China's Third-Party Medical Services Industry White Paper 2018: Evolution Paths of 10 Institution Types Under Dual Drivers and Emerging Observation Points

In recent years, with the gradual implementation of policies such as “tiered diagnosis and treatment,” the “two-invoice system,” “medical consortiums,” and “family doctor contracting,” China’s healthcare system reform has deepened further. In the private healthcare sector, the third-party medical services industry has undoubtedly become a major topic of interest. In February 2017, the former National Health and Family Planning Commission issued the Decision on Amending the Detailed Rules for the Implementation of the Regulations on the Administration of Medical Institutions, adding five new categories of medical institutions: “medical laboratory testing centers, pathology diagnosis centers, medical imaging diagnosis centers, hemodialysis centers, and hospice care centers.” The Commission stated that the Detailed Rules, which had been in effect since 1994, no longer met regulatory needs, and that the amendments had long been planned in response to the new industrial environment and development requirements.

Six months later, the authorities reissued the “Notice on Deepening the ‘Streamline Administration, Delegate Powers, and Improve Services’ Reform to Stimulate Investment Vitality in the Healthcare Sector,” expanding the categories of third-party medical service institutions from the previous five to ten, and successively introducing basic construction requirements and operational standards for seven types of third-party medical service institutions.

VCBeat·VBInsight categorizes third-party medical service providers into two groups—diagnostic/technical and clinical—based on their primary customer types across ten categories. It posits that, with the continuous development of China’s healthcare industry, these two types of third-party medical service providers follow distinctly different growth logics. At the operational level, by analyzing the operational workflows of third-party medical service providers, we conclude that, as capital-intensive healthcare service providers, their ability to scale hinges critically on operators’ efficiency in integrating various resources.

Furthermore, why have third-party medical service providers gained official recognition and support? What impact will these entities have on China’s healthcare system? How can they carve out a sustainable path amid fierce market competition? This report provides a detailed analysis of each of these questions.

Source: VCBeat

Within the research framework of VCBeat, we interpret industry evolution through the following lens: the aggregate of technologies, methodologies, and practices within a specific industry during a given period is termed a “domain.” This “domain” comprises underlying technologies, the social relationships formed upon this technological foundation, and the rules, mechanisms, and legal frameworks that coordinate societal operations. When applied to the healthcare sector, this concept corresponds to medical technologies, the operational and interest-based relationships underpinning the healthcare system, and relevant policies and regulations.

When any one of the three elements—technology, relationships, and rules—within this ecosystem changes, the mode of economic operation will shift. As the entire ecosystem achieves a new dynamic equilibrium, the old domain will transition to a new one, and the mode of economic operation will reach a new stability on this basis; this process is termed “re-domaining.” The transition from the old domain to re-domaining rarely happens overnight; it generally takes 20 years or even longer. This required duration is referred to as “relational time.”

In observing the process of domain redefinition, we have developed a research framework that assesses the market potential of new economies by analyzing the drivers of industry change and monitors industry development trajectories to capture market opportunities.

With regard to research on third-party medical service providers, this wave of transformation is primarily driven by changes in market demand and regulatory frameworks, while the impact of advancements in medical technology has been relatively minor. Accordingly, our research approach focuses on two distinct pathways: policy influence and market influence. We aim to identify the key factors shaping the third-party medical services market under these drivers, assess the current state of industry development, establish observation points for in-depth tracking, and seek to capture critical milestones in the ongoing redefinition of the third-party medical services market. In the following sections, we will elaborate on the third-party medical services industry along these lines.

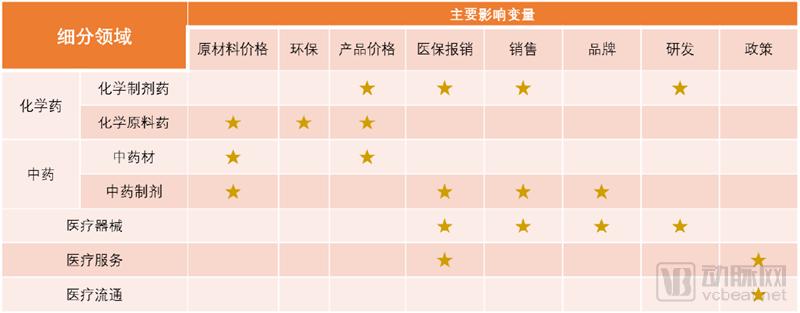

Key Influencing Variables Across Subsectors in the Healthcare Industry

Source: VCBeat

We often say that everything happens for a reason. For a long time, our observation of the healthcare industry’s operations has typically involved tracking key variables that significantly impact the sector. By establishing specific monitoring points, we gain insights into industry changes and determine the current stage of development. Among the factors on our watchlist, policy and health insurance payment mechanisms have the most pronounced impact on the medical services industry. Specifically, regarding third-party medical services, we attribute the recent substantial growth of third-party medical service institutions to two major drivers: policy incentives under the backdrop of tiered diagnosis and treatment, and market supplementation driven by unmet demand.

