India's $50 Billion Generics Empire: How State-Backed 'Copycat' Policies Built the World's Pharmacy

Traveling to India to purchase medications has become the last resort for many patients and their families confronted with exorbitantly priced “life-saving drugs.” Underpinning this phenomenon is India’s highly developed generic drug industry. The country is home to nearly 3,000 generic pharmaceutical manufacturers, accounting for approximately 20% of global generic drug exports, which reached $16.89 billion in 2016.

VCBeat (WeChat ID: vcbeat) has reviewed the historical development and market overview of India’s generic drug industry, aiming to address the following questions: Why is India’s generic drug industry so robust? What are the underlying policy and industrial contexts? What insights can China draw from the development of India’s generic drug sector? Where is India’s generic drug industry headed in the future? As another developing country with relatively weak pharmaceutical innovation capabilities, how can China strike a balance between the interests of innovative drug companies and those of patients?

As of 2015, India had 10,500 pharmaceutical manufacturing units (factories) and more than 3,000 pharmaceutical companies. In terms of scale, the Indian pharmaceutical market accounted for approximately 2.4% of the global market by value, while its share of global pharmaceutical production volume reached 10%.

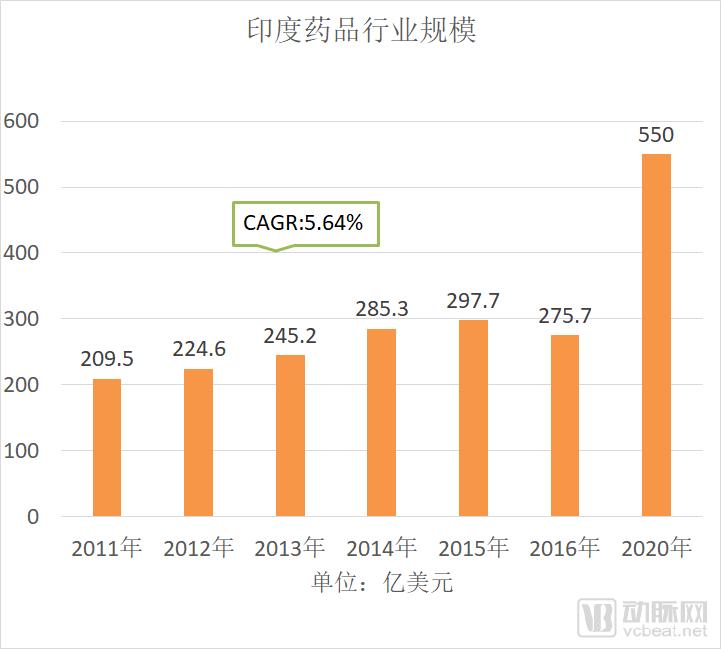

In 2016, the size of India's pharmaceutical market was USD 27.57 billion, with a compound annual growth rate (CAGR) of 5.64% from 2011 to 2016. Driven by factors such as increased government healthcare expenditure and favorable generic drug policies, the market is projected to maintain a CAGR of 12.89% from 2015 to 2020, reaching USD 55 billion by 2020.

