From Challenger to Collaborator: SF Pharma Logistics Expands to 132 Cities with 3 Cold Storage Facilities and 12 Dedicated Pharma Routes

Last year, SF Express’s entry into the pharmaceutical logistics sector was widely discussed. A year on, SF Express has delivered its performance results. According to SF Express’s annual report,Its pharmaceutical transportation network currently covers 132 prefecture-level cities across China, basically covering most key regions nationwide, and provides ambient temperature logistics, less-than-truckload (LTL), express delivery, commercial distribution, and warehousing services. SF Holding’s cold chain network covers 104 cities and surrounding areas, including three pharmaceutical cold storage facilities and 12 pharmaceutical trunk lines.

Beyond SF Express, companies such as China Post, JD.com, and DHL have also entered the pharmaceutical logistics sector to varying degrees, turning it into a new “battlefield” for logistics providers. Meanwhile, incumbent distribution giants—including Sinopharm, Shanghai Pharmaceuticals, China Resources Pharmaceutical, and Jointown Pharmaceutical Group—have not remained idle; they are ramping up investments in the construction of pharmaceutical distribution centers. The convergence of these trends has introduced significant uncertainty into the pharmaceutical logistics market.

As early as March 2014, SF Express established its Pharmaceutical Logistics Division. In November of the same year, it founded the Cold Chain Logistics Division, focusing on cold-chain distribution for food and pharmaceuticals. By August 2016, SF Express had set up 17 cold-chain logistics branches across China. In mid-November, SF Cold Chain held a launch event in Haikou for its national ground transportation trunk network for pharmaceuticals, demonstrating its continuous strategic moves.

In response to the specific regulatory requirements of the pharmaceutical industry,SF Medicine has obtained GSP certification and third-party logistics licensing.As of now, SF Medicine possesses robust logistics infrastructure and network capabilities, with its pharmaceutical transportation network currently covering 132 prefecture-level cities across China, thereby providing basic coverage of most key regions nationwide.

SF Medicine boasts a professional talent pool and management system. In terms of talent, SF Holding employs licensed pharmacists and a specialized pharmaceutical quality management team from renowned domestic and international pharmaceutical manufacturing and distribution enterprises. Regarding its management system, SF Holding has established multiple quality control regulations and standard operating procedures for pharmaceutical cold-chain logistics, covering all stages including order management, pickup, transportation, transshipment, and delivery.And in accordance with GSP requirements, conduct relevant quality training and assessments for personnel involved in pharmaceutical logistics operations, including operational staff, quality assurance personnel, and operations management staff., to enhance end-to-end cold chain logistics management and traceability capabilities.

SF Pharma possesses five core closed-loop logistics and supply chain service capabilities, providing the industry with services including, but not limited to, long-haul transportation, urban distribution, pharmaceutical warehousing, last-mile delivery to end consumers, and clinical laboratory logistics. Leveraging robust information technology and the integrated resources across SF Holding’s various business segments, SF Pharma has collaborated with industry benchmark clients to develop comprehensive solutions addressing warehouse network layout, inventory and logistics management, and circulation channels and distribution, in response to the reforms of the “Two-Invoice System” for pharmaceutical distribution.

SF Pharma Logistics: Main Products

Source: SF Holding 2017 Annual Report

Cold-chain transportation is a key focus of SF Pharma’s logistics layout. As of the end of 2017,SF Holding’s cold-chain network covers 104 cities and surrounding areas, including three pharmaceutical cold-storage warehouses and 12 pharmaceutical trunk lines., connecting core cities in Northeast China, North China, East China, South China, and Central China;24,000 sq m pharmaceutical cold storage, has obtained all necessary certifications and operational permits, including the Drug Operation Permit, GSP Certification Certificate, Medical Device Business Operation Permit, and the approval from the national food and drug administration authorities for “pilot work on third-party modern pharmaceutical logistics”; it operates 916 refrigerated vehicles, of which 244 are GSP-certified.