2.1 Policies Explicitly Encourage Third-Party Medical Service Providers and Promote Chain and Group-Based Operations

The “New Healthcare Reform” proposed the goal of establishing a “multi-tiered and diversified” medical service system to comprehensively meet the public’s demand for healthcare services. Under this top-level design, policies governing private healthcare provision have been progressively refined, enhancing their operability and creating favorable conditions for capital investment. In summary, the approach rests on two pillars: lowering entry barriers and establishing standards.

In October 2013, the government issued the “Several Opinions on Promoting the Development of the Health Service Industry,” vigorously developing third-party services and guiding the development of specialized medical laboratory centers and imaging centers.

On February 21, 2017, the National Health and Family Planning Commission issued the “Decision on Amending the Detailed Rules for the Implementation of the Regulations on the Administration of Medical Institutions,” adding five categories of medical institutions: medical laboratory testing centers, pathology diagnosis centers, medical imaging diagnosis centers, hemodialysis centers, and palliative care centers.

In August 2017, the National Health and Family Planning Commission issued the “Notice on Deepening the Reform of ‘Streamlining Administration, Delegating Power, and Improving Services’ to Stimulate Investment Vitality in the Medical Field,” adding five categories of independently established medical institutions, including: rehabilitation medical centers, nursing centers, sterile supply centers, small and medium-sized ophthalmic hospitals, and health examination centers.

In terms of standard-setting, the Implementation Rules for the Regulations on the Administration of Medical Institutions, which came into effect in 1994, have become outdated and no longer meet regulatory requirements. Against the backdrop of a new industrial environment and development needs, revisions have long been planned. In late 2016, the National Health and Family Planning Commission successively issued the basic standards and management specifications for seven categories of independently established medical institutions: medical laboratory testing centers, pathology diagnosis centers, medical imaging diagnosis centers, hemodialysis centers, hospice care centers, rehabilitation medical centers, and nursing centers (see Appendix). These measures aim to regulate while promoting the development of independently established medical institutions. The basic standards clarify the fundamental requirements for establishing such institutions, serving as the minimum “red line.”

Third-party medical service providers, also known as “independent medical service institutions,” refer to entities established outside the traditional hospital system that specialize in providing specific diagnostic, laboratory testing, or specialized medical services. In recent years, the government has continuously introduced policies to encourage private capital investment in healthcare and promote the development of third-party medical services, thereby supplementing the public healthcare system and addressing the challenges of difficult and costly access to medical care.