Source: IBEF; Chart by VCBeat

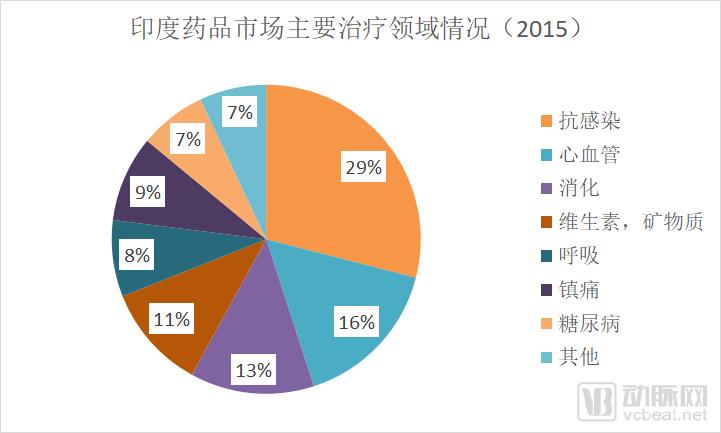

In terms of market structure, generic drugs account for approximately 70% of India's pharmaceutical market, over-the-counter (OTC) drugs for 21%, and patented drugs for 9%. The top-selling drugs are primarily indicated for anti-infective, cardiovascular, gastrointestinal, and vitamin-related conditions. The top five therapeutic subsegments collectively represent 57% of the market, a pattern similar to those observed in the global and Chinese markets.

Source: IBEF; graphic by VCBeat

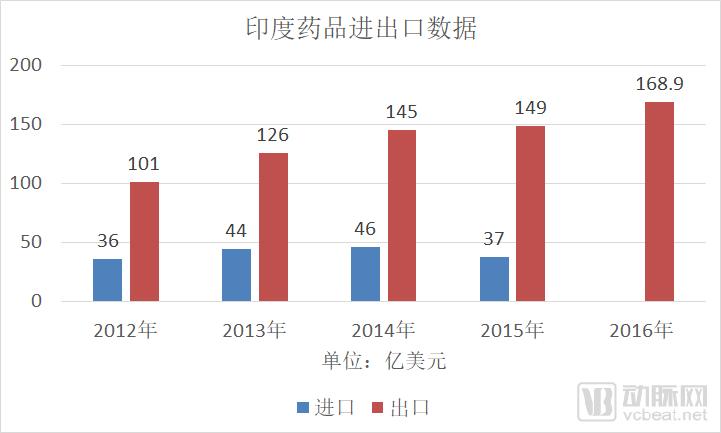

India is a major exporter of generic drugs, accounting for approximately 20% of global generic drug exports. In fiscal year 2016, India’s generic drug exports were valued at $16.89 billion, representing a growth rate of 9.44%. The export value is projected to reach $40 billion by 2020.

Source: IBEF; graphic by VCBeat

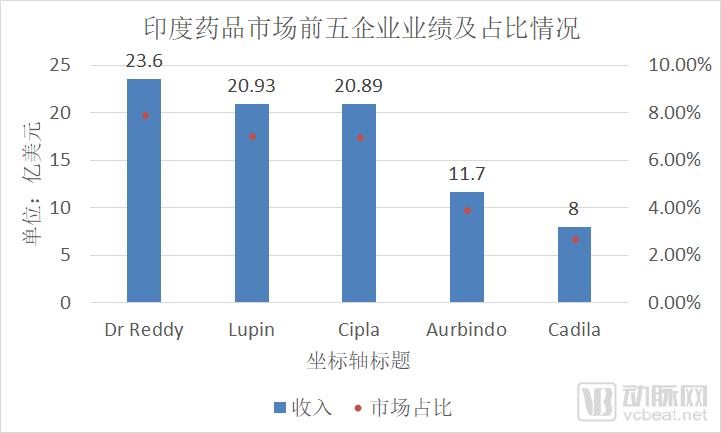

The top five pharmaceutical companies in India are Dr. Reddy’s, Lupin, Cipla, Aurobindo, and Cadila. Dr. Reddy’s reported revenue of $2.36 billion in fiscal year 2016, Lupin reported $2.093 billion, and Cipla reported $2.089 billion.

India’s pharmaceutical market is highly concentrated. Based on data from fiscal year 2015, the top four pharmaceutical companies accounted for approximately 20% of the Indian market, while the top ten held around 40%.

Source: IBEF, chart by VCBeat (Note: Aurbindo’s data is from FY2015; market share is calculated based on FY2015 figures)

Top 10 Predictions for the Future Development Trends of India’s Pharmaceutical Industry:

High R&D Investment.Indian pharmaceutical companies invest 8–11% of their total revenue in research and development (R&D); increased R&D spending will help them strengthen their R&D capabilities, secure more drug patents, and boost sales.

