State-Owned Capital Entry Propels Haihong Holdings' Rebranding to Guoxin Health, Market Cap Doubles to RMB 40 Billion

Recently, Haihong Holdings (000503.SZ) announced that its board of directors had passed a resolution to change the company’s name to “Guoxin Health Care Service Group Co., Ltd.” and its stock abbreviation to “Guoxin Health.”

At the end of last year, Haihong Holdings introduced capital from state-backed investors, transforming from a privately owned enterprise into a state-controlled listed company, while also adjusting its management structure and business operations. This name change signifies that Haihong Holdings has entered a “new era” of development.

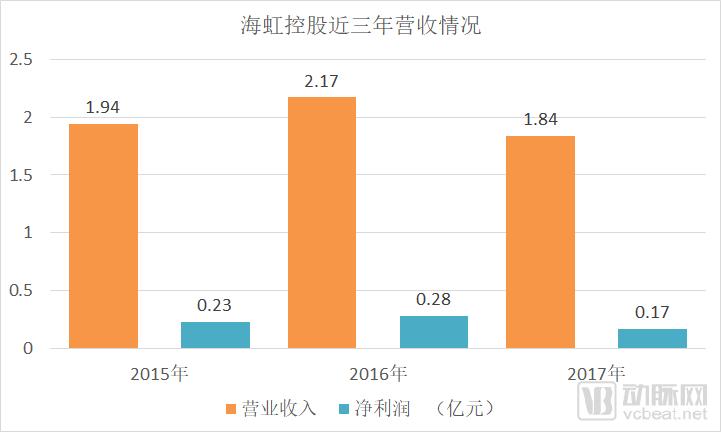

During the same period, Haihong Holdings disclosed its 2017 preliminary earnings report, reporting operating revenue of RMB 184 million for the period, a year-on-year decrease of 15.15%; and net profit attributable to shareholders of the listed company of RMB 17 million, a year-on-year decrease of 40.49%.

Since Haihong Holdings introduced capital from the "National Team," the capital market has placed high expectations on the company. Following the announcement of this plan late last year, Haihong Holdings’ stock price surged, hitting the daily limit up for several consecutive days. Currently, Haihong Holdings’ market capitalization has exceeded RMB 40 billion, doubling its value prior to the introduction of National Team investment and business restructuring.

What will the injection of state-backed capital bring to Hailong Holdings? How will its business direction be adjusted? What are the capital market’s expectations for the company, and what is its future development trajectory? VCBeat (WeChat ID: vcbeat) aims to answer these questions.

500 Million vs. 22 Billion: How Does the “National Team” Leverage Small Capital for Big Gains?

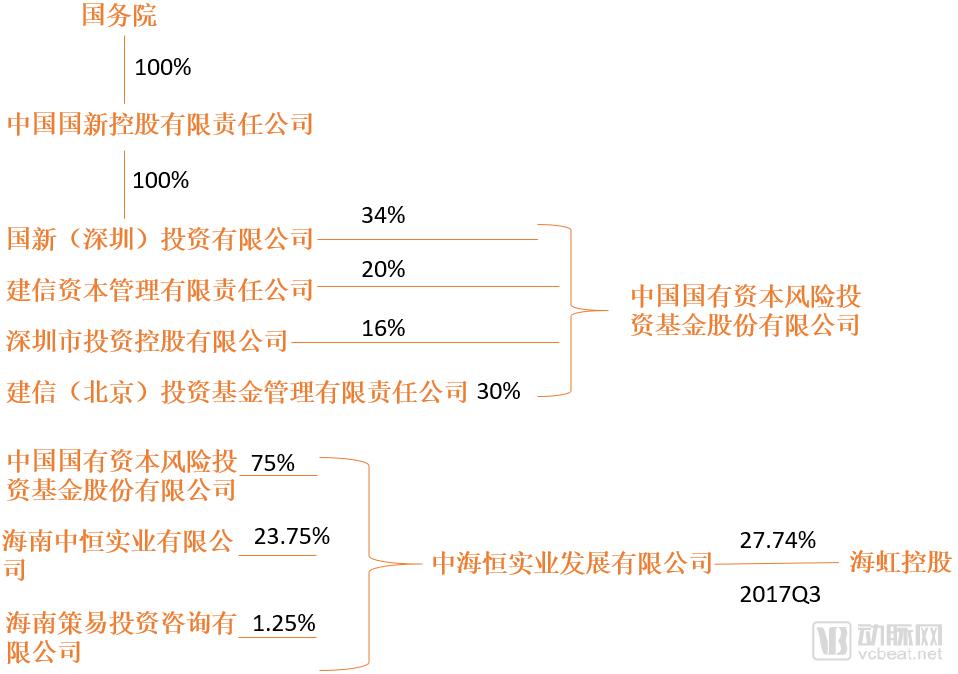

In November 2017, Haikhong Holdings announced a change in its actual controller, with China State-owned Capital Venture Investment Fund Co., Ltd. becoming the listed company’s actual controller. The full name of the fund is China State-owned Capital Venture Investment Fund Co., Ltd., which was registered and established in Qianhai, Shenzhen, in August 2016.

