2018 China New-Model Clinic Operation Report: Insights from 200 Clinics Across 15 Cities and Tens of Thousands of Data Points

Starting from top-level design, policy constraints on physicians establishing clinics have been gradually lifted, and the number of clinics is expected to grow at an annual rate of 6,000–7,000. Is operating a clinic truly a viable business? Is it difficult to establish a clinic? Is it challenging to manage one? What is the biggest obstacle to scaling into a chain? Should one target the high-end or low-end market? Is it better to locate in residential areas or commercial districts?

It is believed that clinic operators raise many relevant questions before entering this industry. However, no matter how many questions there are, they cannot stop doctors from starting their own businesses or prevent private capital from entering the clinic sector. As primary healthcare practice venues, clinics require relatively small investments and have simpler operations. Nevertheless, surveys indicate that profitability remains a widespread challenge for new-type clinics in China. So, what is the way forward for clinics?

VCBeat has interviewed the heads of dozens of new-type clinics. Meanwhile, researchers at VBInsight collected data from over 200 clinics of various types over a two-month period, conducted on-site visits to more than 80 clinics—including well-known new-type clinics in the industry—and held face-to-face interviews with founders and managers, thereby completing this “2018 Report on the Operation of New-Type Clinics in China》. During the interviews, VCBeat designed a survey questionnaire covering more than 30 dimensions related to clinic operations and conducted detailed analysis and research on the data.

This report will analyze the current development status, configuration, operational performance, and business strategies of new-type clinics in China. We believe that VCBeat’s insights and foresight in the clinic sector will be made more precise and compelling through data-driven evidence.

I. Industry Insights

Clinics, situated at the very end of China’s healthcare network, are characterized by high fragmentation, large numbers, and a relatively low tier. However, this has not prevented clinics from becoming a hot business sector attracting significant capital attention in the current stage. Various stakeholders have begun to increase their investment in and development of clinics. A wave of clinic openings is on the rise.

When physicians enter the market to launch their own ventures, establishing a clinic is an excellent option, characterized by low capital requirements and self-assumed risks. Private capital also faces the choice between building hospitals or clinics when entering the healthcare sector. Hospital investments are capital-intensive, requiring hundreds of millions or even billions of yuan, and involve a lengthy ramp-up period. In contrast, clinics require significantly less investment, offer substantial market capacity, and have become the primary offline healthcare channel for many internet healthcare companies. Furthermore, in the past two years, prominent physician influencers, foreign-funded healthcare institutions, and publicly listed companies have all actively invested in and expanded their clinic networks.

The diversification of clinic investors has also driven the upgrading of clinic formats and types. A large number of newly emerged clinics near communities have gradually evolved from the small and substandard image in our impression to small yet exquisite establishments. Compared with traditional clinics, new-type clinics have achieved significant improvements in terms of environment, service quality, service capacity, and convenience of medical access.

II. New-Type Clinics Enter Their Prime Development Phase

2.1 Policies on Establishing Clinics Are Being Fully Liberalized

Against the backdrop of deepening healthcare reform, encouraging private investment in healthcare has become an inevitable trend in the development of the medical industry. The key to improving the efficiency and quality of China’s healthcare service system lies in promoting tiered diagnosis and treatment, thereby adjusting the supply of medical services through optimized resource allocation. The national access policies for social capital entering the healthcare service sector have undergone a process of continuous deepening and refinement, evolving from macro-level frameworks to micro-level implementations.

2.2 Policy-Driven Entry of Social Capital into the Clinic Sector

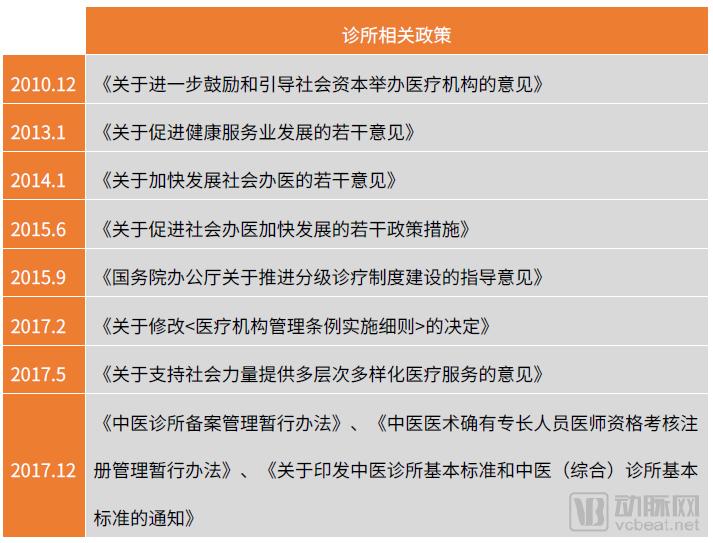

First, vigorously promote privately run medical institutions and introduce private capital. The state has consistently provided strong support for privately run medical services, with progressively fewer restrictions on the entry of private capital into the healthcare sector. The "Opinions on Further Encouraging and Guiding Social Capital to Establish Medical Institutions," issued in November 2010, explicitly encouraged social capital to enter the medical services field.

