Q1 2018 Healthcare Investment Report: 249 Deals, $6.5B Raised, Biotech Leads Funding

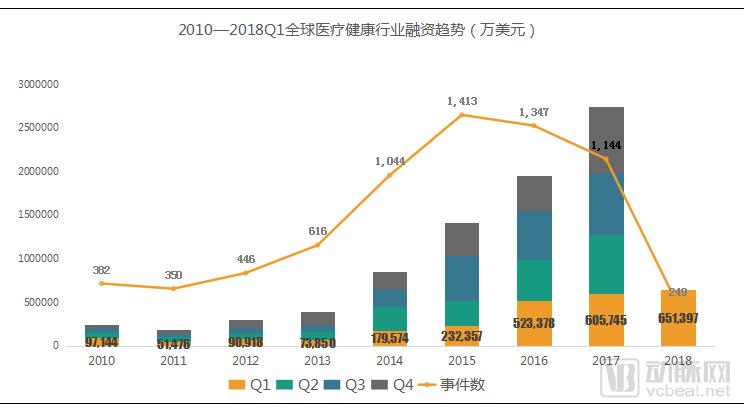

According to VCBeat’s database, there were 249 financing deals in the global healthcare industry in Q1 2018, a year-on-year decrease of 13.5%, while the total financing amount exceeded US$6.5 billion, representing a year-on-year increase of 7.5%. Among all sectors, biotechnology attracted the most investment, ranking first in both the number of deals and total funding, with 52 deals and over US$2.5 billion raised.

Key Views of the Report

Financing in the healthcare sector rose, but at a slower pace;

Biotechnology attracted the most investment, while financing in healthcare support and medical tools remained lukewarm;

Series A, Seed and Angel rounds, and Series B rank in the top three, with financing moving toward maturity;

Domestic biotechnology secured the largest volume of major financing rounds, while primary healthcare and consumer healthcare demonstrated strong performance;

Financing is most active in China’s economically developed regions, with 30% of financing deals occurring in Beijing;

CDH Investments, Sequoia Capital, and Matrix Partners China are the most active, with biotechnology, pharmaceuticals, and digital health being the most favored sectors.

Healthcare Industry Sees Rising Financing Volume Amid Slowing Growth

In Q1 2018, there were a total of 249 financing events in the global healthcare industry, representing a year-on-year decrease of 13.5%. This decline was primarily driven by a significant reduction in financing activities within the medical devices and digital health sectors. The total financing amount exceeded $6.5 billion, marking a 7.5% year-on-year increase, albeit with a slowed growth rate.

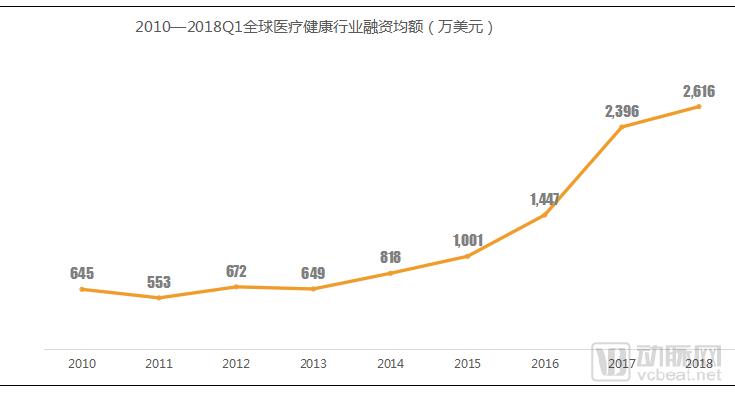

Since 2011, the average size of individual financing deals in the global healthcare industry has risen year by year, reaching a historic high of $26.16 million in Q1 2018. This trend is attributed to the gradual maturation of the industry and increased capital investment.

