Competitiveness Report on Pharmaceutical E-commerce: How YiyaoGo, AliHealth, and Jianke Are Pioneering Pharma E-commerce 2.0

AliHealth

Medical and Health Services Network Service Provider

Preface

Pharmaceutical e-commerce 1.0 refers to a pure online drug sales service model, which utilizes internet information technology to build platforms that provide drug transaction services for pharmaceutical suppliers, distributors, retailers, and individuals. This model features singular service formats, low added value, and limited value creation for users. Pharmaceutical e-commerce 2.0 transforms from a mere drug sales service provider into an entity that, based on drug sales services, extends into a series of value-added services such as SaaS, financial services, diagnosis and treatment services, and health management services, thereby constructing an industrial ecosystem for pharmaceutical circulation and a closed-loop “medical + pharmaceutical” healthcare service ecosystem.

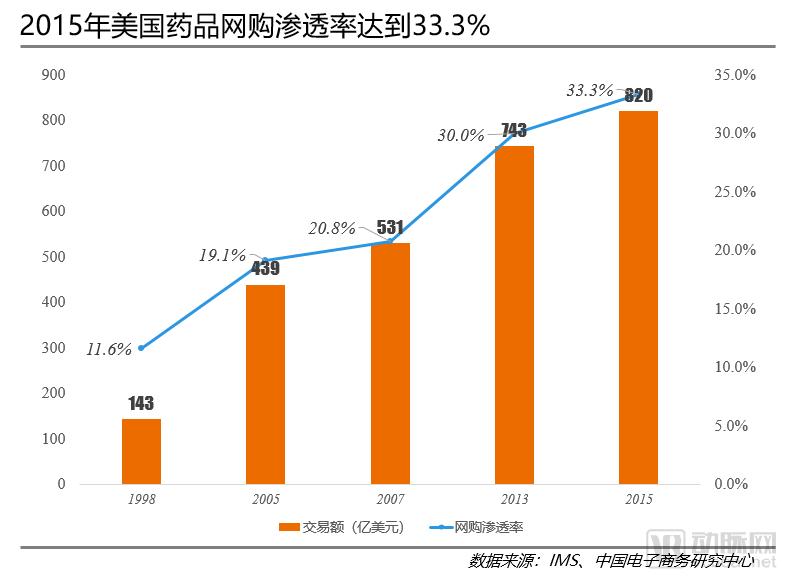

Currently, the online drug purchase penetration rate in China stands at 7.4%, whereas it has reached 33.3% in the United States, indicating substantial growth potential for China’s pharmaceutical e-commerce market. Moreover, the gradual implementation of the separation of prescribing and dispensing, the outflow of prescriptions from hospitals, and the anticipated lifting of bans on online sales of prescription drugs will create new growth drivers for pharmaceutical e-commerce.

From the perspective of the development history of pharmaceutical e-commerce in China, the industry has entered a growth stage. Major e-commerce platforms vary significantly in terms of drug sales scale, financing capability, supply chain integration capacity, and value-added service capabilities. Enterprises should seize the opportunities presented by the rapid expansion of the e-commerce market, adapt to this trend for transformation, and enhance their comprehensive competitiveness by providing diversified services beyond basic drug sales. B2B pharmaceutical e-commerce integrates upstream and downstream resources, streamlining the links of drug supply, distribution, and procurement. B2C pharmaceutical e-commerce is focusing on online diagnosis and treatment, health management, and medical insurance, providing patients with an integrated service covering consultation, medication, and reimbursement.

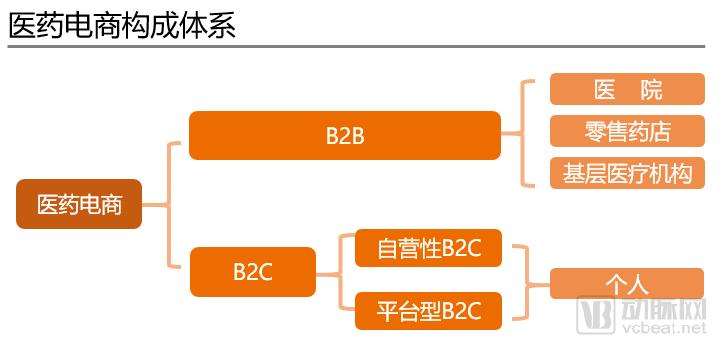

China’s pharmaceutical e-commerce sector primarily consists of B2B and B2C platforms. B2B pharmaceutical e-commerce platforms mainly serve institutional clients, with purchasers including hospitals, primary healthcare institutions, and retail pharmacies. B2C pharmaceutical e-commerce platforms primarily provide medication purchasing services to individual consumers. Based on whether the operations are self-run, B2C models are further divided into marketplace-based B2C and self-operated B2C. The former resembles the Taobao model, where various pharmaceutical merchants are onboarded onto the platform, which provides services such as product display, transaction facilitation, IT support, and data analytics. The latter involves procuring medications independently and selling them through a self-built platform.

