Rock Health Q1 2018 Digital Health Funding Report: $1.62B Raised Across 77 Deals, 37 Companies Acquired

Rock Health’s recently released Q1 2018 Digital Health Funding Report shows that capital enthusiasm in the digital health sector remains strong this year.

Total financing in the first quarter reached $1.62 billion, with three large deals exceeding $100 million each and one major exit case. Compared to last year, controversies over healthcare policies have gradually subsided, and regulatory frameworks are becoming increasingly clear.

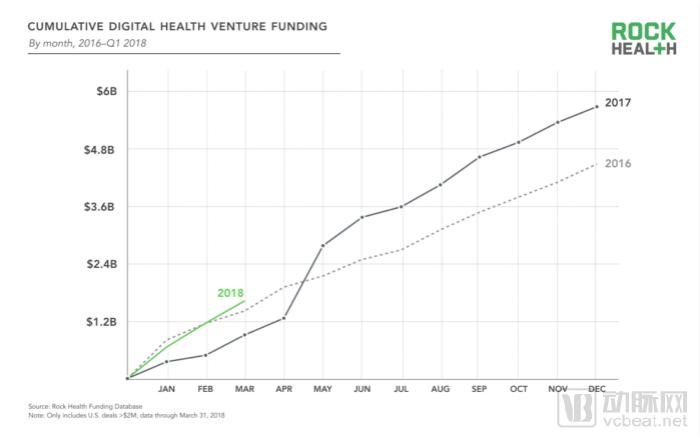

2017 was the biggest year for digital health financing, and investor appetite showed no signs of waning in 2018. In the first quarter of 2018, 77 digital health deals raised a total of $1.62 billion, surpassing the total venture capital financing of $1.44 billion in the first quarter of 2016 to become the largest quarter on record. VCBeat (WeChat ID: vcbeat) has compiled the key highlights of this report for you.

As the digital health industry gradually matures, investors’ appetite for large-scale,Late-stage investments grow more confident. Last year saw a record eight mega-deals valued at over $100 million each; following this trend, three such large transactions have already been completed from 2018 to date:

1. HeartFlow, which creates 3D coronary models to help providers non-invasively detect coronary artery disease, raised $240 million in its Series E financing round;

2. Helix, a consumer genetics company spun out of Illumina, raised $200 million;

3. Collective Health, a portfolio company of Rock Health, raised $110 million for its healthcare benefits solutions developed for employers.

The top 10 largest deals in Q1 2018 accounted for over 55% of the total financing amount for the quarter, yet represented only 13% of the deal count. The average deal size has increased annually over the years, and this quarter was no exception:Average transaction size reached as high as $21 million, compared to $1,640 last year.。

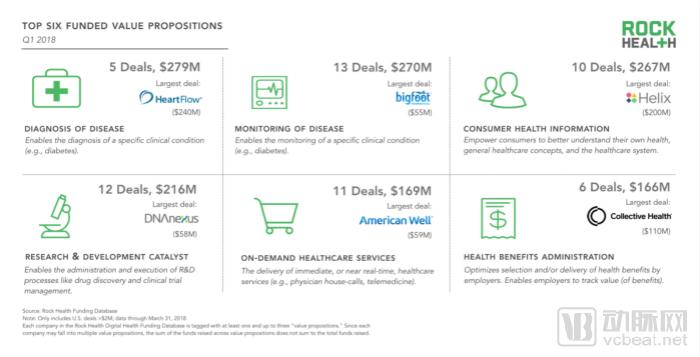

Backed by HeartFlow’s major transaction,Digital Disease Diagnosis Becomes the Largest Sector in Funding Amount for the First Time。

Disease surveillance is the second-largest area in terms of financing amount and also has the highest number of transactions (13 in total).The field of diabetes monitoring has seen a significant clustering phenomenon., Bigfoot Biomedical, Sano, Intuity Medical, Siren, and Common Sensing all secured financing in the previous quarter.

