Hospital Acquisitions Surge as Industrial Capital from Manufacturing, Real Estate, and Insurance Sectors Enters Healthcare; Value-Based Care Emerges as Next Strategic Focus

Recently, listed companies such as Guangzheng Group, Kangzhi Pharmaceutical, Tonghua Jinma, and Hengkang Medical have successively announced their plans to acquire hospital assets.

Behind Listed Companies’ Successive Pursuit of Hospital M&A: Undiminished Enthusiasm of Capital for Healthcare ServicesDriven by policy incentives, favorable developments in the broader health industry, reform mandates for public hospitals under China’s healthcare reform, and the requirement to establish a “multi-tiered and diversified” healthcare service system, the large-scale entry of social capital into the healthcare services sector has become a prominent trend in recent years.

VCBeat (WeChat ID: vcbeat) aims to categorize the types of capital involved in healthcare services, examining their areas of entry, modes of participation, and latest trends. By integrating factors such as policy, industry dynamics, and corporate motivations, it provides a comprehensive analysis of the phenomenon of capital participation in healthcare services.

Overview of Capital Participation in Healthcare Services: Three Types of Targets and Four Categories of Participants

There are roughly four types of participants in private healthcare provision:

Large Healthcare Group

Major healthcare groups, including Peking University Healthcare, CITIC Healthcare, China Resources Healthcare, and Fosun Healthcare, have adopted a “capital + management” approach. They participate in the restructuring of public hospitals while also establishing, investing in, and collaborating with private hospitals. These large-scale healthcare groups now control dozens of hospitals and possess mature expertise in hospital asset management and operations.

Specialty Medical Group

Specialized hospital groups include Aier Eye Hospital, Arrail Dental, Topchoice Medical, and Bybo Oral Care, with treatment areas concentrated in “eyes, ears, mouth, and nose.” Their operational model features nationwide chains and branded operations, with franchising being a key characteristic. Additionally, there are private medical aesthetics and plastic surgery hospitals. Since public hospitals are less adept at these services, private players have seized the opportunity for growth. However, strictly speaking, the medical services they provide are limited, and they should be classified under the consumer services industry.

International Participants

With the rapid rise of China’s economy and increased market openness, many international players have begun to “seek gold” in China. Notable examples include Mayo Clinic, Hospital Corporation of America (HCA), and International Healthcare Group (IHG) from the UK, most of which have entered the Chinese market through investment and collaboration. For instance, Mayo Clinic invested in Huimei Medical, aiming to introduce Mayo’s management expertise to China and build a healthcare management platform. IHG entered the Chinese market in 2015 and established its Chinese brand, “Yingci Medical.”

Industrial Capital

In addition to the more “traditional” players mentioned above, a diverse range of participants have entered the healthcare services sector in recent years, which we categorize as “industrial capital.” Industrial capital can be broadly divided into five categories: pharmaceutical and medical device companies, insurance capital, real estate developers, companies undergoing cross-industry transformation, and investment firms.

Pharmaceutical and Medical Device CompaniesRepresented by Kangmei Pharmaceutical, Lepu Medical, and Allsheng Medical, their logic for entering the healthcare services sector is to extend along the pharmaceutical industry chain, moving from pharmaceutical/medical device businesses into healthcare services. Leveraging their existing abundant medical resources and accumulated capital, they have achieved considerable phased progress in this expansion.

Insurance CompanyBy investing in, acquiring, or establishing healthcare service providers, these companies aim to accumulate experience in exploring managed care health insurance. Representative players include Taikang, Sunshine Insurance Group, and Ping An. For instance, in June 2017, Taikang Xianlin Gulou Hospital, a Grade A tertiary hospital under Taikang Insurance Group, completed its renaming process. Sunshine Fusion Hospital, a large-scale Grade A tertiary hospital jointly built by Sunshine Insurance Group and the Weifang Municipal Government, has been in operation for over a year. Meanwhile, Ping An has launched the Wanjia Cloud Clinic platform to provide information technology services to clinics.

