After Investing in DHCC and Winning Health, Tencent and Alibaba Gain Entry into Core Healthcare Systems

It is not that Tencent and Alibaba have never attempted to penetrate the healthcare institution market; rather, their previous efforts were too superficial and fragmented. A week after Tencent announced a RMB 1.266 billion capital injection into Donghua Chengxin, acquiring a 5% stake in Donghua Software, Alibaba finally made its move by partnering with Winning Health, another giant in healthcare informatics.

Winning Health announced that the significant matter currently under planning involves individual major shareholders of the company negotiating with Yunxin regarding an equity transfer in Winning Health, with the expected transfer ratio reaching 5% or more. However, this equity transfer will not result in a change of control over the company. Based on recent expressions of intent, both parties plan to engage in deep and comprehensive cooperation in the “Internet + Healthcare” sector and further advance the upgrade of their strategic partnership.

Data from the National Enterprise Credit Information Publicity System shows that Shanghai Yunxin is a wholly-owned subsidiary of Zhejiang Ant Small and Micro Financial Services.

By holding this mere 5% equity stake, Tencent and Alibaba are clearly not seeking corporate decision-making power; their ulterior motive is likely to gain deep entry into the healthcare informatics market and build an ecosystem.

Why Have These Companies Suddenly Become So Sought-After? VCBeat believes that the barriers to entry for healthcare institutions are too high. Apart from mobile payments, healthcare institutions have virtually no rigid demand for internet companies. Therefore, these internet firms urgently need to penetrate the healthcare market through medical IT companies.

Not a hospital's core necessity

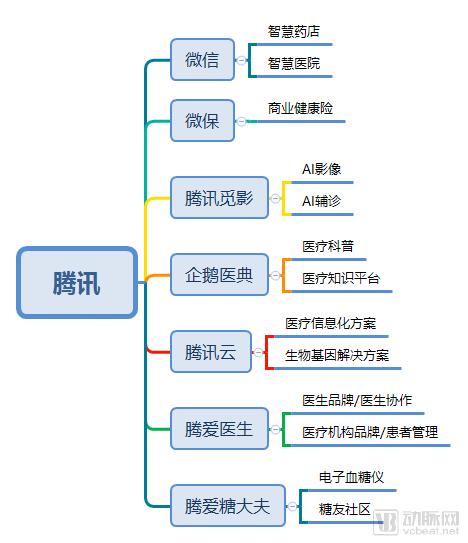

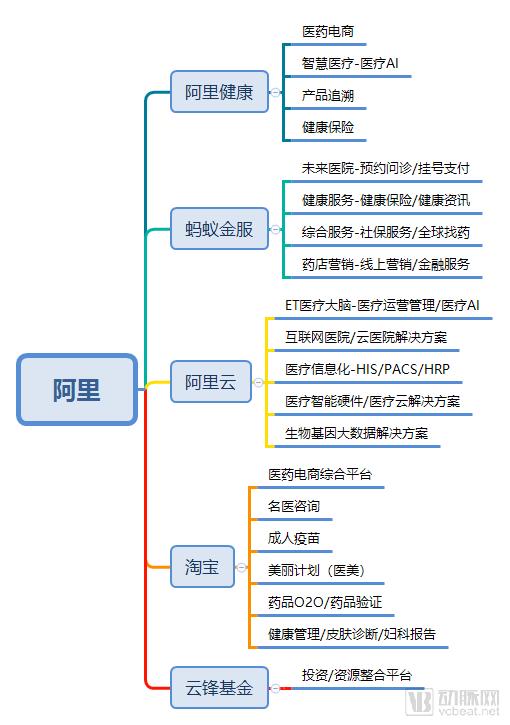

VCBeat has previously analyzed and summarized the respective healthcare industry footprints of Tencent and Alibaba, as follows:

Within this series of products, you will find WeSure (abbreviated as “Weibao”), Tencent’s first majority-controlled insurance platform; Penguin Medical Dictionary, the “encyclopedia” of medical information; Teng Ai Doctor, a social networking platform and toolkit for physicians; and Teng Ai Tang Dafu, an intelligent portable blood glucose meter.

However, the only solution that appears to be closely integrated with healthcare institutions is WeChat Smart Hospitals, which streamline the entire patient journey by connecting key stages: triage (online AI triage and intelligent customer service consultations), appointment scheduling (online registration), consultation (online consultations and offline AI-assisted diagnosis), examinations (offline AI imaging and AI pathology), payment (online payment via medical insurance or commercial insurance, and offline QR code payments using medical insurance), treatment (online medication delivery and offline prescription circulation), and post-visit care (AI follow-ups and online prescription renewals).

