Intuitive Surgical Reports Q1 2026 Revenue Growth of 23% and da Vinci Installations Reach 431 Units

Medtronic

Chronic Disease Medical Device and Therapy Developer

April 21, 2026Intuitive Surgical Releases Q1 2026 Earnings Report: Revenue of $2.77 billion, Up 23% Year-over-Year; Non-GAAP EPS of $2.50, Beating Wall Street Consensus by $0.39.Global surgical volume (da Vinci + Ion combined) increased year-over-year by approximately17%, where da Vinci grew by approximately16%, Ion increased by approximately39%。

This is Intuitive's consecutive double-digit revenue growth over multiple quarters, and it is also the first full-quarter report card after Hugo, Ottava, Versius, and other competing products were successively approved or submitted to the FDA.

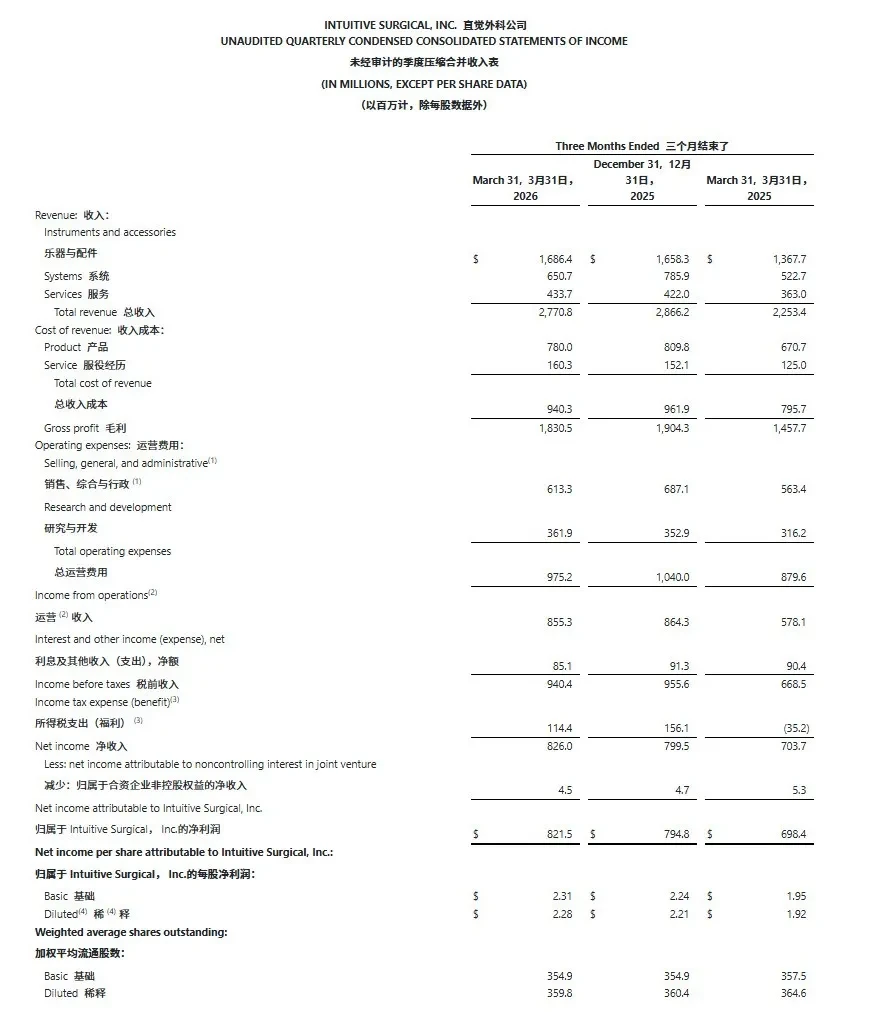

# Core Financial and Operational Data

Intuitive Installations This Quarter431 da Vinci Systems(367 units in the same period last year), including 232 units of da Vinci 5, representing a 58% increase from 147 units in the same period last year.da Vinci 5 accounted for 54% of the new installations this quarter, becoming the main driver of new installations.Ion system installations reached 52 units, compared to 49 units in the same period last year, indicating a slowdown in growth.

As of March 31, 2026,The global installed base of da Vinci reached 11,395 units (up 12% year-over-year), and the installed base of Ion reached 1,041 units (up 22% year-over-year).

In terms of revenue structure:Revenue from consumables and accessories was $1.686 billion (+23%), system revenue was $651 million (+24%), and service revenue was $434 million (+19%). Consumables remain the largest source of revenue, accounting for 61% of total revenue, and are directly linked to surgical volume, forming the most stable growth engine in Intuitive's business model.

Profit End:GAAP Gross Margin 66.1% (64.7% in the same period last year), Non-GAAP Gross Margin 67.8% (66.4% in the same period last year). GAAP Operating Profit $855 million (+48%), Non-GAAP Operating Profit $1.077 billion (+40%). Net Profit $822 million, a year-on-year increase of 17.6%.