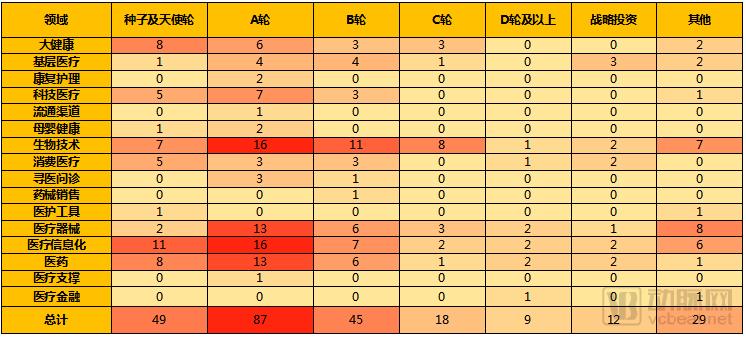

Biotechnology and pharmaceuticals attracted the most investment, while financing remained lukewarm in healthcare support and medical tools sectors.

In Q1 2018, among the various subsectors of the healthcare industry, biotechnology attracted the most capital, ranking first in both the number of financing deals and the total amount raised. Pharmaceuticals, medical devices, primary care, and healthcare informatics also demonstrated remarkable performance.

Notably, in Q1 2018 alone, there were 12 financing events for blockchain companies in the healthcare IT sector, exceeding 50% of the total number of such events in all of 2017. The financing amount for these blockchain companies surpassed $43.92 million, accounting for 10% of the total financing in the healthcare IT sector during that quarter.

Series A, Seed and Angel Rounds, and Series B Rank in the Top Three; Financing Trends Shift Toward Maturity

In Q1 2018, global healthcare financing was dominated by seed/angel rounds, Series A, and Series B rounds, with Series A deals accounting for 35% of the total number of financed projects. An analysis of historical financing rounds indicates a trend toward more mature-stage investments.

Biotechnology Sector Sees the Most Large-Scale Financing Rounds

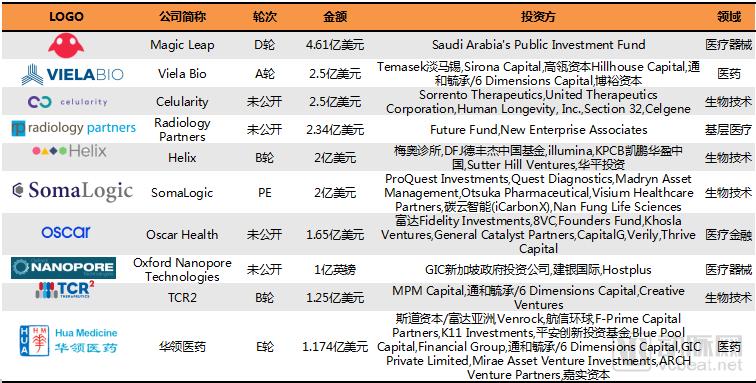

Top 10 Global Healthcare Financing Deals in Q1 2018

In Q1 2018, the financing amounts for the top 10 global healthcare and medical projects all exceeded $100 million. These top 10 funded projects were distributed across the fields of biotechnology, pharmaceuticals, medical devices, primary care, and healthcare finance. Notably, four of these projects were in the biotechnology sector.

Financing Growth Slows, While Biotechnology and Pharmaceuticals See Significant Increases

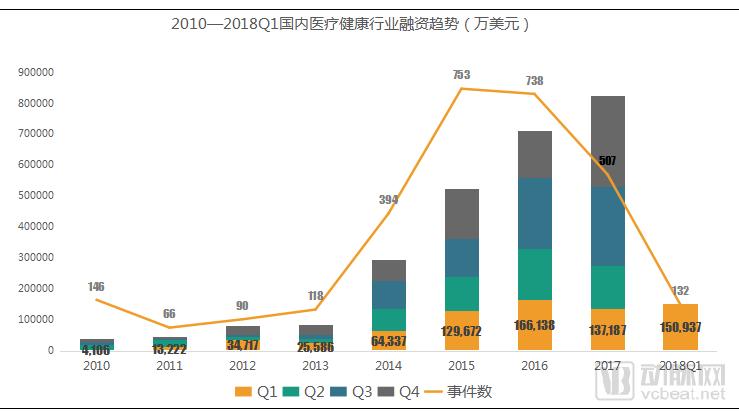

In Q1 2018, there were a total of 132 financing events in China’s healthcare and medical industry, representing an 8% year-on-year increase. The total financing amount exceeded US$1.5 billion, a 10% year-on-year increase; however, the growth in financing scale slowed down and did not reach the total financing volume recorded in Q1 2016. Nevertheless, the financing scale in the biotechnology and pharmaceutical sectors saw a significant rise.

