Primary Healthcare Investment Report: 347 Deals, Over RMB 30.3 Billion Raised, Driven by Hospitals, Internet Hospitals, and Clinics

According to statistics from the VCBeat database, there were 347 financing events in the primary healthcare sector both domestically and internationally between 2013 and May 2018, with total funding exceeding RMB 30.3 billion. Among these, there were 188 domestic financing events, with amounts surpassing RMB 14.4 billion. Hospitals, internet hospitals, and clinics were the main areas attracting investment.

From January to May 2018, there were 22 financing deals in China’s primary healthcare sector, representing a year-on-year increase of 57%. The total funding amount exceeded RMB 6.5 billion, up 44% year on year.

Key Points of the Report

Hospitals, internet hospitals, and clinics are driving the growth of financing scale in primary healthcare;

The number of financing projects in the primary healthcare sector has declined, with capital investment becoming more cautious;

Industry maturation is accelerating, with growth in new projects stagnating;

Hospitals and Internet hospitals attracted the most investment, followed by third-party testing/Financing in the healthcare and family doctor sectors remains lukewarm;

Hospitals and internet hospitals attracted the largest volume of major financing, while clinics demonstrated outstanding performance;

Financing Projects in the Field of Specialized Chronic DiseasesMostMultiple, the amount is slightlySmall;

Beijing Leads in Financing Activity; Beijing, Shanghai, Guangzhou, and Zhejiang Account for Over 70% of Total Funding.

Financing Scale Grows as Capital Investment Becomes More Cautious

From 2013 to 2016, both the number of financing deals and the total amount raised in the primary healthcare sector experienced leapfrog growth. In 2017, the number of financing deals in this sector dropped significantly, with early-stage project financings plummeting from 40 in 2016 to 17 in 2017. However, the total financing amount surged, driven by 12 deals exceeding RMB 100 million each. Notably, Guilian Medical (hospital sector), Gushengtang (clinic sector), and Bodjia Alliance (physician group sector) each secured over RMB 1 billion in funding. This trend indicates that capital began to concentrate on high-quality, mature projects.

From 2013 to 2017, the average financing amount in China’s primary healthcare sector showed an overall upward trend, driven by industry maturation and increased capital investment. Notably, the average financing amount dropped sharply to a trough in 2014, attributable to the high proportion of early-stage projects (reaching 87.5%) and the insufficient share of mature projects.

Specialty chronic disease management, clinics, and hospitals are the most sought-after sectors, with internet hospitals demonstrating outstanding performance.

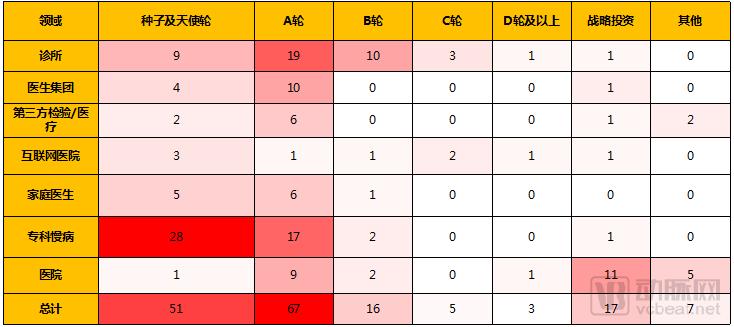

2013–2017 Financing Trends Across Subsectors of China’s Primary Healthcare Market

From 2013 to 2017, among the various segments of China’s primary healthcare sector, specialized chronic disease management, clinics, and hospitals were the most active in terms of financing. The specialized chronic disease segment recorded the highest number of financing deals, totaling 48, but the average transaction size was only RMB 13.78 million, as over 90% of the financed projects were in early stages, which lowered the overall average funding amount. In terms of total funding amount, the hospital sector led with more than RMB 3.4 billion. Notably, although the internet hospital sector had the fewest financing deals, it boasted the highest average transaction size, exceeding RMB 200 million, driven by three mega-deals each worth over RMB 100 million.