As a “national-level” investment fund, the China State-owned Capital Venture Investment Fund was initiated and controlled by China Reform Holdings Corporation, in partnership with Postal Savings Bank of China, China Construction Bank, Shenzhen Investment Holdings Co., Ltd., and other founding entities. With an initial size of RMB 100 billion, its total scale is expected to reach RMB 200 billion in the future. The fund will primarily support technological innovation and industrial upgrading projects of central state-owned enterprises (SOEs), leveraging the radiating and driving effect of state capital to amplify its function and stimulate social investment.

Since its establishment, China National Cultural Industry Investment Fund has completed several major investments, with portfolio companies including United Imaging Healthcare, Megvii (Face++), 3DMed (SiliMed), and Cambricon.

Under the agreement, China State-owned Capital Venture Investment Fund will take a “backdoor” controlling stake in the listed company Haihong Holdings by injecting capital into Haihong’s controlling shareholder, Zhonghaiheng Industrial Development Co., Ltd. The Fund will hold a 75% equity interest in Zhonghaiheng Industrial, which in turn holds a 27.74% stake in Haihong Holdings. This means that China State-owned Capital Venture Investment Fund will indirectly hold approximately 20.80% of Haihong Holdings’ shares.

Table 1: Introduction of Investors and Equity Relationships by Haihong Holdings

Investment Approach of the China National Venture Capital Fund:

1) Pay RMB 500 million in capital increase contributions to Zhonghaiheng Industrial Co., Ltd., of which RMB 300 million shall be credited to the registered capital of Zhonghaiheng, and the remaining RMB 200 million shall be credited to the capital reserve of Zhonghaiheng;

2) Pursuant to the Transfer Agreement, the parties agree that, provided Zhonghaiheng continues to legally and validly exist and no debt disputes arise, China Venture Capital Fund may, within five years from the Registration Date and at its sole discretion based on the actual operational conditions of Zhonghaiheng and Haihong Holdings, decide to inject RMB 3.696 billion into Zhonghaiheng;

Meanwhile, the parties also agreed on repurchase clauses. All parties agree that Hainan Zhongheng (or its designated party) shall repurchase all equity interests in Zhonghaiheng held by Guofengtou Fund upon the occurrence of any of the following circumstances and at the request of Guofengtou Fund:

1) With respect to the subsequent capital injection into the China National Venture Capital Fund as agreed, upon the expiration of five years from the registration date (with each year calculated as 365 days), the China National Venture Capital Fund has decided not to proceed with such implementation;

2) Zhonghaiheng is sued for bankruptcy, reorganization, or dissolution at any time;

The repurchase price for the equity under the aforementioned circumstances shall be the sum of the capital increase contributions actually paid by Guofeng Investment Fund prior to the repurchase date and the interest accrued on such funds at a simple annual interest rate of 5%. Specific matters concerning the equity repurchase shall be separately agreed upon in an equity repurchase agreement to be executed by the relevant parties.

The above clauses indicate that,China State-owned Venture Capital Fund is expected to invest a total of RMB 4.196 billion to acquire approximately 20.80% equity stake in Haihong Holdings. The fund will make an initial capital contribution of RMB 500 million, with the remaining funds to be fully paid within five years.Given the potential gains that China Guofeng Investment may realize from its holdings in Haihong Holdings' stock, this investment could offer substantial upside potential.

Some commentators have also stated that the China National State-owned Capital Venture Investment Fund, with an investment of RMB 500 million, leveraged a listed company valued at over RMB 20 billion (the market capitalization of Haihong Holdings was approximately RMB 22 billion when China National State-owned Capital Venture Investment Fund took control), making it the “most successful” national team fund.

Since the announcement that China Guofeng Investment Fund had taken control of Haihong Holdings, Haihong Holdings’ stock price has soared, hitting the daily upper limit for multiple consecutive days. Currently, Haihong Holdings’ market capitalization has exceeded RMB 40 billion, doubling its pre-“national team” entry valuation.