Alibaba is no exception. Apart from AliHealth’s pharmaceutical e-commerce business, only Alipay can truly be considered a provider of services to hospitals. Alipay claims to have connected with more than 1,500 public hospitals, covering 30 provinces, municipalities, and autonomous regions across China, as well as nearly 200 cities, and has provided over 300 million instances of convenient services such as real-name appointment registration, mobile payments, and medical report inquiries.

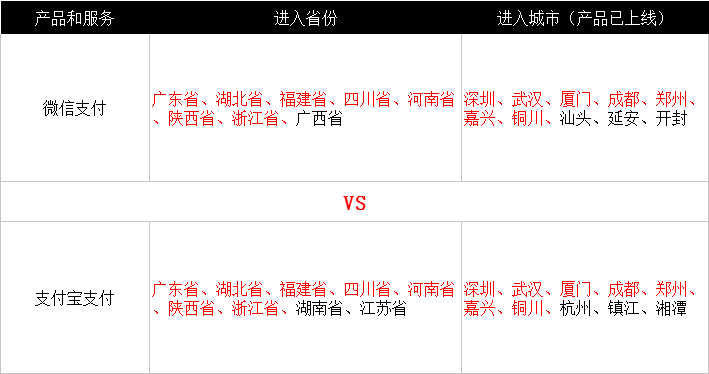

But even with mobile payments, both companies have mostly expanded their markets in second-tier cities or prefecture-level cities.

(Data source: Public information from Tencent and Ant Financial; as of November 2017. Note: Red indicates provinces or regions covered by both WeChat and Alipay.)

Beyond mobile payment solutions, Tencent’s and Alibaba’s products appear to have been implemented only in a piecemeal fashion at individual hospitals, struggling to gain widespread adoption. The primary reason is that healthcare IT has become highly standardized; products not integrated into this standardized framework find it difficult to enter hospitals, as their services are not perceived as true necessities by these institutions.

Hitching a Ride with Industry Leaders

In any industry, leading companies have the most say and even influence industry standardization.

In 2016, the National Health and Family Planning Commission issued the “Notice on Guidelines for Application Functions of Hospital Information Platforms.” This document served as the predecessor to both the “Technical Guidelines for Hospital Informatization Construction (2017 Edition, Trial)” and the “Standards and Specifications for National Hospital Informatization Construction (Trial).” It can be said that companies qualified to participate in the drafting of this document essentially represent the leading enterprises in China’s healthcare informatization industry.

In the “Notice on Guidelines for Application Functions of Hospital Information Platforms,” VCBeat identified this list, which includes Donghua Software and Winning Health.

In addition, there are three industry-recognized standards for hospital informatization in China. They are the National Health and Medical Information Interconnectivity Standardization Maturity Assessment organized by the National Health Statistics Information Center, the "Graded Evaluation Standards for the Application Level of Electronic Medical Record Systems" issued by the Hospital Management Institute of the National Health and Family Planning Commission, and the HIMSSEM RAM rating.

The assessment criteria covered by these standards currently lack corresponding solutions from domestic internet companies. Consequently, you will not find Tencent or Alibaba listed among the participants in these three major informatization rating standards; instead, the participants are predominantly major medical IT giants.

For example, in 2014, the Information and Statistics Center of the National Health and Family Planning Commission announced that the first batch of three regions and four hospitals had passed the assessment of standardized maturity levels for regional (hospital) information interoperability. The First Affiliated Hospital of Zhejiang University School of Medicine successfully passed the assessment, with the project constructed by YiHui Technology.

In early May 2016, Donghua Company successfully won the bid for the Beijing Hospital Information Platform Construction Project. Subsequently, the development and implementation team from the Medical and Health Department was stationed at Beijing Hospital, where they jointly established the Hospital Information Platform Project Team with the hospital. After nearly one month of investigation and demonstration by the Donghua technical team, the Hospital’s Information Department, and relevant departments, a construction plan for the hospital information platform was established. This plan adopted passing the Interconnectivity Standardization Maturity Assessment as the standard, with the goal of achieving Level 4 Grade A certification.

In May 2017, after on-site testing and review by an expert panel, Beijing Hospital was officially certified as achieving Level 4, Class A in the “Assessment of Standardization Maturity for Hospital Information Interconnectivity.”