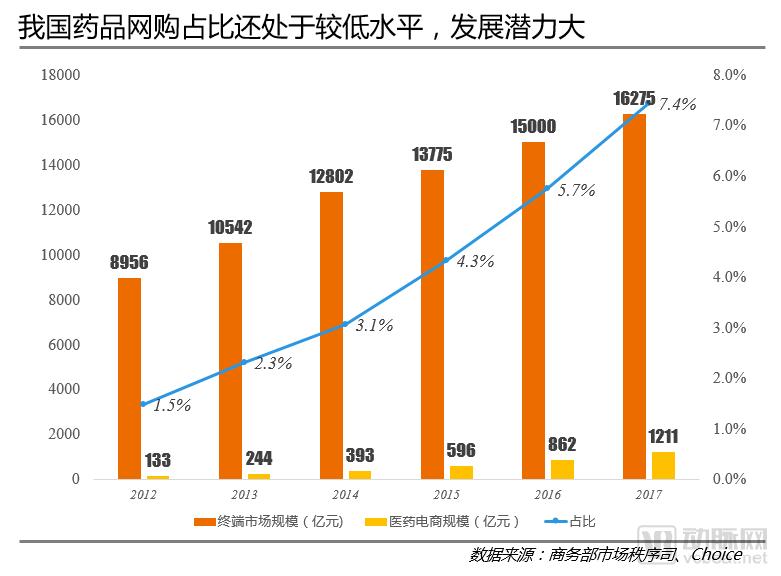

By the end of 2017, the market size of China’s pharmaceutical sales terminals had reached RMB 1.6 trillion, with a compound annual growth rate (CAGR) of 12.6% over the previous five years, demonstrating a trend of rapid expansion. However, during the same period, the market size of China’s pharmaceutical e-commerce sector was only RMB 121.1 billion, accounting for 7.4% of the total pharmaceutical sales terminal market, indicating substantial room for future growth.

This report aims to present how enterprises can innovate their business models in the era of Pharmaceutical E-commerce 2.0, transforming from mere drug sales service providers into builders of a pharmaceutical distribution industrial ecosystem and a closed-loop healthcare service ecosystem. It achieves this by examining the development of pharmaceutical e-commerce in China and the United States, the characteristics of China’s developmental stages, the current status of B2B and B2C pharmaceutical e-commerce markets, and case studies of corporate transformations.

China’s Online Drug Penetration Rate Boasts a CAGR of 37.6%, Indicating Huge Market Potential

Compared with developed countries such as the United States, China's pharmaceutical e-commerce sector started relatively late, and its share in the overall pharmaceutical retail market remains low.

An examination of the U.S. pharmaceutical e-commerce market reveals that its penetration rate exceeded 10% as early as 1998 and has since maintained a high growth trajectory. In 2015, the transaction volume of pharmaceutical e-commerce reached $82 billion, accounting for 33.3% of the total U.S. pharmaceutical sales market, which underscores the widespread adoption of online pharmaceutical retail in the United States. In contrast, while the share of online pharmaceutical purchases in China has been steadily increasing, with a compound annual growth rate (CAGR) of 37.6% over the past six years, the proportion of pharmaceuticals sold online remains below 10%, indicating significant potential for future expansion.

A comparison of the pharmaceutical e-commerce markets in China and the United States reveals that China’s sector remains at a relatively nascent stage, indicating substantial potential for market growth. The primary driver of this disparity between the two markets lies in the differences in their pharmaceutical regulatory systems.

