Medical Unicorn Exits via Acquisition: Biopharma Dominates with Record $7B Deal

In 2013, Aileen Lee, an investor at Cowboy Ventures in the United States, coined the term “unicorn” to collectively refer to startup companies that had been established for no more than 10 years and were valued at over $1 billion by investors or valuation firms. Thus, the term “unicorn” originated in the United States and gradually gained global prominence.

Following Meituan’s acquisition of Mobike, the unicorn in the mobility sector, heated debates have erupted in the capital markets: Is an acquisition ultimately a “harvest” or a way to “lock in profits”? And is it truly as Mobike CEO Hu Weiwei stated, “You must repay capital’s support twofold in the future”?

Indeed, the growth of unicorn companies is inseparable from capital operations. In investment, it is not only important to focus on how to enter a project; for venture capital funds, what is more crucial is how to exit. The exit mechanism is key for venture capital funds to mitigate risks, recover investments, and generate returns.

As China’s A-share market continues to open up, an initial public offering (IPO) has seemingly become the ultimate goal for healthcare unicorns. Due to the high return on investment, an IPO also represents the most ideal exit strategy for investors. However, whether domestically or internationally, going public places significant demands on a company’s sustained profitability and financial strength.

According to VCBeat’s statistics on corporate valuations for IPOs across various exchanges, companies listed on overseas markets such as the NYSE and Nasdaq have demonstrated mid-range valuation performance. High-valued unicorns, in contrast, have become investment targets that evoke mixed feelings among investors. Compared with the IPO boom of 2013 and 2014, returns on investment for VC/PE firms have correspondingly declined. Consequently, exit strategies have shifted from solely betting on IPOs to a diversified approach that includes mergers and acquisitions, equity buybacks, and other methods.