Image source: DHC Software

In June 2017, Shanghai Sixth People’s Hospital officially passed the on-site review for HIMSS EMRAM Stage 6. In its collaboration with Winning Health, Shanghai Sixth People’s Hospital comprehensively implemented a range of informatics solutions from Winning Health’s portfolio, including pharmaceutical logistics, closed-loop blood transfusion management, and clinical decision support systems. The effectiveness of these implementations received high praise from the review team during the assessment.

In the internet industry, Tencent and Alibaba are absolute standard-bearers.

On April 6, 2016, the National Technical Committee on E-commerce Standardization was established in Hangzhou. Liu Ping’an, Chairman of the China Brand Construction Promotion Association, served as the Director, and Jack Ma, Chairman of the Board of Alibaba Group, served as the Deputy Director. The primary mandate of the Committee is to develop and improve standards relevant to the e-commerce sector.

Alibaba dominates e-commerce, while Tencent leads in social networking; both wield significant influence across their respective business ecosystems, which encompass logistics, ride-hailing, and internet finance. However, in the healthcare sector, neither Tencent nor Alibaba has been able to penetrate the core. Consequently, they have had no choice but to partner with industry leaders.

Alibaba’s prior series of capital injections appeared more like a rehearsal before opening up new battlefields. (On May 19, 2017, Hongyun Jiukang, a subsidiary of Alibaba Health, invested RMB 291 million in Jiahe Meikang, a domestic provider of clinical information software. In October 2017, Alibaba Health fully underwrote Mandala’s private placement worth RMB 64.3478 million through cash subscription.)

Collaboration is only the beginning; what matters most is clarifying the business direction and identifying the optimal synergy between both parties.

The Cloud Era Officially Begins

Most products offered by internet companies are built on cloud architectures. In the past, due to security concerns and limited policy support, initiatives by Tencent and Alibaba appeared cautious and incremental, with exploratory collaborations primarily conducted through the signing of strategic cooperation agreements. For example:

In July 2017, Tencent and China Electronics Data initiated a strategic partnership to establish a secure cloud platform for medical big data.

In July 2017, Yilianzhong partnered with Tencent to promote WeChat-based mobile online payment for medical insurance services across nearly 100 hospitals.

In September 2017, Tencent Cloud and Wanda Information signed a strategic cooperation agreement to conduct in-depth collaboration in the fields of smart city development and smart retail.

……

Even Alibaba Cloud, the leader in China’s public cloud market, can only operate on the periphery of the healthcare sector.

For example, a three-tier architecture comprising the infrastructure layer, the Apsara distributed cloud operating system layer, and the cloud and big data layer was provided for the Tianchi Medical Competition (Artificial Intelligence Pulmonary Nodule Algorithm Competition). The cloud and big data layer consists of Alibaba Cloud’s self-developed cloud computing products (ECS, NAS, SLB, VPC) and big data products (ODPS, PAI).

In the competition, 90% to even 95% of the teams utilized 3D solutions. Alibaba Cloud’s Apsara PAI, leveraging its robust linear scalability, provides specialized solutions for 3D workloads. Competing teams can process more than 32 volumes of 128x128x128 or even larger-scale 3D images per iteration at high speed, thereby enhancing the accuracy and effectiveness of nodule detection.

and collaborating with genetic companies to provide storage and data analysis services to gene sequencing enterprises through various pricing models, such as pay-per-computation and monthly or annual subscription plans.

Alibaba Cloud Object Storage Service (OSS) offers three storage classes: Standard, Infrequent Access, and Archive. Standard storage provides rapid real-time access, while Archive storage requires a restoration time of less than one minute before data can be accessed. Data that does not require frequent access is better suited for Infrequent Access or Archive storage, which are more cost-effective.

For instance, when genetic companies need to conduct research and analysis on genomic data, they frequently access such data, necessitating the use of standard storage. In contrast, for historical data, such as user sequencing data from several years ago, low-frequency or archival storage is typically employed.

Internet giants such as Tencent and Alibaba naturally aspire to integrate data from various hospital information systems and store it on cloud platforms, but this initiative faces significant challenges. The prevailing industry consensus is that hospital data is highly sensitive and subject to stringent confidentiality requirements, particularly concerning patient privacy. Hospitals impose rigorous demands on the real-time performance, stability, and security of their systems and medical data.

Article 5 of the Cybersecurity Law of the People's Republic of China clearly stipulates: The State shall take measures to monitor, prevent, and handle cybersecurity risks and threats originating from within and outside the People's Republic of China, protect critical information infrastructure from attacks, intrusions, interference, and destruction, punish cyber illegal and criminal activities in accordance with the law, and safeguard the security and order of cyberspace.