Subsequent policies have gradually lifted restrictions on the geographic regions and service scopes for non-public medical institutions. These measures aim to cultivate a large number of socially run healthcare providers with strong service competitiveness, establish several influential clusters of specialized health service industries, ensure that service supply basically meets domestic demand, and progressively form a new pattern of multi-tiered and diversified medical services.

In May 2017, the State Council issued the “Opinions on Supporting Social Forces in Providing Multi-level and Diversified Medical Services,” which provided specific guidelines for opening medical service institutions to social capital in areas such as market access, approval services, investment cooperation, and opening-up. The policy supports privately run medical institutions in introducing strategic investors and partners, and attracts overseas investors to establish high-level medical institutions in China through joint ventures and cooperative arrangements.

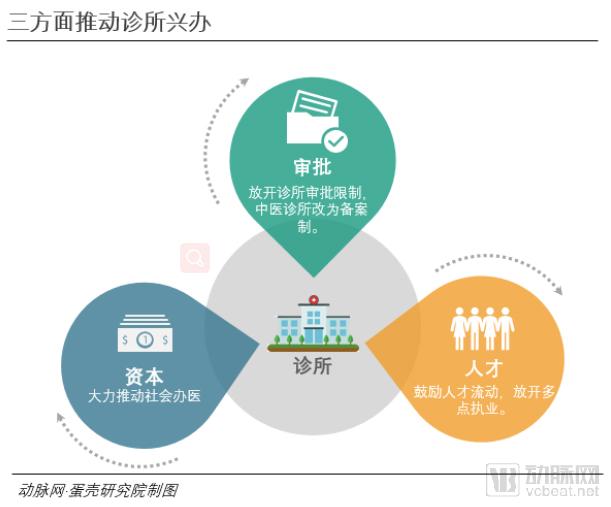

Second, relax restrictions on clinic approval. The establishment of medical institutions is highly complex, often requiring sponsors to expend significant human and material resources. Appropriately easing approval criteria and streamlining the approval process are crucial for private capital. Meanwhile, policies are also relaxing various requirements, such as market access for physicians establishing general practice clinics and inclusion in medical insurance programs, while removing planning restrictions and limitations on departmental configurations at the time of clinic establishment, thereby substantially reducing the barriers to setting up clinics.

In March 2015, the General Office of the State Council issued the Outline Plan for the National Healthcare Service System (2015–2020), which explicitly stated that the establishment of individual clinics is not subject to planning and layout restrictions. In May 2017, the Opinions on Supporting Social Forces in Providing Multi-level and Diversified Medical Services further emphasized that competent authorities shall not impose any restrictions on private medical institutions that meet planning conditions and access qualifications, while streamlining and integrating approval procedures. Reasonable flexibility may be granted in planning reservations for the allocation of large-scale medical equipment by socially run medical institutions. The establishment of individual clinics is not subject to planning and layout restrictions.

The most significant change came with the Interim Measures for the Record-filing Administration of Traditional Chinese Medicine (TCM) Clinics, promulgated in December 2017. Under the new policy, entities establishing TCM clinics may commence practice after filing records with the local county-level administrative department of traditional Chinese medicine, submitting information such as the clinic’s name, address, scope of diagnosis and treatment, and staffing arrangements. The traditional clinic approval system involved seven steps—application, public notice, approval of establishment, environmental protection review, fire safety inspection, final acceptance, and license issuance—resulting in a complex, time-consuming process with high entry barriers. With the shift from an approval-based to a record-filing-based system for TCM clinics, the process has been streamlined to just two steps—application and license issuance—allowing for one-time completion.

Third, encourage talent mobility and lift restrictions. The healthcare industry is a service sector that requires skilled professionals. With the continuous advancement of the new healthcare reforms, national-level restrictions on physicians establishing private clinics, engaging in multi-site practice, and even practicing freely have been gradually relaxed in recent years. Policies are liberating physicians from administrative staffing quotas to become independent social practitioners, while providing support for multi-site practice, thereby enabling more highly qualified doctors to serve in community settings.

On September 11, 2015, the General Office of the State Council issued the Guiding Opinions on Promoting the Construction of a Tiered Diagnosis and Treatment System, which explicitly encouraged eligible physicians to establish private clinics. The document clearly stated that physicians from urban hospitals at the secondary level or above should be encouraged to practice at multiple sites, particularly in primary healthcare institutions, through mechanisms such as multi-site practice. Furthermore, it called for vigorous promotion of privately run medical services, simplification of approval procedures for individual medical practice, and encouragement of eligible physicians to open individual clinics.

With top-level design gradually being liberalized, we believe that health policies across various regions will be progressively implemented in the coming years. The policy barriers restricting physicians from opening clinics are being gradually dismantled, and clinics will increasingly account for a larger share of the healthcare service system.