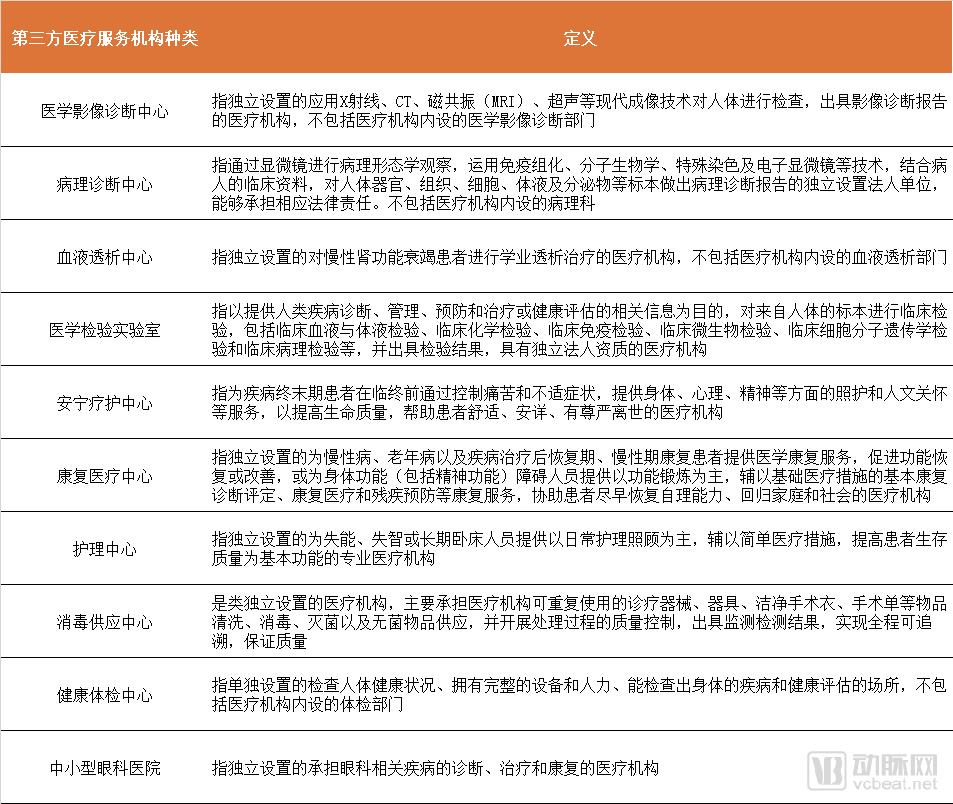

Currently, third-party medical service providers that are explicitly encouraged by official authorities to operate through chain and group-based models include: medical imaging diagnostic centers, pathology diagnostic centers, hemodialysis centers, medical laboratories, hospice care centers, rehabilitation medical centers, nursing centers, sterile supply centers, health examination centers, and small- and medium-sized ophthalmic hospitals. Given that these ten types of third-party medical service institutions have already received official support and possess strong industry representativeness, this report primarily focuses its discussion on them.

Definition of Third-Party Medical Service Providers

Source: Former National Health and Family Planning Commission, VCBeat

In fact, third-party medical service providers have been in existence for a long time. In particular, highly market-oriented entities such as health examination centers and small- to medium-sized ophthalmic hospitals have become an important component of China’s healthcare system. Following the successive release of multiple supportive policies by the National Health and Family Planning Commission in 2016 and 2017, third-party medical service providers once again garnered significant attention from industry practitioners and investors, thereby ushering in major opportunities for development.

# Major Types of Third-Party Medical Service Providers and Related Policies

Source: Analysis by VCBeat · VBInsight

We can see that the policy on opening up third-party medical services was introduced against the broader backdrop of “tiered diagnosis and treatment + promoting private healthcare provision”:

(1) According to data from the 2017 China Health and Family Planning Statistical Yearbook, there are currently more than 29,000 hospitals nationwide, with the total number of medical and health institutions approaching one million. Requiring all primary care medical and health institutions to establish clinical laboratory, medical imaging, and pathology departments would result in a shortage of qualified personnel.

(2) Centralize the establishment of third-party medical institutions and open them to primary care facilities, which facilitates the concentration of limited medical resources and enables regional resource sharing while ensuring quality.

(3) Some high-end laboratory tests are performed in low volumes at individual hospitals, making them cost-ineffective. Engaging independent third-party clinical laboratories to provide these services under contractual management arrangements facilitates quality control and helps ensure medical quality and safety.

The overarching rationale behind the issuance of these documents is to integrate tiered diagnosis and treatment with the promotion of privately run medical institutions, thereby achieving regional sharing of medical resources. This approach aims to enhance primary care capabilities at the grassroots level and meet the development needs of small and medium-sized socialized medical institutions, such as individual clinics. Primarily, through the regional sharing of medical resources, it addresses the shortages of relevant personnel and insufficient diagnostic and testing capabilities at the grassroots level, while also avoiding redundant investments in medical equipment and achieving homogenization of medical quality. Only through integrated development, which fills the gap in grassroots capacity, can patients who might otherwise seek care at large hospitals be retained at the primary care level. Such resource sharing is particularly meaningful in economically underdeveloped areas that are geographically remote and lack adequate medical resources.

2.2 Differences in Customer Groups Lead to Distinct Evolutionary Logics for Third-Party Medical Service Providers

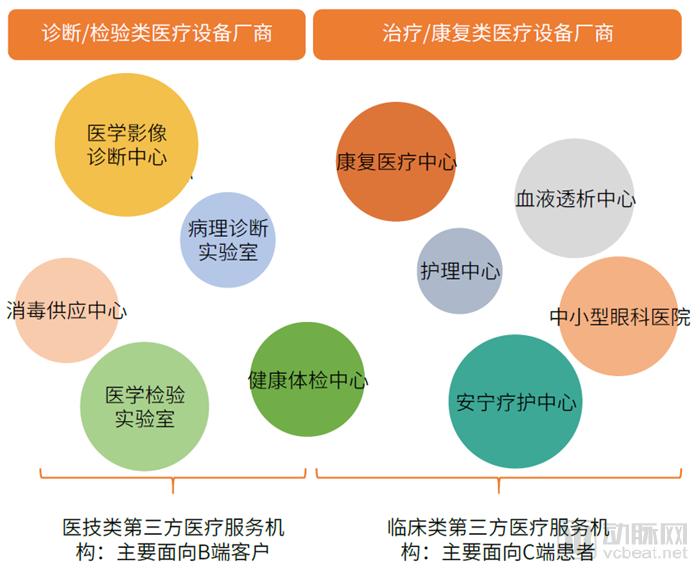

Differences Between Third-Party Medical Service Institutions in the Diagnostic and Technical Support Sector and Those in the Clinical Care Sector

Source: VCBeat

Although third-party medical service providers are legally independent entities, their operational integration with traditional hospitals varies significantly across different types of providers.

