2018 Report on the Commercial Value Realization of Gene Technologies: NIPT Matured in a Decade, with Tumor Testing and Microbiome Sequencing Holding Vast Growth Potential

Genetic research is an exploration of the origins of life, offering an alternative perspective on life and health compared to modern medicine. A company’s mission is to deliver substantial returns to its employees and enhance wealth for its owners, while realizing social value. Genetic companies are no exception; we cannot avoid addressing the issue of commercialization in genetics.

This report tracks the evolutionary trajectory of gene technologies, reviews the commercialization process of the gene industry, proposes a relatively comprehensive evaluation framework, and explores the commercial value of gene technologies.

At the 5th NGS Innovation Developers Conference, VCBeat. Eggshell Institute delivered a presentation titled “Exploring the Commercial Value of NGS.” This article is an excerpt from that report.

This report is divided into four parts, primarily including:

I. Industrial Development Path

1.1 From Devices to Services: Advancements in Basic Research Drive Industry Diversification

1.2 National Strategy: Continuously Elevating the Status of Genomics

II. Landscape of the Gene Industry

2.1 Industry Giants Establish Full-Industry-Chain Layouts, with Downstream Applications Gradually Increasing

2.2 The Sudden Rise of Domestically Produced Sequencers

III. Pathways to Realizing Commercial Value

3.1 Industry Commercialization Assessment Framework

3.2 Clinical-Grade Genetic Applications: Technology Reigns Supreme, Diverse Innovations Flourish

3.2.1 NIPT: A Lucky Ticket, Achieving Commercial Maturity in 10 Years

3.2.2 Tumor Detection and Treatment: Vast Market Potential with Sustained Policy Support

3.2.3 Microbial Sequencing: Basic Research and Regulation Are Still Being Refined, but the Biggest Challenge Is Time

3.3 Consumer-Grade Genetic Applications: Navigating Growing Pains Through Branded Operations

IV. Value Outlook

4.1 The gene industry enters a phase of endogenous growth, with industrial capital flowing in to unlock scenario-based value

4.2 What Are the Boundaries of Cross-Industry Collaboration in Genetic Technology?

1.1 From Devices to Services: Advancements in Basic Research Drive Industry Diversification

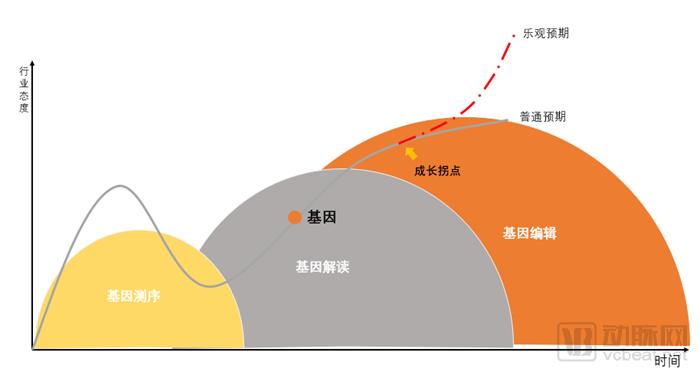

Based on our understanding of the developmental trajectory of gene technology, we categorize its evolution into three stages: the first stage is gene sequencing, the second is gene interpretation, and the third is gene editing.

Noun Explanation:

Gene Sequencing: Gene sequencing refers to the determination of the order of nucleotide bases in DNA molecules using sequencing equipment. It involves identifying and interpreting the sequence of the four bases—adenine (A), thymine (T), cytosine (C), and guanine (G)—to obtain a complete genetic sequence.

Gene Interpretation: The process of comparing curated sequences against an integrated database to identify gene functions and detect loci within the gene sequence that are specific to those in the database, thereby determining the relationship between phenotypic traits and genetic loci.

Gene Editing: A suite of technologies that use biotechnology to directly manipulate the genome of an organism, thereby altering the genetic material of cells. This includes gene transfer within the same species or across different species to generate improved or novel organisms. New genetic material can be inserted into the host genome by isolating and replicating the desired genetic material using molecular cloning techniques to produce DNA sequences, or by synthesizing DNA, which is then introduced into the host organism. Nucleases can be used to remove or “knock out” genes. Gene targeting employs homologous recombination through various techniques to modify endogenous genes, and can be used for gene deletion, exon removal, gene addition, or introduction of point mutations.