2.3 The Development of Clinics in China from a Data Perspective

2.3.1 The number of clinics increases by 6,000 annually

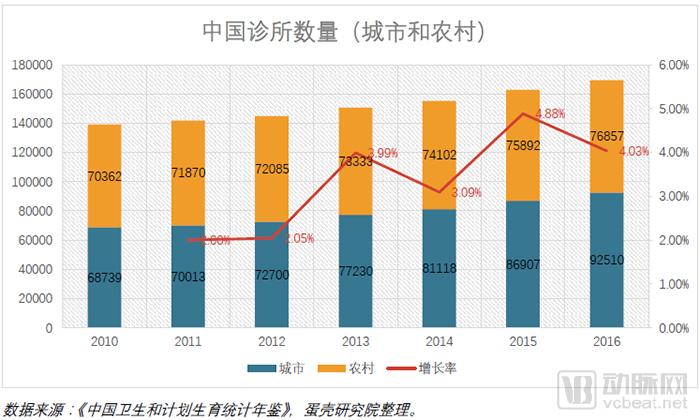

According to public data released by the National Health Commission, the number of clinics has been growing rapidly at a rate of 6,000–7,000 per year since the launch of the new healthcare reform in 2009. Statistical data from the China Health and Family Planning Statistical Yearbook 2017 shows that the number of domestic clinics reached 169,367 in 2016. Among these, the growth rate of urban clinics was significantly higher than that of rural clinics. Over the six-year period, the compound annual growth rate (CAGR) for rural clinics was only 1.48%, whereas the CAGR for urban clinics was 5.07%.

Among clinics, the vast majority are non-public, privately operated facilities. Taking 2016 data as an example, non-public clinics accounted for 96.8% of the total; therefore, the term “clinic” generally refers to private or privately run clinics. The number of public clinics has been steadily declining and is being gradually replaced by privately operated ones.

2.3.2 Where Does the Market Growth in the Clinic Industry Lie?

Although there are numerous individual clinics, their quality is generally low. They face challenges such as a single business model, limited profit growth points, high operating costs, and intense competitive pressure, making it exceptionally difficult for standalone clinics to survive. This situation has created fertile ground for the expansion of clinic chains. To attract more patients, clinics need to shed their traditional image of being small-scale and undifferentiated, and instead draw patients through high-quality, professional services.

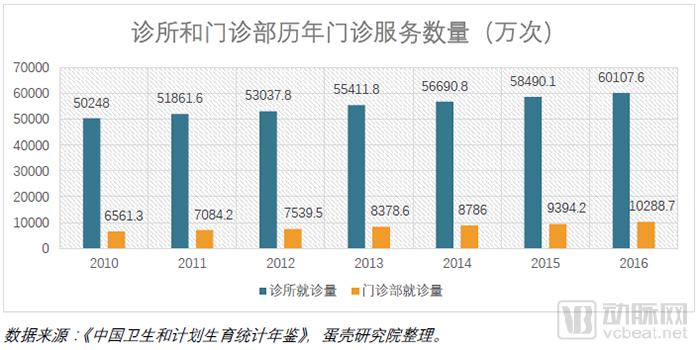

Data indicates that the growth rate of patient visits at clinics and outpatient departments is lower than the expansion rate of the clinics themselves. In other words, as a large number of new clinics emerge in the future, the primary key to success will be increasing patient volume through high-quality medical services and marketing initiatives.

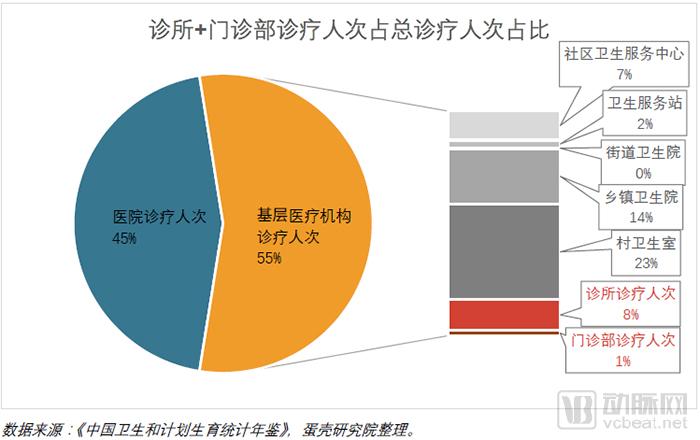

The current objective of China’s healthcare reform is to divert a substantial volume of outpatient visits from hospitals to primary care institutions. Therefore, the trend indicates that hospital outpatient services will shift significantly toward the primary care level. As an important supplement to primary healthcare, clinics will absorb a considerable portion of the patient population. Thus, the first source of incremental patient flow for clinics will come from patients redirected from public hospitals.

In 2016, the total number of patient visits to medical institutions in China reached 7.9317 billion, with 4.366633 billion visits occurring at primary care medical institutions, accounting for over 50%. Among these, the total number of visits to clinics and outpatient departments was 601.076 million, representing only 16.12% of visits to primary care medical institutions and 8.88% of the total patient visits. In the future, the proportion of patients seeking care at clinics is expected to continue rising. The intensive implementation of national policies is poised to drive growth in industries related to primary healthcare, significantly enhancing investment opportunities in the clinic sector.

