Edwards Lifesciences Q1 Revenue Hits $1.65B, Beats Estimates Amid TAVR Share Gains and TMTT Commercial Uptake

Boston Scientific

Medical Device Manufacturer

Medtronic

Chronic Disease Medical Device and Therapy Developer

White Paper + Awards + Forum | The 2nd Global Cardiovascular Conference

Heart Future

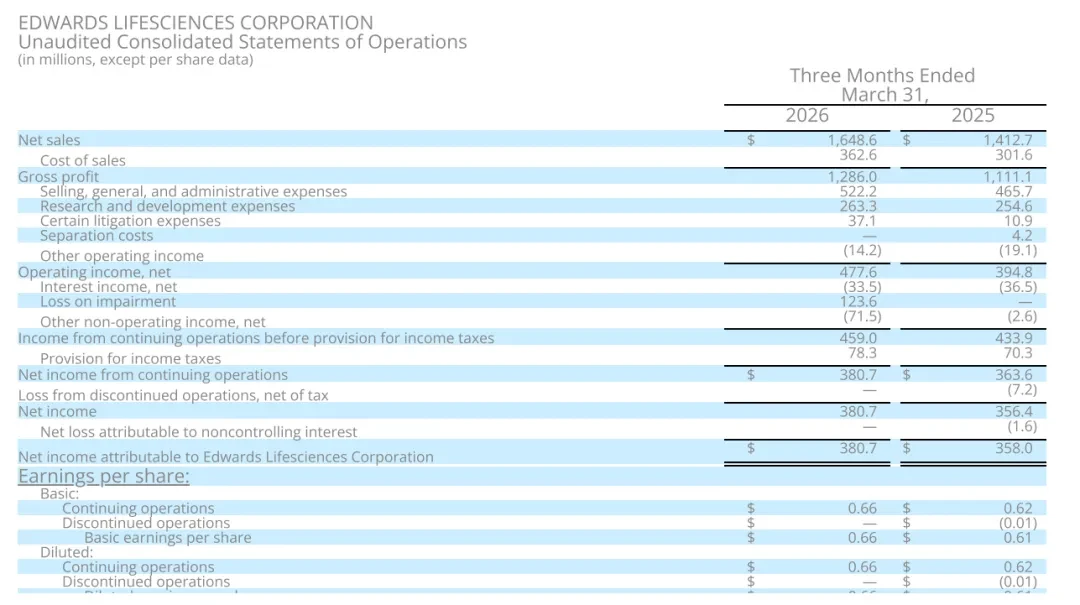

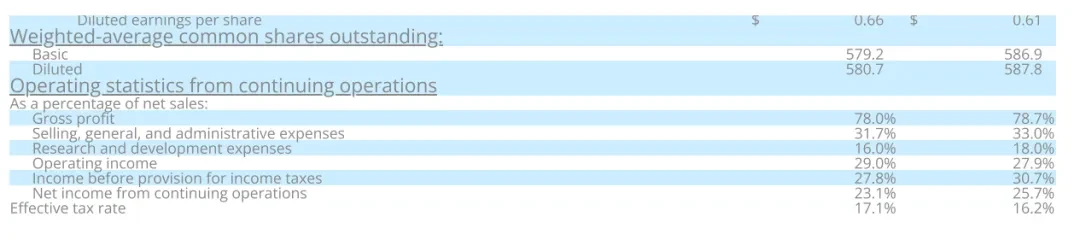

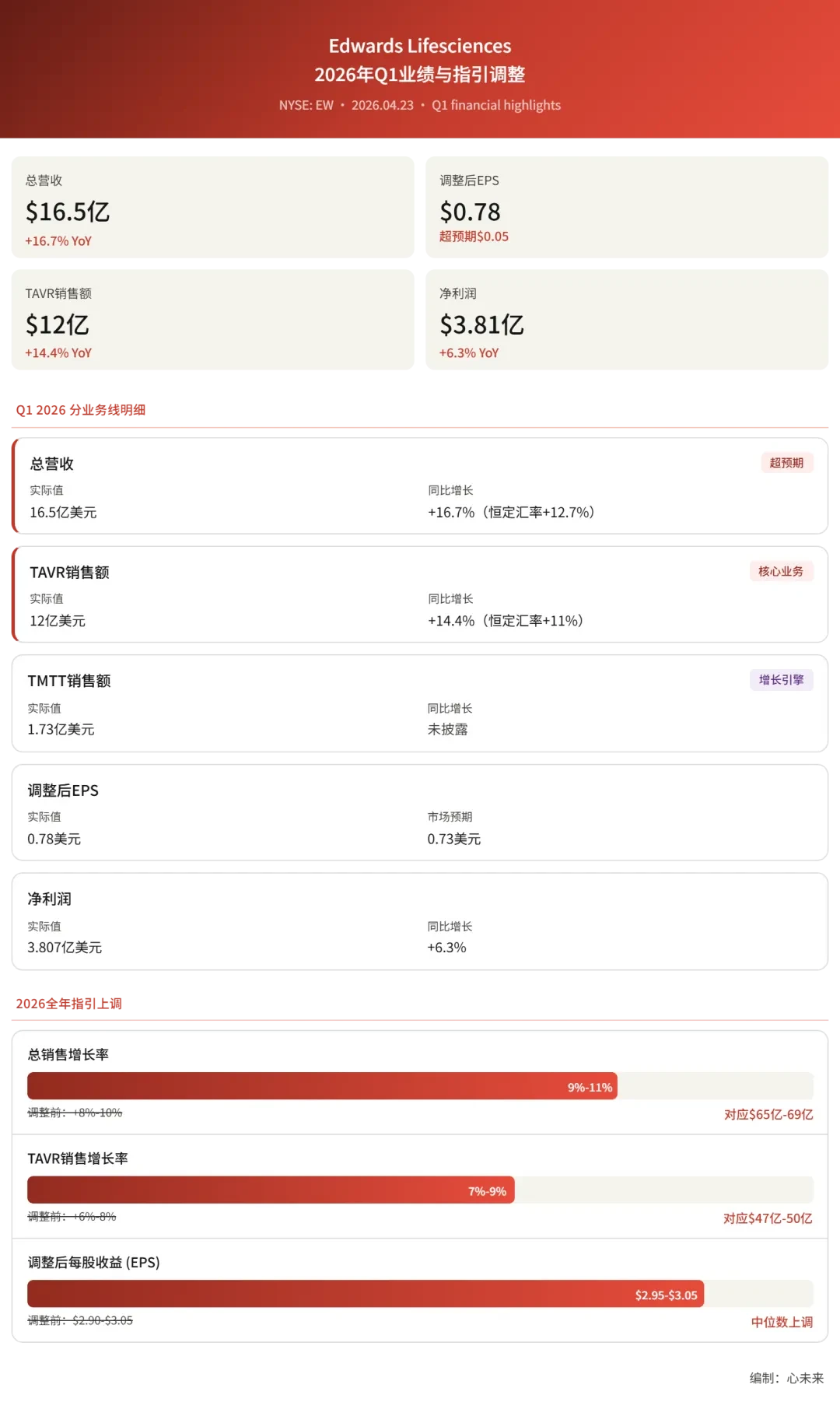

On April 23, 2026, Edwards Lifesciences (NYSE: EW) released its first-quarter 2026 financial report: revenue$1.65 billion(approximatelyRMB 11.3 billion), a year-on-year increase of 16.7% (12.7% growth at constant exchange rates), surpassing Wall Street's expected $1.6 billion; adjusted earnings per share of $0.78, higher than the market consensus expectation of $0.73. After-hours share price rose 4.2% to $83.05.

This is not only a "better-than-expected" quarterly report. More noteworthy are two structural signals:TAVR Business Accelerates Growth After Boston Scientific Exits European Market, andTMTT (Transcatheter Mitral and Tricuspid Valve Therapies) Business Enters a Growth Phase Following the Approval of Sapien M3Edwards simultaneously raised the full-year performance guidance for both TAVR and the entire company, which is uncommon in recent quarters.

# TAVR: $1.2 Billion Quarterly Revenue, Boston Scientific Exit Releases Market Share

Transcatheter Aortic Valve Replacement (TAVR) remains the revenue cornerstone for Edwards. In Q1, global TAVR sales reached $1.2 billion, a year-over-year increase of 14.4% (or 11% growth at constant currency). The company stated that the Sapien series experienced "healthy" growth in the U.S. market, with even faster growth rates in markets outside the U.S.

