Yestar Medical Aesthetics Files for Hong Kong IPO with Over RMB 2 Billion Revenue in Three Years and 15 Clinics Nationwide

VCBeat (WeChat: vcbeat) has learned that on June 15, Yestar Medical Beauty Group Co., Ltd. (hereinafter referred to as “Yestar”), a medical aesthetics service provider, filed its listing application with the Hong Kong Stock Exchange.

Driven by technological innovations in medical aesthetics and growing consumer attention to medical aesthetic services, the global market for such services is expanding rapidly and is expected to maintain robust growth. In 2017, total global revenue from medical aesthetic services reached USD 125.8 billion, up from USD 90.5 billion in 2013, representing a compound annual growth rate (CAGR) of 8.6%. The market size is projected to reach USD 178.2 billion by 2022, with a CAGR of 7.1% from 2018 to 2022.

After an initial phase of extensive development, China’s medical aesthetics services industry has recently entered a period of rapid growth since the 2010s, driven by the sustained expansion of the overall economy and rising individual incomes, which have created a favorable environment for market development.

Furthermore, in recent years, the government has promulgated a series of policies to regulate the industry, ensuring its more robust development. The Chinese medical aesthetics services market is expected to face a tightening regulatory framework, under which large-scale medical aesthetics service providers will stand to benefit significantly.

According to a Frost & Sullivan report, the total revenue of China’s medical aesthetics services market increased from RMB 86.9 billion in 2013 to RMB 192.5 billion in 2017, representing a compound annual growth rate (CAGR) of 22.0%. From 2018 to 2022, the market is projected to grow at a CAGR of 20.1%, reaching RMB 491.1 billion in 2022.

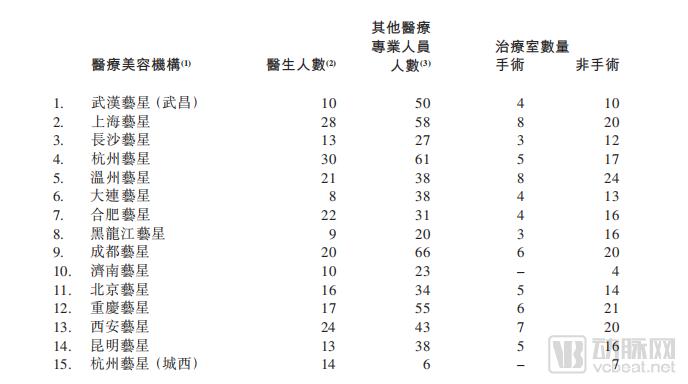

Yestar was established in October 2009. To date, leveraging group-level management and standardized operational processes, it has expanded its network of medical aesthetic institutions through strategic acquisitions and organic growth, establishing a nationwide strategic presence across China. It currently owns and operates 15 medical aesthetic institutions in the core areas of 14 major cities across 13 provinces and municipalities directly under the central government.

Owns 15 hospitals

As of May 31, 2018, Yestar’s medical aesthetic institutions employed 237 physicians, including 9 chief physicians, 34 associate chief physicians, 76 attending physicians, and 118 resident physicians.

Customer Profile and Revenue

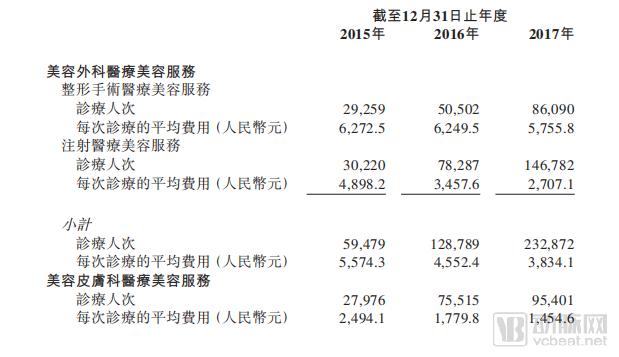

The number of active customers, defined as those who received at least one treatment during the relevant fiscal year, increased from 37,744 in 2015 to 136,591 in 2017, representing a compound annual growth rate (CAGR) of 90.2%.

New customers, defined as those receiving at least one treatment for the first time in the relevant fiscal year, increased from 19,636 in 2015 to 72,795 in 2017, representing a compound annual growth rate (CAGR) of 92.5%.