Table 2: Market Capitalization Trend of Haihong Holdings

On April 13, Haihong Holdings announced that its board of directors had approved the “Proposal on Changing the Company Name and Stock Abbreviation,” renaming the company to Guoxin Health Care Services Group Co., Ltd., with the stock abbreviation changed to “Guoxin Health.”

During the same period, the candidates for the new board of directors of Haihong Holdings were also confirmed. It was decided to nominate Jia Yanyan, Jiang Kaihong, Han Wei, Wang Zhigang, Zhang Ling, and Liu Yingjie as candidates for non-independent directors of the 10th Board of Directors; and to nominate Qian Qingwen, Huang Anpeng, and Wang Xiuli as candidates for independent directors of the 10th Board of Directors.

Table 3: Nominees for the New Board of Directors of Haihong Holdings

From the perspective of the new board’s composition, three executives from the “China Reform Holdings” system have joined: Jiang Kaihong (Deputy General Manager of China Reform Fund Management Co., Ltd.), Wang Zhigang (CSO of China Reform Fund Management Co., Ltd.), and Zhang Ling (Managing Director of China Reform Risk Investment Management (Shenzhen) Co., Ltd., as well as Director and General Manager of Zhonghaiheng Industrial Development Co., Ltd.). This also implies that China Reform Holdings may hold significant influence on the board, possessing decisive power over the future development direction of Haihong Holding. Two executives from the “Haihong system,” Han Wei and Liu Yingjie, have newly joined the board, which also represents the new board’s affirmation of Haihong’s existing business.

Why Did National Team Funds Target Zhonghong Holdings?

The announcement stated that the China State-owned Capital Venture Investment Fund, after conducting on-site due diligence and research, agreed withHaihong Holdings provides intelligent medical insurance audit services to 149 medical insurance pooling entities across 23 provinces in China, accounting for approximately 37.63% of all such entities nationwide. The service covers 270 million insured individuals and involves a total medical insurance pooling fund scale exceeding RMB 500 billion, ranking first in the country.

Having dedicated eight years to the field of medical insurance audit services, Haihong Holdings has built an extensive knowledge and technical framework comprising “Four Databases” and “Twenty-Four Systems.” This effort has resulted in localized medical insurance cost-control audit databases for various regions. These solutions have been repeatedly validated through practices in the refined and professional management of medical insurance funds, yielding a series of products and services recognized by stakeholders—including medical insurance authorities, health and family planning commissions, hospitals, and patients. Offerings include intelligent pre-, during-, and post-event audits and services; big data analytics for operational decision-making regarding medical insurance funds; medical quality evaluation systems; medical insurance payment standards; DRG payment and settlement; health records; and new smart healthcare initiatives.

Guofeng Investment Fund believes that,In the field of intelligent audit and services, Hailiang Holdings is currently the medical insurance fund service company in China with the highest technical level, the most comprehensive product range, and the highest quality.

China State-owned Capital Venture Investment Fund and China Reform Holdings Corporation believe that Neusoft Healthcare, by positioning itself at the core of medical insurance payments, serves as a pivotal hub connecting medical insurance, healthcare services, and pharmaceuticals. With China State-owned Capital Venture Investment Fund becoming the indirect controlling shareholder, and while maintaining the role of the original management team, the company will leverage Neusoft Healthcare’s existing technical services and market share to further enhance its support for medical insurance from both breadth and depth. This strategy aims to achieve refined management, effectively prevent the deficit risk of medical insurance funds, and safeguard the security of social security funds.

On the other hand, by supporting work related to the connotation, systems, and standards of health insurance payment, it helps establish a new order for medical consultations, improve the operational efficiency of medical resources, and enhance pharmaceutical companies’ R&D and market capabilities. By serving every link of the medical security system, it provides support for building a new-type system of medical services, medical security, and supervision and management, thereby offering a practical pathway for the coordinated development of healthcare, medical insurance, and pharmaceutical sectors (the “Three-Medical Linkage”) and for healthcare system reform.

The primary client of Haihong Holdings is the Basic Medical Insurance Fund, which currently stands as China’s largest medical insurance fund in terms of scale, disease coverage, demographic complexity, geographic span, and the richness of data on pharmaceuticals, medical consumables, medical devices, medical service items, and clinical diagnosis and treatment information. Both statistically and managerially, the sample size is sufficiently abundant and discrete to reflect the fundamental characteristics of national health.

