Liu Hao of Hyfinity Capital: Policy Support Fuels Innovation and Nurtures More Healthcare Unicorns

Liu Hao, Founder and CEO of Haoyue Capital

What New Challenges and Opportunities Does China’s Healthcare Capital Market Face with the Introduction of New Healthcare Reform Policies? At the 2018 VCBeat Healthcare Investment Excellence Awards Summit, Liu Hao shared his insights: “Since 2017, the policy environment has undergone significant changes. Unicorns in the healthcare sector will emerge within the next decade, with pharmaceutical companies being the most likely to leverage the new policies to achieve rapid overtaking.”

Liu Hao has nearly two decades of experience in hospital management, investment management, and investment banking within China’s healthcare industry. In 2013, he founded Haoyue Capital, which is dedicated to providing comprehensive capital solutions—including private equity financing, mergers and acquisitions, and restructuring—to top-tier entrepreneurs in China’s healthcare sector, helping them expand their businesses and maximize value in the capital markets.

As of early 2018, Joy Capital had successfully completed over 50 private equity financing and M&A transactions, with a total transaction value exceeding US$1.2 billion.

Below is the transcript of the speech.:

Over the past year, there has been a widespread perception of a significant surge in new policy issuances. Our statistics indicate a total of 67 macro-level policies, with the biopharmaceutical sector being the most frequently addressed, followed by pharmaceuticals, medical devices, regulatory approval, and cost containment.

Among the new pharmaceutical policies introduced last year, the most significant one, in my view, was undoubtedly China’s accession to the International Council for Harmonisation of Technical Requirements for Pharmaceuticals for Human Use (ICH). China’s entry into ICH signifies its embrace of global standards and alignment with international regulatory approval processes and policies for innovative drugs, akin to China’s accession to the World Trade Organization (WTO) many years ago. While encouraging innovation, this move has further impacted traditional large pharmaceutical companies already constrained by regulations on adjuvant medications and the “Two-Invoice System.”

Historically, large pharmaceutical companies have invested very little in R&D. Moreover, 80% of these major pharma firms are grappling with succession issues. In the absence of innovation and drivers for future growth, a rather intriguing phenomenon has emerged: traditional big pharma companies are currently the most aggressive players in the biotech investment landscape.

How Can Traditional Pharmaceutical Companies Find Opportunities Amid Challenges? A Case Study of Fosun PharmaFosun Pharma, a publicly listed pharmaceutical company with nearly two decades of history, initially focused solely on traditional Chinese medicine and generic drugs. Its turnaround strategy relied on organic growth, external expansion, and integration. Today, Fosun Pharma not only owns Henlius, an innovative biopharmaceutical unicorn, but also Ambrx, a company specializing in antibody-drug conjugate (ADC) drug development. In the generics sector, Fosun Pharma successfully acquired Gland Pharma, India’s largest generic drug manufacturer, last year, as well as Handa Pharmaceutical, a U.S.-based biosimilar company under its investment holding structure. Regarding leadership succession, recent news announced that Mr. Guo Guangchang has resigned from his position as Non-Executive Director of Fosun Pharma, signaling the company’s full transition to professional management. Within two years, Fosun Pharma’s market capitalization grew from RMB 30 billion to over RMB 100 billion, making it the fifth company on China’s A-share market to surpass the RMB 100 billion mark.

Over the past few years, China’s pharmaceutical and healthcare sector has seen the emergence of publicly listed companies with market capitalizations reaching hundreds of billions of yuan. In light of these opportunities, how can innovative drug companies achieve rapid overtaking? We believe there are two key strategies: first, fully leverage new drug policies to accelerate the development pipeline; second, pursue international integration while securing rapid financing.

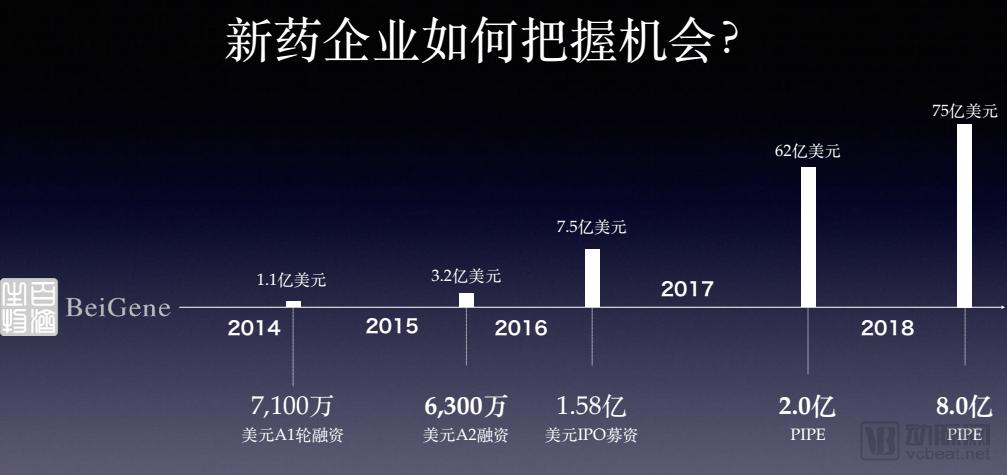

Take BeiGene, for example. The company has raised capital rapidly over the past four years, completing three additional funding rounds after its U.S. listing, and partnering with multinational pharmaceutical giants. It even executed a highly disruptive deal last year by acquiring Celgene’s entire China business. Leveraging innovation and rapid fundraising, BeiGene achieved a market capitalization of $7.5 billion within eight years of its founding, with its stock price surging tenfold in the past year alone.

