China's $115 Billion Push to Replace U.S. Medical Devices Amid Escalating Trade War

On March 22, 2018, U.S. President Donald Trump signed a presidential memorandum on trade against China, officially firing the first shot in the U.S.-China trade war and targeting the ten high-tech industries outlined in the “Made in China 2025” initiative.

On April 16, the U.S.-China trade war escalated further as the U.S. Department of Commerce announced a seven-year ban on U.S. companies selling any electronic technologies or communication components to ZTE Corporation. ZTE found itself at the epicenter of U.S.-China trade frictions, becoming a “sitting duck” for U.S. efforts to curb China’s information technology industry.

In fact, in addition to the information technology industry, China’s high-performance medical device industry, as one of the ten key development areas outlined in “Made in China 2025,” has also unfortunately been hit.

High-performance medical devices primarily include: high-performance diagnostic and therapeutic equipment such as imaging systems and surgical robots; high-value medical consumables such as fully bioresorbable vascular stents; mobile health products including wearable devices and remote diagnosis and treatment solutions; and new technologies such as bioprinting (3D printing) and induced pluripotent stem cells.

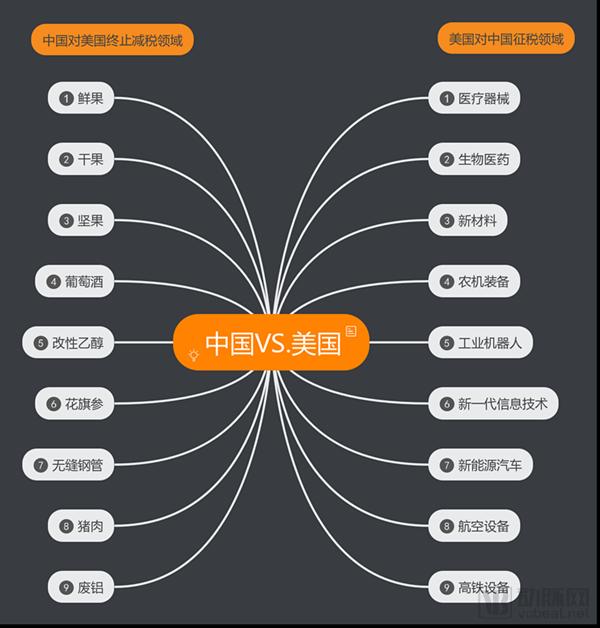

On April 3, the Office of the United States Trade Representative (USTR) released a proposed list of Chinese goods subject to additional tariffs, based on the findings of its “Section 301 investigation.” The proposal recommends imposing an additional 25% tariff on the Chinese products included in the list. The list comprises approximately 1,300 independent tariff lines, with a total value of around $50 billion.

In the USTR's proposed tariff list,The scope covers a wide range of medical devices; in addition to the several categories of high-performance medical devices mentioned in "Made in China 2025," some ordinary medical consumables and low-to-mid-end medical equipment are also included in the proposed tariff list.(See detailed list below).

Clearly, the medical device industry has become a casualty of this round of the U.S.-China trade war.

China-U.S. Medical Device Trade: Import and Export Overview

According to China Customs statistics, in 2017, the total export value of medical devices from China reached USD 21.703 billion, a year-on-year increase of 5.84%, hitting a record high. Among this, exports to the United States amounted to USD 5.838 billion, also representing a 5.84% year-on-year growth.The United States has become the largest export destination for Chinese medical devices, with its ally Japan ranking as the second-largest.

Data source: China Association for Medical Device Industry

Although export value has increased, China’s current medical device exports are still dominated by low-value consumables and mid-to-low-end products, with the industry heavily reliant on low-cost factors such as raw materials and labor. The top ten exported products, primarily consisting of massage and wellness devices and medical consumable dressings, account for 44.5% of China’s total medical device export value.

Data source: China Association of Medical Device Industry

Among these, exports of massage appliances increased by 9.58% year-on-year, reaching USD 2.292 billion; exports of syringes, needles, catheters, cannulas, and similar articles amounted to USD 1.245 billion, with exports of syringes (with or without needles) totaling USD 684 million; exports of therapeutic breathing apparatuses, such as oxygen therapy equipment and artificial respirators, reached USD 592 million; exports of hemostatic materials, including absorbent cotton, gauze, and bandages, totaled USD 769 million; and exports of high-voltage generators, consoles, and related equipment amounted to USD 563 million.