Currently, SF Cold Chain focuses on providing professional, customized, and efficient integrated supply chain solutions for customers in the fresh food and pharmaceutical industries, covering multiple sectors including production, e-commerce, distribution, and retail within the food and pharmaceutical industries. In 2017, the company’s cold chain food and pharmaceutical businesses experienced rapid growth.Tax-exclusive operating revenue reached RMB 2.295 billion,Year-on-year growth of 59.70%.Pharmaceutical industry clients include: Harbin Pharmaceutical Group, China Resources Sanjiu, Sanofi Pharmaceuticals, Guangzhou Pharmaceutical Holdings, etc.

In terms of volume, after years of rapid development, China's express delivery service volume has risen to the top position globally. In 2017, the industry entered a phase of growth rate adjustment. Data from the State Post Bureau shows that in 2017, the volume of express delivery services increased by 28.0%, and business revenue grew by 24.7%. Both figures represent a decline compared to the growth rates in 2016, but they still remain at a relatively high level.

SF Holding also stated that market competition in China’s express logistics industry has become increasingly intense. On one hand, leading express logistics companies are striving to expand their business operations and network coverage through various means. On the other hand, external forces such as e-commerce platform enterprises and social capital are accelerating their entry into the express logistics sector, further intensifying market competition.Should the Company fail to adopt proactive and effective measures to address the evolving competitive landscape, it may face risks of slowed business growth and declining market share.

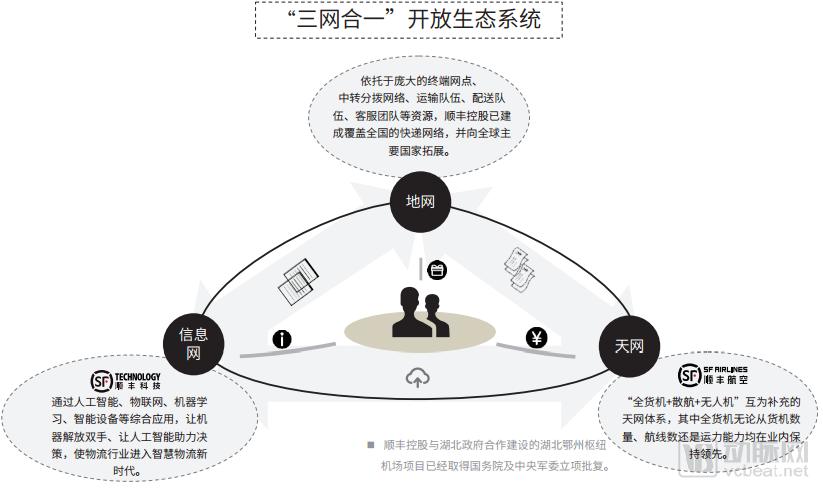

Therefore, SF Express is not only consolidating its existing advantages but also actively seeking new business growth drivers. In terms of consolidating its existing advantages,SF Express builds its core competitiveness through the “Air Network + Ground Network + Information Network” model.“The Sky Network” is an air freight network composed of all-cargo aircraft, belly-hold cargo on passenger flights, and drones; the “Ground Network” consists of tens of thousands of business outlets across China, transit and distribution hubs, road transport networks, warehousing facilities, customer service call centers, and last-mile delivery networks; the “Information Network” encompasses smart devices, intelligent services, data-driven decision-making, smart packaging, machine vision recognition, and the Internet of Vehicles (IoV).

Source: SF Holding 2017 Annual Report

SF Holding’s new businesses are primarily focused on heavy freight, cold-chain logistics, international services, and intra-city delivery. The cold-chain logistics segment refers to the aforementioned food and pharmaceutical cold-chain operations. SF has high expectations for this sector.The plan is to continue improving the pharmaceutical logistics infrastructure in 2018, gradually establishing a nationwide “T+3” pharmaceutical logistics network through multi-warehouse coordination, trunk line transportation scheduling, and supplementary air freight capacity.