Consumer health information technology, which helps patients navigate the healthcare system and manage their own health, is gaining momentum with the boost from the Helix deal.

As we are still in the early stages of 2018, a few large deals can significantly impact the ranking and categorization of financing subsectors. Even so, we continue to see digital health startups not only inAddressing Clinical Nursing Issues (Disease Diagnosis and Disease Monitoring), while also dedicated toReduce Patient Interaction with the Healthcare System(Between healthcare benefits management and on-demand medical care services)Friction。

Top Six Sectors by Financing Amount

1. Disease Diagnosis

Content: Diagnosis of specific clinical symptoms, such as diabetes mellitus

Transaction Performance: 5 deals totaling $279 million

Largest Deal: HeartFlow, $240 Million

2. Disease Surveillance

Content: Monitoring of specific clinical symptoms, such as those associated with diabetes

Transaction Performance: 13 transactions totaling $270 million

Largest Deal: Bigfoot, $55 Million

3. Consumer Health Information

Content: Helping consumers better understand their health, general medical care concepts, and the healthcare system

Transaction Performance: 13 deals totaling $267 million

Largest Deal: Helix, $200 Million

4. Optimize the R&D Process

Content: Optimizing the R&D Process of Drug Discovery and Clinical Trial Management from Administrative and Execution Perspectives

Transaction Performance: 12 deals totaling $216 million

Largest Deal: DNAnexus, $58 Million

5. On-Demand Medical Care Services

Content: Provide immediate or near-real-time medical care services

Transaction Performance: 11 deals, totaling $169 million

Largest Deal: American Well, $59 million

6. Medical Benefits Management

Content: Optimizing Employers’ Selection and Provision of Employee Medical Benefit Programs

Transaction Performance: 6 deals totaling $166 million

Largest Deal: Collective Health, $110 Million

Helix’s $200 million mega-deal and 23andMe’s $250 million transaction in the third quarter of 2017 demonstrate growing interest in the genomics sector.

In fact, digital health companies dedicated to genomics and sequence analysis accounted for 17% of the total funding raised this quarter. Last year, genomics companies represented 11% of the total funding in the digital health sector. With the expansion of reimbursement coverage by the Centers for Medicare & Medicaid Services (CMS), the volume of consumer-generated testing data continues to grow, and the Precision Medicine Initiative has benefited from improved technical infrastructure.The field of genomics appears to be at a turning point。

In contrast to last year’s volatile policy shifts, investors and entrepreneurs may be encouraged by the regulatory progress made this year. As part of the FDA’s $400 million budget, Commissioner Scott Gottlieb has launched a new Center of Excellence on Digital Health initiative, which aims to establish a novel regulatory framework.

This regulatory model expands the existing pre-certification pilot into a program that streamlines the evaluation process for digital health technologies. Companies that have already obtained pre-certification and demonstrated their capability to manage software quality and reliability will benefit from this initiative.

We have observed increased activity among the nine companies participating in the pre-certification program. Pear Therapeutics is currently collaborating with Novartis to develop digital prescription therapeutics for the treatment of schizophrenia and multiple sclerosis, with the aim of obtaining FDA clearance. This collaboration representsPharmaceutical companies are increasingly recognizing digital therapeutics as a viable treatment modality.and valuable commercial investments.

Furthermore, Fitbit plans to seek FDA clearance for its sleep apnea and atrial fibrillation detection tools, marking the company’s more serious commitment to chronic disease use cases.

Apple Health Records has released a beta version that allows patients of certain providers, such as Johns Hopkins and Cedars-Sinai, to store and share medical records on their iPhones. As part of the University of California, San Francisco (UCSF) health research, Samsung’s newly launched smartphones will feature built-in optical sensors to measure blood pressure and stress levels.