According to incomplete statistics from VCBeat (WeChat ID: vcbeat),All of these products, which rank among China’s top ten medical device exports, are included in the U.S. list of Chinese medical devices subject to additional tariffs.

Furthermore, this round of U.S. trade war also focuses on intellectual property and high-tech sectors, explicitly aiming to curb the potential rise of high-performance medical devices listed in "Made in China 2025."

In recent years, Chinese-made high-end medical devices, including imaging equipment such as ultrasound and patient monitors, as well as high-value consumables like artificial joints, have gradually demonstrated their influence in the international market. Additionally, exports of products such as cardiac pacemakers, prosthetic body parts, and scintillation cameras have seen significant growth, with a year-on-year increase exceeding 30% in 2016. Notably, these products are also included in the U.S. proposed tariff list against China.

Furthermore, the international competitiveness of China’s orthopedic and fracture care devices has improved significantly in recent years. The export outlook for Chinese dental equipment and materials has been relatively optimistic, with dental handpieces demonstrating strong competitiveness in the global market, and exports of dental X-ray equipment and dentures showing rapid year-on-year growth. These products have also been included in the list.

Once this tariff list is implemented, the blow to China’s medical device industry will be greater than expected, and some export-oriented enterprises will also suffer significant direct impacts. Taking Mindray as an example, currently, one out of every five newly purchased patient monitors in U.S. operating rooms is from Mindray, and one out of every eight anesthesia machines is from Mindray. Mindray’s ultrasound systems rank among the top three in the U.S. point-of-care (POC) market. Notably, the products subject to the new U.S. tariffs on Chinese goods include patient monitors and anesthesia machines.

The overseas market for medical devices differs from the domestic market in China. When Chinese products enter developed country markets, price becomes a significant advantage under conditions of product homogeneity. The imposition of tariffs on high-performance medical device imports from China would directly impact the market sales of some companies in the industry, potentially bringing an abrupt end to the emerging global expansion of Chinese-made equipment and high-value consumables.

Chinese Medical Device Companies’ M&A Activities in the U.S. May Face Restrictions

Trade rivalry is, at its core, a technological contest. In addition to restricting Chinese products, the United States also aims to curb the development of China’s high-tech industries.

If the impact of additional tariffs has so far been limited in scope, then U.S. restrictions on Chinese medical device companies’ investments and acquisitions of U.S. firms, along with curbs on the flow of high-tech innovations from the United States to China, would deliver a significant blow to China’s medical device industry.

As early as February this year, the Trump administration released the “2018 Trade Policy Agenda and 2017 Annual Report,” using it to launch a Section 301 investigation aimed at preventing China from acquiring U.S. technology and intellectual property through unreasonable and discriminatory measures.

It is an undeniable fact that China relies on imports in the field of high-end medical equipment. In recent years, driven by policy support and capital investment, domestically produced medical devices have achieved certain technological breakthroughs, with some sectors even narrowing the gap or catching up. However, when it comes to the most cutting-edge and frontier technologies, the United States remains the undisputed leader. At this stage, U.S. technology continues to hold significant importance for Chinese medical device companies.

Furthermore, an analysis of overseas mergers and acquisitions by Chinese medical device companies in recent years reveals that the majority of high-value and high-impact transactions are associated with the United States.Chinese medical device companies still favor U.S. technology in their overseas M&A activities.If the Sino-U.S. trade war continues to escalate and Chinese medical device companies face restrictions on mergers and acquisitions in the United States, it will inevitably have a certain impact on the development of China's medical device industry.

800 Billion Yuan in State Support Fuels the Rise of Domestic Medical Devices

So, how can one remain invincible in this protracted war against trade barriers? The rise of domestic products is the key!

From the perspective of China's medical device market, high-end products are primarily reliant on imports. Although China has more than 2,000 enterprises with export certification, most of these companies exhibit relatively weak competitiveness in terms of scale and brand recognition, and lack core technologies. As a result, their exports are predominantly conducted through Original Equipment Manufacturing (OEM) arrangements, lacking proprietary brands, which places them at an overall disadvantage in international market competition.

Accelerating the enhancement of technological innovation capabilities within China’s medical device industry and strengthening industry-academia-research collaboration in medical device R&D have become urgent priorities. The US-China trade war has further intensified these challenges, making the rise of domestically produced medical devices key to avoiding strategic vulnerability in this bloodless conflict.