Medical service institutions typically serve as a bridge within the healthcare system, connecting suppliers of medical resources (such as pharmaceuticals, medical devices, and physicians) with demanders (patients). Third-party medical service institutions differ slightly; according to the official definition, they encompass not only traditional medical service institutions but also those providing auxiliary and supportive services to traditional medical service institutions.

Based on the different stages of integration into the medical care process, we categorize third-party medical service providers into two types: The first type comprises diagnostic and technical third-party medical service providers, which primarily deliver auxiliary medical services such as diagnosis and laboratory testing through specialized equipment; these include medical imaging diagnostic centers, clinical laboratories, pathology diagnostic laboratories, and sterile supply centers. The second type consists of clinical third-party medical service providers, which operate in more core segments of healthcare delivery and primarily offer medical services that directly impact patient health, such as treatment and rehabilitation; these include hemodialysis centers, hospice care centers, rehabilitation medical centers, nursing centers, and small- to medium-sized ophthalmic hospitals.

From the upstream perspective of the industry chain, the primary suppliers for both medical technology-oriented third-party medical service providers and clinical-oriented third-party medical service providers include medical equipment manufacturers. However, the former focuses its demand on diagnostic and laboratory testing equipment, while the latter prioritizes therapeutic and rehabilitation equipment.

From the downstream perspective of the industry chain, third-party medical service institutions specializing in medical technology primarily provide supportive services to B-end clients such as hospitals and clinics, whereas those focused on clinical services deliver medical care directly to C-end patients. Due to differences in their customer bases, these two types of third-party medical service institutions have diverged in their development logic.

Third-party medical technology services primarily handle outsourced testing and diagnostic tasks for hospitals and clinics, maintaining a partnership with traditional healthcare institutions. Large public hospitals, where patients are concentrated, represent the largest market for these third-party medical technology service providers. For independently established medical institutions specializing in laboratory testing, medical imaging, and pathology, hospitals are “clients” rather than competitors. Currently, patients and test samples in China are mainly concentrated in tertiary hospitals located in large and medium-sized cities. Even secondary and primary hospitals at the county and city levels, though smaller in scale, offer comprehensive services. This distribution pattern grants hospitals decisive control over test items and sample submission channels. Therefore, independent clinical laboratories must collaborate with hospitals to obtain access to samples.

Furthermore, for the rapidly growing individual clinics and similar institutions, establishing their own laboratory, pathology, and imaging departments would undoubtedly incur prohibitively high costs. Sharing testing and diagnostic resources within the region provides strong support for the development of these institutions.

Clinical third-party medical service providers are essentially in direct competition with traditional healthcare institutions, squeezing their market share and driving competition primarily through demand differentiation.

Notably, while health examination centers appear to belong to the category of third-party medical service institutions providing diagnostic and technical services based on their service workflows, their client base extensively includes individual health check-up participants, and the industry demonstrates a high degree of market-oriented operation. Therefore, in this report, we do not classify them strictly as either third-party diagnostic and technical medical service providers or third-party clinical medical service providers; rather, they occupy an intermediate position between these two categories.

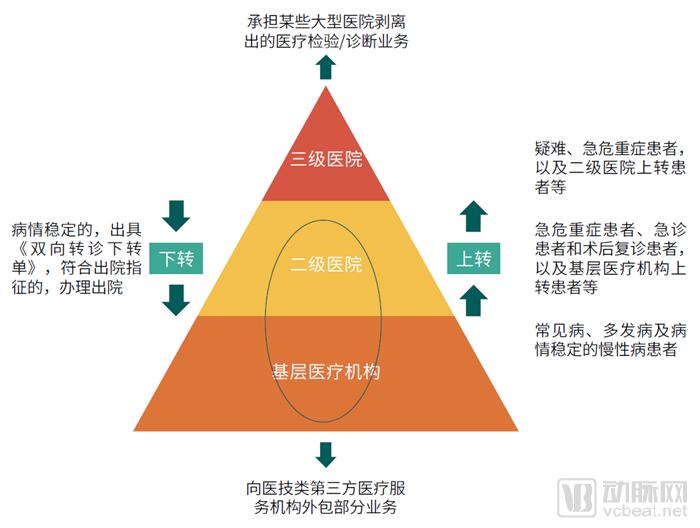

2.3 Third-Party Medical Technology Service Providers Driven by the "Tiered Diagnosis and Treatment" Policy

The Positioning of Third-Party Medical Technology Service Providers in the "Tiered Diagnosis and Treatment" System

Source: VCBeat · VCBeat Research Institute

The maturation of an industry is typically accompanied by specialized division of labor, as practitioners fulfilling their respective roles can reduce overall costs and improve quality, thereby further driving rapid industry development. The rise of third-party medical service providers specializing in medical technology stands as one of the hallmarks of the healthy growth of China’s healthcare industry.