Given that payers, providers, innovation procurers, and investors require factual evidence prior to adoption and reimbursement, we can anticipate that more companies will demonstrate the efficacy of digital interventions through controlled studies. Enterprises may also seek FDA approval to substantiate that their digital products serve as rigorous clinical tools.

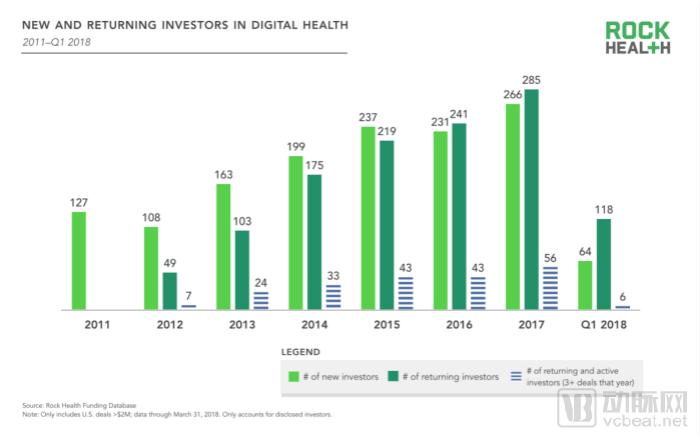

From 2018 to date,182 (public) investors have participated in 77 transactions. In 2016, more than half of digital health investors were repeat investors who had participated in at least two digital health deals since 2011.

This trend continued in 2017, with the gap between repeat investors and new investors widening further, indicating an increased proportion of follow-on investments by investors returning to this sector.

Among all digital health investors, 803 (58%) can be considered as tryouts, having made only one transaction. On the other hand, 145 (10%) have conducted six or more transactions.

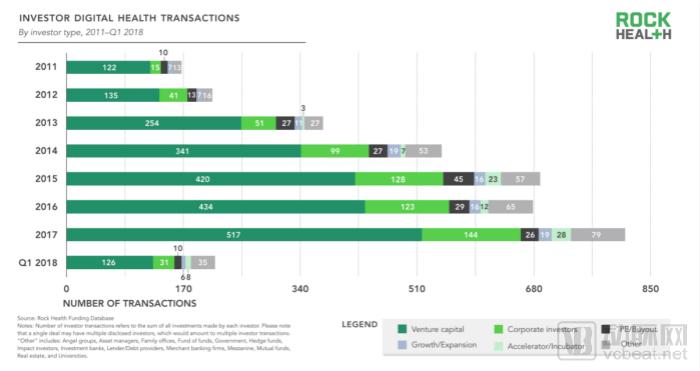

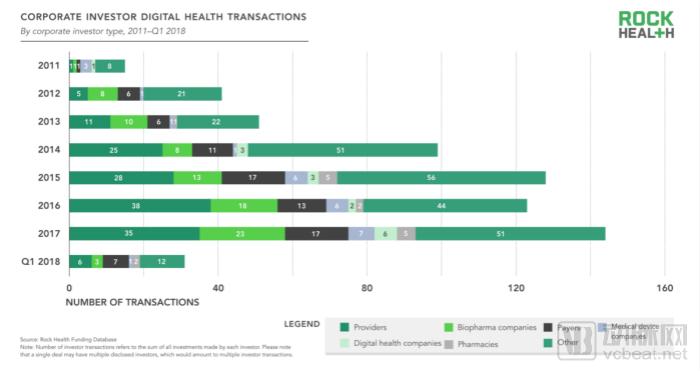

In addition to tracking investors for each transaction, we also monitor investor types in our digital health financing database. We categorize investors into traditional venture capital, corporate investors, private equity (PE), accelerators/incubators, and other investors (such as family offices and hedge funds).

As expected,Traditional venture capitalists are the most prominent investors in the digital health sector., accounting for 64% of public investment transactions. Corporations are the second most active type of investor, representing 17% of investor transactions. Private equity firms account for 5% of investor transactions.