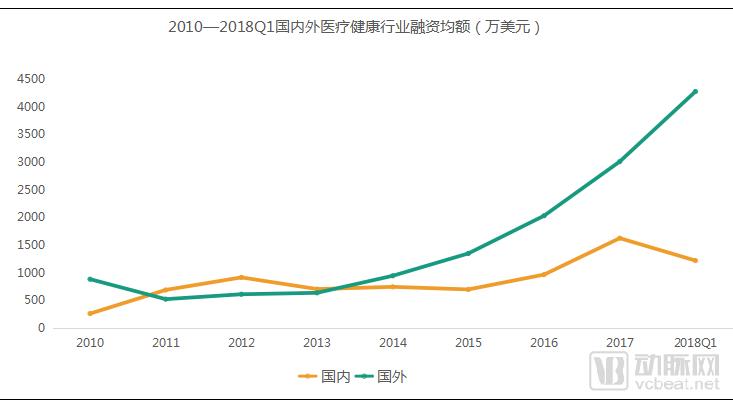

Since 2010, the average size of individual financing rounds in China’s healthcare industry has shown an upward trend, yet its growth rate has lagged behind that of foreign markets. Particularly after 2015, a significant gap has emerged between the average financing amount per deal in China and abroad. This disparity is primarily attributed to the slower growth in financing scale within China’s rehabilitation and nursing, digital health, medical devices, and healthcare informatics sectors compared to their international counterparts, as well as a substantial decline in financing volumes in the online medical consultation and maternal-and-child health segments in China.

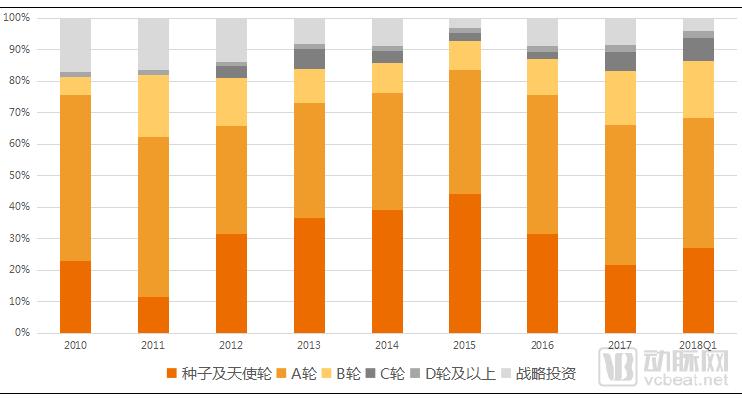

Early-stage financing declines, with funding rounds shifting toward later stages.

An analysis of financing rounds reveals that, overall, China’s healthcare industry is gradually maturing, with funding activities shifting toward later-stage rounds, while some new projects have also emerged.

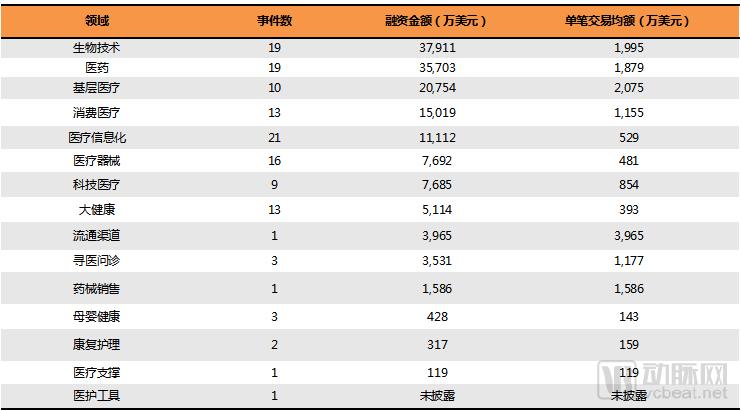

Biotechnology and pharmaceuticals attracted the most investment, while primary care and consumer healthcare showed strong performance.

