Three State-Owned Pharmaceutical Distribution Giants Surpass RMB 100 Billion in Revenue, Reshaping Industry Landscape

As policies such as the “Two-Invoice System,” “Zero Markup,” and “Separation of Prescribing from Dispensing” are progressively implemented, their impact on the performance of the pharmaceutical industry has become increasingly clear. Judging by the performance of relevant companies, pharmaceutical manufacturers are transforming their marketing strategies, placing greater emphasis on building in-house sales teams and professional promotion capabilities. Pharmaceutical distributors are actively diversifying their business portfolios and pursuing horizontal and vertical M&A integration across the industry to accelerate scale-driven growth. Meanwhile, pharmaceutical retailers are focusing on new retail models to capture the trend of “prescription outflow.”

Listed companies serve as the optimal window for observing industry dynamics. With the completion of their annual report disclosures, we now have high-value case studies and data support for analyzing industry operational trends. VCBeat (WeChat ID: vcbeat) has compiled the 2017 annual reports of listed companies in the pharmaceutical commerce sector, aiming to analyze the current competitive landscape and future development trends of the pharmaceutical distribution industry based on these annual report data.

State-owned enterprises hold an absolute dominant position in China’s pharmaceutical distribution market. The top three national pharmaceutical distributors are all state-owned: Sinopharm Group, China Resources Pharmaceutical, and Shanghai Pharmaceuticals. Leading regional pharmaceutical distributors also have state-owned backgrounds, such as Nanjing Pharmaceutical, Huadong Medicine, Chongqing Pharmaceutical, Liuzhou Pharmaceutical, and Renmin Tongtai.

Based on financial report performance, the majority of pharmaceutical commercial enterprises achieved performance growth exceeding 10%, with only a few companies experiencing stagnant or negative growth. Neptunus Pharmaceutical’s commercial business revenue growth ranked first, reaching 70.86%; other companies, including Realcan Medicine, Jiashitang, Liuzhou Pharmaceutical, Tasly, Jointown Pharmaceutical Group, and Luyan Pharmaceutical, also demonstrated robust growth in their pharmaceutical commercial business revenues.

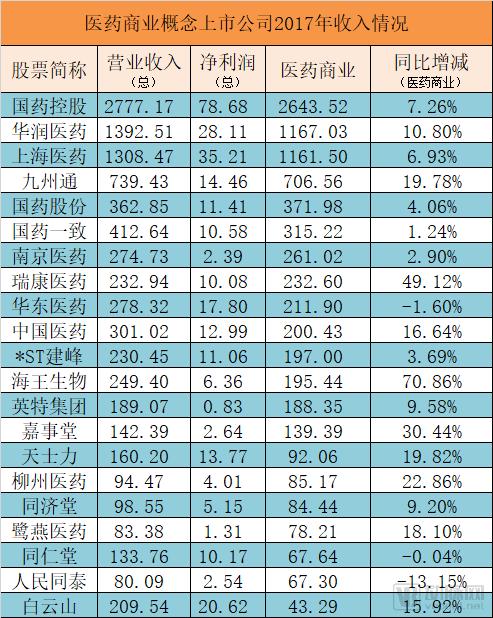

Below are the 2017 revenue and net profit figures for listed companies in the pharmaceutical distribution sector, along with the growth rates of their pharmaceutical distribution business revenues:

Data Source: Annual Corporate Reports, Compiled by VCBeat

Sinopharm Group is the undisputed "leader" of the pharmaceutical distribution market, its main listed subsidiaries engaged in pharmaceutical distribution are Sinopharm Group (HK.01099), Sinopharm Co., Ltd. (600511), and Sinopharm Consistent (000028).In 2017, the three listed companies reported a combined revenue of RMB 355.266 billion and a net profit of RMB 10.067 billion, with the pharmaceutical commerce segment generating a total revenue of RMB 333.072 billion.

The three subsidiaries of Sinopharm Group engaged in pharmaceutical distribution have slightly different divisions of labor, among which,Sinopharm Holding is a national comprehensive pharmaceutical supply chain service provider., providing distribution and delivery services for pharmaceuticals, medical devices, diagnostic reagents, and other products. By the end of 2017, Sinopharm Group’s subsidiary distribution network had covered all 31 provinces, autonomous regions, and municipalities directly under the central government in China. The number of its direct customers reached 15,032 (referring exclusively to tiered hospitals, including 2,301 tertiary hospitals, which are the largest and highest-level facilities), with 128,000 small-scale end-users (including primary healthcare institutions) and 87,000 retail pharmacies. During the reporting period, Sinopharm Group’s pharmaceutical distribution business generated revenue of RMB 264.352 billion.