Delayed Funding Rounds, Stagnant Growth in New Projects

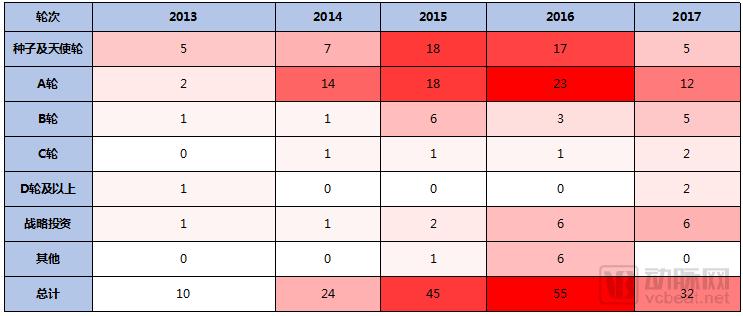

Distribution of Financing Rounds by Sub-sector in China's Primary Healthcare Market, 2013–2017

From 2013 to 2017, financing in China’s primary healthcare sector was predominantly concentrated in early-stage projects, which accounted for 71% of all deals. Among these, early-stage projects in the specialty chronic disease segment represented the highest proportion at 94%, indicating a severe shortage of mature-stage projects. In contrast, the hospital sector had the lowest share of early-stage projects at 34%, with financing occurring at later stages.

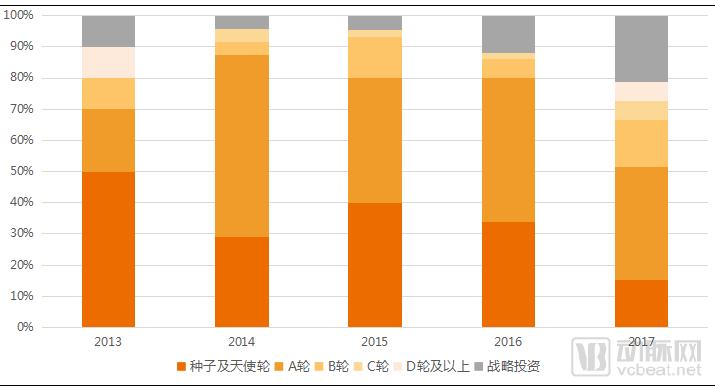

Distribution of Financing Rounds in China's Primary Healthcare Sector, 2013–2017

An analysis of the distribution of financing rounds over the years reveals that, from 2013 to 2017, domestic primary healthcare financing in China generally shifted toward more mature stages. Specifically, between 2013 and 2016, the number of financed projects continued to rise, with early-stage financing projects showing sustained growth. However, in 2017, the number of financed projects dropped sharply, and the growth of new projects stagnated.

Internet Hospitals and Clinics Attract the Largest Volume of Major Financing Rounds

2013-2017 Financing in China's Primary Healthcare SectorTOP10

From 2013 to 2017, the top 10 funded projects in China’s primary healthcare sector each secured over RMB 100 million. These top 10 projects were distributed across internet hospitals, hospitals, clinics, physician groups, and third-party laboratory testing/medical services. Among these, internet hospitals and clinics had the highest number of large-scale financing deals, each accounting for three spots.

Beijing Leads in Hottest Financing Activity; Beijing, Shanghai, Guangzhou, and Zhejiang Account for Over 80% of Total Funding

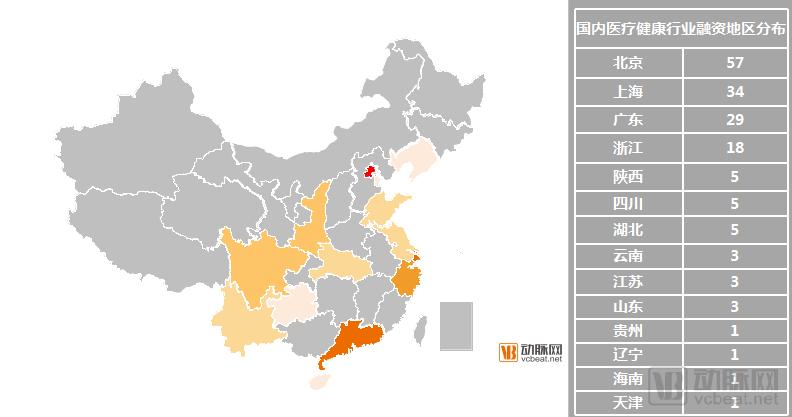

2013–2017 Geographic Distribution of Financing in China’s Primary Healthcare Sector

From 2013 to 2017, financing activities in China’s primary healthcare sector were primarily concentrated in Beijing, Shanghai, Guangdong, and Zhejiang. Among these, Beijing witnessed the most vigorous financing activity, accounting for 34% of the total number of financing events in the primary healthcare sector. The top four regions collectively accounted for 83% of all financing events in this sector.

