China's 2017 Medical Imaging Market Valued at RMB 200 Billion: Emerging Opportunities in Third-Party Imaging Services

China originally had no third-party medical imaging services, with each hospital purchasing its own equipment. Constrained by the existing system, public hospitals favored acquiring large-scale medical devices, particularly high-end models. This practice not only enhanced the hospital’s image but also provided tangible benefits to relevant personnel. As a result, imaging equipment in most regions of China was overallocated (i.e., the majority of devices in a given area remained idle and failed to operate at full capacity). Due to the same systemic constraints, these underutilized devices could not be accessed by third-party providers, leading to significant waste of resources.

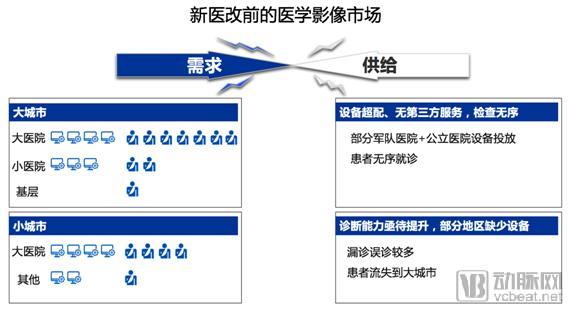

The obvious characteristics of the healthcare market before the new healthcare reform were:

(1) In major cities, renowned hospitals possess abundant medical equipment but serve a disproportionately large patient population, resulting in prolonged waiting times. Mid-tier hospitals (such as secondary hospitals) also have considerable equipment resources but see fewer patients, leading to significant underutilization. Meanwhile, primary healthcare institutions, despite having a smaller patient base, suffer from a lack of equipment. Unmet demand for diagnostic examinations is partially absorbed through socially deployed equipment at certain military and public hospitals.

(2) In small cities, the local largest central hospitals or people’s hospitals generally have medical equipment well-matched to patient volumes, with minimal queuing. Other hospitals may be equipped with imaging devices but see very few patients. The primary challenges in small cities are low standardization of imaging acquisition and limited diagnostic capabilities. In some economically underdeveloped regions, equipment configuration remains suboptimal, leaving considerable room for improvement.

Since the healthcare reforms, the state has vigorously promoted a tiered diagnosis and treatment system, aiming to keep patients at primary care facilities in grassroots cities for initial consultations, with referrals to large hospitals reserved for complex and critical cases. In the medical imaging market, the government has implemented four major reforms:

(1) Military hospital reforms and the cessation of paid services led to the termination of all imaging equipment placement projects, making further operations impossible;

(2) Examination fees have dropped significantly, transforming radiology departments from highly profitable units into low-margin or even loss-making ones (under full-cost hospital accounting);

(3) Reclassify large-scale medical equipment from “non-administrative licensing items” to “administrative licensing items,” and strengthen the approval process for public hospitals’ acquisition of equipment configuration permits;

(4) Introduce measures to encourage social participation in healthcare, such as the establishment of independent imaging centers and the sharing of imaging resources.

The national strategy is clear: promoting tiered diagnosis and treatment necessarily entails supporting third-party imaging services, reducing government expenditure, controlling medical costs, and increasing social investment.

However, the existing market structure cannot be changed overnight. It is challenging for third-party medical imaging, an emerging sector, to take root and grow from the established industry landscape. At present, the third-party medical imaging market comprises only two segments:

(1) The market void left by the withdrawal of military hospitals and public hospitals accounts for 5%-33% of the imaging market in major cities, with significant variations across different cities;

(2) The demand for upgrading imaging equipment in county-level and prefecture-level cities has transformed the traditional equipment sales model into partnerships with third-party imaging centers. This market is difficult to quantify, as it depends on specific regional demands and opportunities, and more importantly, on whether the operator can integrate local resources and persuade hospitals to forgo independent equipment purchases in favor of collaborating with third-party providers.

The combined market size of these two segments is estimated to be approximately RMB 15–20 billion.

In fact, there are various estimates of market size, but no precise data are available. By analyzing data from the China Health Statistics Yearbook and the National Bureau of Statistics, it can be estimated that the total annual revenue from hospital examination fees (primarily comprising imaging examinations and laboratory tests) in 2017 was approximately RMB 300 billion. Based on general industry experience that imaging examinations and laboratory tests each account for half of such fees in hospitals, hospital imaging examination fees amounted to roughly RMB 150 billion. When including the market served by primary healthcare institutions, the overall medical imaging market is estimated at around RMB 200 billion. It is projected to grow to approximately RMB 250 billion by 2020.

To successfully operate an imaging center, or even establish a chain-based imaging center service system, four core competencies are required:

(1)Financial Strength: Capable of providing long-term financial support, which is a fundamental capability.

(2)Operational Capability: To ensure the sustainable survival of an imaging center, it must possess either the capability to acquire patient traffic through market-oriented means or the ability to establish close collaborative partnerships with public hospitals that already have established patient flows. At least one of these two capabilities is mandatory.

(3)Expert Resources: Imaging centers should be able to gather China's top imaging examination technologies and diagnostic experts, improve the quality of imaging examinations, and extend high-quality diagnostic capabilities to primary healthcare institutions through internet and artificial intelligence technologies, thereby highlighting the advantages of third-party imaging services.

(4)Chain Management: Traditional medical imaging service providers, despite having numerous projects across China, operate in silos, lacking unified and standardized management capabilities and synergies. The radiology departments within large hospitals and third-party imaging centers follow entirely different management models; managers from public hospital radiology departments often struggle to adapt to market demands, resulting in a current shortage of talent skilled in managing chain medical institutions. With the rise of private healthcare organizations, this has become a challenge across various specialized sectors of the medical industry.

How to Do It? To this end, on June 10, we invited several industry experts with practical experience in medical imaging, including representatives from investment firms and entrepreneurs. The details are as follows:

From policy to industry development trends, from building online traffic entry points to enhancing offline customer acquisition capabilities, and from the standardization to the chain operation of imaging centers, we invite government officials, industry experts, hospital directors, and numerous industry professionals to jointly explore the “New Structure.”

At this Imaging Center Forum, VCBeat will also release a related report. This report embodies the long-standing industry focus and insights of VCBeat, its editors, and researchers at VBInsight, serving as a concrete manifestation of VCBeat’s values and methodology. Stay tuned.

Limited-Time Special Ticket Offer

Scan the QR code to register

Certainly,“New Structure” – 2018 Primary Healthcare Innovation Practice SummitIn addition to the Third-Party Medical Imaging Development ForumFrontier Forum, in addition, there are alsoForum on Innovation and Practical Development of Medical Consortiums, Frontier Forum on Chronic Disease and Health Management, Forum on the Development of Pharmaceutical Retail and Distribution, Forum on Clinic Development, Forum on the Development of Third-Party Hemodialysis Centers, and five other major forums. The conference has invited more than 70 industry leaders to gather in Hangzhou, looking forward to meeting you!

We have always approached the study, documentation, and exploration of developments in the third-party medical imaging sector with a sense of humility and reverence. By scanning the QR code at the end of this article to join our community, you will gain access to 37 primary care reports authored or curated by VCBeat’s VBInsight. Additionally, you will connect with like-minded professionals who share your interest in Medical Consortiums, facilitating meaningful exchanges.