Sinopharm Group Co., Ltd. is a subsidiary of Sinopharm Holding, specializing in the distribution of narcotic and psychotropic substances as well as high-end prescription drugs., with its base in Beijing and coverage extending across the national pharmaceutical market, is committed to providing customers with professional third-party pharmaceutical logistics services. In June 2017, four subsidiaries of Sinopharm Holding—Sinopharm Holding Beijing, Sinopharm Holding Kangchen, Sinopharm Holding Huahong, and Sinopharm Holding Tianxing—were integrated into Sinopharm Group Pharmaceutical Co., Ltd. (Sinopharm Pharma), making it the sole pharmaceutical distribution platform for Sinopharm Group in the Beijing region and further consolidating its leading position in the regional pharmaceutical commerce sector.

Sinopharm ConsistencyIn 2016, it underwent restructuring and was strategically positioned as Sinopharm Group’s national pharmaceutical retail integration platform, completing its integration with Guoda Drugstore and achieving“China-wide Retail + Distribution in Guangdong and Guangxi + Industrial Investment”strategic transformation and upgrading. Its distribution business is mainly concentrated in the Guangdong and Guangxi regions, where it is the largest pharmaceutical distributor; its retail business covers 19 provinces across China, with nearly 4,000 stores, and retail revenue exceeded RMB 10 billion in 2017.

Second place is China Resources Pharmaceutical., with its 2017 revenue reaching RMB 139.251 billion, the proportions of its pharmaceutical manufacturing, pharmaceutical distribution, and drug retail businesses were 15.3%, 82.2%, and 2.5%, respectively; the pharmaceutical distribution business generated RMB 116.703 billion in revenue, a year-on-year increase of 9.3% (or 10.8% when measured in RMB terms).

In 2017, China Resources Pharmaceutical completed the layout of its distribution business in four previously unserved provinces: Jiangxi, Hainan, Qinghai, and Xinjiang. By strengthening provincial-level platform construction, accelerating network penetration into lower-tier markets, and expanding reach into grassroots markets, it further consolidated its regional leadership advantages. As of the end of the reporting period, China Resources Pharmaceutical’s distribution network covered 27 provinces, municipalities directly under the Central Government, and autonomous regions across China, serving 5,475 secondary and tertiary hospitals, 37,941 primary healthcare institutions, and 30,270 retail pharmacies.

Shanghai Pharmaceuticals ranks third., with its 2017 revenue reaching RMB 130.847 billion and net profit amounting to RMB 3.521 billion; the pharmaceutical commercial business generated revenue of RMB 116.150 billion, representing a year-on-year increase of 6.93%.

In 2017, Shanghai Pharmaceuticals completed the acquisition of Cardinale Health China’s entire business, a 51% equity stake in Sichuan Shenyu Pharmaceutical, and a 99% equity stake in Xuzhou Pharmaceutical. This enabled the company to break through into the markets of Sichuan, Chongqing, Guizhou, and Tianjin, expanding its direct distribution network coverage from 20 to 24 provinces and consolidating its leading position in niche sectors such as imported pharmaceutical agency, medical device agency, and third-party professional logistics services.Meanwhile, in response to the "Two-Invoice System" requirements, it has continuously increased the proportion of its pure sales business (reaching 62.35%).; and actively expanded its hospital pharmacy trusteeship business, adding 97 new pharmacies under management to bring the total to 226; improved the modern logistics network and advanced the construction of regional logistics centers.

Comparison of the Three Giants: Sinopharm, China Resources, and Shanghai Pharmaceuticals

Data source: Corporate annual reports, compiled by VCBeat

Based on discussions and analyses by management teams across various enterprises, it is widely acknowledged that policy is the primary factor influencing performance. The most frequently cited policy is the “Two-Invoice System.” Other policies mentioned repeatedly include “zero markup,” sunshine procurement, secondary price negotiations, tiered diagnosis and treatment, health insurance cost containment, and adjustments to the drug reimbursement list.

