations that contribute to human health. For example, in the 2016 Gallup poll assessing corporate reputation, 50% of more than 1,000 adults gave the pharmaceutical industry a negative rating, making it the second-least favored business sector. This marked the pharmaceutical industry’s worst performance in the 16-year history of the survey.

These negative perceptions expose a serious problem: the industry has failed to innovate in a manner consistent with stakeholders’ definitions of value. Predatory product pricing harms the entire industry.

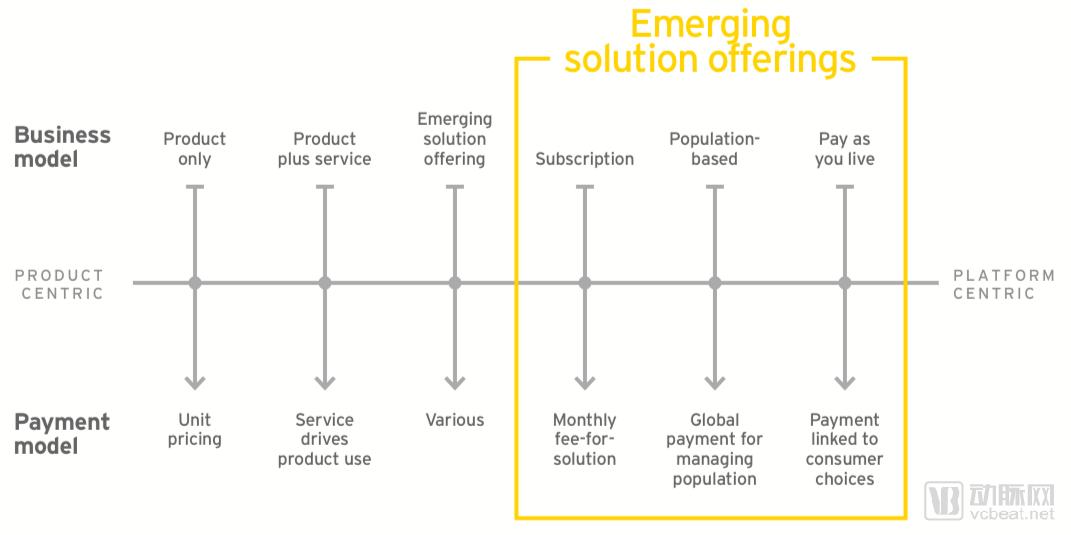

Subscription-Based Model: The subscription model enables consumers to access more affordable services. For physicians, this model allows them to devote greater attention to individual patients and provide continuous, follow-up care. For life sciences companies, the subscription model offers direct engagement opportunities with other healthcare stakeholders.

Pay for Lifestyle: A recent trend in the insurance market is the rise of the “Pay for Lifestyle” (PAYL) model, which rewards customers for adopting healthy behaviors, such as maintaining a healthy weight or not smoking. Wearable devices or mobile phones can help patients provide data to insurance companies. This model encourages consumers to pay lower premiums and enjoy a healthier lifestyle. In the long term, this will reduce users’ risk of developing chronic diseases.

# Paradigm Shift

1. To create future value, life sciences companies must determine how to identify disruptive advantages in today’s era of transformation;

2. The diversity of data and analytics presents new opportunities for life sciences companies to rethink innovation;

3. Platforms that connect, integrate, and share data will become the core drivers of future value creation;

4. These platforms can generate diverse data streams and link them with clinical data;

5. The company also needs to consider developing new features related to customer engagement, personalized services, and data integration, which are core to emerging care platforms;

6. Life sciences companies can acquire these capabilities through in-house development, flexible partnerships, or acquisitions.

These customer-centric capabilities will drive life sciences companies to leverage data to transform their business models, creating shared value for themselves and health stakeholders across the entire ecosystem.