Rise of the Niche 'Internet + IVD' Market: A New Growth Engine for Traditional 'Instrument + Reagent' Models?

With the continuous penetration of internet technologies and mobile terminals, and the growing reliance of the national economy and general consumers on the internet, China’s economic development model has fully entered the internet era.

“Internet Plus” has been applied across various industries, and the highly regulated healthcare sector is no exception. Particularly in light of recent policy relaxations regarding “Internet Plus Healthcare” and a stream of positive developments, the prospects for internet-based healthcare are exceedingly promising.

Internet-based healthcare cannot be separated from medical testing, which has also placed the IVD industry, a provider of diagnostic services, at the forefront of growth. The “Internet + IVD” niche market is gradually emerging.

China's IVD Industry Sees Rapid Growth, Reaching a Scale of 65 Billion Yuan

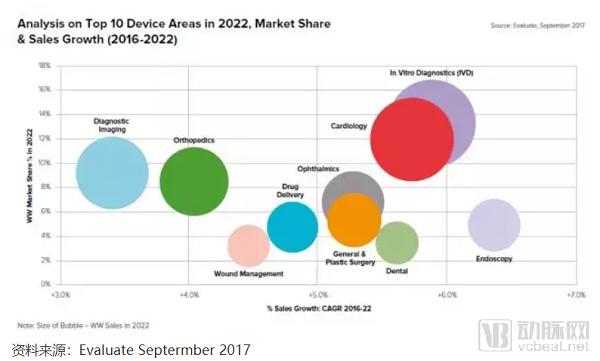

As the largest subsector of the medical device industry, In Vitro Diagnostics (IVD) is hailed as the “eyes of physicians” due to its rapidity, convenience, high accessibility, and high efficacy. By analyzing human samples (such as blood, body fluids, and tissues) outside the human body, IVD provides critical information for clinical diagnostic decision-making. Currently, more than 80% of clinical disease diagnoses rely on in vitro diagnostics.

According to statistics from Evaluate MedTech, in vitro diagnostics (IVD) remains the largest subsector within the medical device industry. From 2016 to 2022, the global IVD industry achieved a compound annual growth rate (CAGR) of 5.9%, surpassing the overall medical device industry’s growth rate of 5.1% during the same period. IVD sales are projected to reach $69.6 billion in 2022, accounting for 13.3% of global medical device sales.

Although China’s in vitro diagnostics (IVD) industry started late, it has developed rapidly. Over the past five years, China has become the fourth-largest IVD market globally, trailing only the United States, the European Union, and Japan. According to statistics from CACLP, the size of China’s IVD market exceeded RMB 65 billion in 2017. While the growth rate of the IVD market is expected to slow down in the future, it will still maintain a growth rate of approximately 15%.

Data Source:Wind, Zhemin Investment (Data as of January 9, 2018)

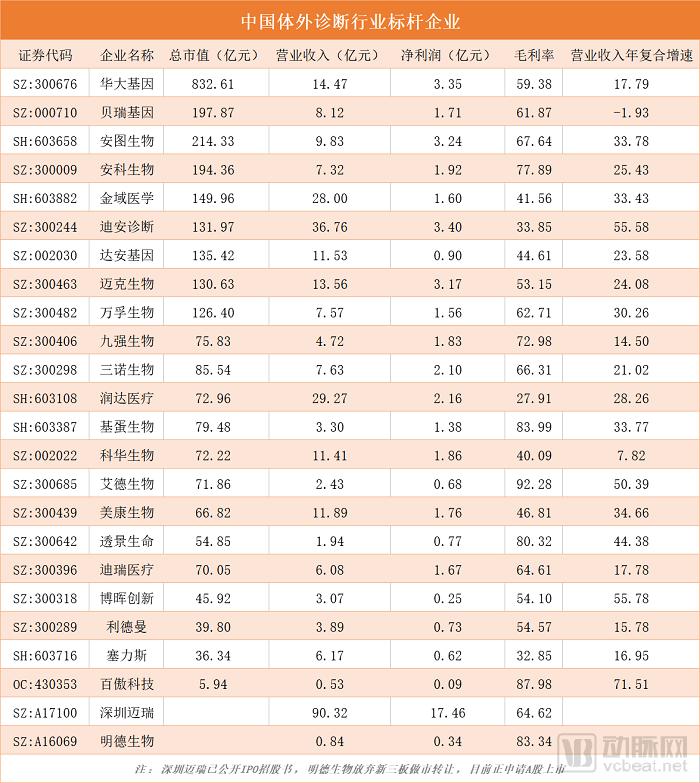

Although China’s IVD industry has been catching up rapidly in recent years, with benchmark companies such as BGI Genomics, Wondfo Biotech, Sinocare, and Getein Biotech having secured a foothold in the market, the industry remains highly fragmented and suffers from severe product homogenization and a lack of core competitiveness. The high-end IVD market continues to be monopolized by imported brands such as Roche, Abbott, and Johnson & Johnson.