Suppliers (hospitals, healthcare systems, and clinics) are the most active type of corporate investors, accounting for 24% of all public corporate investment transactions. Biopharmaceutical companies account for 13% of corporate investor transactions, followed by payers at 12%.

Many corporate investors are classified as “Other” because they do not fall under the traditional category of healthcare companies. These companies includeGeneral Electric, Amazon, Best Buy, Apple, Baidu, and other non-traditional companies,They have shown sustained interest in digital health startups, but typically to advance their own healthcare strategies.

As strategic investors, corporate investors behave as expected. Between 2011 and 2017, suppliers were most likely to invest in digital health companies, focusing on non-clinical and clinical workflows. Payers were most likely to invest in population health management startups and biopharmaceutical R&D optimization companies, such as those focused on drug discovery and clinical trial management.

Suppliers’ robust investment may also be driven by the effects of digitalization itself. The majority of customers for startups are suppliers: 60% of digital health startups sell their products to suppliers, while 20% sell to payers and 15% to biopharmaceutical companies. In other words, the commercial value offered by startups aligns most closely with hospitals and healthcare systems, making them most likely to attract investor interest.

With both peaks and troughs, the M&A data curve for digital health in the first quarter of 2018 resembled a roller-coaster ride. A total of 37 digital health companies were acquired this quarter, and this year’s M&A activity is poised to surpass last year’s 119 deals as well as the record of 146 deals set in 2016.

The first acquisition deal of 2018 was Allscripts’ $100 million purchase of Practice Fusion, representing only a small fraction of the latter’s $1.5 billion unicorn valuation. Allscripts had previously proposed a $250 million investment in this free, cloud-based electronic health record (EHR) company but withdrew the offer after the U.S. Department of Justice investigated and fined another company in the EHR sector $155 million.

Subsequently, the U.S. Department of Justice launched an investigation into Practice Fusion’s compliance regarding its electronic health record (EHR) system; however, Allscripts assumed full responsibility for the findings, leading Practice Fusion to accept a lower acquisition offer.

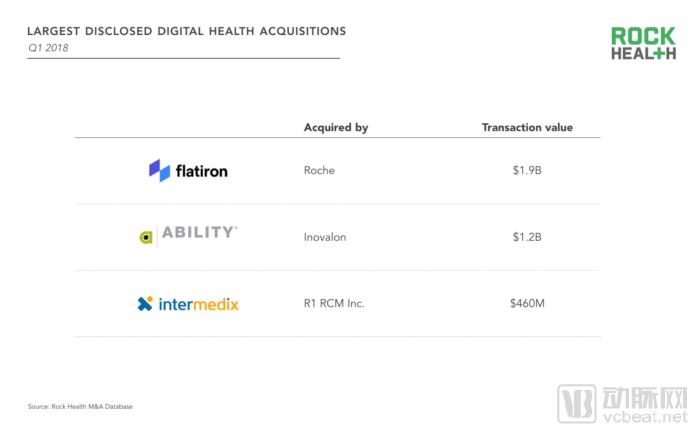

Notably, a few weeks later, Roche acquired Flatiron Health for $1.9 billion, a price nearly 1.6 times the company’s previous valuation of $1.2 billion. Founded in 2012, Flatiron was acquired within five and a half years. The company aggregated the largest real-world oncology dataset in the United States from 265 community oncology practices using its electronic health record (EHR) platform and six major academic medical centers.

The company generates high-quality data directly from electronic health records by strategically combining the expertise of clinical oncology specialists with machine learning and natural language processing, thereby enhancing data abstraction efficiency.

Furthermore, companies leveraging artificial intelligence and machine learning algorithms raised $339.3 million, accounting for nearly 20% of the total funding in the first quarter of 2018. Flatiron’sThe oncology dataset is a key driver of this acquisition.. This enables Roche to leverage specific data on drug efficacy to accelerate clinical trials and market promotion, while reducing overall R&D costs.