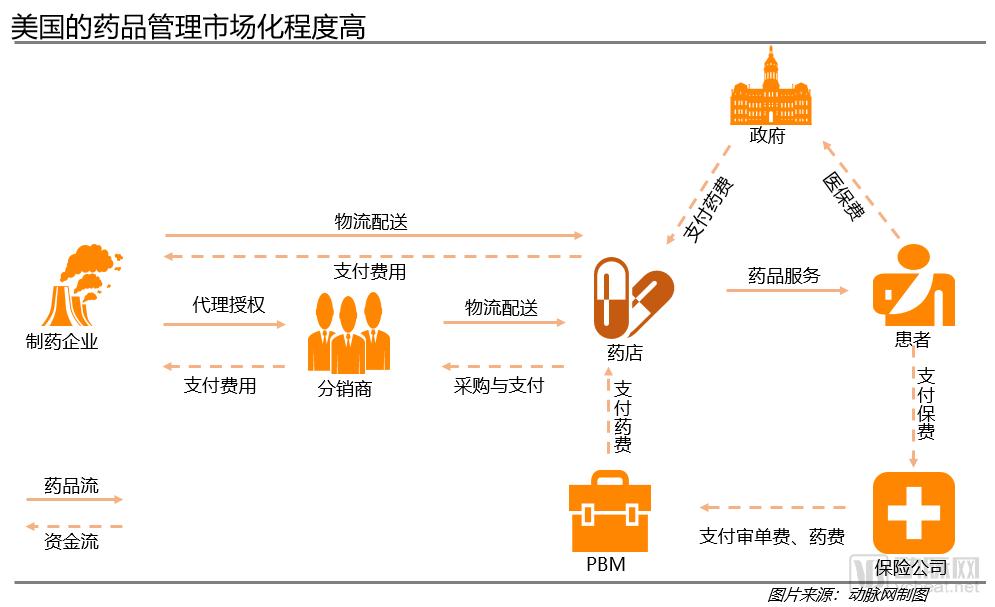

The U.S. pharmaceutical market is highly commercialized, with prescription drugs fully subject to market forces. Pharmaceutical manufacturers, distributors, pharmacy benefit managers (PBMs), and insurance companies play dominant roles in drug supply and management. The U.S. has a well-developed commercial health insurance system; patients can access drug reimbursement services simply by paying premiums to insurance providers. Meanwhile, government-sponsored basic health insurance also covers a portion of patients’ medication costs. Notably, the widespread presence of PBM organizations plays an irreplaceable role in the overall U.S. pharmaceutical management system. As specialized third-party entities independent of pharmaceutical manufacturers, distributors, healthcare providers, and the government, PBMs negotiate contracts with drug companies, healthcare institutions, and insurers to control medication costs without compromising the quality of medical care.

In addition to the pharmaceutical regulatory system, the United States’ comprehensive health insurance system is also a major driver behind the development of the U.S. online pharmaceutical e-commerce sector. American citizens can use health insurance to pay for both online and offline medication purchases. Notably, in 2010, former U.S. President Barack Obama signed into law the Patient Protection and Affordable Care Act (PPACA). Led by the U.S. government, this legislation aims to expand health insurance coverage among the American population and reduce healthcare costs. The Act allows individuals and small businesses to purchase health insurance for themselves, their families, and their employees through government-run health insurance marketplaces, while providing subsidies for insurance premiums to low- and middle-income individuals and families, thereby ensuring that every citizen has access to government-backed healthcare coverage. The enactment of the Affordable Care Act signifies enhanced reimbursement protection for residents’ medication expenditures.

Currently, China's pharmaceutical e-commerce sector remains at a relatively low level, primarily due to the following three reasons:

(1) Drug administration in China is primarily government-led, with strict governmental controls over the production, distribution, and consumption of pharmaceuticals. Public medical institutions account for more than 70% of drug procurement, and drug consumption is mainly realized through patients obtaining medications during hospital visits. Meanwhile, policies prohibit the online sale of prescription drugs to individuals; given that prescription drugs constitute approximately 85% of the total pharmaceutical market size, this restriction significantly limits the sales scale of pharmaceutical e-commerce. Therefore, it is necessary to break administrative monopolies in drug administration and enhance the marketization level of the pharmaceutical industry.

(2) The imperfections in the medical insurance payment system, where online consumption cannot be paid for using medical insurance and the pooled fund of medical insurance cannot be used for retail payments. In the future, medical insurance payments need to include online drug purchases within the scope of reimbursement.

(3) Delivery time lag for pharmaceuticals: As online drug delivery requires time, patients with acute conditions tend to purchase medications from offline pharmacies. Improving the timeliness of drug delivery has become an urgent issue for pharmaceutical e-commerce platforms.

China's pharmaceutical e-commerce sector has entered a phase of rapid development, with the industrial landscape basically established.

Although there are constraints on the development of pharmaceutical e-commerce in China, the market size changes in recent years show that the compound annual growth rate (CAGR) of pharmaceutical e-commerce sales over the past six years has reached 55.5%, and the CAGR of the proportion of pharmaceutical e-commerce in the terminal drug market is as high as 37.6%. This indicates that China's pharmaceutical e-commerce has entered a stage of rapid development.