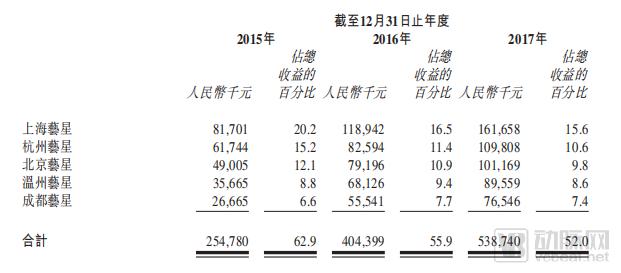

Top 5 Hospitals by Revenue

Existing customers, i.e., customers who meet the following criteria: 1) received at least one treatment during the relevant fiscal year; 2) had previously received at least one treatment. The number of such customers increased from 18,108 in 2015 to 63,796 in 2017, representing a compound annual growth rate (CAGR) of 87.7%.

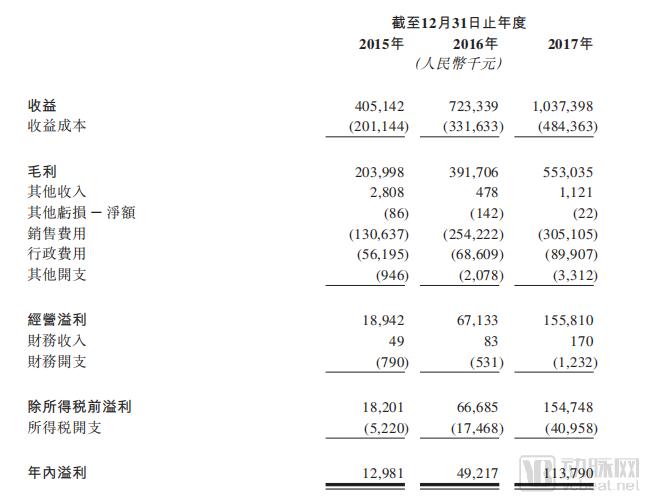

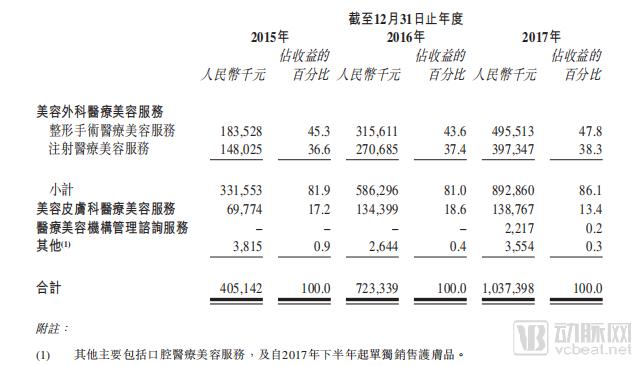

Revenue increased from RMB 405.1 million in 2015 to RMB 723.3 million in 2016, and further rose to RMB 1.0374 billion in 2017, representing a compound annual growth rate (CAGR) of 60.0%.

Net profit increased from RMB 13 million in 2015 to RMB 49.2 million in 2016, and further rose to RMB 113.8 million in 2017, representing a compound annual growth rate (CAGR) of 196.1%.

Business Model

Medical aesthetic services are medical procedures primarily aimed at improving an individual’s appearance. These procedures are generally elective and can be performed on various parts of the face and body. According to the Administrative Measures for Medical Aesthetic Services issued by the former Ministry of Health in 2002, medical aesthetic services are mainly provided by the following departments: cosmetic surgery, cosmetic dermatology, cosmetic dentistry, and cosmetic traditional Chinese medicine.

Aesthetic surgery primarily encompasses surgical cosmetic medical services and injectable cosmetic medical services. Surgical cosmetic medical services refer to surgical procedures aimed at altering the appearance of various facial or body parts (such as the eyelids, nose, breasts, and face), typically involving local or general anesthesia, as well as partial or full incisions.

Injectable medical aesthetic services involve the injection of substances such as botulinum toxin type A, collagen, poly-L-lactic acid, and hyaluronic acid dermal fillers into targeted areas of the face or body to reshape facial or bodily contours or reduce wrinkles. Compared with surgical medical aesthetic procedures, injectable treatments offer a faster recovery time and relatively lower risks.

Aesthetic Dermatology primarily offers energy-based device treatments, which are performed using various forms of energy devices (including lasers, radiofrequency, and ultrasound). These treatments include laser hair removal, laser skin resurfacing for wrinkle reduction, laser treatment for acne scars, laser pigmentation removal, radiofrequency skin tightening, and intense pulsed light (IPL) therapy for skin whitening and rejuvenation.