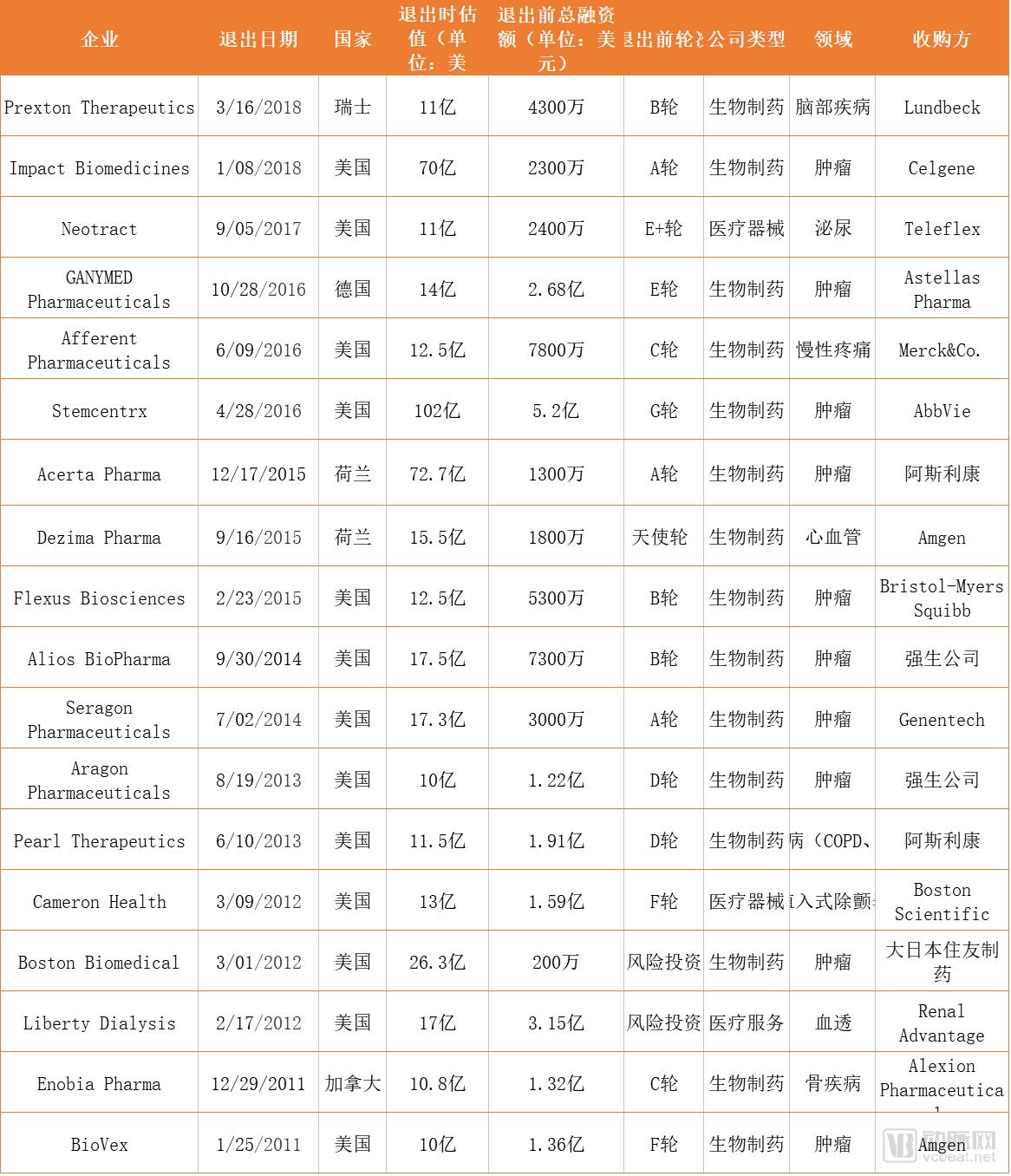

According to CB Insights’ Unicorn Database, 19 healthcare unicorns exited via mergers and acquisitions (M&A) between 2010 and 2018. What are the distinctive characteristics of these companies? VCBeat has compiled and analyzed the data to explore the underlying logic behind M&A exits in the healthcare unicorn sector.

According to data from the Unicorn Tracker, a total of 32 companies in the healthcare sector have exited since 2009 through various means, including initial public offerings (IPOs) and acquisitions. Among them, 11 companies exited via IPOs, with a combined valuation of $16.93 billion, while 18 companies exited through acquisitions, reaching a total valuation of $47.54 billion at the time of exit.

Based on the above data, IPOs and M&A have become the mainstream exit strategies for capital and enterprises.

Data indicates that companies choosing to list on the NASDAQ incur average costs exceeding $1 million, with total listing expenses accounting for 8% to 25% of the capital raised. These costs primarily include promotional expenses, legal fees, audit fees, financial advisory fees, underwriting fees, and direct listing fees. The magnitude of listing expenses depends on company size, fundraising methods, and the amount of capital raised. Consequently, overseas unicorns do not shy away from mergers and acquisitions (M&A) as a faster exit strategy for liquidity, with individual transaction values often surpassing the proceeds from an initial public offering (IPO).