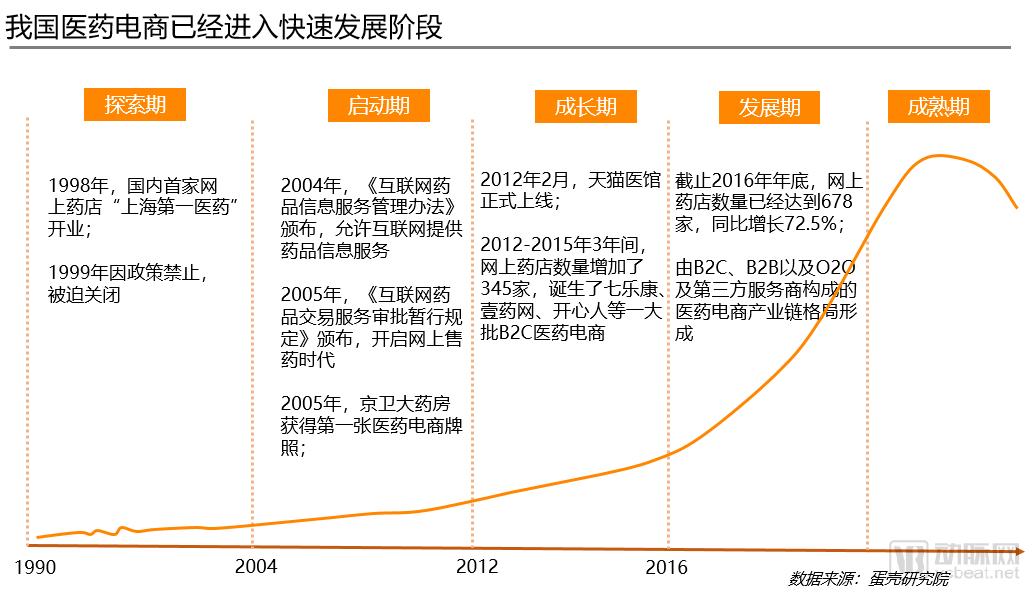

From the initial foray of the first online pharmacy to the present, China's pharmaceutical e-commerce sector has undergone three phases—exploration, initiation, and growth—and has now entered a period of accelerated development.

In 1998, before China had implemented any policies related to pharmaceutical e-commerce, the first online pharmacy, “Shanghai First Pharmacy,” emerged. However, on December 28, 1999, the China Food and Drug Administration (CFDA) issued the Interim Provisions on the Circulation Management of Prescription and Over-the-Counter Drugs, which prohibited the online sale of both prescription and over-the-counter drugs, forcing Shanghai First Pharmacy to shut down. For the next 14 years, no online pharmacies appeared in China.

On July 8, 2004, the China Food and Drug Administration (CFDA) promulgated the Measures for the Administration of Internet Drug Information Services, permitting enterprises that had obtained an “Internet Drug Information Service Qualification Certificate” to provide paid drug information and other services to online users via the internet. On September 29, 2005, the CFDA further issued the Interim Provisions on the Approval of Internet Drug Transaction Services, stipulating that drug retail enterprises could sell over-the-counter drugs online. The issuance of these two policies granted legal status to pharmaceutical e-commerce. Jingwei Pharmacy obtained the first pharmaceutical e-commerce license in China, marking the entry of pharmaceutical e-commerce into the drug retail sector. By 2012, there were a total of 48 online pharmacies in China.

In 2012, Tmall Pharmacy officially launched. As a professional pharmaceutical shopping channel under Tmall, it aggregated online shopping services for OTC drugs, medical devices, family planning products, contact lenses, branded health supplements, and traditional tonics, thereby establishing a standardized model for pharmaceutical e-commerce and providing a reference for the development of other players in the sector. In 2013, the number of online pharmacies surged to 134, representing a year-on-year increase of approximately threefold, and giving rise to a host of well-known pharmaceutical e-commerce platforms such as Qilekang, 111.com.cn, and Kaixinren. On May 28, 2014, the China Food and Drug Administration (CFDA) released the Administrative Measures for the Supervision of Online Food and Drug Operations (Draft for Comment), which permitted internet enterprises to sell prescription drugs against prescriptions in accordance with drug classification management regulations. The release of this draft spurred a large number of pharmaceutical companies to enter the e-commerce sector. Between 2012 and 2015, a total of 345 online pharmacies were established in China. Although the number of online pharmacies grew rapidly during this period, most lacked mature business models and remained in a phase of continuous exploration, indicating that China’s pharmaceutical e-commerce industry was still in its growth stage.