Song Haibo, Secretary-General of the China National Association of Health Industry Enterprise Management, stated that by the end of 2017, there were more than 1,000 in vitro diagnostic (IVD) manufacturers and over 20,000 distributors in China. However, fewer than 15 IVD manufacturers had annual revenues exceeding RMB 1 billion, and their combined sales volume was merely equivalent to the domestic sales of a single well-known international brand.

How Chinese IVD companies can narrow the gap with international giants and prevail in the new round of competition amidst such an awkward situation is a question of great concern to the entire industry.

Xu Jianxin, Chairman of Aupu Bio, first proposed the concept of “IVD+.” For China’s in vitro diagnostics (IVD) industry to rise, “IVD+” may offer a new pathway.

The greatest distinction between IVD+ and traditional IVD lies in the organic integration of traditional practices with modern internet technologies, big data management, computing, and artificial intelligence.

With the application of new technologies in the medical field, the entire healthcare industry has entered an era of comprehensive diagnostics and holistic health, where data interoperability and mutual recognition of test results have become inevitable trends. Some traditional IVD companies have also begun to deploy “Internet+” product portfolios, aiming to leverage the internet to provide more precise and effective professional information matching services.

For example, Aupu Bio has proposed the iPOCT concept, Wondfo Biotech has established a presence in personal chronic disease health management, and Mingde Biology has made attempts in “Internet +” data products, among others.“Internet + IVD” has become an indisputable industry trend.

Internet + POCT: iPOCT Enables Personalized Precision Diagnosis and Treatment

As one of the most promising segments within the IVD industry, POCT is characterized by its ease of use, immediacy, and flexibility in sample type selection. With the integration of the internet and medical informatics, POCT is increasingly becoming internet-enabled, a trend that has emerged in recent years with the appearance ofThe Concept of iPOCT (Intelligent Point-of-Care Testing).

The core concept of iPOCT is characterized by “automation, cloud integration, and precision.” As a product of integrating POCT with the Internet and big data, iPOCT enables real-time recording and monitoring of test results. Furthermore, through cloud-based platforms, physicians can gain real-time insights into patients’ conditions, provide timely feedback, and adjust treatment plans as necessary.

For example, Alere’s RALS System in the United States is a personalized system that integrates data with products. It collects patients’ test results and relevant data from point-of-care devices, evaluates the data based on user-configurable criteria, and transmits it to a central laboratory (or physician) for analysis within an information system that delivers corresponding results. Reportedly, this device is now used by more than 2,000 hospitals across the United States.

According to VCBeat, by the end of 2017, numerous manufacturers had implemented the iPOCT concept, such as Aupu Bioengineering with its gold immunochromatography, turbidimetry, and fluorescence platforms; Liangdian Technology with its quantum dot platform; and Cosmile with its chemiluminescence platform. In addition, some publicly listed companies have established dedicated teams to develop next-generation products.

Taking Aupu Bio as an example, it is the earliest enterprise to enter the POCT field, second only to Wondfo Biotech.Over the past two decades, Autobio has defined the Chinese term for POCT, promoted the promulgation of relevant national standards, proposed innovative concepts such as iPOCT, and implemented the application of the iPOCT concept at the point of care through its existing product portfolio.

In particular, the Automan fully automated specific protein point-of-care testing analyzer, launched in 2015, ushered in a new era of fully automated, track-based, whole-blood testing, and batch testing of capillary blood. The recently launched Mini+ fully automated specific protein analyzer not only inherits the features of the Automan but also sets a new record for the smallest footprint among fully automated specific protein analyzers.

Aubio is a rare enterprise in the POCT field that possesses innovative thinking. It is also a company with multidisciplinary foundations in optics, mechanics, electronics, biology, big data, and the internet. Currently, it has achieved certain results in H-type innovation and in promoting the development of POCT products toward artificial intelligence and big data.