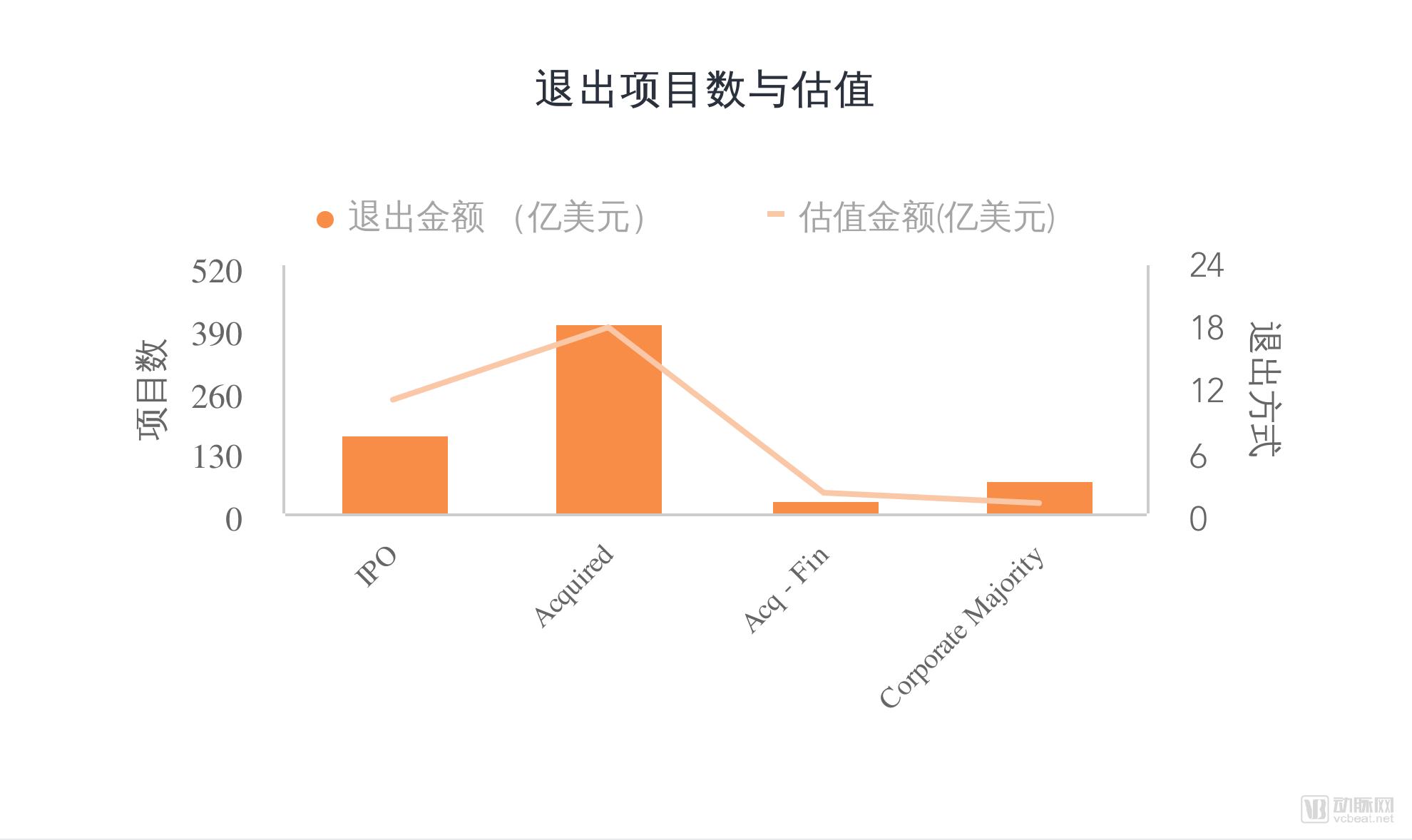

Unicorn Companies Exited via Acquisition in Recent Years (Data Source: CB Insights)

Industry Distribution of Companies (Data Source: CB Insights)

Given the extended liquidity cycle associated with initial public offerings (IPOs), which necessitates substantial ongoing capital investment from companies, mergers and acquisitions (M&A) have remained a central theme in the global life sciences and healthcare industry over the past two decades. Among the aforementioned unicorn M&A transactions, 15 deals were in the biopharmaceutical sector, accounting for 75% of the total, with a combined valuation reaching RMB 42.29 billion.

There were fewer companies in the medical device and healthcare service sectors, with three and one company respectively. Their valuations at exit were RMB 3.9 billion and RMB 1.7 billion, respectively.