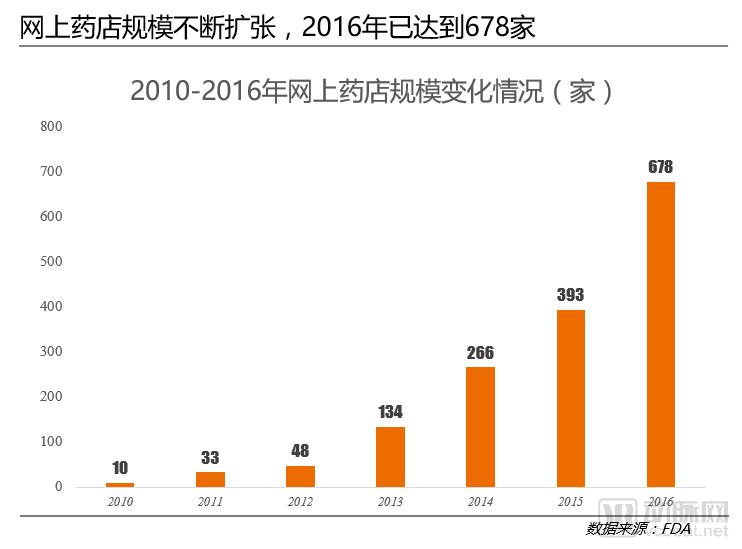

After experiencing the start-up and growth phases, the business models of pharmaceutical e-commerce enterprises had taken shape by 2016: the B2C model represented by 1 Drug Network (1 Yao Wang), Jianke, AliHealth Pharmacy, and JD Health Pharmacy; the B2B model represented by Yi Yao Gou, Jointown Pharmaceutical Network, My Medicine Network (Wo De Yi Yao Wang), Weiming Penguin, and Yaoshibang; and the O2O model represented by Kuai Fang Song Yao and Yao Dao Jia. The industrial landscape of China’s pharmaceutical e-commerce sector has been established, with a cohort of representative enterprises emerging in each respective niche. In 2016, the number of online pharmacies in China reached 678, a year-on-year increase of 72.5%, marking the entry of pharmaceutical e-commerce into a period of rapid development.

Currently, the industrial ecosystem of pharmaceutical e-commerce in China has basically taken shape. With operators at its core, it connects resource providers, third-party service providers, and users externally, integrating the production, distribution, payment, and consumption links of pharmaceuticals. Meanwhile, during this period, the government has introduced a series of policies to promote the development of pharmaceutical e-commerce.

From the perspective of policy content, the government strongly supports the development of pharmaceutical e-commerce. In particular, following the cancellation of the B and C licenses for online transaction qualifications, the A license was also abolished. This signifies that China’s pharmaceutical e-commerce sector has transitioned from an approval-based system to a filing-based system, thereby lowering the entry barriers.

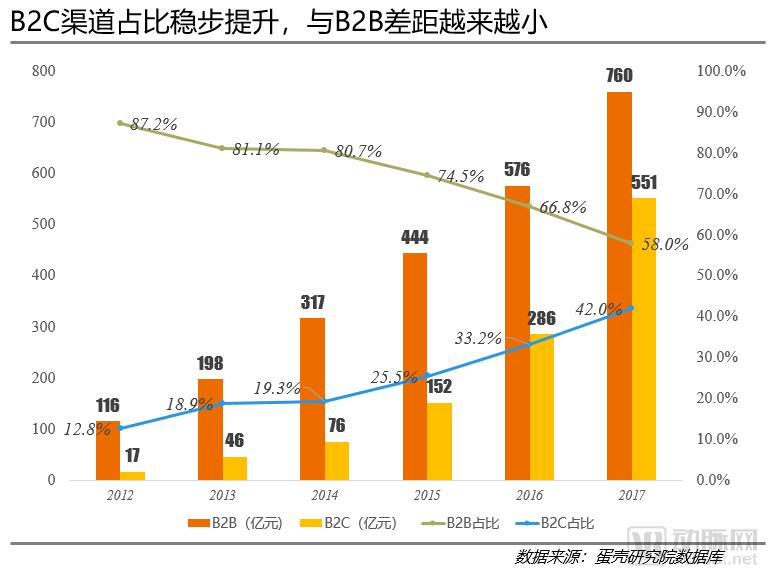

China's e-commerce market primarily comprises two types of platforms: B2B and B2C. The B2B segment holds an absolute dominant share, accounting for over 50% of the market in each of the past six years. This dominance is largely driven by bulk procurement from B-side customers, mainly consisting of hospitals, primary healthcare institutions, and retail pharmacies. However, in terms of market share distribution, the proportion of B2C has been increasing year by year, while that of B2B has been declining, resulting in a narrowing gap between the two.