Precisely due to the protection of national medical data, hospital information management departments place significant emphasis on the background of cloud computing companies and maintain a conservative stance toward cloud products offered by foreign enterprises such as AWS and Microsoft. Consequently, in terms of cloud product selection, companies like Alibaba Cloud and Tencent Cloud have relatively greater opportunities.

Furthermore, physicians place significant importance on medical data, particularly in the context of scientific research, and are often reluctant to store such information on cloud platforms. Currently, hospital cloud adoption primarily encompasses non-core clinical systems, such as office automation and health examination systems. However, hospitals remain hesitant and conservative about migrating core clinical systems—such as Electronic Medical Records (EMR), Hospital Information Systems (HIS), and Laboratory Information Systems (LIS)—to the cloud.

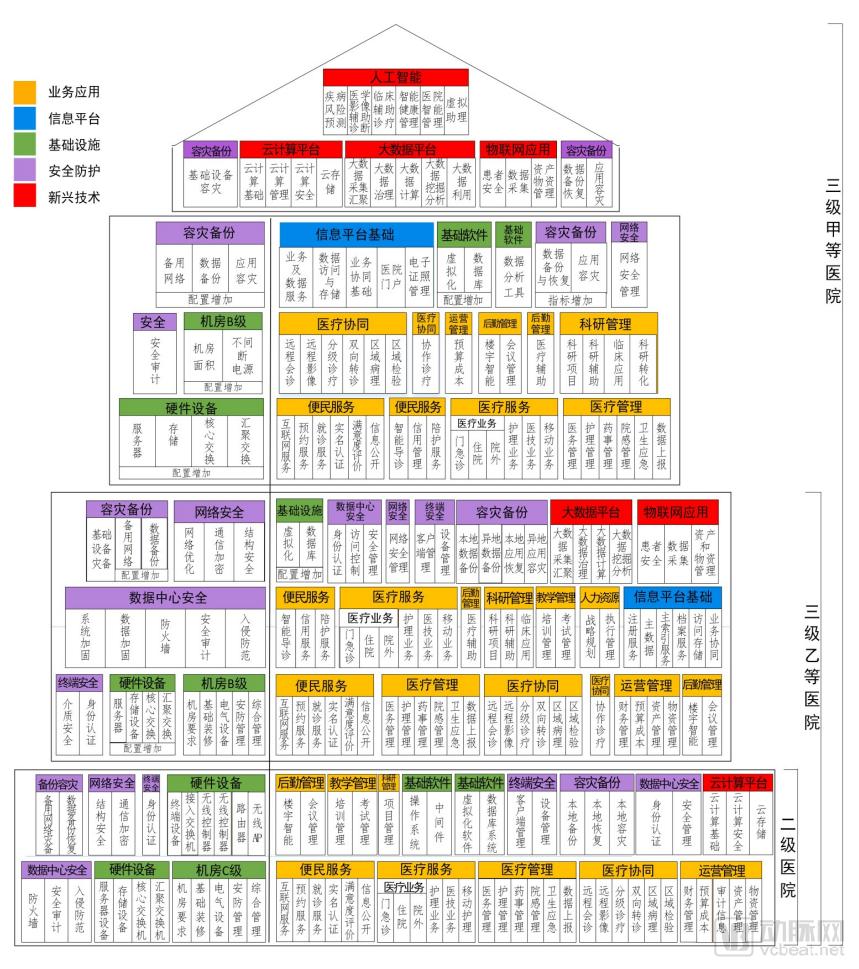

Until the introduction of a standard document. In April 2018, to promote and regulate hospital informationization construction, the National Health Commission formulated the “National Hospital Informationization Construction Standards and Specifications (Trial)” (hereinafter referred to as the “Construction Standards”). The document comprises five chapters and 22 categories, with a total of 262 specific items, clearly defining the content and requirements for hospital informationization construction in the next phase.

In this document, cloud computing, big data, artificial intelligence, and the Internet of Things (IoT), as emerging technologies, occupy the highest tier in the informatization architecture of Grade A tertiary hospitals. For Alibaba and Tencent, which rank first and second in China’s public cloud market, the long-awaited opportunity has finally arrived.

Future: A New Market Landscape?