After making a controlling investment in Haihong Holdings, China Reform Venture Capital Fund designated it as a strategic project for both the fund and China Reform Holdings Corporation Ltd., actively seeking understanding and support from the government and relevant departments to accelerate the development of the healthcare insurance fund management services industry.

By obtaining relevant authorizations or collaborating with authorized institutions, and implementing effective measures to ensure security, we will innovate the development mechanism for national medical and health data. We will explore the comprehensive implementation of Pharmacy Benefit Management (PBM) in China, provide Third-Party Administrator (TPA) services for commercial medical and health insurance, deliver big data services for the pharmaceutical industry, and offer internet-based intelligent medical services. Furthermore, we will build a public service big data platform, cultivate new central state-owned enterprises in the health and medical big data sector, promote the development of the health and medical industry, and maximize social benefits while ensuring shareholder returns.

Haikong Holdings: To Focus on Five Major Businesses in the Future

With the infusion of state-backed capital, a corporate name change, and adjustments to its board of directors and management structure, Haihong Holdings has completed the first step of its sweeping “reform,” which has been well received by the capital market. So, where will Haihong Holdings’ business head in the future to gradually fulfill its “promises” to the capital market?

According to Haihong Holdings’ official statement, the company has established a new development strategy by leveraging its own strengths, market offerings, and competitive landscape. In the next phase, its strategic focus will center on the following key areas:

1) Medical Insurance Cost Control Audit Services

The basic audit system was integrated and upgraded into the “Cloud Platform for Economical Management of Medical Insurance,” providing comprehensive technical outsourcing and services for medical insurance administration, referred to as “Third-Party Review Services.” The goal for 2018 was to consolidate the existing market share in 149 pooling areas while continuing to capture new markets and achieve nationwide coverage across China.

Regarding fees, the cloud platform service fee is charged first. Taking a pooling area with a population of 3 million as an example, the charging standard for the cloud platform is RMB 5 million.

In addition, for regions facing a high risk of medical insurance fund deficits and an urgent need for cost containment, we provide a safety net service for the medical insurance fund. Haihong Holdings will jointly establish a deficit reserve fund with the government. For example, if a city’s medical insurance fund totals RMB 2 billion, the company and the local government will each contribute 50% of 5% of the fund size into a co-managed account to prevent the fund from going into deficit. The core of Haihong’s ability to prevent such deficits lies in its cost-containment capabilities.

The fee structure for the basic coverage services of the medical insurance fund is as follows: The first component covers operational costs, amounting to no less than 2% of the medical insurance fund; the second component serves as an incentive bonus, ranging from 10% to 20% of the savings achieved through cost containment measures. These fees are paid by fiscal authorities rather than from the medical insurance fund itself. As Haihong transitions from a private enterprise to a central state-owned enterprise (SOE), government payment practices have shifted from constituting improper benefit transfers to representing allocated shares of SOE profits, thereby significantly reducing the complexities associated with local government payments.

2) DRG Fund Settlement Services

Currently, there are approximately a dozen versions of DRG-based fund settlement services available in China, provided by more than ten companies. Among them, Hailiang’s DRG solution holds a first-mover advantage and is the most advanced. It is the only DRG system that has achieved full fiscal-year fund settlement within a medical insurance pooling area and gained recognition from all medical institutions. Through four years of effort, Hailiang successfully implemented full fiscal-year fund settlement in Jinhua, Zhejiang Province, in 2017. At present, Zhejiang and Guangxi Provinces are promoting Hailiang’s DRG system province-wide, with fees already being charged. The fee structure is based on the scale of the medical insurance fund in each pooling area, ranging from several million yuan.

3) Medical Insurance Payment (Price) Standard Services

Currently, only Haihong is capable of determining medical insurance payment prices. The company possesses the statistical and supervisory capabilities to monitor local drug reimbursement catalogs, pharmaceutical manufacturers’ creditworthiness, drug quality, and pricing across all covered regions. A prefecture-level pooling area typically includes 30,000–35,000 drug varieties, which require re-declaration during annual price adjustments. Leveraging our highly sophisticated algorithms with stringent entry thresholds, we establish reasonable pricing for drugs included in the reimbursement catalog: reasonably increasing prices for low-cost, high-efficacy drugs to protect traditional manufacturers of affordable medicines, while bringing down unreasonably high prices. This process involves complex considerations such as consistency evaluations and pharmacoeconomics. The delivery of this service relies on Haihong’s proprietary national database of drug prices and products—an asset not even currently available to the National Medical Products Administration (NMPA)—built upon years of accumulated foundational data.