Real Estate DeveloperThey are also actively expanding into healthcare services. Real estate developers such as Wanda, Evergrande, Sino-Ocean, and Yihua have accumulated years of experience in operating senior living properties and have subsequently begun to lay out projects including general hospitals and specialized hospitals. In addition, collaborations between real estate developers and chain clinics or health management companies to establish community clinics and health management centers within residential communities have become a current hotspot.

Optimistic about the development trends in the broader health industry, many companies whose core businesses were not originally in this sector have begun to make cross-industry moves. Examples include Changbao Shares, Jinzi Ham, and Guangzheng Group. Taking Changbao Shares as an example, the company is primarily engaged in the research and development, production, and sales of specialized steel pipes such as those for natural gas, boilers, and machinery, making it a quintessential manufacturing enterprise. In 2017, it made a one-time investment of nearly RMB 1 billion to acquire three hospitals.

According to incomplete statistics from VCBeat, in 2017, data up to the end of October alone showed that 27 listed companies announced their participation in nearly 50 hospital projects. These projects covered general hospitals, specialized hospitals, rehabilitation centers, and the renovation of public hospitals, with primary modes of participation including acquisitions, investments, and new constructions.

With the implementation of policies such as tiered diagnosis and treatment, clinics have become attractive investment targets. A wide variety of new general practice and pediatric clinics have emerged across the country, driving the upgrading of clinic models through chain-based and branded operations. Behind this trend stand institutional investors: for instance, Legend Capital, Dehui Capital, and Qiming Venture Partners invested in Johnson Medical; Sequoia China invested in Zhibei Pediatrics; and Matrix Partners China, CICC, and Tiantu Capital invested in Distinct HealthCare.

Participation of Various Capital Sources in Healthcare Services

In terms of importance, general hospitals, specialized hospitals, and clinics are the three most prevalent types of medical institutions and constitute a vital component of the healthcare system, fulfilling nearly all of the population’s healthcare service needs.

“New Healthcare Reform” has seen rapid growth in the number of these three types of medical service institutions. According to the National Health and Family Planning Commission’s Statistical Yearbook, since 2009, the number of general hospitals in China has increased by approximately 5,000, reaching 18,000 by the end of 2016; specialized hospitals have increased by about 3,000, reaching 6,642; and outpatient clinics have increased by roughly 36,000, reaching 216,000.

Changes in the Number of General Hospitals, Specialized Hospitals, and Clinics

Data source: National Health and Family Planning Commission Statistical Yearbook, compiled by VCBeat

The growth in the number of three major types of medical institutions is driven by multiple factors, including policy, capital, and market dynamics. Among these, the influx of social capital into the healthcare services sector is the most core driving force, specifically manifested in the increase in the number of privately-run or non-public medical institutions.

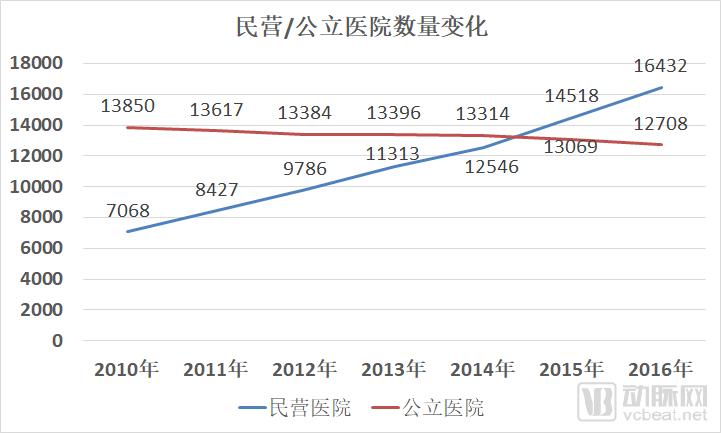

According to the National Health and Family Planning Commission’s Statistical Yearbook, since the launch of the “New Healthcare Reform,” the number of private hospitals has increased by approximately 1,500 per year, while the number of public hospitals has shown a downward trend. In 2015, the number of private hospitals surpassed that of public hospitals for the first time, reaching 16,400 by the end of 2016—nearly 4,000 more than public hospitals.