Generic drug exports continue to grow.The generic drug business is a key driver behind the expansion of India’s pharmaceutical market, and exports of generic drugs are expected to continue growing rapidly in the coming years;

Increased international cooperation.Multinational corporations are collaborating with Indian pharmaceutical companies to develop new drugs. For instance, Cipla has established an exclusive partnership with the Serum Institute of India to distribute vaccines in South Africa. Additionally, six leading pharmaceutical companies have formed a consortium named “LAZOR” to share best practices, thereby enhancing efficiency and reducing operational costs.

Indian Domestic Pharmaceutical Companies Expand Overseas.For instance, Cipla is establishing a $32 billion facility in Africa to produce antiretroviral and antimalarial drugs, making it currently the largest supplier of antimalarial medications in Africa;

Public-Private Partnership (PPP) in the R&D Sector.The Indian government has invested billions of dollars and social capital to establish joint venture funds; in April 2017, Clavita Pharmaceuticals and GITAM (Gandhi Institute of Technology and Management) University signed a cooperation agreement, under which both parties will collaborate on personnel exchanges, joint conferences, and staff training.

Patent Law Reform.The Ministry of Commerce and Industry promulgated the Draft Patent (Amendment) Rules in 2015, which came into effect in 2016. These rules reduced the time limit for filing enterprise patent applications from the previous 12 months to 4 months, thereby shortening the overall acceptance period. However, taking into account the adaptation process for enterprises, the filing deadline may be extended by an additional 2 months, up to a total of 6 months, upon submission of additional supporting documentation and payment of prescribed fees. This measure is part of the “Make in India” reforms.

An Increase in Product Patents.India has reaffirmed its commitment to intellectual property protection, which has spurred a surge in patent applications; for instance, in December 2016, Suven Life Sciences obtained a patent for a product used in the treatment of neurasthenia.

Faster Approval Times.To compete with global players, India has significantly streamlined its drug approval process, substantially reducing the time to market for new drugs.

The Era Dominated by Foreign Pharmaceutical Companies Before 1970;

1970-1990, Indian local pharmaceutical companies began to develop;

From 1990 to 2010, local generic drug manufacturers achieved comprehensive development and simultaneously initiated the export of active pharmaceutical ingredients (APIs) and generic drugs;

Since 2010, Indian pharmaceutical companies have begun to focus on R&D innovation, challenging the innovative drug market.

Source: IBEF; Chart by VCBeat

Policies serve as the cornerstone for cultivating India’s pharmaceutical industry. Through measures such as patent laws, compulsory licensing of patents, and regulations on compound patent grants, India has laid the foundation and bought time for the development of its domestic pharmaceutical enterprises.

Prior to 1970, India implemented the internationally prevalent product patent system for pharmaceutical compounds. Patents held by foreign pharmaceutical companies were strictly protected, while domestic firms had weak R&D capabilities and were virtually unable to compete with their foreign counterparts.

To address this situation, India enacted the Patents Act in 1970, breaking the patent monopoly held by foreign pharmaceutical companies. Specifically, the law distinguished between product patents and process patents, with protection granted only to process patents. This allowed Indian domestic pharmaceutical firms to reverse-engineer and produce generic versions of foreign companies’ products. Additionally, the 1970 Patents Act significantly shortened the term of patent protection for pharmaceuticals.

While wielding the patent stick, India also enacted the Drug Price Control Order (DPCO), primarily aimed at setting price ceilings for specified high-volume active pharmaceutical ingredients (APIs) and key formulations. This measure ensures that consumers can access medicines at lower prices and restricts pharmaceutical companies from reaping excessive profits. This approach has effectively reduced drug prices but has also hindered the operations of foreign pharmaceutical companies in India. The Drug Price Control Order was amended multiple times in 1979, 1995, 2002, and 2012, further squeezing the profit margins of manufacturers, distributors, and retailers.