The development of first-generation gene sequencing technology was marked by the implementation of the Human Genome Project. However, limited sequencing throughput and high costs remained the primary obstacles to in-depth genomic analysis. The introduction of high-throughput sequencing technology in 2005 initially addressed this issue, leading to a rapid decline in the cost of human genome sequencing. The extensive procurement of sequencing instruments and the sequencing of various animals and plants helped cultivate China’s talent pool in sequencing technology, accelerated the country’s understanding of the genomics industry, and laid the foundation for China’s entry into the field of genomic data interpretation.

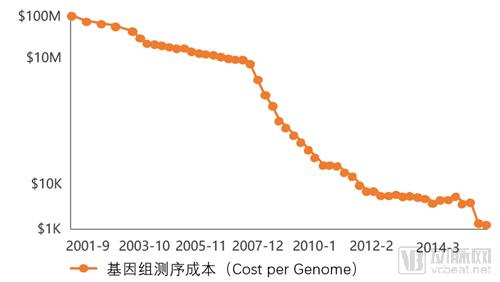

Advancements in sequencing technology have led to a rapid decline in costs, significantly driving commercial development. Second-generation sequencing technologies reduced the average cost of gene sequencing per megabase from $5,292 in 2001 to $0.014 in 2015 (a nearly 380,000:1 reduction). The cost of personal genome sequencing was approximately $100 million in 2001; by 2014, Illumina’s HiSeq X Ten sequencing platform had lowered the cost of whole-human-genome sequencing to under $1,000. In January 2017, Illumina launched its NovaSeq series of high-throughput sequencing platforms. On January 9, 2018, at the J.P. Morgan Healthcare Conference, global genetic testing giant Illumina announced the release of the NovaSeq sequencers, which reduce the cost of gene sequencing to $800 thanks to their unparalleled throughput, streamlined operation, low cost, and flexibility.

The NovaSeq series has also achieved breakthroughs in sequencing speed. While whole-genome sequencing on the HiSeq X takes 72 hours, the NovaSeq series reduces this time to 40 hours. Although the $100 genome has not yet been fully realized, Illumina states that this goal will be achieved within the next few years. The launch of the NovaSeq system at least marks the advent of the era of $100-level gene sequencing. With further technological upgrades, it is believed that the market price for gene sequencing will drop to $100, leading to a broader user base and more extensive applications for genetic testing.

Genome Sequencing Costs, 2001–2016

The second phase of genetic interpretation, in simple terms, involves deciphering human genetic information to describe individual physiological functions, disease characteristics, and personalized factors relevant to disease treatment. These insights can be applied to talent assessment, health management, disease risk evaluation, disease diagnosis, and medication guidance. Genetic interpretation uses gene sequencing results as its foundational input and relies on a deep understanding of biological processes as its core technology, serving as a fundamental informational guide for health and lifestyle. Gene decoding represents an advanced evolution of genetic testing; compared to conventional genetic testing, it offers more precise and forward-looking interpretation of genetic information and personalized recommendations.

The third stage is gene editing. While gene interpretation can identify the causes of disease, and targeted drugs, interventions, and healthcare plans can be designed based on the identification of pathogenic genes through gene decoding, these approaches cannot fundamentally eliminate the root causes of disease. Since genetic defects are present in every cell of the human body, and diseases arise from the combined effects of these defects in every cell or at least in a large number of cells, only by removing the pathogenic genes is it possible to fundamentally treat diseases caused by genetic defects. Moreover, many severe diseases are caused by changes in a single gene at a single locus. Gene decoding can accurately determine the location of the defective gene, thereby making gene correction possible.

As foundational gene sequencing technologies mature and costs decline rapidly, the emergence of gene interpretation and gene editing technologies has endowed the genomics industry with diverse characteristics. We anticipate that the industry will reach an inflection point and embark on an optimistic growth trajectory when gene interpretation technology enters its latter half of development and gene editing technology advances into its early stages.