In Q1 2018, the biotechnology and pharmaceutical sectors attracted the most investment within China’s healthcare industry, aligning with global healthcare financing trends.Furthermore, primary healthcare, consumer healthcare, healthcare IT, medical devices, and healthtech have demonstrated strong performance.

In Q1 2018, financing rounds in China's healthcare sector were predominantly seed and angel rounds, Series A, and Series B, which together accounted for 83% of all deals. Notably, Series A financing events comprised 39% of the total number of financing events.

In the field of healthcare informatization, there were a total of 21 financing events. The financing rounds were primarily Seed and Angel, Series A, and Series B, which together accounted for as high as 86% of the total number of financing events in this sector.

In the biotechnology sector, there were a total of 19 financing events, with seed and angel rounds, Series A, Series B, and Series C being the primary stages. These four categories accounted for as high as 84% of the total financing events in this field.

In the pharmaceutical and healthcare sector, there were a total of 19 financing events. The funding rounds were predominantly Seed/Angel, Series A, and Series B, which together accounted for as high as 89% of the total financing events in this sector.

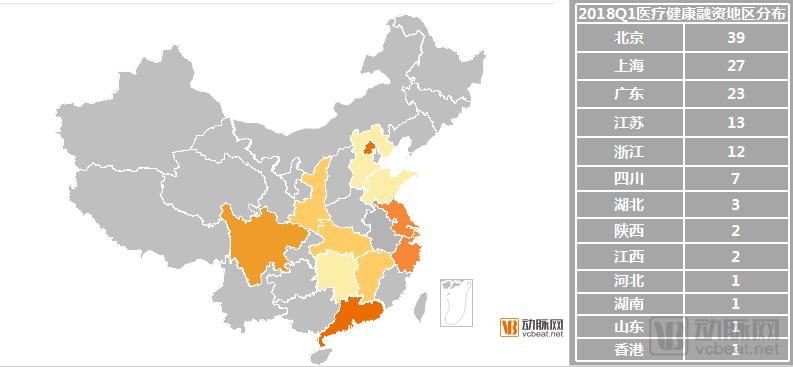

Economically Developed Regions See the Hottest Financing Activity, with 30% of Deals Occurring in Beijing

In Q1 2018, financing events in China’s healthcare and medical industry were primarily concentrated in economically developed regions, including Beijing, Shanghai, Guangdong, Jiangsu, and Zhejiang. Among these, Beijing witnessed the most vigorous financing activity, accounting for 30% of the total number of financing events in the domestic healthcare and medical sector.

CDH Investments, Sequoia Capital, and Matrix Partners China Are the Most Active; Biotechnology, Pharmaceuticals, and Digital Health Are the Most Sought-After Sectors

Most Active Investment Institutions in China's Healthcare Sector, Q1 2018

In Q1 2018, a total of 209 investment firms entered the domestic healthcare sector in China. Among them, CDH Investments, Sequoia Capital China, and Matrix Partners China were the most active. These investors focused primarily on biotechnology, pharmaceuticals, digital health, consumer healthcare, and medical devices.