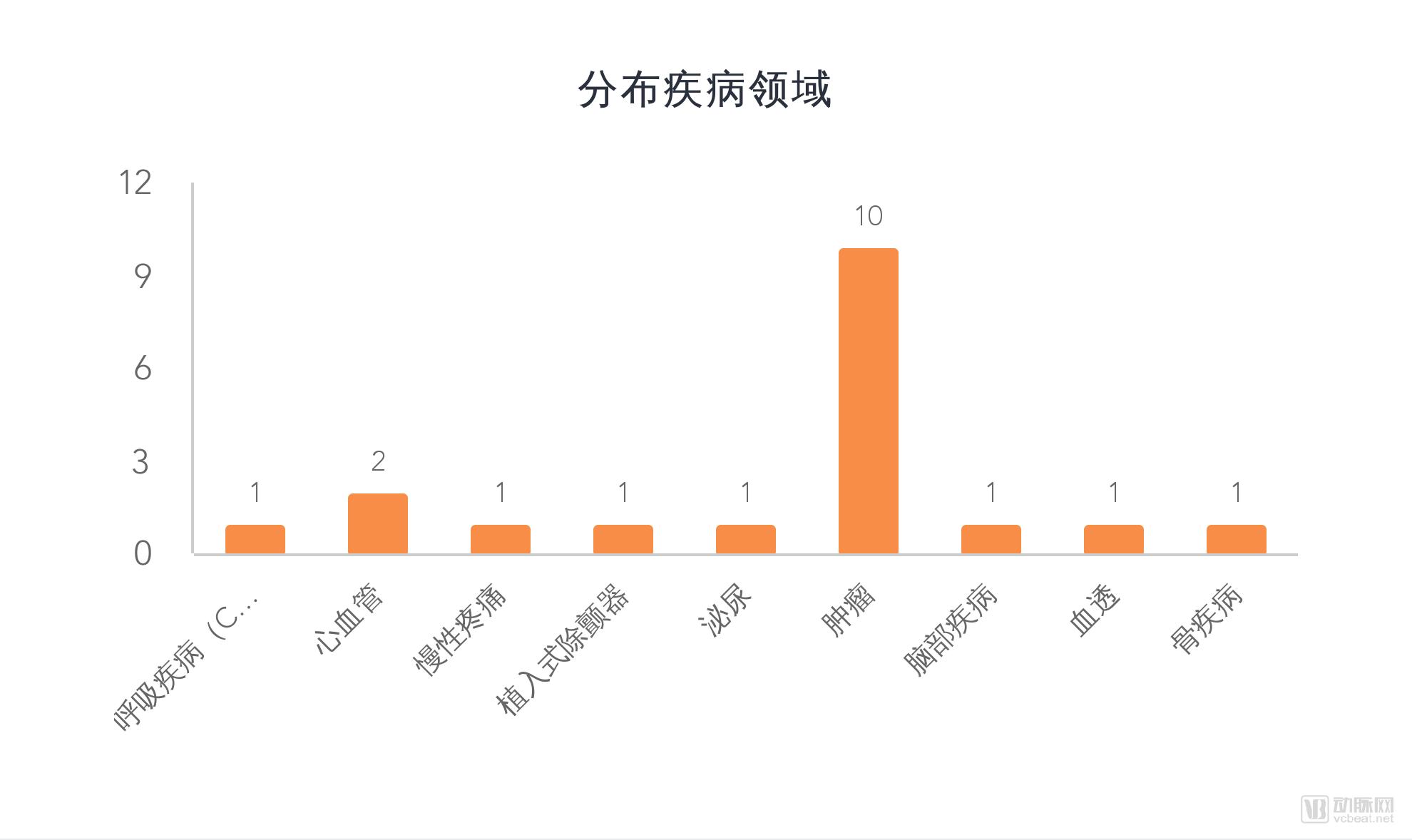

Distribution of Acquired and Exited Unicorn Companies by Disease Area (Data Source: CB Insights)

In terms of disease distribution, Liberty Dialysis, which provides medical services, operates in the hemodialysis sector, while Neotract, a medical device company, focuses on urological and gynecological surgical instruments. In the biopharmaceutical field, companies developing oncology products have led the way in terms of M&A activity. In fact, among healthcare companies choosing IPOs as an exit strategy, biopharmaceutical firms have also become the main force, with many betting on immunotherapy drugs.

This is because the industry is strongly technology-driven. Its high degree of specialization, significant industry barriers, and stringent entry thresholds contribute to a highly regulated market. Meanwhile, there is a substantial number of sub-segments targeting different indications, allowing investment institutions to execute corresponding exit strategies based on products developed for specific indications. Furthermore, the entire biopharmaceutical industry is subject to strict regulation and heavily influenced by policy. Capital can intervene at various stages and across different segments of the entire industrial chain, including pharmaceutical R&D, manufacturing, product sales and distribution, and downstream medical services.

In Silicon Valley Bank’s 2018 forecast on healthcare investment and financing trends, it was suggested that the biopharmaceutical sector would likely witness more than 20 large-scale M&A exit deals in 2018.