The key variable driving the acceleration of OUS is the change in the competitive landscape. In May 2025, Boston Scientific announced a global halt in sales of the Acurate neo2 and Acurate Prime TAVR systems and abandoned its FDA application. Previously, in the pivotal IDE trial results published at TCT 2024, Acurate neo2 failed to meet the primary endpoint of non-inferiority compared to Edwards Sapien 3 and Medtronic Evolut. Boston Scientific's Acurate product line in Europe contributed approximately $200 million in revenue for the full year 2024, with this market share now shifting towards Edwards and Medtronic.

Edwards raised its full-year TAVR sales growth guidance for 2026 from 6%-8% to 7%-9%, corresponding to a full-year TAVR sales forecast of $4.7 billion to $5 billion. According to data from industry research firms,Global TAVR Market Size Expected to Reach Approximately USD 7.1 Billion by 2026Edwards maintains a dominant position with approximately 55%-60% of the global market share.

Currently, the TAVR market has effectively formed a duopoly between Edwards and Medtronic. Medtronic's Evolut FX/PRO+ series unveiled the five-year data from the Evolut Low Risk Trial at the 2025 ACC, demonstrating sustained benefits in low-risk patients compared to surgical AVR, further solidifying its competitive position.The core competition in the TAVR sector has shifted from "who can get approval" to "who can continuously accumulate evidence on low-risk indications and durability data."

# TMTT: $173 Million, Sapien M3 Approval Opens New TMVR Increment

Q1 Transcatheter Mitral and Tricuspid Therapies Revenue $173 Million. Edwards stated that the global volume of mitral and tricuspid surgeries is experiencing "estimated double-digit" growth, with the company's growth rate surpassing the overall market.