In 1994, the General Agreement on Tariffs and Trade (GATT) decided to establish the more globally oriented World Trade Organization (WTO). As a GATT member state, India acceded to the WTO in 1995 through direct transition. Following its accession, India signed the Agreement on Trade-Related Aspects of Intellectual Property Rights (TRIPS). TRIPS mandates strengthened international protection of intellectual property rights and aims to reduce distortions and barriers in international trade, thereby promoting the development of the global economy and trade. This necessitated aligning India’s Patents Act of 1970 with the TRIPS Agreement.

However, India’s status as a developing country granted it a ten-year transition period for the formal implementation of the TRIPS Agreement, deferring its entry into force in India until 2005. Between 1995 and 2005, India amended its Patent Act multiple times to gradually align its patent protection framework with TRIPS requirements. In 2004, India promulgated the Patents (Amendment) Ordinance, 2004, which extended patent protection to both pharmaceutical products and processes, and set the term of protection at the internationally standard 20 years.

Over the 35 years from 1970 to 2005, India leveraged its “unique” pharmaceutical patent protection regime to carve out development space for domestic pharmaceutical companies. By producing generic drugs, Indian pharmaceutical firms gradually integrated with the international market, thereby achieving the “primitive accumulation” of India’s pharmaceutical industry.

Although the passage of the new Patent Act means that Indian pharmaceutical companies must prioritize patent protection, two other policies introduced by India continue to leave room for the ongoing development of the country’s generic drug industry. These two policies are “patent validity” and compulsory licensing.

As previously mentioned, India was required to comply with the TRIPS Agreement starting in 2005 following its accession to the WTO, which meant that generic drugs were likely to face risks of patent infringement. However, within the TRIPS framework, India introduced considerations of timing and efficacy into its pharmaceutical patent protection: the Patent Act only provides protection for new drugs invented after 1995 or for modified drugs that demonstrate a significant enhancement in therapeutic efficacy, and does not support patents for derivative drugs.

In practice, many pharmaceutical companies launch combination or derivative drugs based on existing medications before their patents expire, thereby securing new patent protection. Major global pharmaceutical markets also uphold patent rights for such derivative drugs. Among the thousands of new drug applications submitted annually, a significant proportion consists of these derivative products. India’s approach, which partially disregards the patent validity of derivative drugs, effectively reopens a backdoor for its domestic generic pharmaceutical manufacturers.

Moreover, India has fully leveraged its “advantage” as a developing country by implementing compulsory patent licensing for pharmaceuticals, arguing that despite low national income, its population should have access to cutting-edge medicines.

Compulsory patent licensing is also “legally grounded.” Under the TRIPS Agreement, World Trade Organization members may use patented technology without the patent holder’s consent, provided that such use is authorized by the state in accordance with law and that adequate remuneration is paid to the patent holder. Relying on this provision, India can impose compulsory licenses on drug patents for reasons including public interest, Indian traditional knowledge, and public health.

India’s 2004 Patent (Amendment) Ordinance further expanded the scope of “compulsory licensing” for patents, extending it to cover medicines for cancer, chronic diseases, and other conditions. It also permitted India to export generic versions of such drugs to countries and regions lacking manufacturing capacity, thereby laying the foundation for the global market presence of Indian generic pharmaceuticals.

It is worth noting that in 2012, the State Intellectual Property Office of China issued the Measures for Compulsory Licensing of Patent Implementation, which stipulates that, for the purpose of public interest, a request may be made to grant compulsory licenses for the manufacture of patented pharmaceutical products and their export to least-developed countries or regions, as well as to developed or developing members of the World Trade Organization (WTO) that have notified the WTO in accordance with relevant international treaties of their intention to act as importers.

India’s pharmaceutical industry has carved out a distinctive path with unique “Indian characteristics.” As one of the world’s largest exporters of generic drugs, India annually supplies low-cost generics to more than 100 regions worldwide, significantly enhancing global patients’ access to medications. Due to the affordability of these generic drugs, patients from some developed countries also choose to seek medical care or treatment in India, earning the country the nickname “the Pharmacy of the World.”