1.2 National Strategies Continuously Elevating the Status of the Genomics Industry

As a key innovative technology in medical advancement, genetic testing has been elevated to the status of a national strategy in China, driven by the consecutive issuance of several important policies in recent years.

Below is a review of China’s major gene-related policies from 2015 to the present:

July 2015, “Notice on the Implementation of Major Project Packages for Emerging Industries”: “Accelerate the clinical application of genetic testing and the domestic production of genetic testing instruments and reagents, with a focus on genetic screening for hereditary diseases and birth defects, so as to promote the widespread and public-benefit adoption of advanced health technologies such as genetic testing.”

March 2016, “Draft of the 13th Five-Year Plan”: Genomics was included among the 100 major projects and initiatives planned for implementation in China over the next five years.

July 2016, “13th Five-Year Plan for National Scientific and Technological Innovation”: “Focus on overcoming core key technologies in precision medicine, such as next-generation gene sequencing technology, omics research, and big data integration and analysis technology; develop a batch of precise application solutions and decision support systems for early screening, molecular subtyping, personalized treatment, efficacy prediction, and monitoring of major diseases.”

January 2017, "13th Five-Year Plan for the Development of the Biological Industry": Genetic testing capabilities (including preconception, prenatal, and newborn screening) to cover more than 50% of the birth population.

In May 2017, the Ministry of Science and Technology issued the Notice on Printing and Distributing the “13th Five-Year” Special Plan for Biotechnology Innovation. The document identified breakthroughs in several cutting-edge key technologies as the next priority tasks, including the development of next-generation gene sequencing technologies, novel gene manipulation technologies, and microbiomics.

In addition to elevating gene technology to a national strategic level through policy, implementation efforts have also advanced rapidly; guided by the “Plan,” various localities have promptly issued corresponding guidelines.

On January 16, 2017, the official website of the Hainan Provincial People’s Government released the “Opinions of the General Office of the Hainan Provincial People’s Government on Supporting the Application of Gene Testing Technologies,” which put forward 12 recommendations covering areas such as the establishment of a testing institution system, improvement of payment mechanisms, industrialization, and talent development. Meanwhile, Hainan Province also proposed to strengthen support for key projects, including financing support and international cooperation.

In May 2017, the Zhejiang Provincial Price Bureau, the Health and Family Planning Commission, and the Human Resources and Social Security Department jointly issued a notice in accordance with the “Notice of the National Development and Reform Commission on Issues Concerning the Acceleration of Acceptance and Review of New Medical Service Price Items,” establishing pricing standards for multiple molecular diagnostic products.

In addition to these two regions, multiple provinces including Hunan, Guizhou, Henan, and Guangdong have successively introduced corresponding supportive policies since 2015. Furthermore, local price bureaus have established pricing standards for non-invasive prenatal testing (NIPT), and certain provinces and municipalities have included NIPT in their medical insurance coverage.

On October 10, 2017, the General Office of the National Development and Reform Commission (NDRC) issued a reply concerning the construction plans for the second batch of demonstration centers for genetic testing technology applications. The General Office of the NDRC granted preliminary approval to the construction plans submitted by the development and reform commissions of Hebei, Liaoning, Jiangxi, Chongqing, Hainan, and Qinghai provinces (municipality), as well as those of Dalian and Xiamen.

The reply letter requires all provinces and municipalities to actively study and implement measures supporting the application of genetic testing technologies, strengthen coordination among various functional departments, improve the management systems and mechanisms of demonstration centers, promote technological innovation, product innovation, service innovation, and business model innovation by relevant entities, and facilitate the widespread adoption of genetic testing technologies for public benefit.

1.1 Industry Giants Expand Across the Entire Value Chain, with Downstream Applications Gradually Increasing

In the gene sequencing industry’s supply chain, upstream players are primarily manufacturers of sequencing instruments and reagents/consumables. While sequencing instruments serve as the revenue platform for these manufacturers, it is the instrument-compatible reagents and consumables that truly generate profits.