Upon examining the acquiring companies, we find that there were no cross-industry mergers and acquisitions in the aforementioned M&A events. Even Johnson & Johnson, a company with diversified businesses, had dedicated medical device R&D operations and its pharmaceutical subsidiary, Janssen, at the time of acquisition. Most unicorn enterprises were acquired by traditional biopharmaceutical giants that had gone public before the 1990s and employed more than 10,000 people.

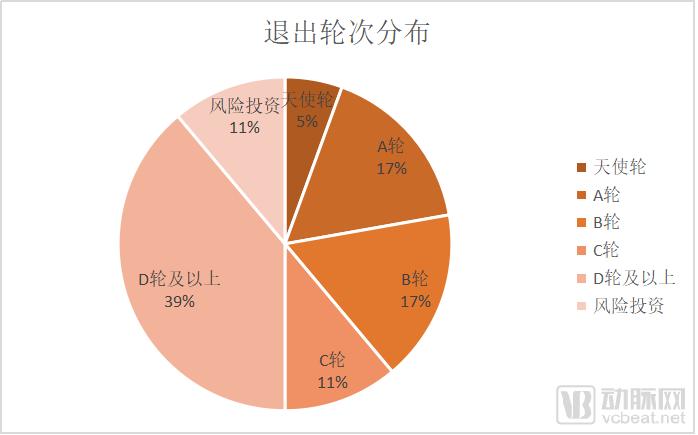

Distribution of Funding Rounds Prior to Acquisition (Source: CB Insights)

Biopharmaceuticals are characterized by "high investment, high risk, and high returns." Large companies tend to acquire firms with mature late-stage products already on the market, while biopharmaceutical companies require substantial capital investment in research and development.

According to reports from The Economic Observer on Chinese biopharmaceutical unicorns, clinical trials are a mandatory stage prior to drug approval and market launch. Phase III clinical trials, which involve the largest patient enrollment, are primarily designed to verify drug efficacy. This phase also represents the most capital-intensive stage before market entry, with costs varying by scale but typically ranging from tens of millions to several hundred million RMB. On average, bringing an innovative drug from research and development to market takes 12 years and costs $1 billion. For biosimilars, the average cost is $200 million. Consequently, companies in this sector require continuous investment and tend to undergo multiple rounds of financing.

In terms of the funding rounds prior to exit, nine unicorn companies were at Series D or later, with firms such as BioVex and Stemcentrx having even reached Series F and Series G.

Based on past cases, in recent years, mergers and acquisitions of unicorns in the healthcare industry have generally favored technology-driven enterprises. Furthermore, two general trends have emerged:

1. Capital tends to favor later-stage, R&D-driven companies that have achieved certain milestones in clinical trials; in most cases, only after a company’s products have undergone extensive clinical research over a prolonged period can these companies become viable acquisition targets.

2. An analysis of M&A cases involving listed companies also reveals, to a certain extent, that most mergers and acquisitions aim to extend the industry chain by incorporating more advantageous assets into the existing product portfolio. For instance, after Impact Biomedicines’ investigational drug fedratinib was lifted from FDA clinical hold and returned to research and development, Celgene stepped in directly, seemingly reaping the benefits with minimal effort. This acquisition significantly expanded Celgene’s own product pipeline.

Stemcentrx

Acquirer: AbbVie, a developer of cancer stem cell therapeutics

Acquisition Amount: $5.8 Billion

On April 28, 2016, biopharmaceutical research giant AbbVie announced the acquisition of cancer-focused pharmaceutical company Stemcentrx for $5.8 billion, comprising $2 billion in cash and $3.8 billion in stock. Additionally, AbbVie will make milestone payments totaling $4 billion. Stemcentrx will also distribute $400 million to its shareholders.

Stemcentrx, founded in 2008, raised a total of $520 million through several rounds of financing from investors including ARTIS Ventures, Sequoia Capital, and Founders Fund. This acquisition also enabled its backer, Founders Fund, to realize gains of at least $1.7 billion, marking the largest return in the firm’s 11-year history.