China’s population is aging rapidly, with nearly one-quarter of its citizens projected to be over the age of 65 by 2050. The country’s stage of social development and demographic shifts have made it imperative to prioritize rehabilitation care, chronic disease prevention and control, and the integration of medical and elderly care services within primary healthcare reform. An increasing number of Chinese people are suffering from non-communicable chronic diseases such as diabetes, endocrine disorders, and cardiovascular diseases. Against the backdrop of an aging society, the existing healthcare system has limited capacity to deliver primary care services for common illnesses, chronic conditions, rehabilitation, and integrated medical-elderly care. Currently, the management of these conditions is concentrated in hospitals, but there is a gradual shift toward community health service centers. Clinics, however, have not yet played their due role in chronic disease management and rehabilitative treatment for the elderly. Therefore, clinics should strategically tailor their departmental structures and target populations to better serve elderly patients with chronic diseases.

The second source of incremental patient volume for clinics stems from enhanced accessibility to medical services, which enables better and faster resolution of residents’ common health issues. According to survey data from PwC’s report “New Entrants and the New Medical Economy,” 38% of consumers forgone medical care when they had healthcare needs in the past year. Aside from symptom alleviation as the primary reason, conflicts with work schedules, conflicts with family responsibilities, and financial considerations accounted for 51%, 35%, and 28% of the responses, respectively.

The above data indicates that enhancing the convenience of healthcare services represents a primary opportunity for new entrants in the medical entrepreneurship sector. By locating clinics within communities, healthcare accessibility is significantly improved, allowing residents to enjoy more convenient medical services. This approach delivers better diagnostic and treatment services for common and chronic diseases, enabling a broader population to access healthcare with greater ease.

The third source of market growth for clinics is medical services targeting the mid-to-high-end population. These clinics represent a new and rapidly growing force in the market, attracting patients through upscale medical environments and compassionate healthcare services. Such clinics better demonstrate the service value of physicians and humanistic care in medicine, providing high-quality, efficient, and convenient medical services. Driven by the wave of consumption upgrades and strong capital interest, the surge in visits to these novel clinics continues to spread across major cities.

III. 15 Cities, 200 Clinics, Tens of Thousands of Data Points: A New Self-Portrait of Clinics

Prominent healthcare providers such as the Mayo Clinic in the United States, Hong Kong’s Quality HealthCare Medical Services, and Singapore’s Parkway Pantai all began as single clinics. Through high-quality medical services and long-term dedication, these clinics grew from small practices into renowned healthcare institutions within the industry.

In recent years, private clinics in China have encountered their most favorable opportunities for development. How, then, should we strengthen our core competencies to seize these opportunities? Key operational considerations include strategic site selection and layout, innovation in business models, strategies for expanding the patient base, and approaches to attracting physicians.

VCBeat Research Institute selected 15 cities across China—Beijing, Shanghai, Guangzhou, Wuhan, Shenzhen, Chongqing, Chengdu, Urumqi, Tianjin, Hefei, Changsha, Kunming, Wuxi, Fuzhou, and Hangzhou—conducting on-site visits to over 80 clinics and collecting data from more than 200 clinics. Through face-to-face interviews with founders and managers, and by analyzing the survey data and interview content, the institute has summarized key management strategies for the development of new-type clinics.

The following data analysis is based on clinic operational data collected by VCBeat Research Institute. The 80 clinics interviewed included more than 20 well-known domestic mid-to-high-end chain clinics, resulting in tens of thousands of words of authentic records on the clinic ecosystem. (As some data dimensions could not be obtained with 100% completeness during the research, the data are presented in percentage form.)

3.1 Big Data Reveals Emerging Trends in New Clinics

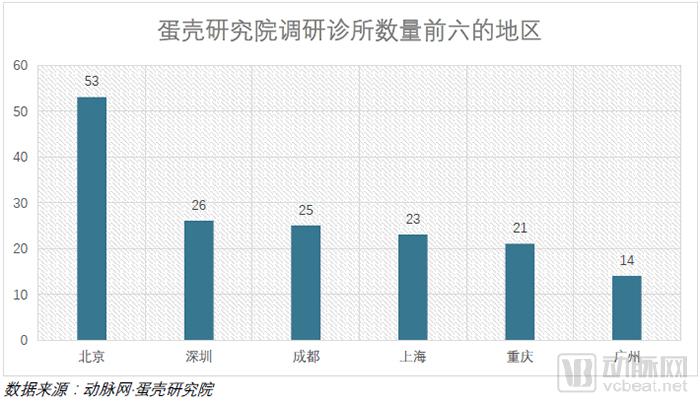

This survey primarily focuses on high-end new-type clinics and chain clinics, rather than individual private clinics, which account for the largest proportion in terms of quantity. The operational experience and performance of new-type and mid-to-high-end clinics are more worthy of our reference, and these clinics are mainly concentrated in first-tier cities. The table below shows the number of clinics in the top six cities visited and from which data were collected during this survey of new-type clinics. Beijing had the highest number, with 53 clinics surveyed, while the number of clinics surveyed in other cities was fewer than 10.