The midstream segment comprises companies that provide sequencing services. These firms purchase upstream sequencing instruments to serve downstream demand, generating revenue from service fees.

The downstream sector is divided into two parts: scientific research and clinical applications. Sequencing technology was first applied in the research sector, and later gradually entered the clinical sector through mature processes. Currently, downstream market applications are extensive and diverse.

We can view the upstream manufacturers and R&D developers of sequencers and consumables, as well as the midstream providers of sequencing services, as the “shovel sellers” in this genomic “gold rush.” They earned their first pot of gold by providing technologies for basic research during the early stages of the genomics industry, before gene sequencing technology was widely adopted in clinical applications.

In downstream application areas, reproductive health applications represented by NIPT have matured, while the consumer-grade healthcare sector outside of serious medical care is also flourishing. Overseas companies such as Ancestry and 23andMe have each sequenced over one million individuals, while domestic firms like 23Mofang and WeGene have already served more than 100,000 customers. These companies have completed initial user education efforts and are approaching financial break-even.

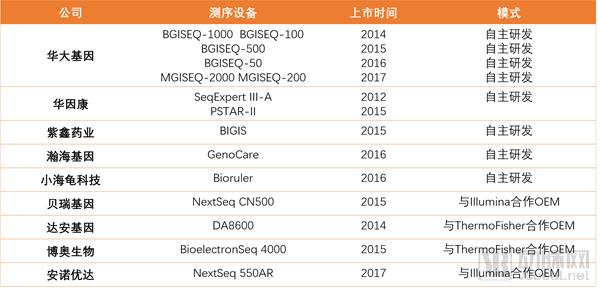

2.2 The Emergence of Domestically Produced Sequencers

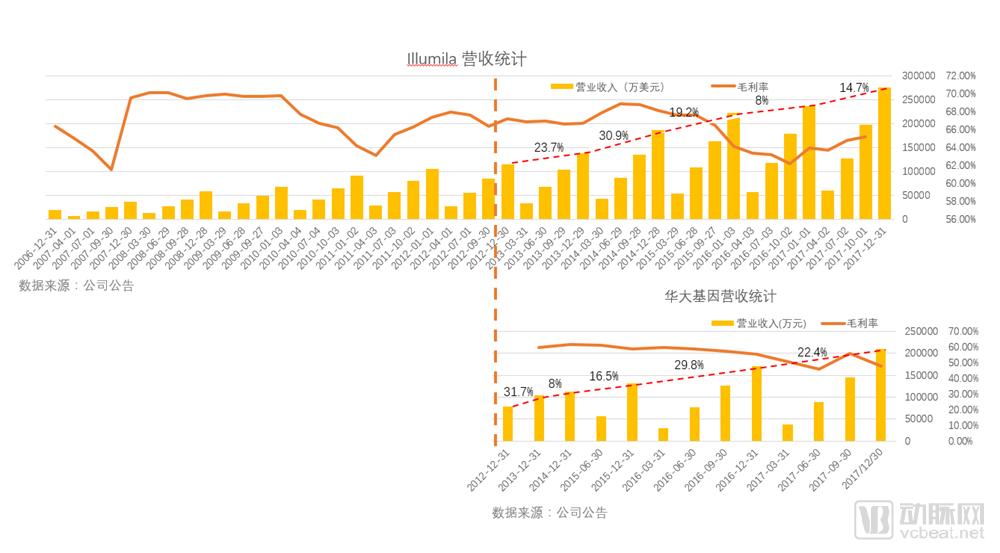

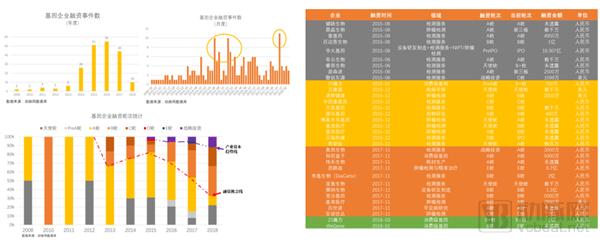

In 2017, two industry leaders, BGI Genomics and Berry Genomics, went public one after another. The tumor detection sector was poised for rapid growth, microbiomics gradually expanded under policy guidance, and the industry’s development became increasingly diversified. Meanwhile, with the launch of domestically developed sequencers independently innovated by MGI Tech and Hanhai Gene, the battle for domestic substitution in the upstream sequencing segment was officially underway.