Yixing’s revenue is primarily derived from providing:

1. Aesthetic surgical medical beauty services, including plastic surgery-based medical beauty services and injection-based medical beauty services;

2. Aesthetic dermatology medical aesthetic services. Plastic surgery medical aesthetic services refer to surgical procedures that permanently alter the appearance of facial or bodily features (such as eyelids, nose, breasts, and facial contours), whereas injection-based medical aesthetic services are used to enhance personal appearance, causing only minimal trauma to the body without leaving surgical incisions.

Yixing’s Revenue Performance Over the Past Three Years

Aesthetic dermatology medical beauty services mainly include energy-based device treatments, such as pigmentation removal, skin whitening and rejuvenation, body contouring, skin hydration, skin lifting and tightening, hair removal, scar repair, soothing for sensitive skin, mole removal, acne treatment, and female intimate area treatments.

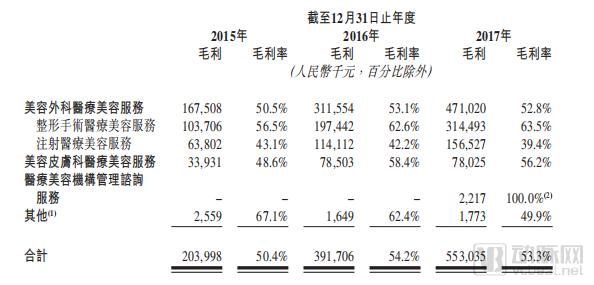

Gross Profit Margins for Surgery, Dermatology, and Management Consulting

Energy-based device treatments achieve aesthetic results by utilizing energy-emitting equipment such as lasers, radiofrequency devices, ultrasound devices, intense pulsed light (IPL) devices, and cryolipolysis machines.

3. Since April 2017, has derived partial revenue from providing management consulting services to medical aesthetic institutions.

Gross Profit Margin and Net Profit Margin

The gross profit margin for injectable medical aesthetic services decreased from 43.1% in 2015 to 42.2% in 2016, and further declined to 39.4% in 2017, primarily due to a decrease in the average fee per consultation, while the cost of injectables (which constitutes the major portion of the cost of revenue for injectable medical aesthetic services) remained relatively stable.

Revenue from Surgery, Dermatology, and Other Departments

The gross profit margin of aesthetic dermatology medical beauty services increased from 48.6% in 2015 to 58.4% in 2016, primarily due to the commencement of operations by newly established medical beauty institutions in 2015 and a substantial increase in their business volume in 2016.

Patient Visits and Clinical Care Overview

Since the majority of revenue and costs for aesthetic dermatology medical beauty services are fixed costs (i.e., depreciation of medical equipment), an increase in patient visits will lead to higher revenue without a corresponding rise in costs, thereby achieving greater economies of scale.

The gross profit margin of aesthetic dermatology medical beauty services was 58.4% in 2016 and 56.2% in 2017, remaining relatively stable.

Competitive Landscape

China’s medical aesthetics service providers mainly consist of three types of institutions: hospitals, outpatient departments, and clinics. Hospitals include general hospitals and specialized hospitals capable of providing all medical aesthetics services, particularly those involving highly complex plastic surgery procedures.

However, outpatient departments and clinics may only provide basic cosmetic surgical procedures for medical aesthetic services. Regarding the establishment of clinical departments, hospitals and outpatient departments may establish all four medical specialties, including cosmetic surgery, cosmetic dermatology, cosmetic dentistry, and cosmetic traditional Chinese medicine. In contrast, clinics may establish no more than two such departments.

With the rapid development of the medical aesthetics industry in China, it may attract more domestic or international practitioners to join, and Yestar will face competition from future market entrants.

Competitors include private specialized medical aesthetic hospitals, outpatient departments, and clinics within the same region, as well as the medical aesthetic departments of public and private general hospitals.

Driven by continuous technological upgrades and advancements, the medical aesthetics industry faces intense competition and rapidly shifting market trends. As clients increasingly seek innovative, high-quality, and cost-effective medical aesthetic services, providers must engage in ongoing competition with their peers across multiple dimensions, including service quality and scope, the comprehensiveness and diversity of medical equipment, and pricing.

Furthermore, it may face competition from numerous unregulated medical aesthetic service providers in the market. These providers do not hold the necessary business licenses and permits but may offer similar services at lower prices.