From the external environment perspective, since pharmaceutical commercial enterprises have long operated by advancing funds (there is a certain credit period from purchasing goods from upstream industrial enterprises to receiving payment from hospitals), thereforePharmaceutical commercial enterprises often engage in financing to replenish working capital.—Long-term and short-term borrowings, margin financing and securities lending, share issuance, commercial factoring, etc.; therefore, financing costs also affect the performance of pharmaceutical commerce businesses.Rising financing interest rates have impacted the profitability of pharmaceutical commercial operations.

Two-Invoice System

The “Two-Invoice System” mandates that only two invoices can be issued for pharmaceuticals from manufacturers to hospitals, which has disrupted traditional pharmaceutical distribution operations. In this context, the “pure sales” model, where distributors sell directly to medical end-users, complies with regulatory requirements. Influenced by the “Two-Invoice System,” distributors have placed greater emphasis on deepening their commercial channels and expanding coverage of terminal outlets. As noted in Jointown Pharmaceutical Group’s annual report, “The company has continued to vigorously expand its presence in the mid-to-high-end hospital market at the secondary level and above, with its hospital pure sales business maintaining rapid growth.” The company’s hospital pure sales business generated RMB 14.616 billion in revenue, representing a year-on-year increase of 32.96%.

Deepening “Healthcare Reform”

Deepening “healthcare reform” encompasses a wide range of initiatives, such as comprehensive public hospital reforms, the establishment of medical consortia, tiered diagnosis and treatment, separation of prescribing from dispensing, zero-markup policies for pharmaceuticals, and cost containment within medical insurance schemes. These policies have had varying impacts. Overall, however, the goal of “healthcare reform” is to triage patients by directing those with minor or chronic conditions to primary care facilities, thereby alleviating the burden on large tertiary hospitals. In terms of outcomes, the growth in patient visits at Grade II and Grade III tertiary hospitals has remained at a reasonable level, demonstrating the pronounced effectiveness of the tiered diagnosis and treatment system.

Meanwhile, to strengthen primary healthcare supply, restrictions on medication at the primary care level have been lifted, leading to rapid growth in the primary pharmaceutical market. Pharmaceutical distribution companies are placing greater emphasis on this segment. As primary healthcare experiences a comprehensive rise, both pharmaceutical manufacturers and commercial enterprises are increasingly prioritizing the primary care market by increasing their investments through academic promotion, physician education, network development, and patient education. However, as it currently stands,The lack of supporting policies for medication restrictions at the primary care level has left a ceiling on market growth due to medical insurance caps, which has also become the biggest obstacle for pharmaceutical companies expanding into the primary care market.

Separation of Pharmaceutical Services from Medical Care; Outflow of Prescriptions

The separation of medical services from pharmaceutical sales and the outflow of prescriptions should be discussed within the context of deepening “healthcare reform.” Under the influence of policies,Pharmacies have become cost centers for hospitals, incentivizing hospitals to divest their pharmacy operations and creating opportunities for prescription outflow.Prescription outflow is essentially a process of redistributing profits from drug sales, involving various stakeholders across the industry chain, including pharmaceutical manufacturers, distributors, hospitals, physicians, and pharmacies. From an industry layout perspective, companies such as Shanghai Pharma, Jointown Pharmaceutical Group, and Guoda Drugstore are actively expanding their presence through strategies that include hospital-adjacent pharmacies, DTP (Direct-to-Patient) pharmacies, electronic prescription platforms, and online delivery services.

From the perspective of policy evolution trends,“Separation of prescribing and dispensing” will continue to advance, and the outflow of prescriptions is an irreversible trend.Retail pharmacies and integrated wholesale-retail enterprises, which have long been at the forefront of pharmaceutical distribution and retail, possess extensive experience in pharmaceutical distribution, logistics, and pharmaceutical care services, and will be the first to benefit from the outflow of prescriptions. Other related developments, such as Direct-to-Patient (DTP) pharmacies, electronic prescription circulation platforms, and online delivery services, are concomitant phenomena of prescription outflow and also present significant growth opportunities.