In the domestic medical device sector, the primary direction of the new policies remains to encourage innovation. This is because the most prevalent issue facing Chinese medical device enterprises is a lack of innovation in the high-value consumables segment, with competition concentrated in low-end markets characterized by low-level, repetitive rivalry. A limited product portfolio results in a very low market ceiling. In reality, outstanding companies have the capability to establish a foothold in China while targeting the global market.

Last year, the applications of international heart valve giants Edwards and Medtronic to enter the Chinese market were rejected because their products could not address the contraindication for bicuspid aortic valves, a condition prevalent among Chinese patients. In addressing the challenge of bicuspid aortic valves, Venus Medtech achieved milestone progress and successfully obtained China’s first CFDA approval for its transcatheter aortic valve product, the Venus-A-Valve, in April 2017, marking a significant product innovation within China. Meanwhile, Venus Medtech’s retrievable and dry-stored pulmonary and aortic valves are undergoing global clinical trials, demonstrating its product innovation oriented toward the global market.

In the realm of medical services, private healthcare institutions, AI and big data applications, and public hospitals each face distinct challenges. Private healthcare institutions, in addition to grappling with the complexities of medical consortia, suffer from weak brand operational capabilities, persistently high customer acquisition costs, and significant difficulties in achieving scalable chain operations—issues that require internal resolution. AI and medical big data still lack practical, on-the-ground applications, making it difficult to expand profitability. Meanwhile, public hospitals have been significantly impacted by the abolition of drug markups. Furthermore, healthcare service enterprises generally lack high-quality management teams.

Under these conditions, what opportunities exist for healthcare services? The first is differentiated competition. Over the past five to ten years, many investment firms invested in a series of healthcare service providers in Beijing, Shanghai, and Guangzhou, directly competing with large state-owned hospitals, but most struggled with poor performance. In contrast, chain healthcare service providers that initially focused on second- and third-tier cities have successfully established a foothold. For example, Aier Eye Hospital started in Changsha and Wuhan and became the world’s largest ophthalmology provider last year.

For large public hospitals, the primary operational objectives are cost control and efficiency improvement. As the era of significant hospital expansion has passed, third-party outsourcing of medical services will present substantial opportunities for investors over the next five, ten, or even twenty years.

In the field of healthcare investment, numerous challenges also emerged last year. We have briefly summarized them as follows: First, exits. The first three quarters of last year saw a surge in exit activities, but tightening policies have since imposed significant pressure. Second, deleveraging. Fundraising for RMB-denominated funds has become extremely difficult, and USD-denominated funds may once again take center stage this year. Third, post-investment management. This is an issue that many new funds may not yet fully recognize; however, it is worth noting that over 80% of the private equity financing deals we have handled have involved secondary share exits and restructuring.

In response, healthcare investment funds are beginning to pursue differentiated competition by selecting a specific niche sector and expanding their layout across the upstream and downstream value chains, thereby generating strong synergies. A recent notable phenomenon is the shift from “Find” to “Found.” In certain investment areas with substantial return potential, where suitable investment targets are scarce, funds are establishing their own teams and founding companies. This represents a highly intriguing trend.

In the private equity sector, last year’s hotspots were primarily concentrated in artificial intelligence, gene sequencing, oncology drugs, and large-scale medical equipment. Looking ahead, we believe the following areas will emerge as key trends: first, biopharmaceuticals; second, leveraging the momentum in biopharmaceuticals, CROs and CMOs will also present opportunities. Finally, community-based pharmacy chains and third-party outsourcing services are also likely to become popular investment themes.

In the field of mergers and acquisitions (M&A), we have previously observed a significant volume of M&A activity in the distribution channel sector, with many funds even establishing new companies specifically to carry out acquisitions. In the coming years, we predict that the following areas will become hotspots for M&A: First, gene sequencing. Over the past five years, venture capital (VC) and private equity (PE) firms have invested in hundreds of gene sequencing companies; however, successful exits remain rare (with BGI and Berry Genomics being notable exceptions). A wave of industry consolidation is therefore inevitable. Second, hospitals, as investment returns in the healthcare services sector have fallen far short of institutional expectations in recent years. Third, Chinese enterprises will accelerate overseas M&A activities targeted at acquiring high-tech patents.

In the domestic IPO market, the most prominent highlights were the listings of BGI Genomics on the A-share market and WuXi Biologics on the Hong Kong Stock Exchange (HKEX). The biopharmaceutical sector scheduled to launch on the HKEX in 2018 is highly anticipated, with innovative pharmaceutical companies such as Henlius Biotech and Innovent Biologics set to go public sequentially. Additionally, the listings of the two giants in internet healthcare—Ping An Good Doctor and WeDoctor—are also drawing significant attention. On the A-share front, under the “Unicorn New Policy” designed to meet challenges from U.S. and Hong Kong stock markets, the return of WuXi AppTec and Mindray Medical, as leading representatives of the biopharmaceutical and medical device sectors respectively, from U.S. exchanges will undoubtedly be a major market event.

Finally, over the next decade, China will see a growing number of healthcare unicorn companies emerge and expand globally. After all, despite numerous challenges, many companies have carved out unique paths, seized opportunities, and achieved success. Thank you all.