As the number of private hospitals has surged, their patient volume has also climbed year by year. Taking the number of inpatients as an example, private hospitals accounted for only 4% of total inpatient admissions in 2005, a figure that rose to 16% by 2016—an increase of approximately 12 percentage points—indicating growing public acceptance of private healthcare institutions.

Changes in the Number of Private and Public Hospitals

Data Source: National Health and Family Planning Commission Statistical Yearbook; compiled by VCBeat

Policies on Private Healthcare Provision Are Being Refined Year by Year, Creating a Favorable Environment for Capital Entry

“The New Healthcare Reform” proposed the goal of establishing a “multi-tiered and diversified” medical service system to comprehensively meet the public’s demand for medical services. Under this top-level design, policies governing privately run medical institutions have been progressively refined on an annual basis, enhancing their operability and creating favorable conditions for capital entry.

Key Policies on Socially-Run Healthcare in Recent Years

As can be seen, privately run healthcare is one of the key tasks in this round of healthcare and pharmaceutical system reform, involving many important aspects such as relaxing market access for social capital, allowing social capital to participate in the reform of public hospitals, planning for clinic establishment, and coordinating medical services with health insurance.

In May 2017, the State Council issued the “Opinions on Supporting Social Forces in Providing Multi-level and Diversified Medical Services” (hereinafter referred to as the “Opinions”), which serves as a phased summary of policies for privately-run healthcare institutions. Playing a guiding role, the document features detailed planning and strong operability.

In the “Opinions,” general practice medical services, physician groups, and healthcare groups were for the first time designated as areas encouraged for development. The “Opinions” set forth the objective that by 2020, a large number of privately run medical institutions with strong service competitiveness would be established, gradually forming a new pattern of multi-level and diversified medical services.

To achieve this goal, the “Opinions” also provide specific implementation plans. For instance, to address the shortage of talent in privately run medical institutions, it is proposed that physicians be allowed to practice at multiple facilities, thereby promoting orderly physician mobility and multi-site practice, while encouraging physicians to establish clinics at the grassroots level. In response to the disadvantaged position of privately run medical institutions in areas such as approval processes, subsidies, equipment procurement, and health insurance support, measures are proposed including simplifying approval procedures, expanding flexibility in planning quotas for the allocation of large-scale medical equipment, and strengthening fiscal, tax, and investment/financing support.

It is also important to note the improvement of supporting policies for private medical institutions. For instance, restrictions have been relaxed regarding the types of third-party medical service providers, investment entities, and administrative approvals. Additionally, basic standards and management regulations have been established for three categories of medical service institutions: hospice care, rehabilitation medicine, and nursing centers.

At this year’s “Two Sessions,” the Government Work Report pointed out that the next steps should support social forces in increasing the supply of medical services and expand foreign investment access in healthcare and other sectors, thereby reaffirming the direction for the gradual deepening of private capital’s participation in healthcare services.

An overview of the evolution of policies on privately-run healthcare in recent years reveals that healthcare reform is progressively entering a phase of deeper, more complex challenges. As healthcare reform advances into this critical stage, privately-run medical institutions are expected to play a more significant role, and support for their development has become more substantial and targeted. The “reform” process is incremental; the continuously refined policies have created a favorable environment for private capital to enter the healthcare services sector, thereby fostering the prosperity of privately-run healthcare.

Medical Asset Operational Capabilities and Value-Based Healthcare to Become Key Focus in the Next Phase

Under rational top-level design and planning, policies encouraging privately run medical institutions have been progressively implemented and refined. This has fully mobilized the enthusiasm for private participation in healthcare, leading to a sustained and rapid increase in the number of private medical institutions, along with continuous improvements in their comprehensive service capabilities. From the perspective of public acceptance, the rise in patient visits demonstrates that privately run medical institutions have played an irreplaceable role in meeting residents’ healthcare needs.