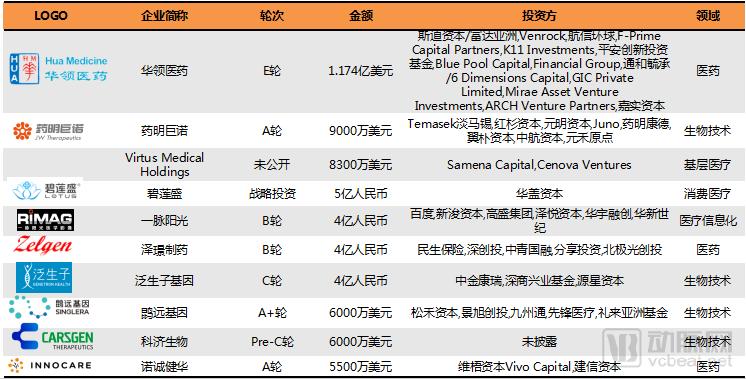

Top 10 Financing Deals in China's Healthcare Industry in Q1 2018

In Q1 2018, the financing amounts for the top 10 healthcare projects in China all exceeded $50 million. These leading deals were distributed across biotechnology, pharmaceuticals, primary care, consumer health, and healthcare informatics. Notably, the biotechnology sector remained a favorite among investors, accounting for four of the top 10 spots, aligning with global healthcare industry trends. Furthermore, Hua Medicine, which ranked first, secured a place among the top 10 largest healthcare financings globally this quarter.

Hua Medicine

Hua Medicine Technology (Shanghai) Co., Ltd. was established in June 2011. It is a clinical-stage drug development company based in China with a global outlook, dedicated to developing breakthrough first-in-class innovative drugs. The company’s current R&D portfolio includes therapeutics for type 2 diabetes and disorders of the central nervous system.On March 27, 2018, Hua Medicine announced the completion of its Series D and Series E financing rounds, raising a total of USD 117.4 million. The proceeds are expected to be fully utilized to fund the completion of two Phase III clinical trials in China for Dorzagliatin (HMS5552), the world’s first-in-class diabetes drug, as well as pre-commercialization preparations. Dorzagliatin (HMS5552) is a fourth-generation glucokinase activator with a novel mechanism of action that effectively targets functional impairment of glucokinase, the body’s blood glucose sensor, offering the potential to address the root cause of type 2 diabetes.

Juno Therapeutics

Juno Therapeutics (NASDAQ: JUNO), a global leader in oncology cell immunotherapy, and WuXi AppTec jointly established Shanghai Juno Therapeutics Biopharmaceutical Co., Ltd. in China in February 2016 as a developer of CAR-T cell immunotherapy technologies. By combining Juno’s world-leading chimeric antigen receptor (CAR-T) and T-cell receptor (TCR) technologies with WuXi AppTec’s R&D and manufacturing platform and its extensive experience in the local Chinese market, the two parties aim to build China’s leading cell therapy company and develop innovative cell immunotherapies for patients with hematologic malignancies and solid tumors.Its leading CAR-T product, JWCAR029, has successfully filed an Investigational New Drug (IND) application with the China Food and Drug Administration (CFDA) and entered the clinical trial phase.

Currently, JW Therapeutics has established a clinical GMP manufacturing facility that complies with international standards and quality systems, and has assembled a leading team with extensive experience in the biopharmaceutical industry.On March 8, 2018, JW Therapeutics announced the completion of its $90 million Series A financing round. Li Yiping, Co-founder and CEO of JW Therapeutics, stated that the company would leverage this financing to advance the clinical trials of its JWCAR029 product, expand its R&D pipeline, and establish a new industrial-scale production facility.

Virtus Medical Holdings

Virtus Medical Holdings is a private healthcare provider in Hong Kong, China.On March 2, 2018, Virtus Medical Holding announced the completion of an $83 million financing round provided by Samena Capital and Qianji Capital.

Biliansheng

Beijing Biliansheng Medical Aesthetics Outpatient Department Co., Ltd. is the leading enterprise in China’s chain medical services for hair transplantation. The company’s business spans hair care, hair maintenance, hair transplantation, and home-use products. Currently, its directly operated clinics cover more than 20 provincial capital cities across first- and second-tier regions in China, with all its hair transplantation branches under direct operation. Biliansheng boasts the most robust team of full-time licensed physicians in the industry, including professors and chief physicians who receive special government allowances from the State Council, as well as numerous senior member physicians of the World Hair Transplant Association.

