Four Types of Integration Ahead: The Future of Chinese Medical Groups Viewed Through Sino-U.S. Healthcare Disparities

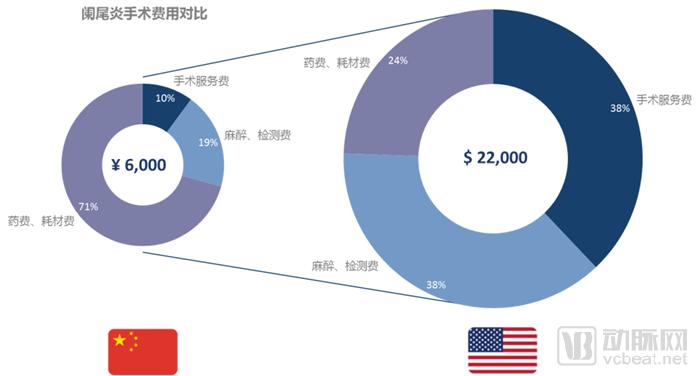

Currently, there is a significant disparity in the intrinsic value of physicians practicing in the United States and China. Taking appendectomy as an example, the cost for the same procedure is approximately RMB 6,000 in China, whereas it amounts to USD 22,000 in the United States. The surgeon’s fee, which reflects the physician’s professional value, accounts for about 10% (approximately RMB 600) of the total cost in China, compared to roughly 38% (approximately USD 8,300) in the United States.

If we look solely at the absolute surgical costs, the revenue for appendicitis treatment in the United States is approximately 20 times that of China. However, if we examine surgical service fees—which reflect the value of physicians—the figure in the United States is nearly 90 times higher than in China. This disparity underscores the difference in the intrinsic value of physicians between the two countries and serves as a key internal driver that will increasingly motivate doctors to leave the “public system” in the future.

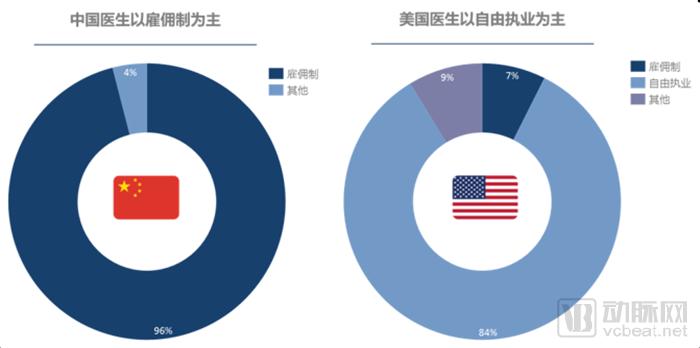

Beneath the vast disparity in intrinsic value lies the difference in the degree to which doctors in China and the United States are affiliated with hospitals. In the U.S., physicians primarily practice independently. More than 84% of practicing physicians in the U.S. are in independent practice, while only about 7% are employed. In contrast, among the nearly 5 million licensed physicians in China, close to 96% are either employed or practice at designated institutions, commonly referred to as “institutional affiliates.”

Due to China’s unique historical and institutional context, the government maintains tight control over healthcare service providers and health insurance payments. As specialized service professionals, physicians are treated as core resources tethered to the state-run system. The relationship between hospitals and doctors is akin to that of the urban-rural household registration (hukou) system or peasants bound to the land under the collective land tenure system; the medical profession remains firmly locked in place, unable to achieve fully market-driven, free mobility to this day.