3.1.1 The clinic is relatively large in scale, primarily operating as an outpatient department

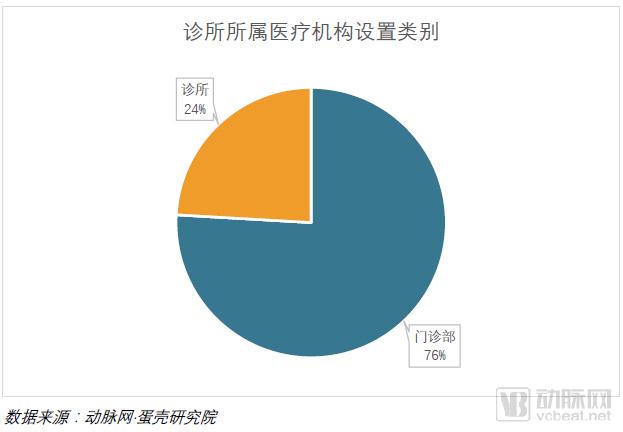

Historically, we have collectively referred to this category of medical institutions as “clinics.” However, surveys indicate that many clinics, particularly new-type ones, are registered as “outpatient departments” due to their larger scale and broader range of specialties. The term “outpatient department” is somewhat cumbersome, so people prefer to use the term “clinic.”

In the United States, the literal translation of “clinic” is indeed a clinic. Small-scale outlets such as MinuteClinic are called clinics, while healthcare giants like the Mayo Clinic and Cleveland Clinic also bear the name “clinic.” Thus, the naming convention does not hinder the development and growth of medical institutions. We also look forward to seeing our own Mayo and Cleveland emerge from the clinics we have surveyed.

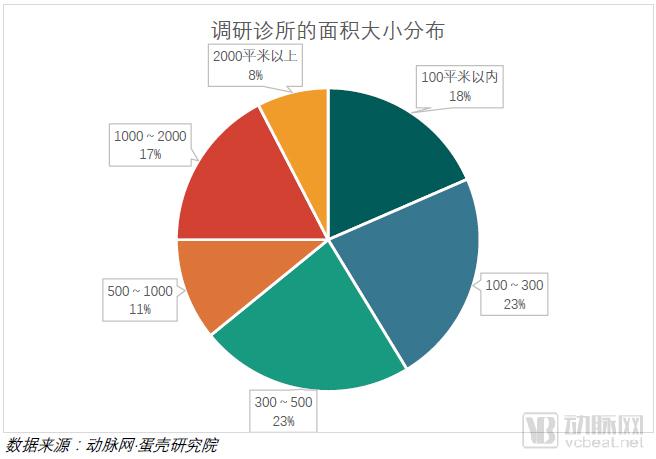

3.1.2 One-third of clinics have an area exceeding 500 square meters

Clinics with an area of less than 100 square meters are all individual practices positioned to provide community medical services. These clinics have weak competitiveness and account for 18% of the clinics surveyed by VCBeat Research Institute. Medium-to-large clinics with an area of over 1,000 square meters collectively account for 25% of the surveyed clinics. Such clinics generally offer a wider range of departments and can provide patients with relatively comprehensive medical services. With their larger footprint, these clinics have more space available for layout, allowing for more aesthetically pleasing interior design in areas such as waiting rooms and observation zones.

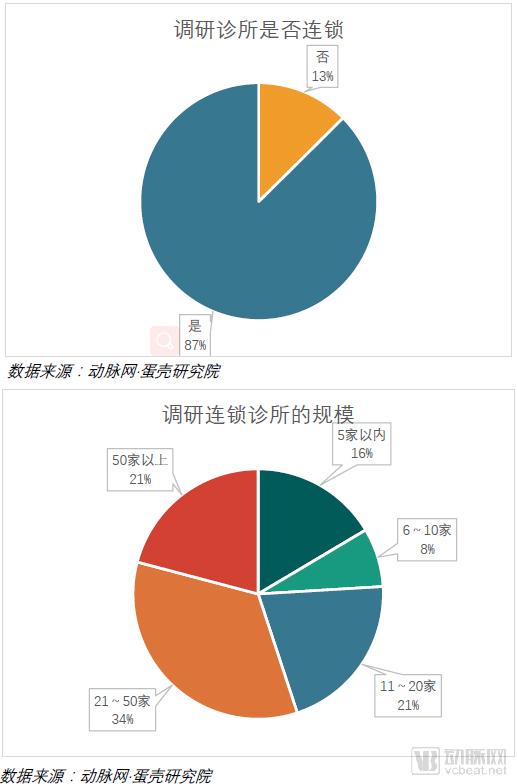

3.1.3 Chain Clinics Account for Over 80%

Private healthcare institutions will inevitably develop toward chain operations and economies of scale to reduce costs and improve efficiency. In China’s healthcare market, there is a significant gap compared to the U.S. market in terms of the chain-based and scaled development of medical institutions such as clinic chains, hemodialysis centers, and third-party medical laboratories. According to our survey data analysis, the chain affiliation rate among new-type clinics exceeds 80%. However, this figure does not reflect the overall clinic market, but rather the segment dominated by mid-to-high-end new-type chain clinics.