In mapping out the gene industry’s value chain, it becomes evident that after years of cultivation in the midstream and downstream segments, industry giants have accumulated sufficient talent and resources to begin penetrating upstream activities, thereby establishing a comprehensive industrial ecosystem. In the upstream segment of the gene sector—particularly in the core area of sequencers—Illumina, Thermo Fisher Scientific, and Roche are the three market leaders. They control the lifeline of the upstream sequencing industry and wield absolute influence globally. However, as the sequencing industry matures and the market expands, some of their customers have started to enter the upstream market, becoming competitors.

In the early years, due to the immaturity of their technology and market presence, these companies rarely unveiled products even after announcing their entry into the upstream market, posing little threat to later entrants. Over time, however, these companies have gradually matured in both talent and technological reserves, allowing former followers to grow stronger and more competitive.

Today, Illumina and Thermo Fisher Scientific are surrounded by a new wave of competitors eyeing their dominant market positions. BGI Genomics launched two new sequencers this year; although their market share remains far behind that of the HiSeq X and Life Ion Proton platforms, the BGISEQ series has demonstrated product feasibility through scientific research and is gradually gaining industry acceptance and recognition.

In April 2017, the open-access journal GigaScience published the first human whole-genome resequencing data generated by the BGISEQ-500 sequencing platform. The release of these BGISEQ-500 sequencing data also laid the foundation for the development of domestically produced sequencers in China.

Data published in the journal GigaScience includes a comparison of sequencing data from the BGISEQ-500 and Illumina’s HiSeq 2500 platforms. The results demonstrated that the BGISEQ-500 PE100 and HiSeq 2500 PE150 datasets exhibited high alignment rates, similar genome coverage, and concordant variant detection outcomes. Within just over a year, the BGISEQ-500 platform has facilitated the publication of 23 high-impact articles in international academic journals, with a cumulative impact factor of 142.

Furthermore, for Chinese enterprises, domestically produced equipment holds greater advantages in terms of product pricing and after-sales service quality. With products offering both Price Guarantee and Quality Guarantee, coupled with the macro trend of import substitution in the medical device sector, BGI Genomics is highly likely to gradually challenge their position in the domestic market.

The general-purpose sequencer of the BGISEQ-500 platform, along with its supporting reagents, the NIFTY® test kit, and the nucleic acid extraction kit, all obtained the CE Mark for medical devices in the European Union in 2017. This signifies that these sequencing instruments and products, intelligently manufactured in China, comply with the regulatory requirements of the European In Vitro Diagnostic Medical Devices Directive and meet the EU’s stringent safety and health standards. Furthermore, this indicates that BGI’s sequencers are positioned not merely as domestic alternatives but are poised to expand into international markets.

In the future, as these domestically produced products mature, the industry may witness a wave of import substitution. Furthermore, due to the price advantage of domestic products, there may be an overall price reduction for market-oriented products.

Meanwhile, the rising proportion of domestic in-house procurement and advancements in technological capabilities are making industrial specialization increasingly pronounced. In the future, companies may no longer seek to control every link of the value chain; instead, they will leverage their own strengths while integrating the expertise of others to jointly build an ecosystem.

Overview of Major Domestic Sequencers

3.1 Industry Commercialization Assessment Framework

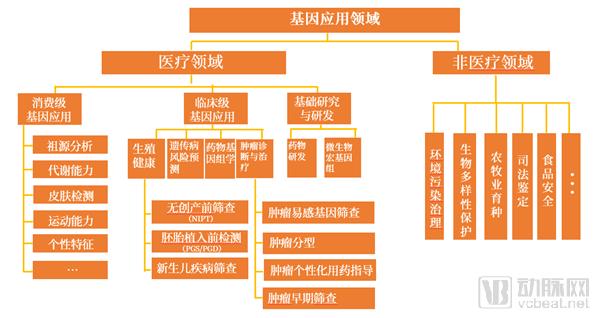

Based on current research directions in gene sequencing, its applications can be categorized into medical and non-medical fields. The medical field primarily encompasses consumer-grade genetic applications, clinical-grade genetic applications, and basic research and development. Non-medical applications will not be elaborated upon here.