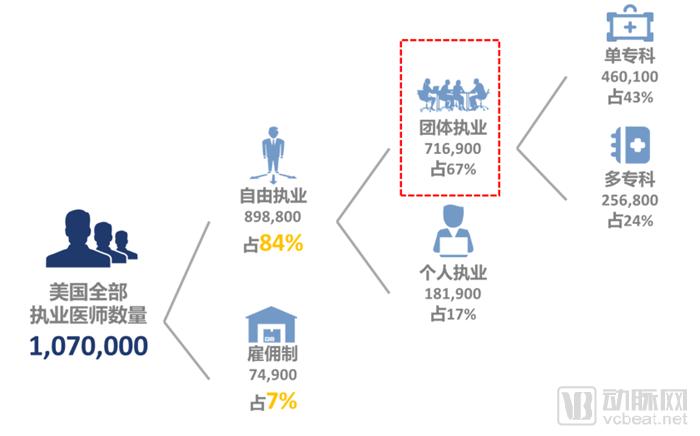

In the United States, private practice is the predominant mode of medical practice, with the majority of physicians engaged in group practice. Among the more than one million practicing physicians in the U.S., those in group practices account for 67% of all privately practicing physicians. Of these, 43% belong to single-specialty physician groups, reflecting a trend toward specialized division of labor within the U.S. healthcare system. Nearly half of all physicians in group practices are part of small, specialized groups comprising ten or fewer members.

1988,The United States enacted the Stark Law, which established detailed legislative provisions for physician groups and laid the foundation for their subsequent development. The core of the Stark Law encompasses four key aspects:

Physician groups must be registered as a single, legal entity.

Group Medical Practice (Physician Group) requires two or more physicians to jointly register as a single legal entity. Both for-profit and non-profit structures are permissible, provided the primary objective is to deliver Designated Health Services (DHS). Physician groups may take various forms, including professional corporations, limited liability companies, foundations, non-profit corporations, unincorporated associations, and other such entities or organizations.

Physician groups shall provide at least 75%.Medical Services

Physician groups should focus on medical services as their core business, with patient-oriented medical services accounting for at least 75% of the group’s workload.

Physician Groups Must Establish a Unified Fund Management Mechanism

Physician groups should establish internal decision-making mechanisms to centrally manage and control group assets, revenues, and expenditures; the medical service income of all member physicians shall be uniformly managed by the group.

The total profits of physician groups are primarily derived from medical insurance funds.

The overall profits of physician groups primarily stem from payments for health services designated by U.S. government-sponsored insurance programs such as Medicare and Medicaid, as well as reimbursements from commercial health insurance. The Current Procedural Terminology (CPT) codes serve as the primary basis for determining insurance payment amounts and for the internal distribution of revenues within physician groups.

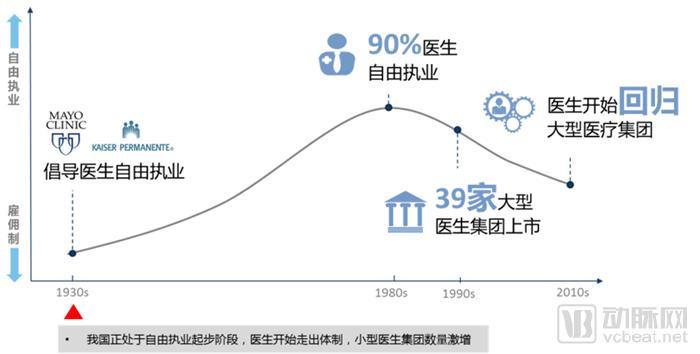

The practice of independent physician practice in the United States began in the 1930s, pioneered by the Mayo Clinic and Kaiser Permanente, and peaked in the 1980s, with nearly 90% of physicians practicing independently.A turning point emerged in the 1980s, as some physicians began to shift from independent practice back to an employed model.

This shift stems from three factors: first, the enactment of the Stark Law mentioned above, which provided legal regulation for the development of physician groups.

Second, the development of new Health Maintenance Organizations (HMOs) has squeezed physician groups.The healthcare delivery system has always been a dynamic game involving three parties: physicians, hospitals, and insurance companies. Due to imbalanced and conflicting interests among these stakeholders, the system has been characterized by a zero-sum dynamic. The emergence of Health Maintenance Organizations (HMOs) serves as a typical example of how hospitals and insurers formed an alliance of shared interests, thereby enhancing the bargaining power of physician groups.