On January 9, 2018, an investment consortium led by Huagai Medical Health Fund, under Huagai Capital, completed a strategic controlling investment in Biliansheng, the leading hair transplant company in China’s medical aesthetics industry. The total investment amount was RMB 500 million. This marks Huagai Capital’s largest strategic investment to date in a specialized segment of the medical aesthetics sector.

Following the introduction of Huagai Capital, Biliansheng will further strengthen its brand operations, team building, and business expansion, actively seizing market share in the hair transplantation sector and further consolidating its competitive advantages. Meanwhile, Biliansheng stated that it will take this strategic investment as an opportunity to continue promoting the transformation and upgrading of hair transplantation services, leading the standardized development of the medical aesthetics industry.

Zeng Zhiqiang, Managing Partner of Huagai Medical Fund, stated that the hair transplant industry, as an important niche segment within the medical aesthetics sector, has in the past fewThe industry has been developing rapidly. The hair transplantation business combines the essential nature of medical care with the consumption upgrade characteristics of medical aesthetics, resembling the plastic surgery industry from 5 to 10 years ago. The entire industry is currently at the tipping point of an explosion.

Yimai Yangguang

Yimai Yangguang Imaging Hospital Group, invested and established in 2014 by multiple elites from China’s medical imaging industry, specializes in the investment and operation of medical imaging centers, technical development of medical imaging cloud platforms, and training of medical imaging professionals. Its three core business segments are Independent Medical Imaging Centers, Medical Imaging Cloud Services, and the Medical Imaging Academy.

Currently, Yimai Yangguang has formedA regional medical imaging consortium model based on third-party medical imaging centers, linked by a medical imaging cloud platform, and supported by professional input from a Medical Imaging Academy.Yimai Yangguang Medical Imaging Center Network has covered Beijing, Jiangxi, Zhejiang, Shandong, Guangxi, Guangdong, Liaoning, and JiIn regions such as Jilin, Hubei, Hunan, and Inner Mongolia, more than 20 imaging centers have been established, with daily patient examinations exceeding 10,000.

On January 30, Yimai Yangguang Imaging Hospital Group announced at a press conference that it had completed a RMB 400 million Series B financing round led by investors including Baidu Capital and Goldman Sachs.

Mr. Wang Shihe, founder of Yimai Yangguang, stated that in addition to continuously expanding its network of imaging centers, the company will place greater emphasis on talent development and technological innovation in the field of medical imaging.

Baidu Capital expressed strong confidence in Yimai Yangguang’s specialized team, its broad growth prospects, and the application of artificial intelligence in the field of medical imaging. In the future, Baidu Capital will support Yimai Yangguang’s technological upgrades in artificial intelligence, big data, and cloud computing, comprehensively enhancing operational efficiency and the level of intelligent diagnosis.

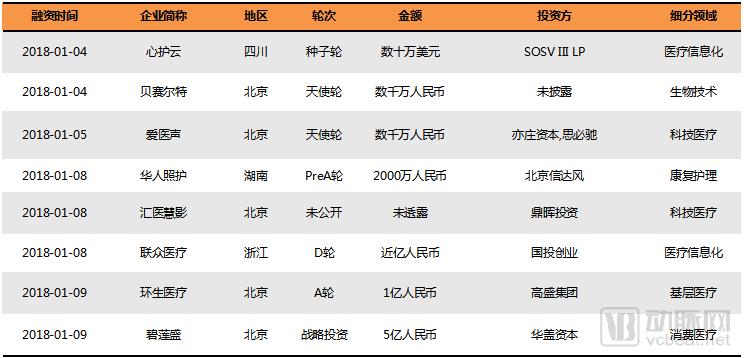

Due to the extensive length of the financing list for Q1 2018, only a partial list is displayed here. To view the complete Q1 2018 financing list, please access the VCBeat Knowledge Base mini-program to download the full “Q1 2018 Healthcare Industry Investment and Financing Report” free of charge.