The medical insurance payment price is a crucial element in promoting equitable healthcare. For drugs listed in the same reimbursement catalog, low-income patients may be forced to request cheaper, less effective medications due to financial constraints, whereas wealthy patients can afford higher-quality drugs. However, if the reimbursement rate remains identical for both groups, the rights of financially disadvantaged individuals are significantly undermined, resulting in inequity. In this context, the role of the medical insurance payment price is of paramount importance.

The company has currently signed contracts with 30 prefecture-level cities to provide services related to medical insurance payment prices. In terms of fees, one part is an annual service fee of RMB 300,000–500,000 charged to medical insurance handling agencies; the other part is an annual certification fee of RMB 600–1,000 per product specification declared by pharmaceutical companies.

4) Commercial Insurance TPA Services

Currently, the scale of China's health insurance market remains very small. Although it achieved a 100% growth rate last year, commercial health insurance is expected to reach the same order of magnitude as public medical insurance in the future, with its market potential exceeding RMB 1 trillion.

The company has established a Third-Party Administrator (TPA) team and begun preparatory work for client engagement and big data product design. In the future, the company will leverage its accumulation of massive clinical diagnosis and treatment data to provide services to commercial insurance companies for health insurance products, aligning with government policies that permit the use of personal account balances to purchase commercial health insurance. Currently, the company has partnered with 10 commercial health insurers to deliver and charge for medical, pharmaceutical, and personal health management services tailored to specific populations.

Revenue Model: 1. Charge a service fee equivalent to 10%-15% of the sales revenue from insurance products sold through the company’s distribution channels (including hospitals and individual consumers). 2. Leverage the company’s big data capabilities to co-design precise insurance products with insurers, provide Third-Party Administrator (TPA) services, and establish a profit-sharing and risk-sharing model.

5) Health Management Services

The future represents a major source of profitability for Haihong, which serves a broad client base including government entities, basic medical insurance programs, commercial insurers, healthcare institutions, pharmaceutical companies, and individual consumers. In the area of chronic disease management, the company already has relevant products in place. Chronic care service packages are jointly designed by medical insurance administrative agencies, healthcare institutions, and Haihong. The pricing for these service packages is determined through expert review and negotiation. The company has already implemented fee-based services in regions such as Zhejiang and Guangxi, with charging standards ranging from RMB 200 to RMB 400 per person per year.

The Future of Haihong Holdings: A Medical Insurance Service Company with a Market Cap of 100 Billion?

Haihong Holdings’ latest “reform” has made it a darling of the capital market. However, this is not the first time in its development history that it has become a “favorite” of investors.

The historical origins of Haihong Holdings can be traced back to the Hainan Chemical Fiber Factory, established in 1986. In 1991, it was restructured into “Hainan Chemical Fiber Industrial Co., Ltd.” and listed on the Shenzhen Stock Exchange in November 1992, becoming one of the first batch of listed companies in Hainan Province.

In 1997, Hainan Haihong Holdings invested in the establishment of “China Public Network Information Technology and Service Company,” marking its entry into the internet and telecommunications value-added services sector. In 1999, Ourgame World, then China’s largest online board and card game platform, sold a 79% equity stake to China Public Network for RMB 5 million.

In 2001, two years later, Haihong Holdings acquired a 66.7% stake in Zhonggong Network, thereby gaining direct control of Ourgame World. This move positioned Haihong as the “first internet stock” at the turn of the century, enjoying unparalleled prominence. At that time, today’s internet giants such as Baidu, Alibaba, and Tencent had just been established and had not yet identified sustainable profit models. However, despite its prestigious “halo,” Haihong Holdings’ revenue struggled consistently, and the company even faced delisting at one point.

Since 2009, against the backdrop of China’s new healthcare reform, Haihong launched its Pharmacy Benefit Management (PBM) business and entered into a partnership with ESI, the largest PBM company in the United States. PBM, short for Pharmacy Benefit Management, is a specialized third-party service for health insurance. Its core approach shifts from fee-for-service to managed care with end-to-end monitoring, strictly controlling healthcare expenditures through models such as prescription review, disease prevention, health management, and diagnosis-related group (DRG)-based payment, thereby reducing costs for insurers and corporate employers.

Haohong Holdings’ primary benchmark is ESI, short for Express Scripts, the largest PBM company in the United States. According to its 2016 annual report, it covered more than 95% of retail pharmacies nationwide, with annual revenue reaching $100.2 billion and net profit of $3.4 billion.

