Will Chinese Medical AI Firms Face a 'ZTE-Style' Chip Embargo? Insights from a Newly Filed IPO Prospectus

The widely discussed “ZTE incident” continues to unfold. The U.S. Department of Commerce’s issuance of an export denial order against ZTE is not only a ripple effect of the escalating China–U.S. trade war, but also highlights the gap in capabilities between China and the United States in high-end, cutting-edge industries.

In modern warfare, technological competition will be a significant force, with China and the United States having already engaged in several confrontations.

As early as April 2016, the Chinese private equity investment firm CanyonBridge proposed to acquire Lattice Semiconductor. On November 3 of the same year, Lattice accepted the acquisition offer and announced that it would be acquired by CanyonBridge for $130 million, covering all outstanding shares and its debt.

Lattice Semiconductor is one of the top four global FPGA manufacturers, alongside Xilinx, Altera (acquired by Intel), and Actel (acquired by Microsemi). Headquartered in Portland, Oregon, USA, the company primarily produces communication chips used in automotive, computer, mobile devices, and other equipment, which are also applicable to military communications. It remains one of the few manufacturers capable of producing programmable logic chips.

This was ostensibly a voluntary commercial transaction, yet it was deemed by the Committee on Foreign Investment in the United States (CFIUS) to pose a threat to U.S. national security and thus failed to clear review. On September 14, 2017, President Trump directly issued an executive order blocking the deal. The attempt by Chinese investors to acquire FPGA technology through this acquisition ended in failure.

Another significant event occurred in February 2015, when China’s National Development and Reform Commission imposed a fine of RMB 6.088 billion on Qualcomm; in March 2017, the United States fined ZTE $892 million, an amount also close to RMB 6 billion.

In April 2018, prior to the ZTE incident, China’s Ministry of Commerce continued to delay its approval of Qualcomm’s acquisition of NXP, a move aimed at securing greater protection for Chinese enterprises. The intense chip war between China and the United States has also made the Chinese public acutely aware of the nation’s vulnerabilities in the semiconductor industry.

Following the sanctions imposed on ZTE, a wave of extensive discussion erupted in China. Amidst this backdrop, an AI chip acquisition drew significant attention: on April 20, Alibaba Group completed a full acquisition of C-Sky Microsystems Co., Ltd., the only independent embedded CPU IP Core company in mainland China.

On April 19, Alibaba DAMO Academy announced that it is developing a neural network chip—Ali-NPU. With this move, Alibaba has made a strong entry into the chip industry through independent R&D, acquisitions, and other means.

In the past two years, artificial intelligence has begun to rise globally, with the most robust development occurring in China and the United States. The ascent of AI technology has been driven by enhanced computing power, where chips such as GPUs and NPUs have played an indispensable role, significantly accelerating the iteration and R&D speed of AI products.

Amid the ongoing chip dispute, will the fallout spread to the artificial intelligence sector, particularly the medical AI industry that we closely monitor? If Sino-U.S. trade tensions escalate further, could medical AI companies find themselves “strangled” in much the same way as ZTE? VCBeat consulted numerous industry experts on this question.

The Medical AI Industry's Chip Dependency on the United States

Due to the need for large-scale data computation in medical artificial intelligence research, the demand for chips is extremely high.

In the field of medical artificial intelligence, there are two primary scenarios for using chips in data processing. One involves leveraging chips for computational tasks during laboratory model training to facilitate AI product iteration. The other entails embedding chips into imaging workstations or medical devices after product development is complete.

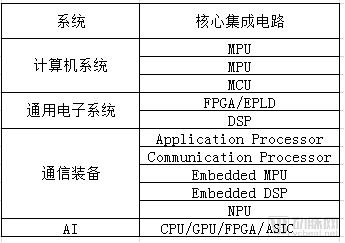

Currently, there are four main types of AI acceleration chips: CPU, GPU, FPGA, and ASIC (such as Google’s TPU). Among these, the GPU is the most widely used general-purpose chip, primarily due to NVIDIA’s aggressive promotion, high efficiency, and cost-effectiveness. CPUs suffer from low efficiency, while ASICs and FPGAs are custom and semi-custom chips, respectively; although they offer high efficiency, their limited demand results in low production volumes and high prices.

During the model training phase, companies predominantly rely on general-purpose chips. This process typically leverages NVIDIA GPUs, Intel CPUs, and FPGAs from other manufacturers. In the deployment phase, the implementation of medical AI products remains heavily dependent on chip technology. One approach is a cloud-based solution, where products are hosted in the cloud to deliver medical services. While this reduces costs, it offers somewhat limited real-time performance. Another approach involves integrating AI algorithms and software systems into custom-designed chips, which are then embedded into medical devices. This strategy helps lower power consumption, ensure system performance, and reduce device size.