We can observe that significant technological barriers may exist between these genetic applications. For instance, there is a substantial divide between reproductive health and microbial metagenomics in terms of both technology and application scenarios, whereas reproductive health shares an inherent affinity with genetic disease risk prediction. Given these complex relationships and the varying stages of technological development across different genetic fields, what conceptual framework should we adopt to evaluate their commercialization potential?

We can break down the proposition of commercializing genes into the following three questions:

What problems does genetic sequencing actually aim to solve? How is value demonstrated at each stage of the process? Who pays for this service?

Determining what problems gene sequencing aims to solve is a prerequisite for evaluating genetic applications, as it indicates whether the application is necessary and assesses the size of the market space. How value is demonstrated at each stage reflects the implementation progress of genetic applications, addressing the question of how to execute them. Therefore, we break this issue down into three indicators: market entry barriers, difficulty in data acquisition, and challenges in replication and deployment. Once gene technology is implemented to address a specific problem, it is essential to identify channels for value monetization.

Based on the aforementioned metrics, we can evaluate genetic applications to identify the sectors with the most promising growth prospects.

3.2 Clinical-Grade Gene Applications: Technology Reigns Supreme, Diverse Innovations Flourish

3.2.1 NIPT: A Lucky Ticket, Achieving Commercial Maturity in 10 Years

Since its inception in 2008, NIPT technology has been around for a decade. Over these ten years, the technology has progressed from emergence to clinical implementation, transitioning from a blue ocean to a red ocean market, and evolving from disorder to standardization.

In 2016, the removal of pilot restrictions on NIPT marked its formal integration into mainstream clinical in vitro diagnostics.

In 1997, Professor Dennis Lo of The Chinese University of Hong Kong accidentally discovered the presence of cell-free fetal DNA in maternal peripheral blood. Subsequently, many scientists and biologists in the field sought to develop diagnostic products for fetal diseases based on this discovery.

In 2010, NGS-based non-invasive prenatal screening technology began to enter clinical practice.

Prior to the advent of next-generation sequencing (NGS), clinical screening for Down syndrome primarily relied on two methods: serological screening and amniocentesis. Amniocentesis is considered the gold standard for diagnosis; however, it is invasive and carries a risk of miscarriage. Although serological screening is non-invasive, its detection rate and false-positive rate are less than satisfactory. The emergence of non-invasive prenatal testing (NIPT) has addressed one of the most urgent needs in clinical prenatal screening.

This technology quickly demonstrated its clinical application potential and began to expand rapidly in clinical settings. During this process, an increasing number of companies entered the industry. Each company operated independently, with no unified standards for operational procedures and testing methods.

In February 2014, the National Health and Family Planning Commission (NHFPC) and the China Food and Drug Administration (CFDA) jointly issued a directive to halt unauthorized practices, marking the beginning of standardized clinical application of high-throughput sequencing. Services were suspended, registration applications required, and new clinical trials mandated; companies were required to re-establish their quality systems in accordance with CFDA standards. BGI Genomics’ NIFTY non-invasive prenatal testing (NIPT) became the first product to receive CFDA certification.

In 2015, the National Health and Family Planning Commission issued a notice on pilot programs for the clinical application of high-throughput sequencing. Eight medical testing laboratories, including BGI Genomics, and 108 prenatal diagnostic institutions were granted pilot qualifications. The pilot program was officially terminated in 2016. After one year of small-scale validation by regulatory authorities, non-invasive prenatal genetic testing began to be conditionally permitted nationwide.