Evaluation of the Competitiveness of China's Pharmaceutical E-commerce: Yi Yao Gou and 111.com Emerge as the Most Comprehensive Leaders

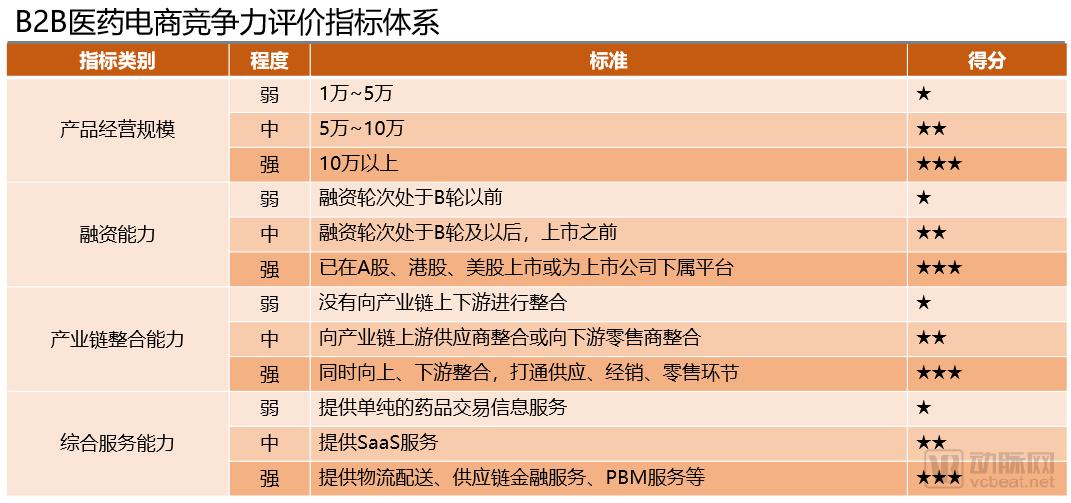

To better illustrate the development status of major pharmaceutical e-commerce platforms, VCBeat Institute selects four dimensions—product operation scale, financing capability, industrial chain integration capability, and comprehensive service capability—as components of competitiveness to evaluate mainstream B2B pharmaceutical e-commerce platforms. For B2C pharmaceutical e-commerce platforms, it selects four dimensions—product operation scale, financing capability, diagnosis and treatment service capability, and additional service capability—as components of competitiveness for evaluation.

Product Business Scale: The scale of product operations is primarily reflected by the variety of pharmaceutical products listed on major e-commerce platforms (different specifications of the same drug are counted as one category). A greater variety of pharmaceutical products indicates a larger business scale, covering a wider range of diseases and patient populations.

Financing Capability: The strength of a company’s financing capability reflects the recognition by capital markets or investment institutions of an e-commerce enterprise’s growth prospects; later-stage financing rounds indicate stronger corporate development.

Supply Chain Integration Capability: As enterprises reach a certain stage of development, they expand upstream and downstream along the supply chain to integrate resources, thereby enhancing their bargaining power with suppliers and control over downstream retailers.

Comprehensive Service Capabilities: Building upon the provision of drug transaction information services, pharmaceutical e-commerce platforms offer value-added services such as SaaS solutions, logistics and distribution, and supply chain finance. These services deliver higher value to suppliers and retailers, thereby enhancing the platform’s appeal to customers.

VCBeat evaluated the competitiveness of 10 B2B pharmaceutical e-commerce platforms by collecting and organizing relevant data on major players in the sector. The top five were Yiyao Gou, Jointown Pharmaceutical Network, My Medicine Network, Yaojingcai, and Putian Pharmaceutical & Medical Device Network.

Data Source: VCBeat

(1) YiYaoGou

Product Portfolio Scale ★★: Over 60,200 items

Financing Capability ★★★: Shanghai Pharmaceutical Zhongxie Pharmaceutical Co., Ltd. is a subsidiary of Shanghai Pharmaceuticals, which is listed on both the Shanghai Stock Exchange and the Hong Kong Stock Exchange.