It is evident that both model training and scenario-based applications impose stringent requirements on chips. At the current stage, although Chinese medical AI companies are on par with their counterparts in Europe and the United States in terms of software and algorithms, the chips they use are almost entirely dependent on imports from the U.S. There are few domestic companies with AI chip design capabilities; Cambricon Technologies stands out as a representative example, yet it still lacks proficiency in packaging and manufacturing processes.

Will the United States ban the export of AI chips to China?

Currently, nearly all chips used in AI products rely on imports, whether they are NVIDIA GPUs, Intel CPUs, or Google TPUs, with the United States being the exporting country. In the aftermath of the ZTE incident, will medical AI companies face a similar fate? Industry experts told VCBeat that the likelihood is very low. There are three reasons:

First, ZTE violated the laws of the countries in which it operates.

The reason ZTE was subjected to the ban lies in the false statements made by ZTE Corporation to the Bureau of Industry and Security (BIS) in 2016 and 2017. On April 16, 2018, the U.S. Department of Commerce’s Bureau of Industry and Security decided to activate the denial order against ZTE Corporation and ZTE Kangxun Telecommunications Ltd., on the grounds that ZTE had failed to timely reduce bonuses and issue letters of reprimand to certain employees involved in historical export control violations, and had made false representations regarding this matter in two letters submitted to the U.S. government on November 30, 2016, and July 20, 2017.

Unlike ZTE, Chinese AI companies have only utilized chips for product development and domestic operations, without engaging in export sales. In particular, the medical AI industry remains in the R&D phase and has not yet achieved large-scale commercial application, which in itself does not constitute a threat.

Second, China's chip procurement volume is enormous, making a comprehensive blockade impossible.

Source: Gartner, January 2018

According to Gartner’s survey data, three of the top ten global chip purchasers in 2017 were Chinese companies—Lenovo, Huawei, and BBK Electronics—ranking fourth through sixth worldwide, while ZTE did not make the list.

In 2017, Lenovo’s procurement amounted to $14.671 billion, Huawei’s to $14.259 billion, and BBK Electronics’ to $12.103 billion. By comparison, ZTE’s chip procurement volume was not the largest, and its procurement share from major U.S. companies such as Broadcom and Qualcomm was relatively modest.

According to a report by The Wall Street Journal, 65% of Qualcomm’s $22.3 billion in revenue generated in fiscal year 2017 came from China, up from 57% in fiscal year 2016. In Broadcom’s 2017 revenue, 54% was derived from the Chinese market. These figures suggest that sanctions against ZTE would not significantly harm major U.S. companies; rather, given China’s substantial procurement of U.S. chips, a comprehensive ban on chip exports would have a profound impact on the U.S. semiconductor industry.

3. Low Overlap Between Communication Chips and AI Chips

The chips that the U.S. has banned from sale to ZTE have low overlap with those used for AI applications.

The primary chips used by AI companies are GPUs, CPUs, and FPGAs. Although these are also imported from the United States, they do not overlap with the types of chips used by ZTE. Therefore, in terms of the scope of the chip sales ban, the impact on AI companies is virtually negligible.

FPGAs Will Be the Key Focus for Chip Development in the AI Sector

Although a comprehensive ban on chip sales in the United States is unlikely, the reliance on foreign-controlled core technologies has left Chinese people feeling deeply ashamed and helpless in the wake of the “ZTE incident.” During this period, it has become evident that independent research and development of chips has emerged as a critical trend for the next stage of growth among medical AI enterprises. In addition to dedicated chip design firms, medical AI companies such as Infervision and Xishi Heterogeneous Computing have also begun to venture into chip research.

