Walmart Eyes Humana Acquisition to Accelerate Healthcare Ambitions

Recently, VCBeat (WeChat ID: vcbeat) learned from The Wall Street Journal that a retail giant is planning to acquire the health insurance company Humana.

In fact, Walmart’s expansion has never ceased over the years. However, whether through vertical mergers or horizontal expansion, Walmart’s growth footprint has never crossed the boundaries of its core retail sector. This makes Walmart’s choice of Humana, a leading player in healthcare services, as its acquisition target appear somewhat self-contradictory. So how should we interpret this acquisition? Let us begin by examining the dynamic changes within the healthcare industry.

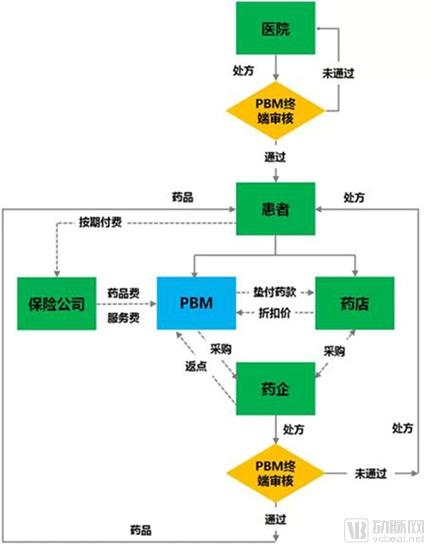

Let’s begin with a set of data: according to CB Insights, annual healthcare spending in the United States reaches $3.5 trillion. As a highly market-oriented country, the U.S. has seen market forces permeate every sector, including healthcare. In the American healthcare system, Pharmacy Benefit Managers (PBMs) serve as the central hub, coordinating hospitals, pharmaceutical companies, and health insurers to operate efficiently, thereby delivering high-efficiency, low-cost healthcare services to Americans.

Humana, which is set to be integrated into Walmart’s empire, started out in health insurance and has also ventured into the PBM sector, where it has recently been thriving.Aetna had attempted to acquire Humana as early as 2015, but the effort ultimately failed.

Faced with the lucrative opportunities in the healthcare industry, market participants are naturally eager to act. In developed market economies, a company that does not aspire to monopolistic dominance is hardly considered a successful enterprise. Through successive rounds of consolidation, the U.S. pharmacy, health insurance, and Pharmacy Benefit Manager (PBM) sectors have evolved into highly concentrated market structures. However, the advent of the internet has blurred the boundaries across all industries, leading to a series of cross-sector consolidation dramas within the healthcare sector.

First, in late 2017, CVS Health Corporation proposed to acquire Aetna for $69 billion, creating a cross-sector integration of “pharmacy + health insurance.”Shortly thereafter, in early 2018, Amazon announced a joint venture with investment giants Berkshire Hathaway and JPMorgan Chase to establish a healthcare company aimed at providing medical services to their employees. This move was widely interpreted as a signal that Amazon was entering the healthcare industry. Subsequently, Cigna proposed a $54 billion merger with Express Scripts, a pharmacy benefit manager (PBM), creating a cross-sector integration of “health insurance + PBM.” In all these cross-industry consolidations, the parties involved stated their intention to leverage deep collaboration to deliver better healthcare services at lower costs. In other words, once completed, these transactions would inevitably have a significant impact on the landscape of the U.S. healthcare industry.

At this point, you might ask: “With the healthcare industry undergoing such dramatic changes, what does it have to do with Walmart, the neighborhood grocery and department store chain?” Having such a question indicates that you are unaware of Walmart’s other identity.

Walmart opened its first store in Arkansas, USA, in 1962, went public on the New York Stock Exchange in 1972, and became the largest retailer in the United States in 1988. By 2018, it had become the world’s largest retailer, the largest private employer, and ranked first among the Fortune Global 500 companies.

How about Walmart Pharmacy?

For more than half a century, Walmart has been known as a place to purchase a wide variety of goods. What you may not know is that Walmart is also one of the largest pharmacy chains in the United States, with over 4,700 retail pharmacies located across the country.

At the end of 2017, data firm CB Insights mapped out the acquisition landscape of U.S. chain pharmacy giants, which included Walmart.

According to CB Insights, for many consumers, the era of standalone local pharmacies is long gone, replaced by large retailers with stronger financial backing and greater brand recognition. Today, the top four pharmacy chains by store count—Walmart, Walgreens, CVS Health, and Rite Aid—collectively operate more than 25,000 retail pharmacy locations. CB Insights compiled M&A data from 2012 to 2017 and found that while Walmart engaged in acquisitions most frequently among these pharmacy giants, it is Walgreens that has been truly active in the healthcare industry.

Drawing on the methodology of CB Insights, VCBeat has summarized Walmart’s acquisition cases that are publicly available. Since 1999, Walmart has completed a total of 28 acquisitions, with the largest being the $8 billion purchase of e-commerce platform Jet.com in June 2016.