However, there are still many challenges to overcome in the actual implementation of prescription outflow.For instance, issues regarding prescription sources involve collaboration and profit-sharing arrangements with hospitals and physicians; concerns about medical insurance pooling include whether out-of-hospital medication purchases are reimbursable and if reimbursement policies are consistent; and questions remain as to whether the pharmaceutical care capabilities of community pharmacies are adequate to ensure medication safety.

Drug Tendering

Pharmaceutical products must pass provincial-level tendering to enter public hospitals. In recent years, in addition to provincial tendering, various other procurement methods have been gradually explored, including transparent procurement, secondary price negotiation, Group Purchasing Organizations (GPOs), and price negotiations.Price Caps and Cost Control Are the Themes of Centralized Procurement Bidding, as a result, the winning bid prices and procurement volumes of pharmaceutical commercial enterprises have declined to some extent.

Other Pharmaceutical Policies

Other pharmaceutical policies affecting the pharmaceutical distribution business also include medical insurance cost containment, the “two-invoice system” for medical devices and consumables, and the cancellation of administrative approval for third-party pharmaceutical logistics.

WithNational Healthcare Security Administrationof the establishment, "The Most Powerful Healthcare Payer” signifies a more centralized approach to the fundraising and utilization of medical insurance funds, with the National Healthcare Security Administration (NHSA) playing a more active role in the tendering and procurement process, thereby truly leveraging its function as the “purse strings.” Drawing on experiences from Fujian and other regions, the NHSA will engage in direct negotiations with pharmaceutical and medical device suppliers to effectively reduce procurement prices. Furthermore, during the later stages of functional transformation, the NHSA may collaborate with social institutions through “government purchase of services” models to pilot initiatives such as Group Purchasing Organizations (GPOs).

Previously, on February 3, 2016, the State Council issued a document,Decided to cancel approval items such as the authorization for engaging in third-party pharmaceutical logistics business.Third-party pharmaceutical logistics refers to enterprises with pharmaceutical distribution qualifications sharing their warehousing and logistics capabilities across the industry, opening up these capabilities to all stakeholders in the supply chain. This also means that,Social logistics enterprises that have obtained GSP certification, such as SF Express and China Post, can more conveniently provide third-party logistics services.

Driven by endogenous and external factors such as policies, market dynamics, and capital, leading listed pharmaceutical distribution companies have responded proactively. In terms of response strategies,Mergers and acquisitions integration and diversified business expansion are its primary directions.

In terms of M&A integration, in addition to the aforementioned acquisitions by Shanghai Pharmaceuticals of Cardinal Health’s China business, a 51% equity stake in Sichuan Shenyu Pharmaceutical, and a 99% equity stake in Xuzhou Pharmaceutical, Nanjing Pharmaceutical acquired in September 2017 a 19.9995% equity stake in Jiangsu Huaxiao Pharmaceutical Logistics Co., Ltd., a 20% equity stake in Nanjing Pharmaceutical Nantong Jianqiao Co., Ltd., and a 39.84% equity stake in Nanjing Pharmaceutical (Huai’an) Tianyi Co., Ltd., all held by Zhongjian Zhikang Supply Chain Service Co., Ltd. These three companies subsequently became its wholly-owned subsidiaries.

In addition to horizontal acquisitions, we have also observed someVertical IntegrationFor example, Realcan Medicine acquired Jingquan Traditional Chinese Medicine, Wuxi Dongfang Pharmaceutical, Jinan Chichuang Medical Devices, and Shanghai Hengli Medical Equipment in 2017. During the reporting period, it completed nearly 60 major equity investments, with a total amount reaching RMB 2.159 billion. It was this continuous merger and acquisition integration that drove the sustained growth of Realcan Medicine’s pharmaceutical commercial business, resulting in a year-on-year revenue increase of 49.12%.

Affected by policy, the profit margins and growth rates of pharmaceutical commercial businesses are constrained. Many pharmaceutical commercial enterprises have begun to explore businesses beyond drug distribution, pursuing diversified business expansion, such as venturing into traditional Chinese medicine and chemical drugs,Medical Device Distribution, pharmaceutical e-commerce, third-party pharmaceutical logistics, etc.