Industry Maturation Accelerates, New Project Growth Stagnates

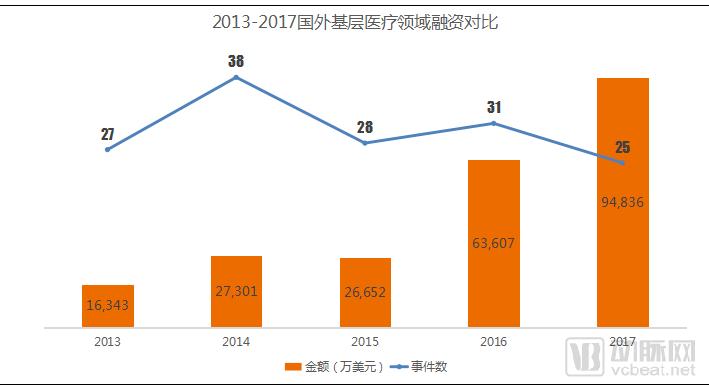

From 2013 to 2014, both the number of financing deals and the total amount raised in the overseas primary healthcare sector saw substantial growth. However, from 2015 to 2017, the number of financing deals stagnated, while the total funding amount continued to rise significantly. This trend was driven by a slowdown in the emergence of new projects, coupled with the accelerated maturation of existing ones.

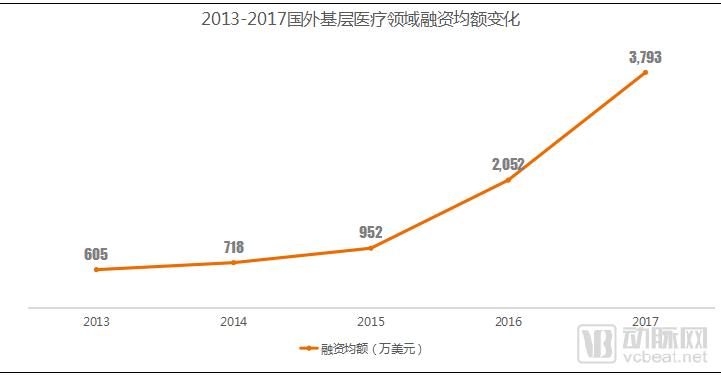

From 2013 to 2017, the average financing amount in the overseas primary healthcare sector continued to rise, driven by a decline in early-stage projects and an increasing proportion of mature projects.

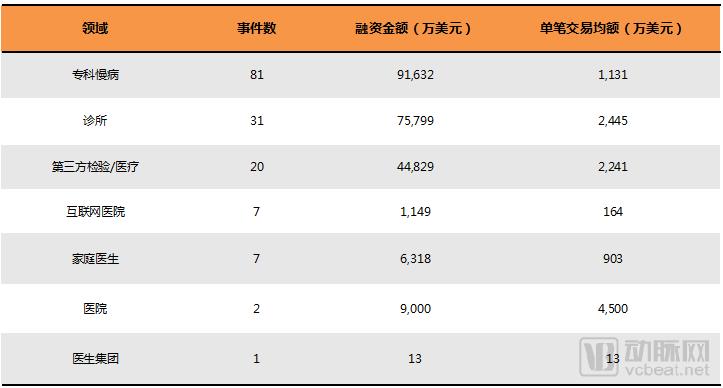

Specialty chronic disease management, clinics, and third-party testing/medical services showed outstanding performance, while financing for physician groups remained lukewarm.

2013–2017 Financing Trends in Subsectors of Primary Care Overseas

From 2013 to 2017, among various sectors of primary healthcare abroad, specialty chronic disease management, clinics, and third-party laboratory testing/medical services attracted the most investment. Notably, the specialty chronic disease sector led in both the number of financing deals and the total amount raised, whereas physician groups and hospitals experienced relatively cooler investment activity.