Supply Chain Integration Capability ★★★: ① Supply Side: Shanghai Pharmaceutical has established manufacturing bases in eight provinces and municipalities across China, as well as overseas. These include specialized active pharmaceutical ingredient (API) bases, modern traditional Chinese medicine (TCM) production bases, high-quality chemical formulation factories, and health supplement production facilities. The company consistently produces over 800 drug varieties in more than 20 dosage forms, ensuring drug supply for Yiyaogou. ② Procurement Side: Shanghai Pharmaceutical operates more than 1,800 retail pharmacies across 16 provinces, autonomous regions, and municipalities nationwide. Its subsidiary, Shanghai Huashi Pharmacy, is the largest pharmaceutical retailer in East China by number of stores. These retail outlets procure products through the Yiyaogou platform.

Comprehensive Service Capability ★★★: Shanghai Pharma established Shanghai Pharmaceutical Logistics Center Co., Ltd., which offers diverse storage conditions suitable for various pharmaceuticals and medical devices. Its distribution network covers Shanghai, the East China region, and 13 provinces across China, reaching 1,200 county-level cities, 3,000 commercial companies, 8,000 hospitals, and 10,000 pharmacies. It provides pharmaceutical distribution services for Yi Yao Gou.

(2) Jointown Network

Product Portfolio Scale ★★★: Over 472,800 SKUs

Financing Capability ★★★: Jointown Pharmaceutical Group listed on the Shanghai Stock Exchange on November 2, 2010. With a current total market capitalization of RMB 34 billion, it ranks among the top 10 pharmaceutical commercial enterprises in China.

Supply Chain Integration Capability ★★★: ① Supply Side: Jointown Pharmaceutical Group owns several drug R&D and manufacturing subsidiaries, including Beijing Jingfeng Pharmaceutical Group Co., Ltd. and Jointown Tianrun Traditional Chinese Medicine Industry Co., Ltd. These entities engage in the R&D and production of dozens of traditional Chinese and Western medicine varieties, serving as pharmaceutical suppliers for Jointown’s online platform and other e-commerce platforms. ② Procurement Side: Beijing Haoyaoshi Pharmacy Chain Co., Ltd., a wholly-owned subsidiary of Jointown Pharmaceutical Group, currently collaborates with over 100,000 pharmacies. These pharmacies are directly connected to Jointown’s online platform, making it their primary procurement channel. Thus, Jointown Pharmaceutical Group has successfully integrated the pharmaceutical production, distribution, and retail segments for its online platform.

Comprehensive Service Capability ★★: Jointown.com provides pharmaceutical purchasers on its platform with informatization system construction, including database development, procurement management, and warehouse management, to enhance enterprise management and operational efficiency.

(3) My Medicine Network

Product Portfolio Scale ★★★: Over 11,200 SKUs

Financing Capability ★★: Completed Series C1 financing, with total funding from previous rounds nearing RMB 1 billion.

Supply Chain Integration Capability ★★: Initiated the establishment of the Healthcare Industry Innovation Alliance, comprising pharmaceutical manufacturers, medical institutions, and financial institutions. This alliance connects the pharmaceutical industry, medical institutions, chain pharmacies, and patients, enabling direct procurement for pharmacy supply chains, virtual inventory management for pharmacies, physician consultations at pharmacy locations, electronic prescription circulation to pharmacies, direct purchase of prescription and over-the-counter drugs at pharmacies, and patient management.

Comprehensive Service Capability ★★★: The company’s independently developed “Feijia Cloud” cloud-based pharmaceutical management system provides retailers with foundational data infrastructure, procurement management, warehouse management, sales management, and quality management, comprehensively enhancing operational efficiency. Meanwhile, the company has launched “Yao Jin Rong,” a supply chain finance product line that offers tailored solutions such as “Bang Ni Fu” (Pay-for-You) and equity pledge loans based on retailers’ varying conditions, thereby addressing challenges in pharmaceutical procurement.

(4) Yaojingcai

Product Portfolio Scale ★: Over 25,000 SKUs

Financing Capability ★★★: JD.com is a publicly listed company on the U.S. stock market.

Supply Chain Integration Capability ★: Yaojingcai has not yet completed the integration of its upstream and downstream supply chain, but it will gradually streamline the pharmaceutical supply, sales, and procurement processes by leveraging JD Group’s supply chain advantages in the future.

Comprehensive Service Capability ★★★: Launched "Yao Baitiao," offering "Baitiao" financial services to purchasers with a maximum credit limit of RMB 500,000 and interest-free repayment within 30 days. Additionally, it leverages JD.com’s proprietary logistics network to provide pharmaceutical distribution services for the Yaojingcai platform.