Achieving precise results is the most significant pain point in the current POCT industry. To attain testing performance comparable to that of central laboratories, the POCT sector has proposed the concept of “Lab on a Chip.” However, for certain assays, such as glycated hemoglobin (HbA1c), conventional methods struggle to meet clinical standards. It is imperative to develop more advanced technologies, such as microfluidics and novel sensors, to truly fulfill clinical requirements.

However, the current challenge is that while the technology is feasible, the cost is not; conversely, when the cost is manageable, the technology remains unattainable.With the evolution of technology, new disruptive technologies are likely to emerge in the future to balance cost and performance.

New IVD Trend: “Small but Beautiful” Internet-Based Health Testing

The miniaturization of IVD devices (especially POCT) is currently the mainstream trend, and the ultimate form of miniaturization is “virtualization,” giving rise to an emerging, disruptive testing technology—Internet-Based Virtual Instrument Testing。

This is an emerging in vitro diagnostic (IVD) approach that leverages software systems to replace traditional instruments for diagnostic purposes. It requires no physical hardware (including both conventional instruments and smart hardware), incurs no hardware costs, offers superior mobility, and achieves medical-grade testing performance, thereby effectively addressing the current challenge in the IVD industry of balancing cost and performance.

With the emergence of internet-based virtual instrument testing methods, a new niche sector within the in vitro diagnostics (IVD) industry has been born: the internet health testing industry.

VCBeat has compiled a list of the major global players currently relying on internet-based virtual instruments for health monitoring, including 10 companies and one individual. These include Scanadu from the United States, Chert from Switzerland, U-Check from India, as well as the following Chinese enterprises: Baokailun, Yunyanxing, Kangyun Hulian, Niaodafu, Yunzhijian, Zhangyi Technology, Puze Zhongkang, and Youshan.

Chinese enterprises mainly emerged in 2015 and 2016, indicating that the entire Chinese internet health monitoring market is still very young. The only companies with public financing are Yunyanxing (Chunfeng Venture Capital) and Kangyun Interconnect (Mango Capital).

According to publicly available information, the only companies worldwide known to have obtained medical device qualifications are Chert from Switzerland and the Chinese enterprise Kangyun Hulian. The latter has undergone systematic medical device inspection, testing, and certification in both China and Germany. Its data meets the requirements of various certification bodies, while no other companies have publicly provided comparable data at this time.

According to information previously obtained by VCBeat, Kangyun Interconnect’s “Cloud-Based Intelligent Detection System” (CONIN) passed the review of the National Medical Products Administration in April 2018 and officially obtained a medical device registration certificate, making it the first qualified “Internet + IVD” medical testing system in China.With this system, users can achieve medical-grade health testing using just a smartphone and a test kit, without the need for any hardware instruments.

From a product portfolio perspective, Kangyun Hulian is currently the company with the most comprehensive product line among all enterprises. It offers a wide range of testing services, including vital signs monitoring, routine urinalysis, biochemistry, immunology, specific protein assays, genetic testing, food safety testing, and environmental testing. These offerings cover more than 80% of health-related tests available on the market, enabling the management of nearly all conditions within general internal medicine. In contrast, other companies in the market currently offer only routine urinalysis.

In terms of patent layout, Kangyun Interconnect is also the enterprise with the highest number of patent applications. It has currently laid out more than 100 intellectual property rights, including dozens of patents (25 of which are invention patents), covering various core links such as detection systems, detection methods, and sensors.

According to industry authorities, internet-based health testing is an emerging market characterized by low public awareness, inadequate regulations, and considerable disorder. Consequently, professionals generally believe that a truly compliant internet-based virtual instrument testing system should possess the following characteristics:

First, complete certification is required; specifically, both the reagents and software must hold Class II or higher medical device registration certificates. Otherwise, the testing system would be considered non-compliant, and the use of unlicensed medical devices may even constitute a criminal offense under the Criminal Law.

Second, given the high concentration of patents in the industry, products that lack licensing for core technology patents and rely solely on packaging patents and pending invention applications are highly likely to be infringing.

Third, if reagents are not encrypted, they cannot be traced in an open environment. In the event of safety hazards, it becomes difficult to assign liability, posing challenges for law enforcement. Furthermore, the lack of encryption prevents companies from establishing a closed-loop business model.