Dilation

During its nationwide expansion, Yestar plans to expand into new regions through a combination of acquisitions and organic growth, which may result in a larger and more complex organization. Executing the expansion plan is expected to consume management’s attention and energy and incur substantial additional expenses. The ability to successfully expand into new markets depends on numerous factors, primarily including capabilities in the following areas:

1. Identify geographic markets suitable for the provision of services;

2. Determine the preferences of local consumers;

3. Addressing competition in the local market;

4. Negotiate acceptable lease terms, including the desired rent;

5. Hire, train, and retain an increasing number of physicians and other personnel;

6. Successfully integrated new medical aesthetic institutions into the existing control structure and operational systems, including information technology systems;

7. Ensure sufficient funding is secured for financing, maintaining capital investment in new medical aesthetic institutions, or conducting acquisitions.

Furthermore, managing growth and expansion, as well as achieving and sustaining profitability, will continue to depend on management, physicians, administrative, operational, and financial personnel, as well as infrastructure. To accommodate growth, it is necessary to continuously manage relationships with suppliers and customers.

The medical aesthetics business largely depends on the ability to identify, recruit, and retain a sufficient number of qualified physicians. Due to the lengthy training period for specialists (including academic research and clinical training), which can take up to eight years or even longer for certain specialized fields, the short-term supply of specialist physicians is limited. The relative scarcity of qualified physicians in China has led to intense competition in recruiting them.

Strategic Vision

Leveraging high-quality and safe services, Yestar has accumulated a strong reputation and brand influence. Through a robust brand strategy, it has built a broad customer base and a loyal clientele. Meanwhile, by establishing a group-level management structure and standardized operational processes, and supported by an experienced, stable, and international management team, Yestar sustains its rapidly expanding business model.

1. Expand the network layout of medical aesthetic institutions and further strengthen market leadership through strategic acquisitions, organic growth, and the provision of management consulting services;

2. Further improve the quality and standards of medical aesthetic services;

3. Further expand the customer base and enhance brand awareness;

4. Expand our supply of medical aesthetic services and explore opportunities related to stem cells and regenerative medicine;

5. Further strengthen information technology infrastructure.

As one of the fastest-growing medical aesthetics service markets globally, China ranked second in terms of the total number of medical aesthetics procedures and third in terms of total revenue from medical aesthetics services in 2016. This was primarily due to the following factors:

1. The trend of population aging, the growing willingness to improve or maintain personal appearance, and the widespread social acceptance of medical aesthetic services;

2. Rising disposable income and increasing consumption levels;

3. Development of Medical Aesthetic Technologies;

4. Increased capital investment in the medical aesthetics services industry; China’s medical aesthetics services market is projected to sustain rapid development from 2018 to 2022, with a compound annual growth rate (CAGR) of 24.7%, and is expected to reach RMB 302 billion by 2022.

Market Overview

In terms of 2017 revenue, cosmetic surgical medical aesthetic services and cosmetic dermatological medical aesthetic services together accounted for approximately 97% of China’s total medical aesthetics market. Notably, cosmetic surgical medical aesthetic services alone represented 77.8% of the total Chinese medical aesthetics service market by revenue in 2017.

Revenue from medical aesthetic services provided by cosmetic surgery increased from RMB 32.9 billion in 2013 to RMB 77.2 billion in 2017, representing a compound annual growth rate (CAGR) of 23.7%, and is projected to reach RMB 230.8 billion in 2022.

Revenue from medical aesthetic services in cosmetic dermatology increased from RMB 7.6 billion in 2013 to RMB 19.4 billion in 2017, representing a compound annual growth rate (CAGR) of 26.3%, and is projected to reach RMB 64.6 billion by 2022.

Revenue by Department

Among the most popular cosmetic surgery and medical aesthetic services (including double eyelid surgery, breast augmentation, thigh liposuction, and rhinoplasty), the average price of breast augmentation increased steadily from 2013 to 2017 and is projected to experience slight growth from 2018 to 2022, primarily driven by its increasing popularity and relatively high technical requirements.

The approximate average price of rhinoplasty remained relatively stable from 2013 to 2017 and is projected to remain stable from 2018 to 2022. The approximate average prices of double eyelid surgery and thigh liposuction both decreased slightly from 2013 to 2017 and are expected to continue declining from 2018 to 2022, primarily due to intense competition.