AbbVie, a global research-based biopharmaceutical company, employs nearly 25,000 people worldwide and markets its products in more than 170 countries. On January 2, 2013, AbbVie was officially spun off from Abbott Laboratories and began trading independently on the New York Stock Exchange.

AbbVie has been continuously expanding its footprint in oncology. Last year, it acquired a biopharmaceutical company, thereby gaining access to the promising anticancer drug Imbruvica. The experimental monoclonal antibody elotuzumab received FDA approval, and last month, the breakthrough anticancer drug Venclexta also gained FDA approval.

In this acquisition, AbbVie was primarily attracted to two key assets of Stemcentrx: Rova-T, a leading drug for the treatment of lung cancer stem cells, and its technology for targeted identification of cancer stem cells.

Charles Rudin, Director of the Thoracic Oncology Service at Memorial Sloan Kettering Cancer Center, stated, “Rova-T is the first biomarker-based therapy that contributes to the treatment of small cell lung cancer.” As early as 2016, VCBeat Research Institute highlighted several innovative areas worthy of attention and still in blue-ocean markets in a quarterly report, noting that biomarker technologies for tumor diagnosis and treatment were entering a period of technological breakthrough, which would lead to an increasing number of mergers and acquisitions in this field.

Therefore, the acquisition of Stemcentrx will help strengthen AbbVie’s position as a top-tier player in hematologic oncology.

Impact Biomedicines

Acquirer: Celgene, a biotechnology company headquartered in New Jersey specializing in the treatment of multiple myeloma

Acquisition Amount: $7 billion

The transaction consists of three components: Celgene paid $1.1 billion in upfront cash to the San Diego-based company. Celgene will make an additional payment of $1.4 billion contingent on progress toward U.S. Food and Drug Administration (FDA) approval. Finally, Celgene will make milestone payments based on Impact’s sales performance, paying up to $4.5 billion if annual net sales exceed $5 billion.

TechCrunch hailed the deal as one of the highest-return transactions, and according to a joint statement released by the two companies, Celgene expressed strong interest in Impact Biomedicines’ fedratinib.

Fedratinib is a highly selective JAK2 inhibitor currently undergoing clinical trials in 877 patients across 18 clinical studies, showing promise for the treatment of myelofibrosis, a type of blood cancer.

Acerta Pharma

Acquirer: AstraZeneca, a global pharmaceutical giant

Acquisition Amount: $4 billion

In this acquisition, AstraZeneca acquired a 55% stake in the biotechnology company Acerta Pharma for $4 billion to reshape its product portfolio.

AstraZeneca will pay $2.5 billion upfront to acquire this equity stake, with an additional $1.5 billion payable upon the first U.S. regulatory approval of Acerta’s hematologic cancer drug acalabrutinib or by the end of 2018, whichever occurs earlier. Additionally, AstraZeneca holds an option to acquire the remaining shares of Acerta for $3 billion, contingent upon the achievement of certain milestones.

Furthermore, the company may exercise its option to acquire the remaining 45% stake at various junctures, contingent upon conditions such as the initial approval of acalabrutinib in the United States and Europe and the full maturation of commercial timing. Upon announcing the transaction, Pascal Soriot, CEO of AstraZeneca, stated that this investment aligns with the company’s strategy of focusing on long-term growth.

Boston Biomedical

Acquisition Amount: $2.63 billion

Acquirer: Sumitomo Dainippon Pharma

Boston Biomedical may not be a well-known company, but its acquisition price was quite substantial, reaching $2.63 billion. In Boston Biomedical’s previous financing rounds, the publicly disclosed funding amount was only $2 million (according to Crunchbase data).

Japan’s Sumitomo Dainippon Pharma acquired Boston Biomedical in February for $2.63 billion, making it the largest acquisition deal of 2012. If the drugs under development achieve commercial success, Boston Biomedical’s investors will receive the full $2.63 billion payout.

In 2017, the FDA granted Orphan Drug Designation (ODD) to three drugs, one of which was DSP-7888, an experimental cancer peptide vaccine from Boston Biomedical, for the treatment of myelodysplastic syndromes (MDS).