The Rise of Internet Healthcare: A New Dawn for Online Health Monitoring

In recent years, China has been in an accelerated phase of healthcare reform, and internet healthcare has developed rapidly by leveraging policy dividends. Particularly this year, the state has comprehensively encouraged the development of “Internet + Healthcare,” ushering internet healthcare into a period of robust growth.

On April 11, Premier of the State Council Li Keqiang, Shanghai Municipal Party Secretary Li Qiang, Director of the National Health Commission Ma Xiaowei, Shanghai Mayor Ying Yong, and other leaders conducted an on-site inspection at the Telemedicine Center of Huashan Hospital Affiliated to Fudan University to examine the new pattern of tiered diagnosis and treatment established through models such as “Internet + Healthcare” and medical consortia.

On April 12, the Premier presided over an executive meeting of the State Council. Matters related to healthcare included: first, the adoption of measures to develop “Internet Plus Healthcare” to alleviate difficulties in accessing medical care and improve public health; second, the decision to implement zero tariffs on imported anticancer drugs and encourage the import of innovative drugs, thereby responding to public expectations and enabling greater benefits for patients.

On April 28, the General Office of the State Council issued the "Guiding Opinions on Promoting the Development of 'Internet + Healthcare'," explicitly stating that internet hospitals may be developed with medical institutions as their foundation; encouraging upper-level medical institutions within medical consortia to leverage artificial intelligence and other technological means to provide remote consultation, remote ECG diagnosis, remote imaging diagnosis, and other services to grassroots levels; and encouraging the use of wearable devices to collect vital signs data for health monitoring and management of pregnant and postpartum women, among other measures.

“Internet + Healthcare,” a lucrative sector valued at hundreds of billions of yuan, has naturally become a fiercely contested arena for internet giants. As early as 2011, BAT (Baidu, Alibaba, and Tencent) had already made strategic moves in the internet healthcare space, giving rise to numerous well-known digital health companies such as WeDoctor, Haodf Online, DXY, Chunyu Doctors, Ping An Good Doctor, and AliHealth.

Current internet healthcare companies primarily operate in areas such as appointment scheduling intermediation, doctor-patient communication, pharmaceutical e-commerce, offline clinics, physician tools, and smart hardware. Consequently, the internet healthcare sector has largely realized multiple processes, including appointment booking, payment, lightweight consultations, and medication purchasing.

However, there is still a critical link in the entire internet healthcare sector that has not been adequately addressed: testing.The current development of internet-based healthcare still relies on offline health examinations as the basis for diagnosis. Since it is difficult for physicians to make an accurate diagnosis based solely on patients’ descriptions, in most cases, patients are still required to visit hospitals for tests, which incurs substantial time costs.

It can be said that the testing phase is currently the bottleneck of internet healthcare.Whoever solves this problem will be the first to achieve a closed-loop business model in internet healthcare.

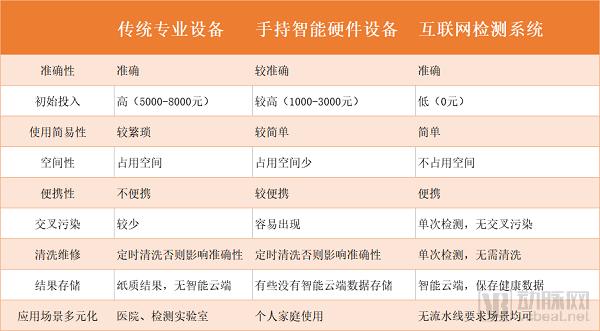

Currently, there are three main methods by which internet healthcare companies complete testing:Through testing with traditional offline instruments, through testing with smart hardware or wearable devices, and through testing with internet-based virtual instruments。

The First TypeOffline traditional instrument-based testing is currently the mainstream diagnostic approach, characterized by mature technology and high recognition. However, it heavily relies on physical hospitals and incurs high costs for equipment, facilities, and personnel. The lack of mobility in such traditional testing methods renders them of limited value to internet healthcare.

Second TypeSmart hardware and wearable devices have represented a major trend over the past decade, addressing the immobility of traditional diagnostic methods and gaining a certain degree of market recognition. However, these portable smart devices and wearables offer very few health monitoring capabilities, with medical-grade options being particularly scarce, which has drawn significant criticism from the industry. Furthermore, their high prices coupled with limited testing functionalities result in weak consumer purchase motivation, thereby constraining market size.