Price Trends for Various Services

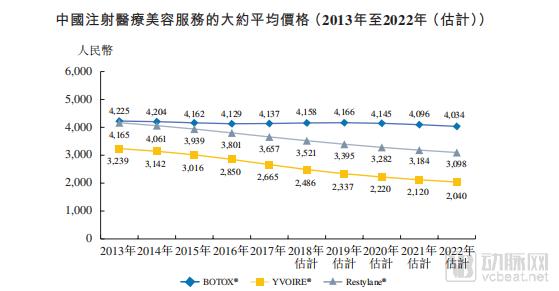

Injectable medical aesthetic services primarily include the administration of type A botulinum toxin and hyaluronic acid. As the only imported brand of type A botulinum toxin approved in China, the approximate average price of BOTOX® injections remained stable from 2013 to 2017. From 2018 to 2022, the approximate average price of BOTOX® injections is expected to remain stable.

In terms of hyaluronic acid injections, the approximate average prices for Restylane® and YVOIRE® injections decreased from RMB 4,165 and RMB 3,239 in 2013 to RMB 3,657 and RMB 2,665 in 2017, respectively, primarily due to intense market competition. The approximate average prices for Restylane® and YVOIRE® injections are projected to continue declining rapidly from 2018 to 2022, as these two overseas brands face increasingly fierce competition from domestic brands.

Price Trends for Injectable Products

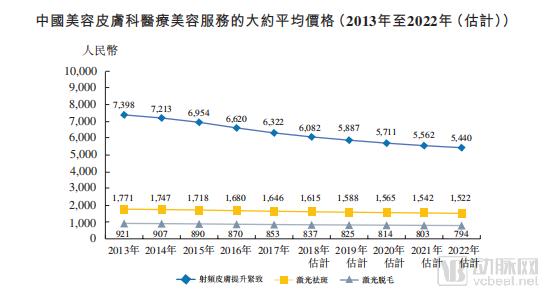

The approximate average prices for radiofrequency skin tightening and lifting, laser pigmentation removal, and laser hair removal decreased from RMB 7,398, RMB 1,771, and RMB 921 in 2013 to RMB 6,322, RMB 1,646, and RMB 853 in 2017, respectively, primarily due to intense market competition. Facing competition from non-medical healthcare centers that also offer certain energy-based device treatments, the approximate average prices for radiofrequency skin tightening and lifting, laser pigmentation removal, and laser hair removal are expected to continue declining during the period from 2018 to 2022.

Skin Care Product Price Trends

Medical aesthetic service providers in China include public and private institutions, with private institutions being the primary market participants. In 2017, private institutions accounted for approximately 80.1% of the total medical aesthetic services market in China by revenue.

Revenue generated by private institutions increased from RMB 31.7 billion in 2013 to RMB 79.6 billion in 2017, representing a compound annual growth rate (CAGR) of 25.8%. Driven by the growing demand for medical aesthetics and the excessive service burden on public institutions, the private medical aesthetics services market is projected to reach RMB 261.2 billion in 2022.

Revenue Status of Public and Private Institutions

In terms of revenue in 2017, cosmetic surgical medical aesthetic services and cosmetic dermatological medical aesthetic services together accounted for more than 97% of the total private medical aesthetic services market in China. In particular, cosmetic surgical medical aesthetic services represented 75.0% of the total private medical aesthetic services market in 2017.

Revenue in the private cosmetic surgery medical aesthetics services market increased from RMB 23.9 billion in 2013 to RMB 59.7 billion in 2017, representing a compound annual growth rate (CAGR) of 25.7%, and is projected to reach RMB 194.6 billion by 2022.

Revenue from the private cosmetic dermatology and medical aesthetics services market increased from RMB 6.9 billion in 2013 to RMB 17.9 billion in 2017, representing a compound annual growth rate (CAGR) of 26.9%, and is projected to reach RMB 61.4 billion by 2022.

Revenue by Department in Private Institutions

Aesthetic surgical medical beauty services mainly include plastic surgery-based medical beauty services and injection-based medical beauty services. In the private medical beauty services market, revenue generated from plastic surgery-based medical beauty services increased from RMB 16.4 billion in 2013 to RMB 40.6 billion in 2017, representing a compound annual growth rate (CAGR) of 25.3%, and is projected to reach RMB 130.6 billion by 2022.