Optimize the end-to-end business model and operational processes for warehousing, trunk transportation, and distribution; further enhance precise temperature control capabilities across multiple temperature ranges (-40°C to 25°C); and improve resource utilization efficiency and operational quality. Continue to strengthen R&D and innovation in validation management technologies for pharmaceutical cold chain equipment and facilities, as well as information system management models. Build comprehensive solution capabilities for industry clients, centered on pharmaceutical manufacturers, vaccine producers, and biopharmaceutical companies.Build the SF Pharmaceutical Supply Chain Service Platform 2.0 for Enterprises.

Beyond SF Express, companies such as China Post, JD.com, and DHL have also entered the pharmaceutical logistics sector to varying degrees, turning the pharmaceutical logistics market into a new “battlefield” for logistics providers.

As early as 2015, a pharmaceutical company under China Post had already been designated by Fujian Province as a distributor for essential medicines. China Post’s subsidiary in Fujian has completed its coverage layout across seven major regions, including Fuzhou, Putian, Sanming, and Quanzhou. Despite being established only two years ago, the local China Post subsidiary has achieved an annual sales volume of RMB 1 billion, a success fully attributed to the recruitment of professional pharmaceutical management personnel, government support, and the backing of the postal network.

On August 29, 2017, JD.com held the “JD Logistics Pharmaceutical Cloud Warehouse Strategic Signing Ceremony and Pharmaceutical Logistics Industry Solutions Sharing Session” at its headquarters. During the event, JD.com signed cooperation agreements with eight well-known pharmaceutical distribution enterprises, including Sinopharm Group, Hongyuntang, and Yikang Pharmaceutical Group, to carry out comprehensive collaboration in the field of pharmaceutical distribution.

The industry will leverage JD.com’s technology platform for resource integration, while JD.com provides diverse solutions for various players across the supply chain, including one-stop delivery services for industrial enterprises, remote feeder-line distribution for pharmaceutical wholesalers, same-city delivery for chain pharmacies, and e-commerce platform logistics.

In addition, Shanghai Pharmaceuticals has entered into a strategic partnership with DHL China. Through collaboration in capital and business operations, the two parties aim to leverage their complementary strengths and share resources, jointly expanding third-party logistics services—including warehousing, distribution, and value-added services—related to pharmaceuticals, general health products, and medical devices.

The strategic moves by the aforementioned companies are closely linked to the relaxation of policies. On February 3, 2016, the State Council issued a document,Decided to cancel approval items such as the authorization for engaging in third-party pharmaceutical logistics business.Third-party pharmaceutical logistics refers to enterprises with pharmaceutical distribution qualifications sharing their warehousing and logistics capabilities across the industry and opening up these capabilities to all stakeholders in the supply chain. This also means that companies such as SF Express and China Post, which have obtained Good Supply Practice (GSP) certification, can more conveniently provide third-party logistics services.

Furthermore, as policies such as the “Two-Invoice System” and the “Separation of Prescribing from Dispensing” are advanced, pharmaceutical distributors’ demand for third-party logistics is intensifying. For instance, pharmaceutical manufacturers previously operated under a regional agency model, where regional agents handled logistics and distribution to city- and county-level markets. However, under the “Two-Invoice System,” this approach fails to meet the “two-invoice” requirement.Pharmaceutical manufacturing enterprises will choose to collaborate with third-party pharmaceutical logistics companies for distribution in city- and county-level markets, thereby achieving the separation of commercial flow and logistics flow.

For example, against the backdrop of the rapid development of pharmaceutical e-commerce, logistics companies can provide online drug delivery services for B2C pharmaceutical e-commerce platforms (strictly speaking, this model also requires GSP certification). In addition, there is strong encouragement for the “online order, store delivery” model, whereby logistics companies can facilitate such services for pharmacies.

In summary, this article outlines several business models for logistics companies entering the pharmaceutical distribution sector. These include contracted distribution on behalf of licensed pharmaceutical distributors, operating as third-party pharmaceutical logistics providers after obtaining drug distribution qualifications, and e-commerce delivery. It is evident that logistics companies have diverse entry points and significant growth potential in the pharmaceutical logistics market.