In highly market-driven healthcare systems such as that of the United States, there is a large number of private physicians who serve as guardians of public health. These practitioners typically operate independently and establish their own clinics. For them, purchasing expensive testing and diagnostic equipment poses a risk of resource waste. Consequently, third-party medical service providers, such as clinical laboratories and medical imaging centers, have emerged to address this need. By aggregating demand from various types of hospitals and clinics across different regions, these entities provide low-cost ancillary and supportive medical services on a large scale, creating mutual benefits.

From the perspective of value chain contribution, China’s third-party medical diagnostic and technical service providers are likewise adhering to the development logic of “reducing healthcare costs and realizing healthcare value.” However, unlike the current healthcare landscape in the United States, China’s medical resources are highly concentrated, with large public hospitals serving as the primary providers of medical services.

Due to the strong siphon effect these hospitals exert, they boast substantial departmental and patient volumes. Given that they have already reduced laboratory and diagnostic costs to a certain extent, outsourcing these services poses two main risks: potential inaccuracies in test and diagnostic results, and the burden on patients of traveling between multiple locations, which detracts from their experience. Consequently, these hospitals maintain a highly uncertain stance toward third-party medical technology service providers.

Furthermore, in accordance with the dynamics of bargaining within upstream and downstream segments of the industry chain, when demanders are numerous and fragmented, suppliers possess relatively stronger bargaining power; conversely, when demanders are few and concentrated, suppliers’ bargaining power is relatively weaker. Currently, third-party medical service providers specializing in diagnostic and technical services in China face insufficient bargaining power.

As China’s healthcare reforms deepen, the introduction of the “tiered diagnosis and treatment” policy has provided valuable momentum for third-party medical service providers specializing in diagnostic and technical services. This policy emphasizes stratifying patients based on the severity, urgency, and complexity of their conditions, with medical institutions at different levels assuming responsibility for diagnosing and treating corresponding diseases, thereby establishing a model characterized by initial consultations at primary care facilities and two-way referrals. Once fully implemented, this policy will fundamentally reshape China’s current healthcare service landscape, directing patients toward small and medium-sized hospitals and primary healthcare institutions. Drawing from historical experience in the United States, a decentralized healthcare service system will open up entirely new markets for third-party medical service providers specializing in diagnostic and technical services.

The primary clients of third-party medical technical service providers can be broadly categorized into two groups: large hospitals and small clinics. The entry barriers to the large hospital market are high, yet it serves the largest patient population and offers the greatest potential market size. Although small clinics have a significantly smaller patient volume compared to large hospitals, they exhibit a strong willingness to outsource certain medical technical departments. The "tiered diagnosis and treatment" policy can effectively segment the large hospital market into the small clinic market. In other words, assuming the total market size remains constant, traditional healthcare institutions will increase their outsourcing of medical technical departments, thereby lowering the market entry barriers for third-party medical technical service providers.

In the context of healthcare reform, official policy undoubtedly provides strong support for “tiered diagnosis and treatment.” Nevertheless, we must remain acutely aware that China’s existing healthcare system has its own deeply entrenched developmental logic, and the implementation of these policies will need to overcome challenges from various stakeholders.

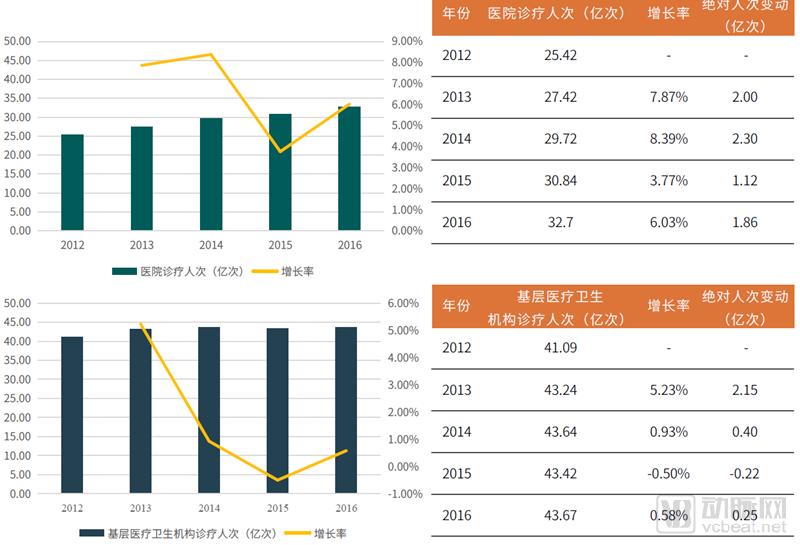

According to data from the 2017 China Health and Family Planning Statistical Yearbook, the number of patient visits at hospitals in China increased from 2.542 billion in 2012 to 3.270 billion in 2016, with a compound annual growth rate (CAGR) of 6.50%; meanwhile, patient visits at primary healthcare institutions rose from 4.109 billion to 4.367 billion, with a CAGR of only 1.53%.