The IBEF report indicates that India’s production costs are nearly 33% lower than those in the United States, its labor costs are approximately half those of Western countries, and the cost of establishing manufacturing facilities in India is only 60% of that in the West.

In addition to cost advantages, a skilled professional workforce and management standards aligned with those of Europe and the United States are key factors behind the rise of India’s generic drug industry. India’s generic drug regulations are well-established, with most practices adhering to U.S. FDA guidelines. There are 546 pharmaceutical manufacturing facilities in India that have received FDA approval, and 2,633 drug products have been approved by the FDA. The United States has become a major export market for Indian generic drugs, with 40% of generic medicines sold in the U.S. sourced from India.

Many developing countries and international organizations have also spoken highly of Indian generic drugs. The World Health Organization, Médecins Sans Frontières, and other entities purchase large quantities of Indian generic medicines annually. Former UN Secretary-General Ban Ki-moon highlighted the significant role of generic drugs in the “United Nations Millennium Development Goals Report,” stating that the development of the generic drug industry is a crucial guarantee for improving healthcare standards and public health in Third World countries. He expressed appreciation and affirmation for the efforts made by India and other nations to strengthen the production of low-cost generic drugs.

Driven by factors such as low prices and rapid market availability, China has also become a major consumer of Indian generic drugs. Some individuals and organizations provide patients with affordable medications through private purchases and cross-border medical services. However, under China’s drug regulatory policies, any drug not registered through the formal approval process is classified as a “counterfeit drug,” and purchasing agents for such products are engaged in illegal activities. Nevertheless, driven by profit motives and the urgent needs of patients, Indian generic drugs have become “life-saving medicines” for many patients.

While India’s generic drug industry has gained public approval for its “Robin Hood” approach, it has significantly harmed the interests of originator drug manufacturers, prompting numerous pharmaceutical companies to file lawsuits against Indian generic firms. A prominent case is the compulsory patent licensing dispute between the multinational pharmaceutical company Bayer and the Indian generic manufacturer Natco Pharma.

In 2005, Sorafenib (sold under the brand name Nexavar), a multi-targeted new drug developed by Bayer for the treatment of advanced renal cell carcinoma, received FDA approval. In 2007, Bayer obtained permission to market the drug in India, where it was priced at €4,300.

At that time, India’s per capita annual income was less than €500, making the drug prohibitively expensive for most Indians. Natco, a local Indian generic pharmaceutical manufacturer, applied to Bayer for permission to produce the drug but was rejected. Consequently, Natco invoked “compulsory patent licensing” and applied to the authorities for a compulsory license to manufacture the drug.

In 2012, the Indian Patent Office approved Natco’s application, allowing Natco to produce Nexavar against Bayer’s wishes and sell it at a price equivalent to €136 per monthly dose. This price was 97% lower than Bayer’s original selling price of €4,300.

Subsequently, India issued compulsory licenses for three patented anticancer drugs: Herceptin (trastuzumab) for breast cancer treatment, Ixempra (ixabepilone) for breast cancer chemotherapy, and Sprycel (dasatinib) for leukemia treatment. These medicines are also high-priced new drugs developed by multinational pharmaceutical companies.

Similar to the situation in India, China is also a major producer of generic drugs. Among the more than 170,000 drugs approved for marketing in China, 95% are generics.

For a long period, China was a major producer of generic drugs but not a leading power in this field. Due to issues such as non-standardized reference listed drugs for evaluation and an imperfect assessment system, the quality of generic drugs has been uneven.

In February 2016, the General Office of the State Council issued the “Opinions on Conducting Consistency Evaluation of Quality and Efficacy for Generic Drugs,” requiring that generic drugs approved for marketing before the implementation of the new classification system for chemical drug registration must undergo consistency evaluation if they had not been approved in accordance with the principle of consistent quality and efficacy with the original reference listed drugs.