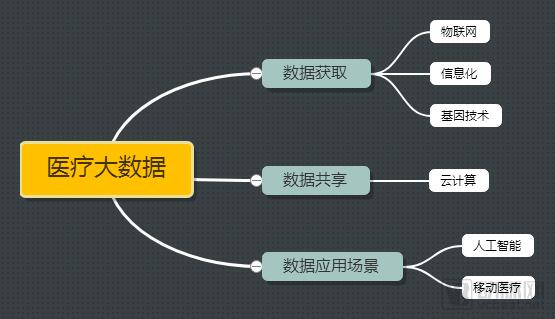

“Cloud, Big Data, IoT, Mobile, and AI”—the diagram below essentially illustrates the relationships among these technologies:

According to Sun Weifeng, Industry Director at the Mobile Informationization Research Center, partnering with healthcare industry system integrators is the primary strategy for deploying medical clouds. Integration with hospitals’ underlying systems represents the most critical—and challenging—link in the entire hospital cloud industry chain. Both internet companies and traditional IT vendors have made collaboration with healthcare system integrators their entry point, leveraging this partnership as a breakthrough to penetrate the underlying systems of the healthcare industry.

In this context, competition in the medical cloud sector will ultimately evolve into a contest of strength and resources among these partners. The competitive landscape for medical clouds will no longer be characterized by individual efforts, but rather by team-based strategies formed through alliances.

The key lies in the word “alliance.”

On May 16, Inspur initiated the establishment of China’s first Strategic Alliance for the Health and Medical Big Data Industry Ecosystem. The inaugural cohort of alliance members comprises more than 30 organizations, including Xiamen Zhiye, Miaoyijia, Huajian Lanhai, Kangfuzi, Renhe Future, Shandong University, and Jinan Industrial Development Investment Group.

Similar to Inspur, in 2018, CEC Health Fund successively invested in Medlinker, a verified physician platform; Unisound, an IoT and AI service provider; Senyi Intelligence, a medical natural language processing company; and Chuanshi Technology, a supply chain technology enterprise in the pharmaceutical industry. The total investment amount for these four deals approached RMB 700 million.

Although these two health and medical big data companies frequently interact with healthcare enterprises, their approaches differ fundamentally. One adopts industrial alliance partnerships, while the other pursues equity investment. Recent developments indicate that the health and medical big data industry has officially entered a phase of territorial consolidation and integration.

Alliances and Coalitions: This inevitably brings to mind that Tencent’s and Alibaba’s series of moves appear to be closely linked to big data in health and healthcare.

Following Tencent’s investment, Han Shibin, Vice President of Donghua Software, stated: “The core value of Donghua Software lies not in its net profit, but in healthcare big data. Thirty percent of the top 100 hospitals across China use Donghua’s Hospital Information System (HIS), and the accumulated big data from this segment holds substantial value.”

Thus, it is evident that big data in health and healthcare is one of the key factors driving collaboration between internet giants and medical IT giants.

In particular, the “Opinions on Promoting the Development of ‘Internet + Healthcare’” issued by the General Office of the State Council on April 28 specifically highlighted internet hospitals, telemedicine, interoperability and information sharing, and family doctor contracting services, thereby charting a clear course for new market opportunities for health IT companies.

As bottlenecks in traditional hospital information systems begin to emerge and penetration by internet companies intensifies, a new generation of cloud-based products—characterized by integration, unification, intelligence, and enhanced connectivity—is poised to become the focal point of hospital informatization upgrades. This explains why Alibaba, which rarely participates in medical informatization conferences, made a high-profile debut with its DingTalk Future Hospital solution at the 2018 China Hospital Information Network Conference. The core of DingTalk Future Hospital lies in its ecosystem and cloud infrastructure.

According to VCBeat, partners for DingTalk Future Hospital will undergo rigorous screening. DingTalk will authorize qualified medical ecosystem partners in each region to oversee the comprehensive implementation of DingTalk Future Hospital in their respective areas. In other words, any healthcare IT company that passes the screening process can join the information service system built by DingTalk.

Image source: Sohu Health

The implementation of traditional healthcare IT solutions has been hospital-centric and relatively fragmented. Each hospital is required to invest substantial human, material, and financial resources, resulting in limited economies of scale. The domestic traditional healthcare IT sector is led by more than ten listed companies, including Donghua Software, Winning Health, Neusoft Group, and Wanda Information. After nearly two decades of development, the market landscape has largely stabilized; however, a true Matthew Effect has not emerged, and industry concentration remains low.

Meanwhile, industrial alliances formed between healthcare IT companies and internet giants such as Tencent and Alibaba, driven by big data in health and medicine, may come to dominate the new landscape of the healthcare informatization market in the future.