As it stands, China’s primary healthcare institutions lag behind hospitals in both the growth rate and the absolute increase in patient visits. Therefore, based on patient visit data from these two different types of medical service providers, we can conclude that the “tiered diagnosis and treatment” policy has not yet achieved its expected results.

Diagnosis and Treatment Services in Hospitals and Primary Healthcare Institutions (2012–2016)

Note:1Hospitals include general hospitals, traditional Chinese medicine (TCM) hospitals, integrated TCM and Western medicine hospitals, ethnic minority medicine hospitals, specialized hospitals, and nursing hospitals;

2Primary healthcare institutions include community health service centers, township health centers, village clinics, outpatient departments, and private clinics.

Source: "2017 China Health and Family Planning Statistical Yearbook", VCBeat

Furthermore, the development of medical consortiums may also exert a certain impact on third-party medical service providers specializing in diagnostic and technical services. Since the primary objective of medical consortiums is to establish an integrated healthcare alliance comprising tertiary hospitals, secondary hospitals, community health centers, and village clinics within a specific region—thereby achieving synergistic sharing and rational allocation of medical resources—secondary and primary healthcare institutions may consolidate certain laboratory testing and diagnostic services into larger hospitals for centralized processing within the consortium. This trend creates competitive pressure on third-party medical service providers focused on diagnostic and technical support.

As healthcare reform invariably entails the restructuring of stakeholder interests, it constitutes a massive systemic undertaking. From a theoretical perspective, although third-party medical technology and diagnostic services enjoy policy support, the effective implementation of such policies cannot be guaranteed, and there is a risk of disruption from Medical Consortia.

Therefore, while we acknowledge the value of third-party medical technology service providers in reducing healthcare costs and enabling specialized division of labor within the overall healthcare system, their market prospects remain significantly influenced by external factors, potentially imposing a certain ceiling on growth.

Where there is crisis, there is opportunity. Although the development of medical consortia competes with third-party medical technology service providers, most high-tier hospitals in many regions are operating at capacity and offer relatively routine testing services. Third-party medical technology service providers should seize the opportunities presented by the growth of medical consortia, actively participate in healthcare infrastructure development, and leverage their strengths to enhance overall clinical care and operational efficiency. A typical example is the Conghua Regional Specialized Medical Consortium for Laboratory Medicine established by KingMed Diagnostics.

In July 2015, the Health Bureau of Conghua District, Guangzhou, established the Conghua Regional Laboratory Medical Consortium, with KingMed Diagnostics’ Conghua Center serving as the lead institution, together with four Grade II-A hospitals, four community health service centers, and eight township health centers. This initiative fully leveraged regional medical laboratory diagnostic resources to implement vertical integration of resources across municipal and primary-level public healthcare institutions. It aimed to gradually achieve sharing of laboratory testing resources within the consortium, enhance regional laboratory diagnostic capabilities and efficiency, and facilitate inter-hospital coordination services such as tiered diagnosis and treatment and referral appointments. Meanwhile, through outsourced testing arrangements, a collaborative mechanism for examination and diagnosis was established between regional medical institutions and third-party independent clinical laboratories (KingMed Diagnostics). This enabled residents in the region to schedule or access advanced-level hospital-equivalent laboratory tests at primary care facilities, thereby promoting the implementation of tiered diagnosis and treatment and mutual recognition of test results within the region.

2.4 Demand-Driven Growth: Clinical Third-Party Medical Service Providers Enrich the Diversity of China’s Healthcare Landscape

Unlike third-party medical service providers in the diagnostic and technical sectors, which primarily aim to reduce healthcare system costs, clinical third-party medical service providers focus more on delivering incremental value atop the existing healthcare framework to meet residents’ growing demand for medical and health services. Therefore, we believe that clinical third-party medical service providers essentially follow the same logic as private medical institutions such as private dental hospitals and private oncology hospitals—shifting the treatment of conditions traditionally managed by public hospitals to private facilities.

However, the greatest difference between private hospitals and public hospitals lies in their operational objectives: private hospitals aim to maximize profits rather than fulfill the public-welfare nature of healthcare. Consequently, capital consistently flows toward specialty areas that generate higher returns. The clinical third-party medical service institutions officially encouraged by the government mainly include sectors previously overlooked by private capital, such as hospice care centers.