Revenue from Injectable Medical Aesthetic Services at Private Institutions

Revenue from private injectable medical aesthetic services increased from RMB 7.5 billion in 2013 to RMB 19.1 billion in 2017, representing a compound annual growth rate (CAGR) of 26.4%, and is projected to reach RMB 64.0 billion by 2022.

Key Growth Drivers

From 2018 to 2022, China’s private medical aesthetics services market is projected to sustain continuous growth at a compound annual growth rate (CAGR) of 26.5%. This anticipated growth is primarily driven by the following key factors:

1. Growing market demand for medical aesthetic services.With the rapid development of Chinese society, fashion culture and the celebrity effect are gradually reshaping people’s aesthetic perceptions. A growing number of young people recognize the importance of physical appearance and seek to maintain their beauty through medical aesthetic services, which they believe can enhance their prospects in job hunting, romantic relationships, and interpersonal communication. Meanwhile, the population aged 30 to 65 is expanding, and this demographic faces the imminent and noticeable onset of wrinkles and skin laxity within a few years, thereby broadening the target consumer base. Consequently, China’s medical aesthetics market is poised for continued robust growth, underpinned by rising demand for anti-aging treatments.

2. Rising disposable income and consumption upgrading.According to data from the National Bureau of Statistics, China’s per capita annual disposable income increased from RMB 18,311 in 2013 to RMB 25,974 in 2017, representing a compound annual growth rate (CAGR) of 9.1%. The rising disposable income among Chinese residents has enhanced their purchasing power, making them more capable than before of affording medical aesthetic services.

Furthermore, to enhance their quality of life, Chinese consumers are shifting from spending patterns focused on housing and food toward service-oriented consumption. Between 2013 and 2017, the proportion of expenditure on dining and apparel declined from 39.0% to 36.1%, while the share allocated to medical and health services rose from 6.9% to 7.9%. Driven by this trend of consumption upgrading, the level of spending on medical aesthetic services in China is expected to continue growing.

3. Medical technologies are becoming increasingly mature, with relatively low risks.With technological advancements, new medical aesthetic technologies can provide customers with more flexible treatment plans. The application of autologous fat transplantation, endoscopic breast augmentation, and rhinoplasty can enhance the quality of plastic surgery while ensuring procedural safety.

4. Increasing investment in the medical aesthetics industry.The rapid development of China’s medical aesthetics services market has attracted numerous private equity and venture capital firms to increase their investment in the industry. With the influx of capital, medical aesthetics institutions may have sufficient funds to achieve business expansion and form large-scale medical aesthetics chain groups. Furthermore, external capital investment facilitates the introduction of advanced technologies and medical equipment by medical aesthetics institutions, thereby further enhancing the quality of medical aesthetics services.

Barriers to Entry

New entrants in China's medical aesthetics services market face the following barriers to entry.

1. Stringent industry regulatory standards.In China, the medical aesthetics services industry is subject to strict regulation. According to the regulations of the former National Health and Family Planning Commission, providers of medical aesthetics services must apply for licenses in accordance with the Administrative Measures for Medical Aesthetics Services. Physicians practicing medical aesthetics must hold valid professional qualifications or relevant industry certifications. Therefore, providers of medical aesthetics services must comply with applicable laws, regulations, and supervisory guidelines.

2. Place high importance on specialized safety service capabilities.Most consumers prefer to seek treatment at medical aesthetic institutions with specialized service capabilities, which are largely determined by the professional expertise of their physicians. However, senior medical aesthetic physicians are a scarce resource in China, and it typically takes a considerable amount of time to train one. Consequently, new market entrants will face difficulties in recruiting and retaining top-tier medical aesthetic talent, thereby compromising their service capabilities.

3. Difficulty in establishing brand reputation.In China, market participants in the medical aesthetics services industry typically rely on brand image to drive business growth. Meanwhile, customers tend to seek reliable and safe services from well-known medical aesthetics institutions. Any unsatisfactory service experience can negatively impact a service provider’s brand reputation. New entrants find it difficult to establish a strong brand reputation in the short term.

4. Significant capital requirements.To enter the Chinese medical aesthetics services market, new entrants typically require substantial startup capital to procure essential medical equipment and products. In addition, medical aesthetics institutions must lease or purchase suitable premises to deliver medical services to customers, which can entail significant costs. Furthermore, recruiting qualified licensed physicians to provide high-quality medical services and lay the foundation for the sustainable development of market participants necessitates considerable investment in both human and financial resources. Therefore, new entrants must secure ample funding in the initial stages to support their business operations.