With the synergistic effects of comprehensive reforms in public hospitals, multi-site practice for physicians, the liberalization of third-party medical services, and coordinated advancement of health insurance, private capital investment in healthcare has entered a fast lane. In terms of competitive market dynamics, a number of large-scale medical groups, specialized hospital chains, and clinic networks with strong brands and capabilities have begun to take shape, mastering core industry elements and establishing a certain market position.

We judge that,Capital’s large-scale entry into the healthcare services sector has entered a new phase. If the previous phase was one of “testing the waters,” with competitive factors primarily reflected in capital scale and industry resources, then the next phase represents an “upgrade” stage for social capital’s involvement in healthcare services. The key competitive focuses should be on the comprehensive operational capabilities of medical assets and the establishment of a “value-based healthcare” service system that delivers optimal cost-effectiveness.

Medical asset operational capabilities are reflected in multiple aspects, including participation in the restructuring of public hospitals, investment in newly built hospitals, and the merger, acquisition, and integration of medical resources.

The “12th Five-Year Plan” for Healthcare System Reform, released in 2012, mentioned that it is possible toGuide social capital to participate in the restructuring and reorganization of certain public hospitals, including those operated by state-owned enterprises, through various means.This policy ushered in a wave of acquisitions of public hospitals by social capital and their participation in the restructuring of public hospitals.

According to incomplete statistics from VCBeat, approximately 30 public hospitals were acquired by listed companies in 2017. For instance, on January 26, 2017, Changbao Shares announced its plan to acquire 100% equity of Shifang Second Hospital, 90% equity of Yanghe People’s Hospital, and 100% equity of Ruigao Investment (which holds a 71.23% stake in Shanxian Dongda Hospital), with the total consideration for these three transactions amounting to nearly RMB 1 billion. Prior to this, companies such as Yibai Pharmaceutical, Hengkang Medical, and Phoenix Healthcare had also carried out acquisitions of public hospitals in various regions.

Relevant companies acquire public hospitals and implement structural reforms primarily for two reasons. First, the target public hospitals have an established operational foundation, with a certain degree of assurance in both patient reputation and operating revenue; thus, acquisition entails lower risk and a more controllable investment cycle compared to building new hospitals from scratch. Second, injecting the acquirer’s management and operational expertise may enhance the hospital’s operational performance, thereby serving the acquirer’s strategic planning and strengthening its healthcare industry chain.

As healthcare reforms deepen and competition in medical services intensifies, some owners of small public hospitals or hospitals run by state-owned enterprises—driven by fiscal and operational pressures—are showing a willingness to “let go.” Consequently, the acquisition and restructuring of public hospitals are poised to become key features of social capital’s entry into the healthcare sector in the next phase.

In addition to acquiring public hospitals, mergers and acquisitions of private hospital companies can also be pursued for integration, which further tests the resource integration capabilities of the relevant entities. If establishing self-built hospitals is considered, efforts must be made in areas such as strategic planning and positioning, management team development, talent recruitment, and compensation structure design.

Once the hospital is established, the focus must shift to cultivating the patient side. A “value-based healthcare” service system centered on patients may become the primary means of serving them. “Value-based healthcare” refers to providing patients with the most cost-effective services at a reasonable cost, emphasizing the comprehensive performance of price, service, and outcomes.

With China’s economic development and rising household incomes, “consumption upgrading” has become a significant trend. Value-based healthcare can be understood as the manifestation of this consumption upgrading in the medical sector. This process, accompanied by the gradual expansion of commercial health insurance, growing emphasis on health management, and the development of “Internet + Healthcare,” will drive innovation across the healthcare industry.

Overall, the entry of social capital into the healthcare services sector has made significant progress, accumulating experience in hospital operations and the integration of medical resources. A cohort of highly experienced leaders with strong brand awareness has also emerged. As the healthcare market becomes increasingly open and international players enter, they will bring more mature models and market expertise for capital participation in healthcare service operations, ushering in a new era for the healthcare services industry.