In the United States, a rare disease is defined as a condition affecting fewer than 200,000 individuals. Pharmaceutical companies developing drugs for rare diseases are eligible for various incentives, including clinical development supports such as tax credits for clinical trial costs, waivers of FDA user fees, FDA assistance in clinical trial design, and a seven-year period of market exclusivity following drug approval.

As the name suggests, “exit” in the capital market refers to the necessity of providing an outlet for capital to withdraw and enter the next cycle after it has accompanied startup companies through their most risky phases. To ensure the continuity of capital operations, a capital exit mechanism is indispensable. Common exit methods mainly include initial public offerings (IPOs), mergers and acquisitions (M&A), listing on the National Equities Exchange and Quotations (NEEQ), equity transfers, share buybacks, reverse mergers via shell companies, and liquidation.

Among these, an initial public offering (IPO) is the exit strategy most favored by investors. An IPO, or Initial Public Offering, commonly referred to as “going public,” is a mechanism through which private equity investments realize value appreciation and exit after a company has reached maturity by listing on a securities exchange. Corporate listings are primarily categorized into domestic and overseas listings. Domestic listings mainly refer to listings on the Shenzhen Stock Exchange (SZSE) or the Shanghai Stock Exchange (SSE), while common overseas listings include those on the New York Stock Exchange (NYSE) and NASDAQ. In the United States, the NASDAQ, as the secondary market, pioneered the venture capital exit mechanism.

Driven by leverage in the securities market, investment institutions can sell off their equity holdings after an IPO to realize substantial returns. For companies, beyond the appreciation of their stock value, more importantly, the capital market’s recognition of strong operational performance enables them to secure additional funding for further growth in the securities market.

According to Rock Health’s 2017 Annual Digital Health Funding Report, 2017 was the year with the highest funding amount in the digital health industry to date, totaling $5.8 billion, and for the first time exceeding $5 billion.

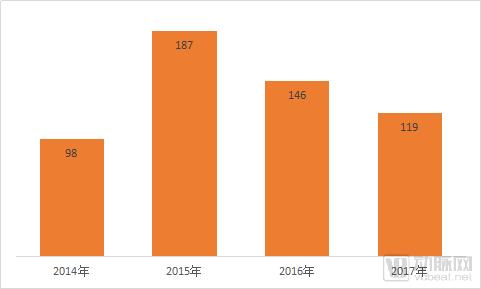

From a market perspective, M&A transaction volume dropped sharply to 119 deals in 2017, with no IPOs recorded, marking the second consecutive year of decline in public M&A activity. The number of digital health M&A transactions in 2017 decreased by 18% compared with 2016 and by 36% relative to 2015, when M&A activity peaked.

Public M&A Transaction Volume in the Healthcare Industry in Recent Years (Source: Rock Health)

Since 2016, the M&A market in the healthcare industry has shown a trend of slow stagnation. However, overall, the entire M&A market remains in a process of steady and balanced development. There are more well-capitalized private enterprises than ever before, and investors are eager to seek potential exit opportunities.

The advantages of exiting through mergers and acquisitions (M&A) lie in the fact that it is not subject to the numerous requirements of an initial public offering (IPO). It features lower complexity and shorter timeframes, while offering flexible and diverse M&A structures. This approach is suitable for startups whose performance is gradually improving but which do not yet meet listing requirements or wish to avoid prolonged waiting periods, particularly when venture capital investors intend to exit. Furthermore, merging companies can share each other’s resources and channels, significantly enhancing operational efficiency.

The disadvantages of exit via mergers and acquisitions (M&A) primarily lie in its significantly lower returns compared to an initial public offering (IPO), as well as higher exit costs. M&A transactions can easily result in the loss of corporate autonomy. Furthermore, companies face considerable challenges in identifying suitable acquirers, timing the transaction appropriately, and achieving a reasonable valuation.

Therefore, for overseas biopharmaceutical companies, the wave of mergers and acquisitions is intensifying, particularly the acquisition of unicorn enterprises, which are characterized by high valuations and unique advantages in specific fields. The number of exits via M&A has surpassed those via IPOs, and M&A is likely to become a major exit channel, primarily because new share issuances remain cautious. For capital seeking rapid liquidity, M&A enables faster exits. Meanwhile, as the industry matures, M&A is also the most effective way to consolidate industry resources.