In addition, Ability Network, a software-as-a-service (SaaS) company that streamlines administrative tasks in the healthcare industry, was acquired by Inovalon, a healthcare data analytics firm, for $1.2 billion in cash and stock. Fitbit acquired Twine Health (undisclosed amount), whose chronic disease management platform has demonstrated significant clinical improvements in diabetes and hypertension.

Of course, gaining capital favor in the field of digital health is not the ultimate goal of this industry; the original intention of digital health is to improve healthcare systems and patients' lives. The following are the latest advances made by digital health companies on their path to obtaining technical certification:

1、Virta

Virta raised $37 million in March 2017. The company is currently conducting a clinical trial to evaluate the medical outcomes of patients with type 2 diabetes receiving Virta’s treatment (n=262) compared to those receiving standard physician-led care (n=87).

The first-year trial results of Virta were recently published in the peer-reviewed medical journal Diabetes Therapy, which included the following medical outcomes for patients in the Virta intervention group:

• Type 2 diabetes was reversed in 60% of patients;

• 94% of patients experienced a reduction or elimination of insulin use;

• 1.3% of patients experienced a reduction in mean HbA1c within one year;

• Average weight loss of 30 pounds within one year.

2、Ambient Clinical Analytics

Ambient Clinical Analytics and Response Evaluation (AWARE) – Ambient’s clinical decision support tool designed to improve patient outcomes and reduce intensive care unit stays and overall hospital length of stay.

In the four intensive care units at Mayo Clinic, the implementation of the AWARE intervention led to a 7% reduction in overall hospital and ICU mortality. AWARE also reduced ICU length of stay by 50% and total hospitalization costs by 30%. Last year, Ambient secured $5.4 million in Series A funding, led by Waterline Ventures and Bluestem Capital.

3、Evidation Health

Evidation collaborated with a researcher from Stanford Medicine to develop an analytical framework for quantifying the cost-effectiveness of mobile cognitive behavioral therapy (CBT) for patients with generalized anxiety disorder (GAD).

After applying this framework, they found that mobile CBT may lead to cost reductions of $2.33 billion and $4.54 billion compared with traditional CBT and no CBT, respectively.

In the analysis, mobile CBT was more effective than traditional or no CBT in improving medical outcomes. Evitation raised $10 million from Sanofi-Genzyme BioVentures last spring to help its partners maximize the impact of their products.

4、AliveCor

AliveCor’s FDA-cleared electrocardiogram (EKG) technology has been validated in two independent studies:

• A study published in the Journal of the American College of Cardiology found that the KardiaBand, a wearable personal electrocardiogram used in conjunction with the Apple Watch, can accurately distinguish between atrial fibrillation and sinus rhythm, a finding that has been reviewed and endorsed by physicians.

• A second study conducted in collaboration with the Mayo Clinic found that KardiaBand, when used in conjunction with deep learning technology, can detect hyperkalemia.

5、IBM Watson

A study conducted at the Mayo Clinic found that IBM’s Watson for Clinical Trial Matching system increased enrollment in breast cancer clinical trials at Mayo by 80%. Furthermore, the time required to screen for clinical trial eligibility was reduced compared with standard methods.

Upcoming Research:

1. Omada Health announces collaboration with the University of Nebraska Medical Center and Wake Forest University to launch the largest clinical trial of a digital diabetes prevention tool;

2. Evidation Health recently launched the DiSCover project, a study aimed at developing better digital biomarkers to help measure the severity of chronic pain, acute episodes, and quality of life. They plan to recruit 10,000 participants in this fully virtual study;

3. Researchers at Indiana University’s Regenstrief Institute, in collaboration with Merck and the National Sleep Foundation, have launched a new study to investigate whether sleep data from Fitbit wearable devices should be considered an important marker in primary care settings.

References:

https://rockhealth.com/reports/q1-2018-funding-keeps-climbing-as-digital-health-startups-double-down-on-validation/