(5) Putian Pharmaceutical and Medical Device Network

Product Portfolio Scale ★★★: Over 201,300 SKUs

Financing Capability ★: The platform is currently at a pre-Series B financing stage.

Industry Chain Integration Capability ★: The company has not yet completed the integration of upstream and downstream resources in the industry chain.

Comprehensive Service Capability ★★★: The company has partnered with Shenzhen Jiumingzhu Information Technology Co., Ltd., a standardized developer and provider of healthcare IT software and services, to deliver medical imaging management systems, electronic medical record (EMR) management systems, and hospital information management systems to hospitals. Additionally, the company has developed Putianbao, a payment and settlement product that provides online payment services to platform users. Premium members on the platform can also apply for supply chain finance services, including contracted payments, installment plans, and financial leasing.

Product Business Scale: The product business scale is primarily reflected by the variety of pharmaceutical products displayed on major e-commerce platforms (different specifications of the same drug are counted as one category). A greater variety of pharmaceutical products indicates a larger business scale, covering a wider range of diseases and patient populations.

Financing Capability: The strength of a company's financing capability reflects the recognition by the capital market or investment institutions of the development prospects of e-commerce enterprises. A later financing round indicates better corporate development.

Diagnostic and Treatment Service Capabilities: The more services provided online by pharmaceutical e-commerce platforms, the greater the convenience for patients. Pharmacist consultations, which primarily address medication purchase inquiries, have become a basic service offered by major B2C pharmaceutical e-commerce platforms. Online registration and doctor appointment services mainly aim to resolve issues such as long waiting times for pre-consultation registration and the difficulty of securing appointments with specialists; some B2C pharmaceutical e-commerce platforms have introduced these services. Online consultation and prescription services primarily address healthcare needs, but only a few B2C e-commerce providers are capable of offering this service.

Additional Service Capabilities: Medication delivery, as a complementary service for online pharmaceutical purchases, is offered by major e-commerce platforms. Chronic disease management, health check-ups, and health insurance services, as extended offerings, are achievable only by a select few B2C e-commerce players. Establishing proprietary or joint-venture hospitals to integrate “medical care + pharmaceuticals” and address both diagnosis/treatment and medication procurement needs is feasible for only a very small number of B2C e-commerce companies, with the majority still in the exploratory and planning stages.

VCBeat compiled and analyzed data on major B2C pharmaceutical e-commerce platforms to evaluate the competitiveness of 15 such companies, with 111.com.cn, Jianke, Haoyaoshi, Qilekang, and AliHealth Pharmacy ranking in the top five.

Data source: VCBeat

The remaining content of this report:

I. Details of Competitiveness Evaluation for B2C Pharmaceutical E-commerce

II. An Analysis of the Business Models of U.S. Pharmaceutical Distributors: AmerisourceBergen and Walgreens Build a New Model for the Pharmaceutical Commerce Industry

III. The Future Development of China’s Pharmaceutical E-commerce: Pharma E-commerce 2.0 Becomes the Mainstream, with Prescription Drugs and Online Medical Insurance Reimbursement Creating New Growth Points

Scan the QR code to join VCBeat membership

NowLong-press to RecognizeScan the QR code above to become an official VCBeat member and gain access to the full version of the "Report on Competitiveness in the Pharmaceutical E-commerce Industry." Additionally, over the coming year, you will enjoy unrestricted access to completeIndustry Trends Report, stay abreast of the latest globalInvestment and Financing Information, boasting a comprehensive range ofMedical Enterprise Database,And the seaFacilitating the connection of high-quality resources.

*Special thanks to Feng Shaohua, Manager of Government Affairs at Rongguan E-commerce; Zhao Xue, Pharmaceutical Industry Analyst; and Zou Xiaoliang, Founder of Weiming Penguin, for their strong support of this report.

References:

"Annual Report on the Development of China's Pharmaceutical Distribution Industry (2017)" (Social Sciences Academic Press)

“E-Commerce in Pharmaceuticals: Policy ‘Emergency Brake’ on Online Sales of Prescription Drugs, Rise of the ‘E-Commerce + Healthcare’ Model, and Prescription Outflow as a New Growth Point [2017 Year-End Review]” (VCBeat)

“Most Comprehensive Scan of the B2B Pharmaceutical E-Commerce Industry: A Full Overview of Policy Evolution, Market Status, and Development Trends” (VCBeat)