U.S. restrictions on technology transfers to China will compel domestic medical device manufacturers to intensify independent innovation and accelerate the commercialization of technological achievements in the medical device sector. Meanwhile, these restrictions will further strengthen the state’s commitment to supporting domestically produced high-performance medical devices, leading to the introduction of more policies that incentivize independent innovation within the medical device industry, thereby accelerating the import substitution of domestic medical devices.

On March 23, the National Development and Reform Commission (NDRC) and the Export-Import Bank of China signed the “Cooperation Agreement on Supporting the Development of Strategic Emerging Industries” (hereinafter referred to as the “Agreement”) in Beijing.

"The Agreement" clarifies that, in order to increase the support of policy-based finance for emerging industries,The Export-Import Bank of China will, during the 13th Five-Year Plan period,Provide enterprises with financing of no less than RMB 800 billion, with priority support for the implementation of initiatives outlined in the "13th Five-Year Plan for National Strategic Emerging Industries," including the development of emerging industry clusters, major projects, and the construction of related innovation platforms.

Medical devices are one of the key industries prioritized for development in the "13th Five-Year Plan" for National Strategic Emerging Industries.

In November 2016, the State Council issued the "13th Five-Year Plan for the Development of National Strategic Emerging Industries." It explicitly proposed that by 2020, five new pillar industries with an output value of RMB 10 trillion each would be established in the fields of next-generation information technology, high-end manufacturing, biology, green and low-carbon industries, and digital creativity. Among these five new pillars with a scale of RMB 10 trillion each, four sectors—information technology, intelligent manufacturing, the bio-industry, and strategic emerging industries—are all related to medical devices.

Subsequently, in January 2017, to implement the "13th Five-Year Plan for National Strategic Emerging Industries Development" and guide the allocation of resources across society, the National Development and Reform Commission issued the 2016 edition of the "Guidance Catalogue of Key Products and Services for Strategic Emerging Industries."

The 2016 edition of the Catalogue covers five major fields and eight industries, further refined into 40 key areas with 174 sub-directions, encompassing nearly 4,000 specific products and services. These include the biopharmaceutical industry (i.e., the pharmaceutical industry) and the biomedical engineering industry (i.e., the medical device industry).

Meanwhile,In the medical device industry, the 2016 edition of the Catalogue has identified four key priority areas—medical imaging equipment, advanced therapeutic devices, medical diagnostic and testing instruments, and implantable/interventional biomaterials—which will receive prioritized support.

The Rise of Domestically Produced Medical Devices: A Clear Trend Toward Import Substitution

Although the ongoing trade war has had an impact on China’s medical device industry, the extent is limited. According to a research report released by Tianfeng Securities’ healthcare team, from a broader trend perspective, China’s high-end medical devices already possess the competitive advantage to compete on equal footing with imported brands.

High-end medical devices have already met the qualifications for import substitution.

According to EvaluateMedTech’s 2015 forecast, the global medical device market was valued at $395 billion, with China accounting for approximately 10% and an industry growth rate of 5% projected over the following five years. The medical device sector comprises numerous subsegments, among which high-end products with significant entry barriers primarily include medical imaging, in vitro diagnostics (IVD), cardiovascular stents, and orthopedics. In China, domestically produced medical imaging equipment holds a market share of approximately 10–20%, while domestic IVD products account for around 30–40%. Within the diagnostics segment, high-end products such as chemiluminescence immunoassays currently hold a market share of approximately 10%. Major competitors in China’s medical device market, such as GPS (GE, Philips, Siemens) and Roche, Abbott, Beckman, and Siemens, are predominantly imported products from companies based in the United States and Europe.

In recent years, with the rise of domestic private enterprises, products in certain niche segments have been able to meet clinical needs. The improvement of talent, capital, and systems has accelerated the process of domestic substitution. In some niche areas, such as the blood cell market in in vitro diagnostics, domestic products already have the capability to replace imports.

Resonance Between Domestic and International Environments Accelerates Import Substitution of High-Quality, High-End Medical Devices

Under the State Council’s institutional reform plan, personnel changes are accelerating the implementation of healthcare reform policies. Initiatives such as tiered diagnosis and treatment and health insurance cost containment will be executed at an unprecedented pace, thereby speeding up the development of the primary healthcare market. Domestic medical device companies will continue to benefit from this incremental growth.