Taking Realcan Medicine as another example, its annual report disclosed that the medical device distribution business generated operating revenue of RMB 7.333 billion in 2017, a year-on-year increase of 152.96%. The business covers 31 provinces and municipalities directly under the Central Government, experiencing rapid growth. In 2017, the company further expanded its device business beyond Shandong Province, completing mergers and acquisitions and achieving business coverage in all 31 provinces (municipalities) across China, thereby realizing rapid growth in its medical device and medical consumables businesses. Currently, the product lines from renowned domestic and international enterprises represented by the company comprehensively meet the clinical needs of healthcare institutions, providing technical services covering all clinical departments.

Jointown also stated that during the reporting period, its medical device and family planning products business continued to maintain a rapid growth momentum, achieving sales revenue of RMB 6.976 billion, a year-on-year increase of 43.23% from RMB 4.871 billion in the same period last year.

Currently, the medical device distribution industry in China suffers from low market concentration and inefficient operations.According to data from Caixin Morita Intelligence, the overall size of China’s medical device market is projected to exceed RMB 760 billion in 2020. Currently, there are 190,000 medical device and pharmaceutical commercial enterprises in China, with the top four distributors accounting for only 12% of the market share, indicating that industry concentration is significantly lower than that of pharmaceutical distribution. With the nationwide pilot implementation of the “two-invoice system” for medical devices and consumables, the industry will undergo transformative resource consolidation, ultimately benefiting leading enterprises with a national presence. In this context,Many pharmaceutical distribution companies have begun to expand into medical device distribution, including Realcan Medicine, Jointown Pharmaceutical, and Jiashitang.

Furthermore, expansion efforts have been directed toward integrated wholesale and retail operations, pharmaceutical e-commerce, and value-added services for hospital supply chain management. For instance, leading pharmaceutical commercial enterprises all operate retail businesses (Sinopharm—Guoda Drugstore; China Resources Pharmaceutical—CR Tang; Yibao Quanxin; Shanghai Pharma—Huashi Pharmacy; Jointown—Haoyaoshi Chain), and are also involved in online pharmacy and online wholesale operations. Logically speaking,Retail operations can fully leverage the cost advantages of distribution channels, enhancing their market competitiveness and generating strong synergies.

Northeast Securities stated that new business models in pharmaceutical distribution, such as third-party pharmaceutical logistics operated by distributors, co-operated pharmacies, managed pharmacies, Supply, Processing, and Distribution (SPD) services, and Direct-to-Patient (DTP) pharmacies, have been successfully implemented in certain provinces across China. Meanwhile, Group Purchasing Organization (GPO) and Pharmacy Benefit Management (PBM) models are gradually being explored. The emergence of these diversified value-added services is creating new profit growth drivers for the distribution industry and accelerating the value reshaping of China’s pharmaceutical distribution sector.

The “National Development Plan for the Pharmaceutical Distribution Industry (2016–2020)” points out that the pharmaceutical logistics industry is currently facing such realities as the continuous growth in market demand for medicines and health services, the ongoing advancement of healthcare system reforms, and an increasingly urgent need for the transformation and upgrading of pharmaceutical distribution.The goal is to achieve by 2020, cultivate and develop a group of large-scale pharmaceutical distribution enterprises with nationwide network coverage and a high degree of intensification and informatization.The annual sales of the top 100 pharmaceutical wholesalers account for more than 90% of the total pharmaceutical wholesale market.

According to data from the “Statistical Analysis Report on the Operation of the Pharmaceutical Distribution Industry (2016)” issued by the Market Order Department of the Ministry of Commerce, there were 12,975 pharmaceutical wholesale enterprises nationwide as of the end of November 2016. If the top 100 distribution companies capture 90% of the market in the future, it would mean that the remaining nearly 13,000 pharmaceutical wholesalers would have negligible market space, with only elimination or integration awaiting them. In other words,The pharmaceutical distribution industry is on the verge of a major reshuffle.

Amid the deepening healthcare reforms, the pharmaceutical distribution industry must cope with pressures from policies such as the “Two-Invoice System,” “Zero Mark-up Policy,” and “Centralized Procurement Bidding,” posing challenges to both operational structures and management models. However, viewed from the perspective of adaptation, these policy pressures also serve as a “catalyst” for industry adjustment and upgrading. By breaking through via mergers and acquisitions, integration, and diversification of business lines, a cohort of leading distribution enterprises better aligned with the developmental needs of the pharmaceutical industry is likely to emerge in the future.