3.1.4 Past Two YearsThe Third Wave of Mid-to-High-End Clinic Construction Emerges

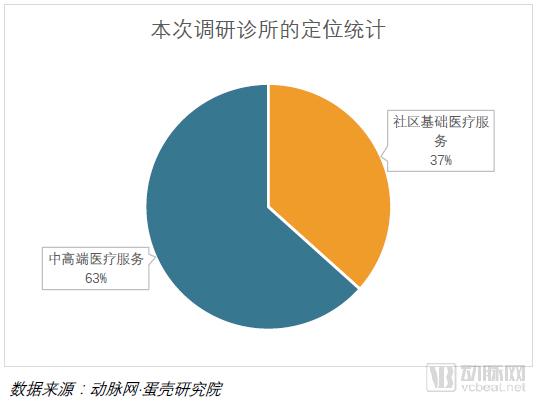

Among the clinics surveyed, one-third are positioned to provide primary community healthcare services, while two-thirds focus on mid-to-high-end medical services. Clinics typically address basic community healthcare needs, managing the diagnosis and treatment of common and frequently occurring diseases among residents. Currently, there are 169,000 clinics and 14,500 outpatient departments in China, with the majority positioned to deliver basic community healthcare services.

In this report, we selected only a small subset of low- to mid-end community clinics and private practices for data research, as these facilities typically have simplistic operational models and limited service capabilities. Most new-type clinics that excel in brand management, product design, service capacity, and operational performance are positioned in the mid- to high-end segments; therefore, our research focus is primarily on these new-type clinics.

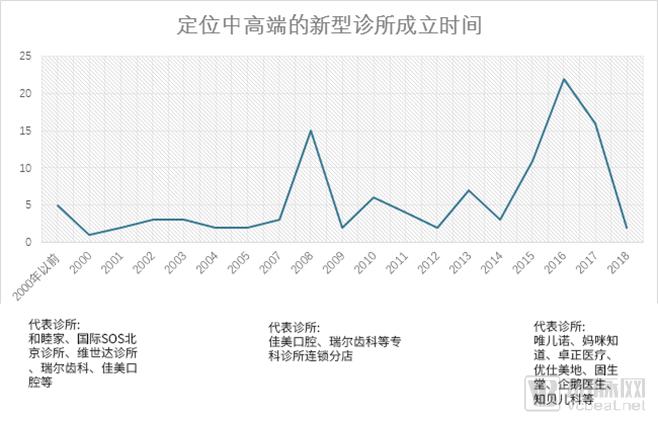

By analyzing the registration dates of these clinics, we have identified three waves of development in the mid-to-high-end new-type clinic sector.

The first wave of high-end private clinics in China emerged in the late 1990s, with establishments such as United Family Healthcare (Hospital), Vista Medical Center, Hong Kong and Macau International Clinic, and SOS International Medical Center choosing Beijing as their initial location. The primary reason for this trend was the rapid economic development during the late 1990s. As China’s economic, cultural, and political hub, Beijing attracted a significant number of foreign enterprises and an increasing expatriate population. Most of these high-end clinics had foreign investment backgrounds and introduced bilingual medical specialists or foreign physicians to provide international-standard medical services to expatriates in Beijing. This also allowed some high-income Chinese residents to experience premium healthcare services that were markedly different from the conventional medical environment in China, thereby building a strong reputation.

The second wave of mid-to-high-end clinics was primarily established around 2008. As per capita income rose in first-tier cities such as Beijing, Shanghai, and Shenzhen, China’s affluent population continued to grow. This demographic’s consumption upgrade has driven higher demands for medical services. Mid-to-high-end individuals require high-quality family physician services, patient and detailed explanations from medical staff, customized health management, long-term medical attention, and multilingual communication—services that public Grade A tertiary hospitals are unable to provide. During this period, some of the earliest market-oriented general outpatient clinics, along with specialized chains in dentistry and medical aesthetics, began expanding their branch networks.

The recent wave of mid-to-high-end clinics has been ongoing since 2016. While the first two waves of such clinics were predominantly oriented toward the high-end segment, clinics established during this current period have adopted a more accessible positioning, with commercial health insurance and out-of-pocket payments serving as the primary means of reimbursement. The key distinction between this third wave and the previous two lies in the increasing specialization of user demand: apart from a small number of general outpatient facilities, there has been a surge in mid-to-high-end specialty clinics focusing on niche areas such as dentistry, pediatrics, and Traditional Chinese Medicine (TCM). In addition to mid-to-high-income individuals seeking differentiated medical services, the target customer base now includes Fortune 500 companies and large state-owned enterprises, which have also become purchasers of these new clinic services.