The first shot of the overseas trade war has been fired, which is expected to have a certain impact on U.S. imported products in the long run. For instance, Abbott and Beckman, major players in chemiluminescence immunoassay (CLIA), primarily offer products imported from the United States and have long dominated the high-end market. The CLIA market was valued at approximately RMB 25 billion in 2017, with these two companies collectively accounting for about RMB 8 billion. Their core product segments—Abbott’s infectious disease assays and Beckman’s hormone assays—are areas where domestic manufacturers are currently able to provide substitutes.

Amid the superimposed resonance of internal transformation and external shocks, numerous enterprises will continue to reap benefits.

Multiple Policies Introduced to Promote the Commercialization of Innovative Medical Devices

In recent years, the Chinese government has repeatedly introduced robust policies in the field of innovative medical devices, with a focus on enhancing innovation capabilities and industrialization levels. These policies primarily revolve around three objectives: accelerating the review and approval of innovative medical devices; prioritizing the development of products with significant clinical value; and achieving breakthroughs in independent innovation to accelerate domestic production.

In February 2014, the China Food and Drug Administration (CFDA) issued the “Special Examination and Approval Procedures for Innovative Medical Devices (Trial),” which required that medical devices applying for approval be mature products possessing invention patents for core technologies, featuring working principles pioneered in China, demonstrating fundamental improvements in performance or safety compared to similar products, representing internationally leading technical standards, and offering significant clinical value.

In October 2016, the China Food and Drug Administration (CFDA) issued the “Procedures for Priority Review of Medical Devices,” which implemented priority review for registration applications of domestic Class III and imported Class II and Class III medical devices intended for the treatment of rare diseases, common cancers, diseases specific to or prevalent among the elderly, pediatric conditions, and other clinically urgent needs. Meanwhile, support was extended to medical devices included in the National Science and Technology Major Projects or the National Key Research and Development Program.

In October 2017, the General Office of the Central Committee of the Communist Party of China and the General Office of the State Council issued a landmark policy featuring 36 reform measures to vigorously promote the development of independently innovated pharmaceuticals and medical devices. On October 31, the China Food and Drug Administration (CFDA) responded actively by aligning with the policy’s strategic direction and formulating the “Amendment to the Regulations on the Supervision and Administration of Medical Devices (Draft for Public Comment).”

Furthermore, regarding market demand, domestic demand in China has been gradually strengthening over the past two years, with corresponding leading medical device companies experiencing remarkable growth rates. Therefore, driven by innovation coupled with rising demand prosperity, the future development of Chinese-made medical devices is highly promising.

US Multi-Billion Dollar Medical Device Industry May Be Affected

In addition to China’s medical device industry, the ongoing US-China trade war will also have a certain impact on the US medical device industry.

Recently, a report on the U.S. information website Fierce Biotech stated that Trump’s policy is likely to have an adverse impact on the U.S. medical device industry, with the scale of involvement potentially reaching billions of dollars. U.S. device manufacturers and patients are likely to bear the cost.

In the latest tariff list, Trump claimed that imposing a 25% tariff on imported pacemakers, orthopedic implants, and other medical devices would help reverse the damage inflicted on the U.S. economy and force China to change its practices. However, some experts argue that this approach will not fundamentally resolve the issue. Currently, Chinese exports of medical devices to the United States account for a relatively small share, with a significant portion of these products being manufactured and sold by subsidiaries of U.S. companies operating in China.

Several market research firms also believe that this policy will harm the U.S. medical device industry. For instance, RBC Capital Markets estimates that the medical device industry will incur costs exceeding $1.5 billion, while AdvaMed suggests that the figure could reach as high as $5 billion. Greg Crist from AdvaMed stated that this move will undoubtedly affect the vital interests of American patients.

These estimates indirectly reflect the fact that, after years of development, China’s medical device industry has gradually transitioned from initial low-value consumables, such as gloves, to high-end equipment with greater technological sophistication. Once tariff policies are implemented, the entry of certain products into the United States—such as MRI scanners, CT scanners, ultrasound instruments, and knee implants—will be significantly affected.

References

Sources: CBI Devices, Medical Device Distributors Alliance, MedTech Innovation Network, Osida, etc.

1、http://mp.weixin.qq.com/s/Q67f8gZmY__zraaRRCIvIA

2、https://mp.weixin.qq.com/s/xK8kAVXI9JimgN2hFKtYVA

3、http://mp.weixin.qq.com/s/wpDPjBW3Ijs5LPJT-yU73Q

4、https://mp.weixin.qq.com/s/IYa7vaY3mtcBIZ3-hjqY-Q

5、http://mp.weixin.qq.com/s/POkWas-lVULXYnVjA_stsw