Under the tailwinds of the PBM concept, Haibang Holdings’ market capitalization also surged, reaching as high as RMB 72.5 billion and breaking into the top ten by market cap in the A-share pharmaceutical and biotechnology sector.

Haihong Holdings’ approach was to sign cooperation agreements with local medical insurance bureaus in the capacity of a third-party tool provider, establishing an intelligent prescription auxiliary review platform and delivering refined management services for medical insurance funds. In the following years, Haihong Holdings successively entered into partnerships with entities such as the Zhanjiang Social Insurance Fund Administration, Zunyi Social Insurance Bureau, Yueyang Medical Insurance Fund Management Office, and Chengdu Medical Insurance Bureau. It provided third-party services for local medical insurance fund management in areas including intelligent auxiliary review of medical insurance claims and medical insurance big data, with compensation structured through government procurement of services.

However, the PBM business requires substantial upfront investment and data accumulation; Haihong Holdings has not seen a significant rise in performance, and its PBM segment continues to operate at a loss.

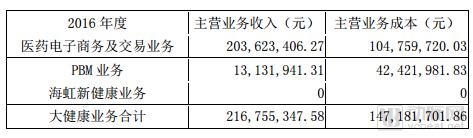

Taking its 2016 data as an example, the PBM business generated RMB 13.132 million in main operating revenue, incurred RMB 42.422 million in business costs, and reported a net loss of approximately RMB 30 million.

Revenue Composition of Haihong Holdings in 2016

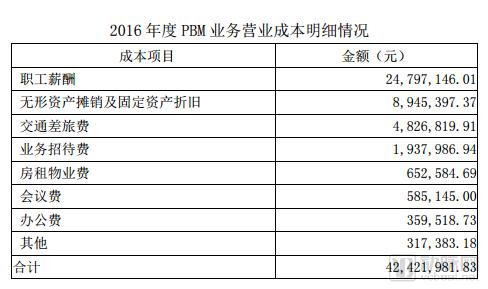

Haihong Holdings PBM Business Cost Breakdown

“The lack of a unified fee schedule” is the primary reason for the losses in Haihong’s PBM business. Factors such as limited information interoperability among hospitals, hidden financial incentives related to pharmaceuticals, and difficulties in standardizing prescription formularies have also constrained the development of its PBM operations to some extent.

Business development has been hindered, and Haihong Holdings intends to introduce capital from state-backed investors to provide a new engine for future growth. From a capital background perspective, state-owned enterprises are more likely to gain advantages in hospital relationships and the integration of healthcare big data, while Haihong Holdings’ existing technological and medical resource accumulation may find better leverage points under this new framework.

As times change, the title of “the first internet stock” has become a thing of the past. Haihong Holdings, renamed Guoxin Health, has adjusted its personnel structure and business direction to focus on the niche field of medical insurance services, embarking on a new journey of development.

From an industry perspective, the current operation of the medical insurance fund is under tight pressure, creating a strong demand for cost containment. There is a need for more diversified and robust cost-control methods and measures. Haihong Holdings’ explorations in prescription review, medical insurance fund guarantees, and DRG-related services have a clear policy foundation, making them relatively easy to implement. Its transition into a state-owned enterprise will further facilitate the implementation of its business model.

Even more promising are the commercial insurance TPA (Third-Party Administrator) business and health management services, both of which represent high-growth segments within the broader healthcare industry. If public medical insurance is characterized by “broad coverage and basic protection,” then commercial insurance constitutes a “multi-tiered and diversified” medical security system. As favorable trends such as the rise of the middle class and consumption upgrading come to fruition, the scale of commercial insurance is poised to surpass one trillion yuan, thereby creating significant growth potential for the accompanying TPA business.

“Where hills bend and streams wind, one doubts there is a path; yet willows darken and blossoms brighten, revealing another village.”After years of exploration, Haikong Holdings has identified a more viable development path. With the backing of state-owned enterprises, it may gradually evolve into a healthcare insurance services company with a market capitalization of RMB 100 billion.

References

Cninfo: 000503 Haihong Holdings – Indicative Announcement on Change in Actual Controller

Cninfo: 000503 Haihong Holdings - Announcement on Change of Actual Controller

Cninfo: 000503 Haihong Holdings 2017 Annual Performance Flash Report

China Merchants Securities: Neusoft Healthcare (000503) — Research Note from February 25, 2018