Third, with the rapid development of HMOs and intensifying competition, many independent physicians have been unable to bear the high fixed costs of solo practice (such as those for health information systems and personnel). This has led many independent physicians to return to employed models, leveraging group operations to amortize fixed costs—a trend that has persisted to this day.

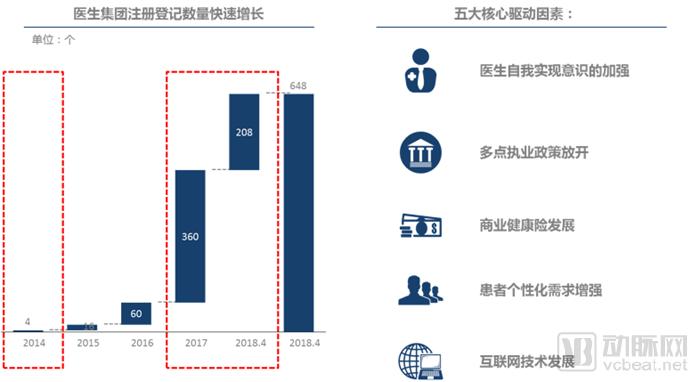

In contrast, China is currently at a stage similar to that of the United States in the 1930s, marking the initial phase of physicians’ transition from an employment-based model to multi-site practice and, ultimately, independent practice. As doctors begin to move outside the traditional public healthcare system, the number of registered small physician groups has surged.

The registration of domestic physician groups began to emerge in 2014.(The First Bodexiaolian), with the liberalization of the multi-site practice policy, an increasing number of physician groups began to emerge rapidly, leading to a substantial surge in registered physician groups by 2017. The primary drivers include five factors:

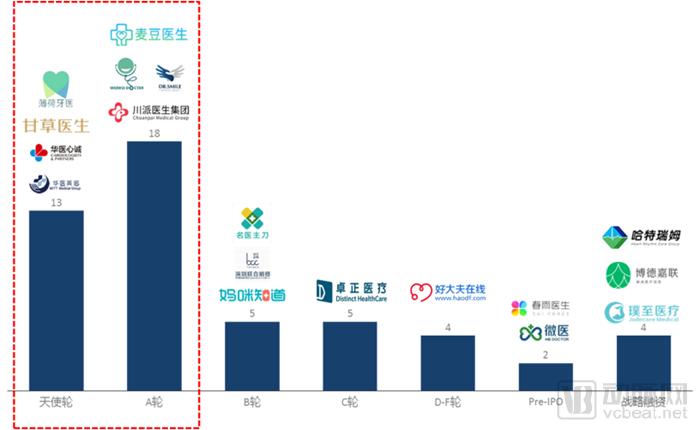

From the perspective of the capital market, an increasing number of physician groups have garnered investor interest and secured financing. However, the vast majority of these financings remain in the relatively early angel and Series A stages. It is foreseeable that, over time, more physician groups will obtain funding, with investment activity progressively shifting toward the more mature mid-to-late stages.

As mentioned above, the healthcare service system is a dynamic game involving three core stakeholders: “physicians–hospitals–payers.” Therefore, based on physicians’ affiliation with medical institutions (primarily hospitals) and their level of integration with payers (mainly social insurance and commercial insurance), we categorize physician groups into four types: comprehensive physician groups, hospital-affiliated physician groups, insurance-linked physician groups, and platform-based physician groups.

Among them, the comprehensive physician groups in the first quadrant are relatively leading players, such as Dr. Zhang Qiang Physician Group, Donglei Brain Hospital, Zhuozheng Medical, and Bodajia Lian. These medical groups typically possess substantial medical resources, operate their own offline medical institutions, and have partially or fully integrated with payers, including insurance companies.

Platform-based physician groups in the third quadrant typically do not own physicians or medical institutions; instead, they operate as third-party service providers for physician groups. By leveraging internet platforms to facilitate connections among physicians, hospitals, and patients, they establish a platform-oriented business model. Examples include Mingyi Zhudao, Xingren Yisheng, and Haodafu.