For generic chemical drugs in oral solid dosage forms that were approved for marketing before October 1, 2007 and are included in the National Essential Medicines List (2012 Edition), consistency evaluation shall be completed by the end of 2018; for those requiring clinical efficacy trials or involving special circumstances, consistency evaluation shall be completed by the end of 2021.

The "Opinions" also stipulate requirements for the selection of reference listed drugs, evaluation methods, and the primary responsibilities of enterprises.

On May 22, 2018, the National Medical Products Administration (NMPA) announced the fourth batch of drugs that had passed the consistency evaluation. To date, a total of 41 drug varieties have passed the consistency evaluation, among which 12 are included in the 2012 edition of the National Essential Medicines List.

For drugs that are the first to pass the consistency evaluation, there are currently three categories of substantive incentives:

First, appropriate support should be provided in terms of medical insurance payment, and medical institutions should prioritize procurement and clinical use;

Second, if more than three manufacturers of the same drug variety have passed the consistency evaluation, varieties that have not passed the consistency evaluation will no longer be selected for centralized drug procurement and other purposes;

Third, pharmaceutical manufacturers that have passed the consistency evaluation may apply for financial support from central infrastructure investment funds and industrial funds, provided they meet the relevant eligibility criteria.

The consistency evaluation is essentially a “remedial measure” for the previous approval of generic drugs, aiming to bridge the gap between generic and originator drugs by ensuring that generics achieve clinical outcomes equivalent to those of the originators. Consequently, generic drugs with insufficient technical capabilities or low willingness to participate in the consistency evaluation are likely to be gradually phased out.

Generic drugs have laid the foundation for the development of China’s pharmaceutical industry. Currently, China is transitioning from a focus on generic drugs to innovative drugs. In October 2017, the General Office of the Communist Party of China Central Committee and the General Office of the State Council issued the “Opinions on Deepening the Reform of the Review and Approval System to Encourage Innovation in Drugs and Medical Devices.” The document proposed reforms to clinical trial management, acceleration of market approval reviews, promotion of drug innovation and generic drug development, strengthened lifecycle management of drugs and medical devices, and enhanced technical support capabilities. These measures aim to facilitate structural adjustment and technological innovation in the pharmaceutical and medical device industries, thereby improving industrial competitiveness.

While promoting the upgrading of the pharmaceutical industry, the Chinese government has also implemented measures such as price negotiations and tariff reforms to lower the prices of new drugs and improve patient access to medications.

In October 2017, the Ministry of Human Resources and Social Security confirmed the inclusion of 36 high-priced drugs for critical illnesses in the national medical insurance coverage. Compared with the average retail prices in 2016, the average price reduction for these negotiated drugs reached 44%, with the highest reduction hitting 70%. The reimbursement standards for most imported drugs after negotiation were lower than the international market prices in neighboring countries.

Effective May 1, 2018, the value-added tax (VAT) on imported anti-cancer drugs at the import stage will be reduced to 3%.

Price negotiations and tariff reforms represent China’s strategic balancing act between the interests of pharmaceutical companies and those of patients. This approach not only sustains the innovation incentives for R&D-intensive pharmaceutical enterprises but also safeguards patients’ right to access treatment, serving as a compromise between commercial interests and patient rights.

Summary

Leveraging the nation’s resources to engage in “copycat” production and giving a “green light” to intellectual property infringement laid a robust foundation for India’s pharmaceutical industry, enabling its generic drug sector to achieve a market size of $50 billion and gain strong competitiveness in the international market.

However, India did not stop at simple imitation; instead, it established a set of drug production standards aligned with European and American regulatory requirements, thereby laying the groundwork for industrial upgrading.

The evolution of China’s pharmaceutical industry follows a similar trajectory, progressing from generic drugs to an integrated model of prevention and innovation, and ultimately achieving “overtaking on the bend” in the biopharmaceutical sector. Bolstered by favorable policies, capital inflows, and market dynamics, China’s domestic pharmaceutical industry still has a long journey ahead.