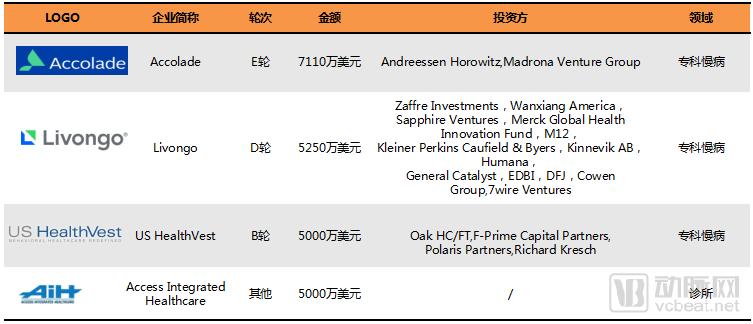

Clinics and Specialized Chronic Disease Fields Attract the Largest Amounts of Major Financing

Funding Amount in the Overseas Primary Care Sector, 2013–2017TOP10

Between 2013 and 2017, the top 10 foreign primary care projects each secured over $50 million in financing. These top 10 projects were distributed across clinics, specialized chronic disease management, third-party testing/medical services, and hospitals, with clinics and specialized chronic disease management accounting for the largest share, four projects each.

Financing Activity Heats Up as Large-Scale Deals Emerge

From January to May 2018, there were 22 financing events in China’s primary healthcare sector, with total funding exceeding RMB 6.5 billion—far surpassing the full-year financing amount of 2017.

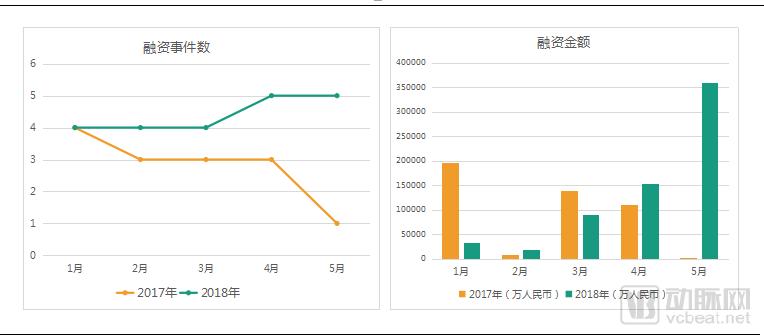

20171-5Month,2018Year1-5Comparison of the Number of Financing Events and Financing Amounts in China's Primary Healthcare Sector by Month

Compared to the first five months of 2017, financing activities in China’s primary healthcare sector were more active during the same period in 2018, with the number of financing deals increasing by 57% year-on-year and the total financing amount rising by 44% year-on-year. Notably, there were 10 large-scale financing rounds exceeding RMB 100 million each in the first five months of 2018, two of which surpassed RMB 1 billion.

Comparison of Financing Rounds in China’s Primary Healthcare Sector: January–May 2017 vs. January–May 2018

Analysis of Financing Rounds: In the first five months of 2018, financing rounds shifted toward later stages compared to the same period in 2017.

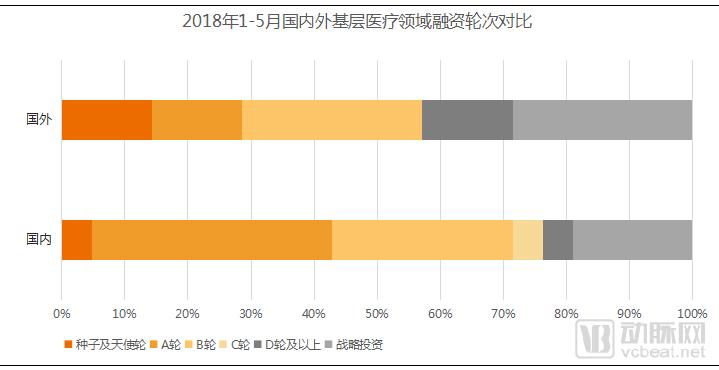

Domestic financing is more active, while overseas financing rounds are at later stages.