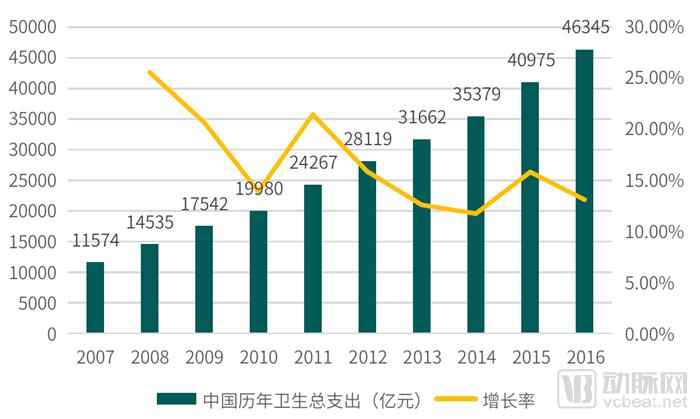

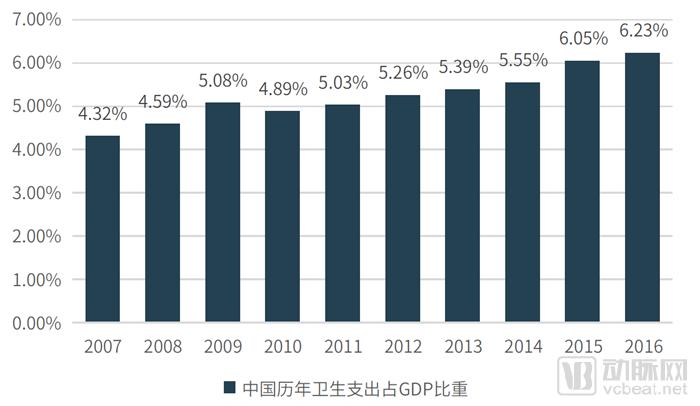

According to the China Health and Family Planning Statistical Yearbook over the years, China’s total health expenditure rose from RMB 1.16 trillion in 2007 to RMB 4.63 trillion in 2016, with its share of GDP increasing from 4.32% to 6.23%, clearly reflecting the growing medical needs of Chinese residents. However, compared with the United States, we anticipate that China’s healthcare industry will continue to maintain a strong momentum of rapid growth in the coming years.

China's Annual Health Expenditure and Its Share of GDP (2007–2016)

Source: China Health and Family Planning Statistical Yearbook; Analysis by VCBeat

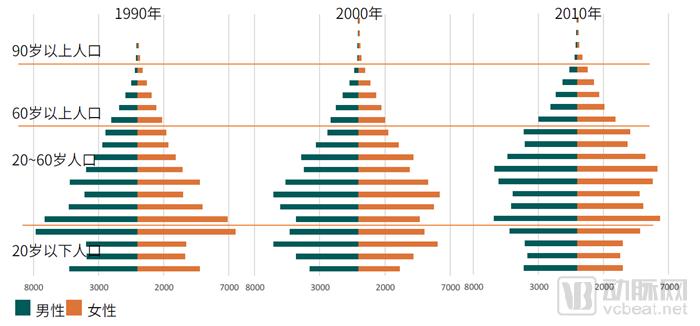

China is currently facing a severe aging trend. In its special report, “Analysis of Development Trends and Investment Opportunities in China’s Healthcare Industry in the Era of Low Fertility,” VCBeat·VBInsight conducted a systematic review and projection of China’s demographic structure, arriving at two key findings: First, the implementation of China’s “two-child policy” has fallen short of expectations, with newborn numbers declining; second, fertility intentions among individuals of childbearing age are low, making a large-scale population decline inevitable.

Statistical Data on China's Historical Population Structure (1990, 2000, and 2010)

Note: 1. The bar chart, from bottom to top, represents age groups in five-year intervals: 0–4 years, 5–9 years, and so on;

2. The unit for each age group in the bar chart is "10,000 people."

Source: Fourth National Population Census, Fifth National Population Census, Sixth National Population Census, VCBeat

Currently, investment in healthcare services is gaining momentum across China, with significant capital already focusing on clinical healthcare service providers encouraged by the government. Compared to policies guiding investment in medical technology-oriented healthcare institutions, policies related to clinical healthcare service providers are more significant in establishing standardized operational norms for these sectors.

3.1 Market Research: Assessing Market Opportunities and Competitive Landscape

The primary risks associated with investing in third-party medical service institutions lie in the substantial capital requirements and the “too big to fail” dilemma inherent in this asset-heavy industry. Therefore, operators or investors should conduct timely and accurate market research during the early stages to define their strategic positioning and gain a clear understanding of current market conditions, thereby avoiding sunk costs resulting from future directional adjustments.