The core driver of TMTT's growth comes from the combined volume increase of three products:

- PASCAL Precision:Transcatheter Mitral Valve Edge-to-Edge Repair (TEER) System, Directly Competing with Abbott's MitraClip G4

- EVOQUE:Transcatheter Tricuspid Valve Replacement System Approved by FDA in 2024

- Sapien M3:Transcatheter Mitral Valve Replacement (TMVR) System, FDA approved in December 2025, isThe First Approved Transseptal Approach TMVR Product。ENCIRCLE Key Trial (single-arm, 299 cases) one-year data shows that 95.7% of patients had MR≤0/1+, with significant improvements in symptoms and quality of life. The technology of Sapien M3 comes from Innovalve, which Edwards acquired for $300 million in 2024.

In the TMVR field, Edwards is not the only player.Abbott's Tendyne transapical TMVR system was approved by the FDA in 2025 for patients with mitral annular calcification (MAC)-related mitral valve dysfunction, forming a differentiated approach in competition with Sapien M3. Medtronic's Intrepid TMVR system is still in the clinical trial phase.

Edwards Raises Full-Year 2026 Company Total Sales Growth Guidance from 8%-10% to 9%-11%, Corresponding to Total Sales Expectation of $6.5B-$6.9B. Adjusted EPS Guidance Increased to $2.95-$3.05 (Previously $2.90-$3.05).

Edwards Lifesciences Q1 2026 Performance by Business Line and Guidance Update

# China Perspective: TAVR Penetration Still Low, Domestic TMTT in Early Stage

China's TAVR market has entered a stage of multi-product competition. In addition to Edwards Sapien 3 and Medtronic Evolut Pro (approved by NMPA in 2022), the main Chinese-produced participants include:Venus Medtech、MicroPort CardioFlow、Peijia MedicalAndNuPulse Medicaletc.

Key Characteristics of China's TAVR Market Differ from the Global Market. First, the proportion of bicuspid aortic valve (BAV) patients among those with aortic stenosis in China is significantly higher than in Europe and the U.S. (approximately 40%-50% vs. <5%), placing higher demands on valve design and deployment precision. Second, the reform of DRG/DIP payment methods has created cost-control pressures for the in-hospital use of high-value consumables; although TAVR has not yet been included in bulk procurement, its future remains uncertain. Third, the overall penetration rate of TAVR in China is still much lower than in mature markets such as Europe and the U.S.

In the TMTT field, the Chinese market is at an even earlier stage. Edwards’ PASCAL and EVOQUE have not yet received NMPA approval. In terms of domestically produced products,Dejin MedicalThe DragonFly Transcatheter Mitral Valve Repair System andYixin MedicalThe MitralFit TEER system, etc., are already advancing in clinical trials or early commercialization, but the overall market size is much smaller than TAVR. The TMVR direction in China is basically in the pre-clinical or early exploration stage.

Edwards' Q1 financial report did not separately disclose performance data for the China region or the Asia-Pacific region. From a global perspective, the Asia-Pacific region is one of the areas with the fastest-growing TAVR penetration rates, and both Edwards and Medtronic consider it a growth engine.

# Heart Future·Observation

The core highlight of Edwards' Q1 report card is not the "exceeding expectations" itself — as the absolute leader in the structural heart disease track, a slight exceedance in a single quarter is not surprising.What truly deserves attention is that the TAVR competitive landscape is shifting from a triopoly to a duopoly.。After Boston Scientific exits in 2025, it will leave behind not only approximately $200 million in European market share but, more importantly, reduce the overall intensity of competition in the field. Edwards and Medtronic's pricing power and bargaining ability will thus be implicitly strengthened.

The second variable worth tracking is the growth curve of TMTT.TAVR took nearly 20 years to progress from the first commercial implantation to achieving nearly $5 billion in annual sales. The clinical demand and market potential for TMTT may be no less than that of TAVR — given the significantly larger patient population with mitral regurgitation globally compared to aortic stenosis — but it involves higher technical complexity and greater anatomical diversity. Although Sapien M3 has been approved, its indications are limited to patients unsuitable for surgery or TEER, and the actual reachable population will take time to verify. Whether TMTT can become Edwards' second growth engine within the next 3-5 years will directly determine the market's recognition of its long-term valuation logic.

At the risk level, valuation pressure cannot be ignored.Edwards' current PE is about 45 times, and the market has already priced in expectations of sustained mid-to-high single-digit growth. If TAVR growth slows due to peak penetration rates, and TMTT's ramp-up speed falls short of expectations, there is considerable room for valuation correction.

What is the next game-changing variable after Boston Scientific exits TAVR? It could be the head-to-head competition results between Medtronic Evolut and Sapien in low-risk long-term data, or the commercial ramp-up speed of the TMVR track. The answers to these two questions will define the investment logic for the structural heart disease track over the next two years.

Full Disease Solution for Cardiovascular Devices

Structural Heart Disease → ▌Medtronic

Vascular Disease → ▌Huamaitech

Vascular Puncture and Closure → ▌Kegang Medical

Research and Development and Clinical Trial Support → ▌Medtronic