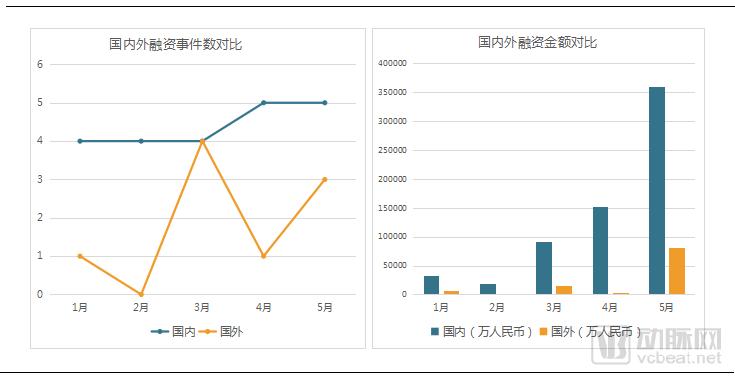

20181-5Comparison of the Number and Amount of Financing Deals in Domestic and International Primary Healthcare by Month

From January to May 2018, financing activities in China’s primary healthcare sector were more active than those abroad, with both the number of deals and the total amount exceeding international figures.

Compared with domestic projects, overseas primary healthcare ventures that secure investment tend to be at later funding rounds, with a higher proportion of mature projects.

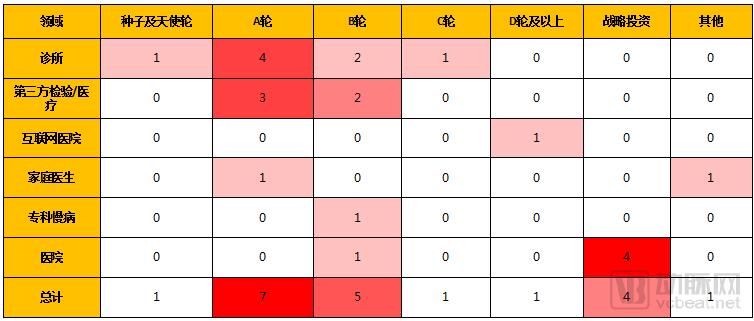

Clinics saw the highest number of deals, while internet healthcare recorded the largest transaction value.

Financing in Various Sub-sectors of Domestic Primary Healthcare from January to May 2018

From January to May 2018, among the various segments of China’s primary healthcare sector, clinics, third-party testing/medical services, and hospitals saw active financing activities. Notably, the clinic segment recorded the highest number of financing deals, accounting for more than 36% of all financing events in primary healthcare. It is worth noting that a mega-round of financing occurred in the internet hospital sector, with WeDoctor raising $500 million in its Pre-IPO round.

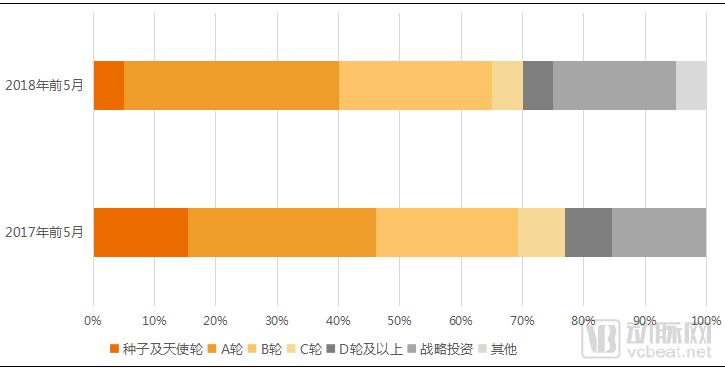

20181-5Distribution of Financing Rounds Across Various Sectors in China's Healthcare Industry by Month

In the first five months of 2018, financing projects in China's primary healthcare sector were mainly concentrated in Series A and Series B rounds, which together accounted for 55%.

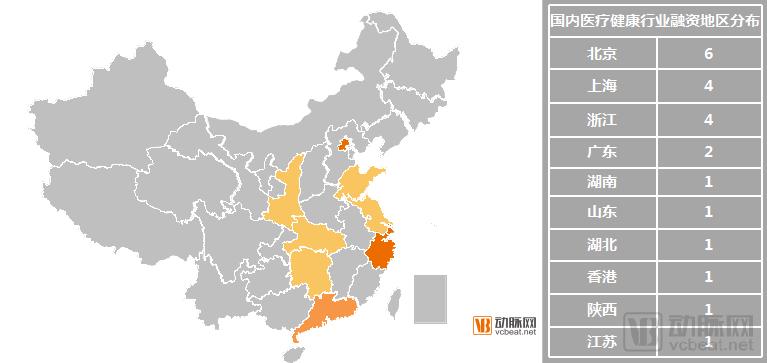

Beijing, Shanghai, Guangdong, and Zhejiang Attract the Most Financing, Accounting for Over 70% of Projects