The core components of market research primarily encompass two key areas: demand analysis and competitive analysis. Investigating the demand side enables an assessment of market size, thereby determining whether market entry is worthwhile. Meanwhile, analyzing the competitive landscape helps operators evaluate whether their enterprise possesses the strength to establish a sustainable competitive advantage—often referred to as a “moat”—and secure a share in a fiercely competitive market.

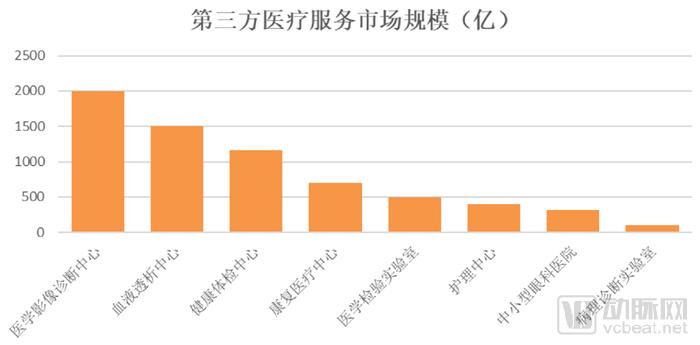

Based on publicly available data, we have estimated the market size for the aforementioned markets:

Data source: VCBeat, public information

We integrated official announcement data from August 2017 with business registration data to estimate the number of third-party service agencies in each subsector:

Number of Third-Party Medical Service Providers

Sources: Qichacha, Tianyancha, VCBeat

Based on VCBeat’s accumulated industry insights, we roughly categorize third-party medical service providers into four distinct markets, using a market size of RMB 50 billion as the threshold for market capacity and a count of 200 related enterprises as the threshold for competitive landscape.

Red Ocean Market: Limited market capacity with intense competition. We have categorized nursing centers into this segment for two primary reasons. First, although China’s aging population trend is intensifying and future demand for nursing care is substantial, awareness of professional nursing services among the elderly remains low at present, indicating insufficient market education. Second, nursing facilities have relatively lower demand for medical personnel compared to other healthcare institutions, making it difficult to establish core competitive advantages, while the industry features a large number of participating enterprises.

Niche Market: Although the market size is relatively small, competition is also comparatively mild. We categorize Central Sterile Supply Departments (CSSD) and hospice care centers under this segment, primarily because they currently receive less attention than other third-party medical service providers, and there are fewer competitors in the market.

Four Market Categories Classified by Market Size and Competitive Landscape

Source: Qichacha, Tianyancha, VCBeat

Potential Market: The market size is large, and competition is intense. The potential market generally includes industries that have reached a relatively mature stage of development, such as health examination centers and small- to medium-sized ophthalmic hospitals. These sectors have been operating in China’s market-driven environment for many years; however, even leading enterprises within these industries face fierce competition and may become trapped in a predicament of price wars.

Blue Ocean Market: A market with substantial capacity and insufficient competition. Among current third-party medical service providers, we have not observed any industry segment occupying this space. This is because, in the commercial world, market equilibrium is typically driven by profit motives, unless a company possesses a core competitive moat. However, a characteristic of the service industry is that while it is difficult to scale up, once significant growth is achieved, the Matthew Effect will be fully realized. Therefore, we optimistically anticipate that third-party medical service institutions capable of establishing strong reputational effects and cost advantages will emerge in this sector.

It should be noted that the above classification criteria merely provide a framework for market analysis, and specific sub-sectors may shift to entirely different quadrants over time as the market evolves.

The above is an excerpt from the White Paper on China’s Third-Party Medical Services Industry 2018. The following content includes:

3.2 Capital Raising: Balancing the Speed and Quality of Expansion

3.3 Location Selection: Enhancing Single-Store Service Utility and Establishing Regional Scale Advantages

3.4 Asset Allocation: Forming a Community of Shared Interests with Upstream Suppliers

3.5 Medical Staff Recruitment: High Dependence on Professional Talent

3.6 Administrative Approval: Further Simplified Procedures and Strong Policy Support

3.7 Market Expansion: Different Logic for Growth Requires High-Quality Services

3.8 Business Expansion: Horizontal and Vertical Integration of the Industrial Chain

IV. The Efficiency of Resource Integration Determines the Rise and Fall of Third-Party Medical Service Providers

4.1 Growth Template: The Path to Growth for Independent Clinical Laboratories

4.2 Resource Allocation Bias Becomes a New Observation Point

Click here to view the report,This report primarily analyzes the key points of ten types of third-party medical institutions, focusing on the overall development history of third-party healthcare service providers and the impact of industry competitive factors.Purchase MembershipFree access to paid reports.