Through all 28 acquisition deals, Walmart has integrated retailers, chain supermarkets, shopping malls, e-commerce platforms, social media platforms, cloud computing providers, and information service providers across the globe, including in Japan, China, Mexico, South Africa, and Chile. The range of categories is undeniably extensive, yet Walmart appears to be focusing solely on becoming a retail behemoth.

Data compiled by VCBeat

Walmart recently announced that it will invest more than $500 million over the next three to five years to establish 50 new stores across India.

Given these acquisition sprees, healthcare companies do not appear to be ideal targets for Walmart. So, does Walmart Pharmacy intend to simply remain a quiet, conventional pharmacy?The answer is actually no.

One of the most intuitive rebuttals is that Walmart once stated in 2014: “Our goal is to become the leading healthcare provider in the industry.”Over the past decade, Walmart has been actively preparing to enter the healthcare sector, achieving a number of notable successes along the way.

Prescription Plan:Walmart offers consumers prescriptions for a total price of $4, helping them reduce medication costs;

Healthcare Convenience:Walmart provides health advisory services to consumers in its stores.Only$40 per visit;

Primary Care Clinic:Through clinics located within stores, consumers can conveniently obtain prescriptions for common illnesses at Walmart, with fees as low as $40 per visit;

Medical Insurance Consultation:In the United States, consumers face a wide array of health insurance options, leading to decision fatigue. Starting in 2014, Walmart partnered with DirectHealth.com, a licensed agent that provides health insurance enrollment consulting services to consumers at Walmart stores.

Beyond that, Walmart’s most closely watched move into healthcare has actually been its partnership with Humana.

Since October 2010, Walmart has partnered with Humana to provide Medicare Part D services. Medicare is a U.S. health insurance program specifically designed for individuals aged 65 and older. In 2012, Walmart and Humana reached an agreement to offer exclusive discounts on healthy food items to select Humana customers at Walmart stores.

It can be said that the partnership with Humana has made Walmart a deep participant in the healthcare industry, rather than just a pharmacy owner.

Additionally, there is a slightly more circuitous rebuttal that can be drawn from recent years’Earnings Conference Callfound in.

During the third-quarter 2017 earnings conference call, Humana CEO Bruce Broussard pointed out, “WalmartLow Price“The Plan” was one of the few bright spots in Humana’s sluggish standalone Prescription Drug Plan (PDP) business during the quarter. He stated, “While we are pleased with the projected growth of our partnership with Walmart, our independently operated PDP business did face certain competitive pressures in 2018. As you may know, Humana offers three PDP options: the Basic Health Plan serving low-income members, the Enhanced Health Plan, and the Walmart Low-Cost Plan. The exceptional growth of the Walmart Low-Cost Plan has positioned us as a leading national provider of individual PDPs.”

During the Q4 2017 earnings conference call, Brian Kane once again mentioned Walmart’s low-price program. He pointed out that while the program’s mail-order utilization rate was the highest among other PDP products, its performance growth had become sluggish amid intensifying competition.“From an M&A perspective, we continue to focus on strategic acquisitions to enhance our capabilities, particularly in the primary care sector, but we are also actively seeking other assets that can strengthen our healthcare services portfolio. Additionally, we are interested in Medicare Advantage assets to increase our market share in underserved markets.”

This indicates that Humana places significant importance on its partnership with Walmart and believes that the collaboration model needs to be improved to address industry competition.

Deep collaboration between the two parties is imminent.

In fact, Walmart’s 2014 declaration included another passage: “We will continuously enrich our product categories and provide diversified services, thereby educating our customers that Walmart is a one-stop service provider.”

Deepening its presence in vertical industries, Walmart is steadily evolving into a large-scale, comprehensive one-stop service provider. If we were to outline Walmart’s customer profile, we would find that the healthcare services segment should be a crucial component of its one-stop offerings. According toBased on data from Kantar Retail’s ShopperScape, we can characterize Walmart’s customers asA Caucasian,51-year-old female, with an annual household income of56,482USD.This segment of Walmart’s U.S. customer base, comprising older adults with relatively limited financial means, constitutes a distinctive niche market for the retailer. Consequently, providing low-cost, high-efficiency healthcare services has become an integral component of Walmart’s one-stop service offering to this targeted segment.

With this, we can broadly understand the event of Walmart acquiring Humana.

We believe that this move should not be seen as Walmart’s emergency response to the internet wave, nor as an attempt to disrupt the healthcare industry landscape, let alone as a self-negation or a strategic pivot. Rather, it marks a further clarification of Walmart’s positioning and represents an essential step toward becoming a one-stop service provider.

In the future, as a crucial component of its one-stop service provider strategy, Walmart’s mutual penetration with the healthcare industry is highly likely to deepen. Recently, Walmart andThe acquisition negotiations with PillPack serve as clear evidence. As a provider of pharmacy sorting and distribution services, PillPack’s integration will better serve Walmart’s customers and help streamline its retail pharmacy operations.