In the first five months of 2018, financing deals in China’s primary healthcare sector were concentrated in Beijing, Shanghai, Zhejiang, and other regions. Beijing accounted for the highest share at 27%, with the four regions of Beijing, Shanghai, Zhejiang, and Guangdong collectively representing 73% of all financing deals.

Hospitals Attract the Largest Volume of Major Financing; Internet Hospitals See Record-Breaking Funding Amounts

Top 5 Financing Amounts in China’s Primary Healthcare Sector (January–May 2018)

From January to May 2018, the top five funded projects in China’s primary healthcare sector each secured over RMB 200 million. These top five deals were distributed across the internet, hospital, and family physician sectors, with hospitals being the most favored by investors, accounting for three of the five spots. Notably, WeDoctor, a player in the internet hospital space, raised $500 million in its Pre-IPO round, setting a new funding record for the internet hospital sector.

WeDoctor

WeDoctor is China's leading mobile internet healthcare service platform, founded in 2010 by Liao Jieyuan and his team. Leveraging internet technology, WeDoctor provides hundreds of millions of users in China with trustworthy services including appointment registration, online consultations, remote consultations, electronic prescriptions, and medication delivery, as part of its internet-based medical and membership offerings.

On May 9, 2018, WeDoctor announced the completion of a $500 million Pre-IPO financing round, reaching a valuation of $5.5 billion. This round set a record for the largest pre-listing financing in China’s healthcare technology sector.

Meijiahe

Meizhong Jiahe is a network of oncology diagnosis and treatment centers and a chain operator of independent medical institutions specializing in radiation therapy, under the umbrella of CCMC Group, a company listed on the New York Stock Exchange. Currently, Meizhong Jiahe operates multiple facilities, including Datong Meizhong Jiahe Cancer Hospital, Shanghai Bairui Oncology Outpatient Clinic, Wuxi Meizhong Jiahe Cancer Hospital, and Shanghai Meizhong Jiahe Medical Imaging Diagnostic Center. The company was officially listed on the National Equities Exchange and Quotations (NEEQ) on January 25, 2016 (Stock Code: 835660). Meizhong Jiahe has remained focused on oncology imaging diagnosis and radiation therapy. As of April 30, 2017, the company had established a nationwide network covering 57 hospitals in 49 cities across 19 provinces, comprising 95 cooperative oncology imaging diagnostic centers and radiation therapy centers. On April 4, 2018, Meizhong Jiahe announced the completion of a RMB 1.5 billion strategic financing round led by CICC Capital.

Virtus Medical Holdings

Virtus Medical Holdings is a private healthcare provider based in Hong Kong, China. On March 2, 2018, Virtus Medical Holdings announced the completion of an $83 million financing round.

Hunan Kexin

Hunan Kexin Health Industry Development Co., Ltd., established in 2014, is a large-scale chain of specialized oncology hospitals. Its currently invested hospitals include Changsha Kexin Oncology Hospital, Huxiang Traditional Chinese Medicine Oncology Hospital, Shaoyang Kexin Oncology Hospital, Yongzhou Kexin Oncology Hospital, Wuhan Lanqing Oncology Hospital, and Wuhan Kexin Oncology Hospital. On May 5, 2018, Hunan Kexin announced that it had secured RMB 240 million in financing, led by Huagai Capital and participated in by Orient Fortune Venture Capital.

Wuhan Aige Eye Hospital

Founded in 2003, Wuhan Aier Eye Hospital is a Sino-foreign joint venture ophthalmic medical group originating from Wuhan. It is a tertiary specialized eye hospital integrating medical care, teaching, scientific research, and blindness prevention. The hospital is designated as a medical insurance provider for Wuhan City, Hubei Province, and for cross-regional medical treatment nationwide. On March 13, 2018, it announced that it had secured $40 million in Series B financing from CDH Investments.

Overview of Financing Events in China’s Primary Healthcare Sector from January to May 2018