Total cash and investments at the end of the quarter were $7.98 billion, a decrease of $1.05 billion from the end of the previous quarter, primarily due to $1.1 billion in stock repurchases and an unnamed corporate acquisition.

# Competitive Landscape: Soft Tissue Track Enters Multi-Player Era

Intuitive has maintained a factual monopoly in the soft tissue surgical robot field for over two decades. However, from the end of 2025 to early 2026, the competitive landscape underwent a substantial change:

- Medtronic Hugo:FDA Urology Indication Approval Expected in December 2025, with the First Surgery in the U.S. Completed at Cleveland Clinic in February 2026. Currently advancing clinical trials for general surgery and gynecological indications. Hugo has already performed tens of thousands of surgeries across more than 30 countries outside the U.S., featuring a modular split-cart design targeting the mid-to-low cost market.

- J&J Ottava:Submit De Novo classification application to FDA in January 2026, with indications covering various upper abdominal general surgeries (including Roux-en-Y gastric bypass). Six-arm structure, targeting multi-quadrant complex surgeries. IDE clinical trial for inguinal hernia repair expected to be approved by the end of 2025. No market approval has been obtained yet.

- CMR Surgical Versius:Received FDA approval for cholecystectomy indication in October 2024. Versius Plus has been approved by the FDA and is advancing U.S. commercialization. Globally, its surgical volume ranks second only to da Vinci (as per company statement).

Comparison of Main Competitors in Soft Tissue Surgical Robotics (As of April 2026)

# Structural Issues Behind the Data

Intuitive's performance this quarter is impeccable in absolute numbers, but there are a few structural signals worth noting.

First, the proportion of da Vinci 5 installations between "replacement" and "incremental" remains unclear.Out of the 431 newly installed systems, Intuitive did not disclose how many were existing customers upgrading from da Vinci Xi/X and how many were net new customers. With an installed base of over 11,000 systems, the cost and difficulty of acquiring net new customers are key to assessing the quality of long-term growth.

Second, the proportion of operating leases has increased.Of the 431 da Vinci installations in Q1, 243 units (56%) were under operating lease, including 118 units on a pay-per-use lease; this compares to 198 units under lease (54%) in the same period last year. The leasing model lowers the upfront capital threshold for hospitals, helping to expand the installed base, but may also reflect tightening capital expenditure in some markets.

Third, the uncertainty of the tariff path is not unique to Intuitive, but its supply chain's reliance on Mexico exposes it more than most of its medical device peers.The company is expanding its capacity in California and Georgia, and planning new factories in Germany and Bulgaria, but the transfer of capacity will take time.

On the competitive front, the FDA approvals of Hugo and Versius alone are unlikely to shake Intuitive's market share in the short term—da Vinci's accumulated clinical evidence, surgeon training system, and consumables lock-in effect form a deep moat. However, for small and medium-sized hospitals that have yet to establish robotic surgery programs, Hugo’s pricing flexibility and Medtronic’s channel advantages in traditional surgical instruments may make it an alternative option for entering the market. Intuitive’s move to further increase the proportion of operating leases and usage-based billing models in Q1 is, objectively, also a preemptive response to potential competition.

# 2026 Guidance: Tariff Risks Quantified

Intuitive Maintains Full-Year da Vinci Surgical Volume Growth Expectation of 13.5%–15.5%.Notably, the actual growth rate of da Vinci surgeries in Q1 was approximately 16%, exceeding the upper limit of the full-year guidance—this implies that the company anticipates a slowdown in growth for subsequent quarters or is adopting a cautious stance towards the macro environment.

The Impact of Tariffs is Clearly Quantified:The company expects tariffs to impact approximately 1.0% of revenue, reflected in the Non-GAAP gross margin guidance of 67.5%–68.5%. This is a slight reduction compared to the 1.2% tariff impact estimate provided during the Q4 earnings report. Intuitive currently manufactures most of its consumables and accessories in Mexicali, Mexico, produces endoscopes in Germany, and sources some materials from China. In its forward-looking statements, the company warned that if additional tariffs exceed expectations, the impact on financial results "could be material."

BTIG analysts summarized this quarter's performance as "growth with guardrails," noting that surgical volumes and system installations continue to exceed expectations, but pressures from competition, pricing, and hospital capital expenditures have emerged in the China, Japan, and European markets.

Well-known surgical robot companies and upstream and downstream enterprises

Comprehensive▌Minimally Invasive Robot | Toda Medical | Intuitive Fosun | Weigao

Endoscope▌Medtronic | Sizherui Intelligent Medical | Constance Medical

Orthopedics▌Rosenthal | MetaMed Intelligent | Changmu Valley | Xin Jun Te| Stryker

Vascular Intervention▌Aibohc | Weimai Medical

Puncture Robot▌True Health | Medtronic

Surgical Robot Tools▌Good Doctor