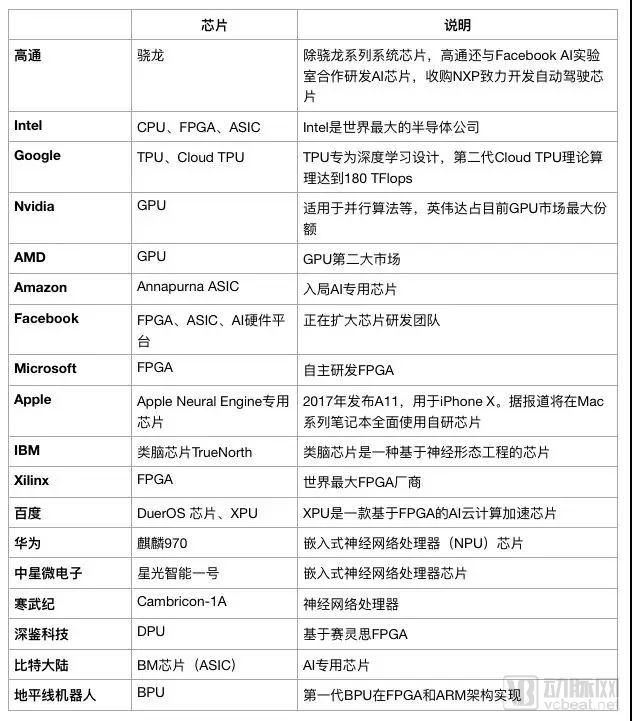

According to the 2017 report “A Comprehensive Analysis of the Development of the Artificial Intelligence Industry in China and the United States” published by Tencent Research Institute, there are 33 chip companies at the foundational layer in the United States, compared with 12 in China. The U.S. is home not only to tech giants such as Google, Intel, and IBM, but also to chip industry leaders like Qualcomm, NVIDIA, AMD, and Xilinx, along with numerous well-performing mid-sized companies and vibrant startups.

Among the chips used by medical AI companies, GPUs and CPUs are primarily employed for deep learning algorithms. In terms of chip architecture, patents, and ecosystem, these two domains are firmly controlled by NVIDIA and Intel, leaving no viable opportunity for new entrants; indeed, the United States holds a complete monopoly. Consequently, Chinese AI enterprises seeking to make significant strides are focusing their development efforts on FPGAs, ASICs, and neuromorphic chips, with the current landscape dominated mainly by small and medium-sized companies.

Image source: New Intelligence, with partial information from Tencent Research Institute

In the field of AI, FPGA chips are most likely to achieve breakthroughs in future chip R&D.

FPGA, which stands for Field-Programmable Gate Array in Chinese, is a type of semi-custom circuit in the field of application-specific integrated circuits (ASICs). It not only addresses the shortcomings of fully custom circuits but also overcomes the limitation of limited gate counts in traditional programmable logic devices. FPGAs are characterized by high performance, low power consumption, high flexibility, and hardware programmability.

If CPUs and GPUs achieve "generality" at the architecture level, then FPGAs achieve "generality" at a lower, circuit level. By programming an FPGA using hardware description languages, it can emulate the architecture of any type of chip, including those of CPUs and GPUs. Baidu’s machine learning hardware system leverages FPGAs to create AI-specific chips, forming the FPGA-based version of Baidu Brain. This has been progressively deployed at scale across Baidu’s products, including applications such as speech recognition and ad click-through rate prediction models.

Chen Hui, CEO of Yasen Technology, explained to VCBeat that FPGAs eliminate the concept of memory, enabling highly efficient transmission of large volumes of data by allowing direct transfer from one unit to another without caching in main memory. This makes them particularly suitable for algorithms with high real-time requirements. Therefore, the integration of FPGAs and AI algorithms will become a major focus of future R&D. Currently, several companies in China, including Deephi Technology, Shenzhen Unigroup, Shanghai Anlogic, and Horizon Robotics, are engaged in FPGA-related research.

Notably, the FPGA sector features high industry barriers, with nearly 9,000 patents forming a substantial intellectual property moat. Even Intel found itself at a disadvantage, ultimately acquiring Altera for $16.7 billion to secure its entry into the FPGA market.

According to Chen Kuan, CEO of Infervision, if China mobilizes its nationwide resources for chip research, it is capable of producing high-quality chips. However, the industrial barriers in the semiconductor sector are extremely high; even with a grasp of fundamental theories, extensive long-term research is required in chip design and industrial packaging. Since its founding in 1968, Intel has taken many years of development to achieve its current success, while China still faces significant shortcomings in chip manufacturing.

Ding Xiaowei, founder of VoxelCloud, stated that the chip technology gap between China and the United States has long existed and has been a continuous topic of discussion within the industry; the ZTE incident merely intensified this issue. However, although there is a disparity between China and the U.S. in the chip sector, Chinese medical AI companies possess their own core technologies in applications and AI capabilities. Both countries have their respective strengths, but their operational processes and methodologies differ, particularly in how they define medical problems and integrate with clinical practice. A rational perspective on the ZTE incident is essential. Chip research and development require continuous trial and error and long-term accumulation. It is crucial to improve the R&D environment and sustain investment to retain talent, rather than pursuing short-lived hype.

China’s Chip Development Requires Joint Efforts from BAT and Startups

China’s Chip Pain: A Growing Emphasis on Core Technologies. The chip industry features high technical barriers, long R&D cycles, and stringent requirements for capital and talent.