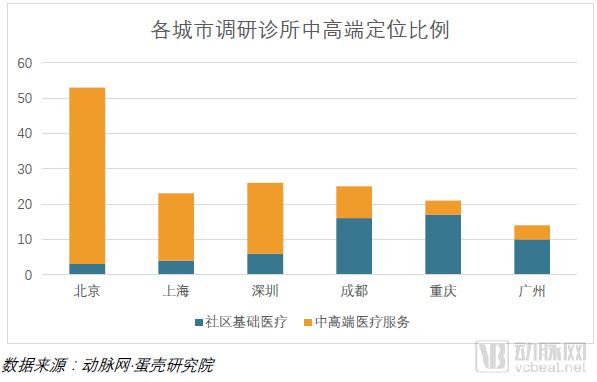

3.1.5 Mid-to-High-End Clinics Are Concentrated in First-Tier Cities

Among the six cities with the highest number of clinics in our survey, we categorized them based on clinic locations. It is evident that mid-to-high-end clinics are predominantly concentrated in first-tier cities, mainly distributed across Beijing, Shanghai, and Shenzhen. In the previous analysis, it was mentioned that Beijing, as China's political, economic, and cultural center, has become the optimal choice for establishing mid-to-high-end clinics. However, even after two decades, mid-to-high-end clinics remain primarily concentrated in Beijing, Shanghai, and Shenzhen.

First, tier-1 cities concentrate the vast majority of China’s elite population and expatriates, who have strong demand for high-end medical services. Second, income levels in tier-1 cities are higher, leading to greater acceptance of premium healthcare offerings. Third, commercial health insurance—a key source of both clients and revenue for mid-to-high-end clinics—is currently available only in tier-1 cities. Mid-to-high-end clinics in tier-2 cities not only need to lower consultation fees to align with market conditions but also lack support from commercial insurance, which may prevent them from achieving long-term profitability.

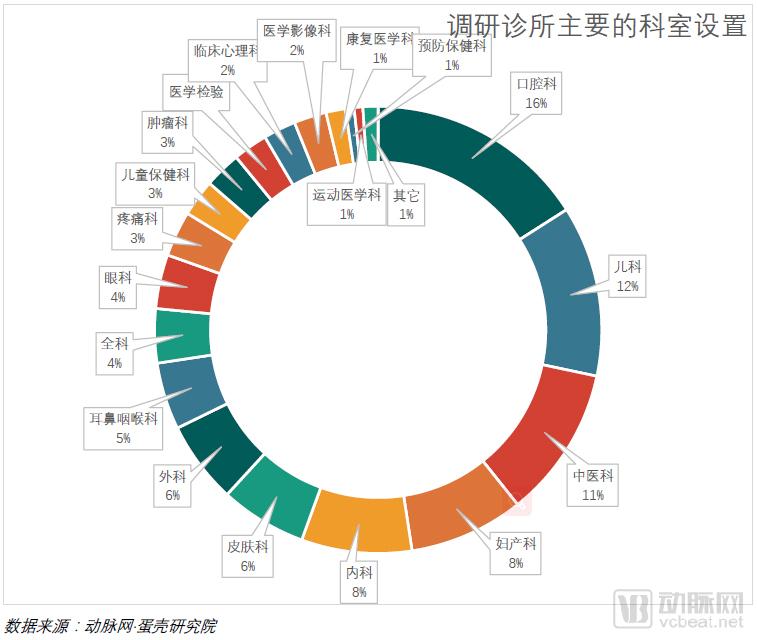

VCBeat Institute conducted a statistical analysis of the departmental structures of surveyed clinics. For the purposes of this analysis, first-level specialties listed in the "Catalogue of Diagnostic and Therapeutic Specialties for Medical Institutions" were used as the statistical units. For instance, second-level specialties such as gynecology were categorized under obstetrics and gynecology, while traditional Chinese medicine (TCM) pediatrics was categorized under TCM. The final aggregated data revealed that stomatology, pediatrics, and TCM are the three most prevalent specialties in clinics.

Stomatology belongs to a highly marketized and mature vertical segment of consumer healthcare, characterized by the extensive use of high-value consumables, high profit margins, and a large number of widely distributed clinics, which has also given rise to numerous large-scale chain institutions.

Pediatrics faces substantial market demand, with relatively easy patient acquisition and significant potential for increasing average revenue per user. However, in public hospitals, pediatrics is characterized by high pressure and low compensation. As demand for pediatric care continues to rise, a large number of pediatricians are leaving public hospitals. The stark contrast in work environments and conditions has attracted many pediatricians to join new types of clinics. Private pediatric clinics, distinguished by their focus on child healthcare and disease prevention, featuring child-friendly décor, and leveraging medical talent from the public sector, are now experiencing explosive growth.

As the nation vigorously promotes traditional Chinese medicine (TCM), the sector has received substantial policy support in healthcare delivery and talent development, making TCM clinics a focal point of capital market interest. The prospects for TCM departments are viewed favorably, evidenced not only by the proliferation of specialized TCM clinics but also by the establishment of TCM departments within many high-end foreign-invested clinics.

IV. Operational Strategies for New-Type Clinics

What Exactly Is a New-Type Clinic? The services offered by new-type clinics should not be defined by attractive decor and high fees, but rather by the delivery of professional medical care. Key considerations include whether patients are treated with respect during their visits, whether they are involved in medical decision-making, and whether physicians possess advanced concepts and up-to-date medical knowledge. If a clinic merely boasts elegant interiors and short wait times, yet its physicians’ service mindset and practices differ little from those of large public hospitals, patients will not perceive the value of consultation fees amounting to several hundred yuan.