The last oneThis refers to the aforementioned internet-based virtual instrument testing, which leverages software systems to replace traditional instruments for diagnostic purposes. It requires no physical hardware (including both traditional instruments and smart hardware), incurs no hardware costs, offers superior mobility, and achieves medical-grade testing accuracy.

Compared with the first two testing methods, internet-based virtual instrument testing offers significant advantages. We boldly predict that, driven by the dual forces of “policy + technology,” the internet health testing industry may become the next major growth opportunity for the IVD industry.

Exploring the Business Model of "Internet + IVD"

As the next wave of opportunity approaches, can companies in the niche sector of internet-based health diagnostics seize the moment and capture the dividends brought by the growth of digital healthcare? Compared with traditional IVD enterprises, what business models will they adopt?

Traditional Model: Distributors pave the way, instruments open the door, and reagents generate profits.

According to VCBeat, most in vitro diagnostic (IVD) companies in China currently rely on distribution channels as their primary sales route, generating excess profits through reagent sales.

Unlike pharmaceuticals, most in vitro diagnostic (IVD) products are distributed through channels. Manufacturers establish differentiated distribution rights, such as first-tier and second-tier distributors, based on the scale of their agents to facilitate channel distribution. For key high-value customers, manufacturers may occasionally opt for direct sales to achieve higher profit margins.

In vitro diagnostics is a high-margin industry, particularly for reagents and consumables, with an average gross margin of 70% across the sector. Consequently, for hospitals with large sample volumes, distributors often provide instruments free of charge at very low prices or through zero-cost placement models, recouping the instrument costs via reagent sales. In contrast, mid- to low-tier hospitals lack sufficient sample volumes to support such cost-free instrument models; therefore, both instruments and reagents are sold directly.

Innovative Model: Open Platform, Serving Upstream and Downstream

The emergence of internet-based virtual instrument testing systems has transformed this traditional model. Internet IVD companies, no longer reliant on physical instruments, have abandoned the conventional profit model of selling instruments and reagents. Instead, they leverage the advantages of the internet to create open platforms that serve both upstream and downstream partners, thereby generating corresponding returns.

Taking Kangyun Hulian as an example, the company plans to build an open platform based on a cloud-based health monitoring system, making standards and authorization publicly available to allow upstream and downstream institutions and enterprises to connect. By providing value-added services to upstream and downstream enterprises, it empowers the entire industrial chain to drive industry advancement.

The open health testing platform serves as a bridge connecting traditional IVD companies with numerous internet healthcare giants, representing an opportunity for manufacturers to engage in internet healthcare while also addressing a critical need within the sector.

For upstream IVD manufacturers, adapting and upgrading traditional test strips to smart test strips involves production processes and workflows that are largely consistent with those for traditional instruments. However, this transition enhances product value-added, thereby driving profit margin growth. Furthermore, by leveraging the advantages of the internet, companies can capitalize on online opportunities, reach a broader user base, and expand their sales channels.

Meanwhile, this also represents a significant benefit for downstream internet healthcare platforms, insurance companies, big data firms, pharmacies, clinics, and elderly care institutions; empowered by internet-based testing, the creation of closed-loop business models has become possible.

In summary, against the backdrop of the internet era, future diagnostic products will evolve toward miniaturization (even virtualization), automation, precision, cloud integration, sharing, and data-driven capabilities.

Furthermore, as new technologies such as the Internet, cloud computing, big data, and artificial intelligence are increasingly applied in the IVD industry, the future development path of the IVD sector will shift “from Diagnostic to Data,” meaning from diagnostic reagents to big data. In other words, under the transformative trend advocated by “Internet + IVD,” the primary competitive arena for IVD companies will evolve from product competition in diagnostic reagents to intelligent health monitoring based on in-depth big data services.

However, the healthcare industry differs from other sectors, as diagnostic results must be accountable to patients; a misdiagnosis could drastically alter a patient’s life. While the adoption of new technologies may bring considerable convenience to both hospitals and patients, it also poses risks to patient privacy and hospital data security. Consequently, many traditional in vitro diagnostics (IVD) companies remain cautious about applying emerging technologies to disease detection.

For the nascent internet-based health testing industry, we are optimistic about its growth prospects and look forward to it injecting fresh vitality into the IVD sector; however, its business model remains to be validated.