Social logistics enterprises are actively entering the pharmaceutical logistics market, while incumbent pharmaceutical distribution companies are also undergoing active transformation. Some small-scale pharmaceutical trading enterprises are comprehensively transitioning into pharmaceutical logistics providers, whereas large-scale distributors represented by Sinopharm Group, China Resources Pharmaceutical, Shanghai Pharmaceuticals, and Jointown Pharmaceutical Group are rapidly expanding their regional network coverage to further enhance their terminal reach capabilities.

Taking Sinopharm Group as an example, by the end of 2017, its distribution network had covered all 31 provinces, municipalities directly under the Central Government, and autonomous regions in China. Its direct customers included 15,000 hospitals (referring specifically to tiered hospitals, including 2,301 tertiary hospitals, which are the largest and highest-level facilities), 128,000 small-scale terminal customers (including primary healthcare institutions), and 87,200 retail pharmacies. In terms of logistics infrastructure, Sinopharm Group operated four hub logistics centers, 42 provincial-level logistics centers, 236 prefecture-level logistics sites, and 26 retail logistics sites across China, bringing the total number of logistics sites to 308.

Regarding the future development plan for its distribution business, Sinopharm Holdings stated that it will continue to “Continue to deepen the distribution network, optimize its layout, and further leverage scale and network advantages.”

Sinopharm’s strategy is a microcosm of the transformation underway among China’s pharmaceutical commercial enterprises. Under the influence of policy, market forces, and other factors, scaling up has become an imperative. The 13th Five-Year Plan for Drug Distribution points out that it is necessary to cultivate a group of large-scale drug distribution enterprises with nationwide network coverage and a high degree of intensification and informatization.The annual sales of the top 100 pharmaceutical wholesalers account for more than 90% of the total pharmaceutical wholesale market.

According to data from the “Statistical Analysis Report on the Operation of the Pharmaceutical Distribution Industry (2016)” issued by the Department of Market Order Regulation under the Ministry of Commerce, there were 12,975 pharmaceutical wholesale enterprises nationwide as of the end of November 2016. If the top 100 distribution companies capture 90% of the market in the future, the remaining nearly 13,000 pharmaceutical wholesalers will face negligible market space, with elimination or integration being their only prospects.

However, it should be noted thatCurrently, neither SF Express nor JD.com has entered the core segment of pharmaceutical logistics, and their market share remains relatively small.This can be attributed to the regional characteristics of pharmaceutical distribution and the high level of industry specialization. The regional nature is reflected in variations in pharmaceutical policies, bidding, and procurement processes across different regions, which require thorough understanding for market entry. Furthermore, as a special commodity, pharmaceuticals demand specialized talent and management expertise for their operation and distribution—capabilities that are currently lacking in general social logistics systems.

However, since third-party logistics providers are keen to enter the pharmaceutical logistics sector, they have made corresponding preparations. Leveraging their advanced logistics management expertise, these providers can upgrade pharmaceutical distribution operations, thereby enhancing efficiency. In fact, the aforementioned collaborations—JD.com with eight pharmaceutical distributors, and Shanghai Pharmaceuticals with DHL China—are typical examples of combining third-party logistics experience with specialized pharmaceutical logistics solutions.

In summary, social logistics enterprises represented by SF Express have entered the pharmaceutical logistics sector driven by business growth. However, they have not entered as “challengers” but as “partners,” collaborating with willing enterprises to leverage their mature logistics expertise to transform pharmaceutical logistics. This aligns with the broader context in which the pharmaceutical industry itself is undergoing changes under the influence of policies and market forces, creating a need for transformation and upgrading. Consequently, both sides are able to identify sufficient points of shared interest.From this perspective, more “SF Express-like” players may enter the pharmaceutical logistics sector in the future, making the pharmaceutical distribution industry highly uncertain.