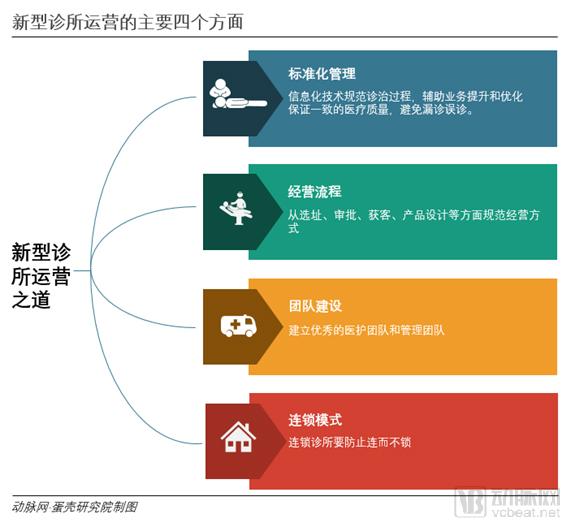

New clinics represent a new medical service-oriented model of diagnosis and treatment, but how should they be operated in practice? In this chapter, we analyze interview data to decode the secrets of clinic management, providing detailed insights from four perspectives: standardized management, operational strategies, team building, and chain models.

Below is the complete table of contents. The full report comprises six chapters and 89 pages. To read the remaining Chapters 4, 5, and 6, please scan the QR code to become a VCBeat member.Download the Full ReportRead it, or purchase the report individually in the VCBeat Reports section.

I. Industry Insights

1.1 Clinics are the smallest-scale medical institutions

1.2 Clinics Are Being Redefined

1.2.1 Small scale and limited number of licensed professionals

1.2.2 Limited Number of Clinical Departments in Clinics

1.2.3 The business nature is primarily for-profit

1.2.4 Consumption Upgrading Drives the Development of New-Type Clinics

1.3 The Development of Clinics in China Has Undergone Four Stages

II. New-Type Clinics Enter Their Prime Development Phase

2.1 Policies on Establishing Clinics Are Being Fully Liberalized

2.2 Policy-Driven Entry of Social Capital into the Clinic Sector

2.3 Development of Clinics in China from a Data Perspective

2.3.1 The number of clinics increases by 6,000 annually

2.3.2 Where Does the Market Growth in the Clinic Industry Lie?

III. 15 Cities, 200 Clinics, Tens of Thousands of Data Points: A New Self-Portrait of Clinics

3.1 Big Data Reveals Emerging Trends in New Clinic Development

3.1.1 The clinic is relatively large in scale, primarily operating as an outpatient department

3.1.2 One-third of clinics have an area exceeding 500 square meters

3.1.3 Chain clinics account for more than 80%

3.1.4 The Third Wave of Mid-to-High-End Clinic Construction Emerges in the Past Two Years

3.1.5 Mid-to-High-End Clinics Are Concentrated in First-Tier Cities

3.1.6 Departments of Stomatology, Pediatrics, and Traditional Chinese Medicine Are the Most Commonly Established

IV. Operational Strategies for New-Style Clinics

4.1 Standardized Management

4.1.1 The Construction of Information Systems Is Crucial

4.1.2 Medical Accreditation Standards Can Serve as a Reference and Aid for the Standardized Management of Clinics

4.1.3 Establishment of Supervisory Mechanisms to Ensure the Implementation of Standardized Management

4.2 Clinic Site Selection and Summary of Operational Strategies

4.2.1 Site Selection—Primarily Based on Positioning; Many Are Located in Commercial Districts

4.2.2 Approval—Clinic Approvals Are Heavily Restricted

4.2.3 Renovation and Equipment Procurement—Maximum Investment of Approximately RMB 10,000 per Square Meter

4.2.4 Pricing—Consultation fees at new-type clinics generally exceed 500 yuan

4.2.5 Customer Acquisition—Diverse Marketing Approaches, with Corporate Health Management as the Breakthrough

4.2.6 Medical Services—What Happens During an Extended 30-Minute Consultation?

4.2.7 Expanding Online Services—The Integration of Online and Offline Channels Emerges as a New Trend

4.2.8 Membership System—Leveraging the membership model to promote compassionate medical services

4.2.9 Insurance—Commercial insurance is a key driver in the development of new clinics

4.2.10 Third-Party Services: Elevating Clinic Service Capabilities to a New Level

4.2.11 Designing Clinic-Derived Products

4.3 Composition and Requirements of the Clinic Team

4.3.1 Most members of the management team do not have a medical background

4.3.2 Promotion and Performance Management of Medical Professionals

4.3.3 What Kind of Talent Do Clinics Need?

4.3.4 Dentists Are the Most In-Demand

4.3.5 The typical income of clinic physicians ranges from 10,000 to 20,000 yuan

4.4 Operational Model of Chain Clinics

V. Capital Markets Are Gradually Increasing Their Attention to New Types of Clinics

VI. Case Studies of New-Type Clinics