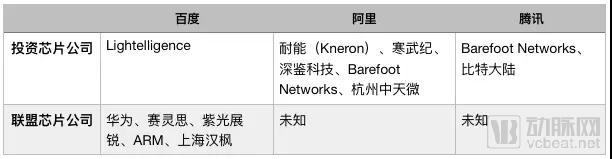

In recent days, news of Alibaba’s acquisition of C-Sky Microsystems has dominated headlines. Many believe that tech giants with deep pockets and a strong commitment to AI development—such as BAT (Baidu, Alibaba, and Tencent) and Huawei—should assume the role of saviors for the AI chip industry. While this perspective holds some merit, the development of China’s AI chip sector requires not only leading enterprises like BAT and Huawei but also concerted efforts from startups.

On the one hand, BAT possesses strong R&D capabilities and demand, having strategically positioned itself in this area well in advance.

In March 2017, Tencent Cloud announced the establishment of a comprehensive AI infrastructure computing platform featuring cloud servers equipped with FPGAs, GPUs, and 25G network interface cards (NICs). It also unveiled a series of technological and ecosystem deployments, including the launch of FPGA-based cloud servers with four cards per instance and GPU-based cloud servers with eight cards per instance. Additionally, 25G NICs were to be deployed on both FPGA- and GPU-based cloud servers, providing the network infrastructure for subsequent GPU and FPGA clusters.

In August 2017, Baidu collaborated with Xilinx to release the XPU at the Hot Chips conference in the United States. The XPU is a 256-core, FPGA-based cloud computing acceleration chip. Baidu also launched the DuerOS smart chip, which integrates Unisoc’s RDA5981 chipset and adopts ARM’s mbed OS kernel along with its secure network protocol stack.

BAT’s investments will help alleviate part of China’s AI chip dilemma in the future.

Image source: New Zhiyuan

On the other hand, we cannot overlook the strength of startups; BAT often expands its strategic footprint by acquiring such companies. Startups in the AI chip sector boast more specialized teams and possess a deeper understanding of the field, as exemplified by companies like Cambricon and Unisoc.

Cambricon is a renowned AI chip developer in China and the world’s first AI chip company to successfully achieve tape-out and deliver mature products. It offers two product lines: terminal AI processor IP and high-performance cloud AI chips.

The Cambricon-1A processor, released in 2016, is the world’s first commercial deep-learning-specific processor. The Cambricon team originated from the Institute of Computing Technology (ICT) of the Chinese Academy of Sciences, which is China’s first national academic institution dedicated to comprehensive research in computer science and technology. A number of high-tech enterprises, such as Lenovo and Sugon, were spun off from this institute, which also serves as a key shareholder of Cambricon Technologies and a long-term partner in industry-academia-research collaboration.

In August 2017, Cambricon Technologies completed a $100 million Series A financing round, jointly invested by SDIC Innovation, Alibaba Entrepreneurs Fund, Lenovo Venture Capital, Guoke Investment, Zhongke Turing, Yuanhe Origin, and Yonghua Investment. Following this round of financing, the company joined the ranks of unicorns.

VCBeat has interviewed numerous medical AI institutions, and when selecting customized AI chips, they prioritize Cambricon’s products.

In the FPGA industry, Shenzhen Pango Microelectronics, a member of China’s “national team,” has also established a strong presence. Founded in 2013, the company is a subsidiary of the listed firm Unigroup Guoxin Microelectronics Co., Ltd.

In November 2017, Unigroup Guoxin Microelectronics increased its capital injection into Unigroup Guochuang, establishing a Chengdu R&D center with a total investment of approximately RMB 597 million to advance the development of FPGAs and corresponding EDA tools. Unigroup PGTech claims on its website to have developed China’s first high-performance FPGA with independent intellectual property rights featuring ten-million-gate capacity.

Another startup, Shanghai Anlogic Inc., has a core team hailing from Lattice Semiconductor, one of the "Big Four" FPGA manufacturers. Currently, Shanghai Anlogic Inc. has completed its Series C financing, with investors including Huada Semiconductor, Hangzhou Silan Microelectronics, and Shanghai Technology Venture Capital Co., Ltd., the integrated circuit fund of the Shanghai Municipal Government.

It can be said that BAT has the capital and demand, while startups have the technology, industry knowledge, and experience. Only through collaboration between both parties can the development of the chip industry be accelerated.

Finally, we extend our sincere gratitude to Ding Xiaowei, CEO of VoxelCloud; Ding Xiaocheng, CTO of Wofang Technology; Chen Hui, CEO of Yasen Technology; Song Jie, CEO of Xishi Heterogeneous Computing; Chen Kuan, CEO of Infervision; and Li Yiming, CTO of Deepwise Medical, for their strong support of this article.