Technologically, NIPT is disruptive, meeting the dual demands of clinical practice. During the one-year pilot period for its removal from restricted lists, local governments and companies provided varying levels of subsidies and price concessions for testing. The improvement of regulatory frameworks and the reduction in costs have enabled the technology to reach primary care hospitals, allowing individuals with relatively lower incomes to benefit as well.

Taking Chongqing Municipality as an example, although NIPT has not yet been included in the medical insurance scheme, free screening has been implemented in two districts and counties—Yubei District and Zhong County—based on the cooperation between BGI Genomics and the local government, while a subsidy of RMB 600 is provided in other districts and counties. In Shenzhen, Guangdong Province, NIPT was included in the medical insurance scheme as early as January 2016, with the test price set at only RMB 855. This year, Shenzhen has further achieved free testing for all pregnant women in the city through fiscal support and coverage by maternity insurance.

3.2.2 Tumor Detection and Treatment: Vast Market Potential Driven by Policy Support

Larger market potential compared to NIPT

During our discussion on the commercialization of genetic applications, we identified non-invasive prenatal testing (NIPT) and oncology (including early cancer screening and clinical cancer diagnostics) as particularly promising sectors. NIPT has a shorter implementation cycle and lower technical barriers, allowing this field to mature prior to clinical cancer diagnostics. However, compared with NIPT, tumor liquid biopsy targets a broader patient population and addresses more urgent clinical needs.

Among alternative products, clinical technologies similar to NIPT include traditional Down syndrome screening and amniocentesis. Traditional Down syndrome screening has lower accuracy, while amniocentesis carries higher risks; in comparison, NIPT technology offers superior advantages.

However, NIPT is only targeted at individuals who are preparing for pregnancy or are already pregnant, resulting in a relatively small audience and low usage frequency; thus, the overall market size is not particularly large. Furthermore, since NIPT testing does not involve subsequent therapeutic interventions, it is difficult to establish a closed-loop industry ecosystem.

In contrast, other clinical methods for tumor detection include radiology, biochemical testing, pathology, histology, and mass spectrometry. However, apart from tissue biopsy, no technology is capable of performing molecular- or genetic-level detection or analysis of tumors. Yet, tissue biopsy is highly invasive, making it an impractical approach for monitoring drug response and tumor recurrence during or after treatment.

Furthermore, since cancer is a complex disease, clinical diagnosis and treatment often require the combined assistance of multi-omics approaches, including radiology, pathology, and histology. In other words, tumor genetic testing and other diagnostic methods are not in a purely competitive relationship, which is fundamentally different from the relationship between NIPT and traditional Down syndrome screening.

More importantly, tumor liquid biopsy involves subsequent treatment and testing after detection, with downstream applications, resulting in a significantly higher usage frequency and larger target population compared to NIPT.

For technology-driven enterprises, both product commercialization and scaling require substantial capital. The 2015 lung cancer diagnosis guidelines have already included liquid biopsy as an indicator, meaning it is a product recognized and accepted by the clinical community. A casual visit to the websites of liquid biopsy companies reveals that nearly all of them promote and introduce clinically graded products (with the exception of early screening tests).

The above is an excerpt from this report. The remaining content includes:

3.2.2 Tumor Detection and Treatment: Vast Market Potential, Continued Policy Deregulation

3.2.3 Microbial Sequencing: Basic Research and Regulatory Frameworks Are Still Being Refined, but the Greatest Challenge Is Time

3.3 Consumer-Grade Genetic Applications: Navigating Growing Pains Through Brand-Centric Operations

IV. Value Outlook

4.1 The Gene Industry Enters a Phase of Endogenous Growth, Attracting Industrial Capital and Initiating Scenario-Based Value Exploration

4.2 What Is the Scope of Cross-Industry Collaboration in Gene Technology?

Please refer to the full report.

Scan the QR code below now to becomeVCBeat Official Member, you can obtainFull Version of the "Report on Realizing the Commercial Value of Gene Technology". Gain deeper insights into the current state and development trends of the genomics industry. Furthermore, in the coming year, you will have unlimited access to the completeIndustry Trend Report, timely access to the latest global investment and financing information, with a comprehensiveMedical Enterprise Database,AlsoMassive Resource Matchmaking。