Currently, the development of physician groups remains in its early stages, and they continue to face significant challenges in the future, primarily stemming from two aspects:

On one hand, it stems from policies and regulations, as reflected in the relatively outdated legislation on physicians’ independent practice, which has led to slow progress in this area; and in the absence of laws and regulations governing the nature and oversight of physician groups, resulting in an unclear medical identity for such entities.

On the other hand, it stems from management and operations., the core question is whether an excellent physician can become an outstanding operational manager. The operational management team of a physician group not only needs to accumulate medical resources but also requires extensive operational experience in human resources systems, financial systems, marketing and sales systems, and information technology systems. This imposes high competency requirements on physicians serving in management roles.

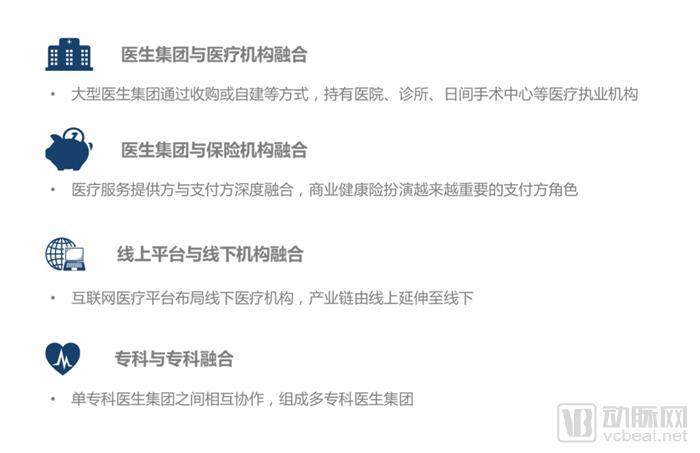

Looking ahead, the future development trends of physician groups will be increasingly characterized by “integration” in four key areas:

In conclusion, we remain firmly optimistic about the future development of physician groups and are convinced that the era of physicians practicing independently will inevitably arrive. Admittedly, although physician groups are still in their early stages of development and face numerous challenges, the opportunities undoubtedly outweigh the challenges.

We believe that with the continuous liberalization of policies, the ongoing development of commercial health insurance, the growing awareness among physicians of their self-worth, and the increasing demand for personalized care from patients, physician groups will undoubtedly become an integral part of China’s healthcare service system, and even emerge as a key provider in the future healthcare delivery landscape.

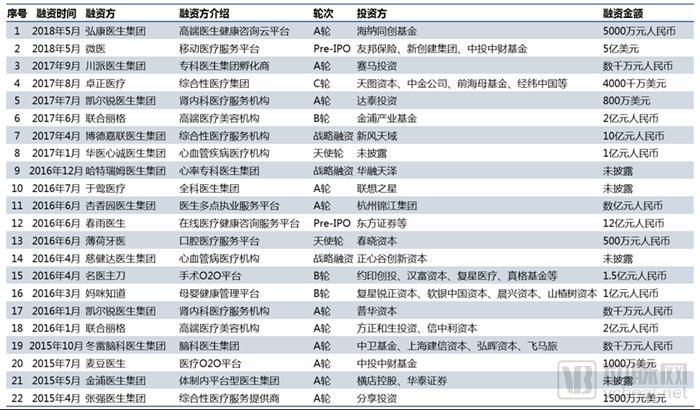

Appendix: A Review of Financing Cases and Policies Related to Physician Groups

This article is compiled from the author’s speech at the inaugural meeting of the Physician Group Branch of the China Non-State Medical Healthcare Institutions Association.

Author Biography

Liu Zeyuan, Senior Manager at China Renaissance Capital, specializes in investment, financing, and mergers and acquisitions within the healthcare services sector. He previously worked at McKinsey & Company and Accenture Consulting, and holds a Master’s degree in Economics from the London School of Economics and Political Science (LSE).