Fundable Early-stage Medical AI Projects Are All But Vanishing

When the revolutionary breakthroughs of artificial intelligence become an annual routine, the number of early-stage projects within the healthcare industry is visibly decreasing.

VBInsight data shows that in 2025, major companies such as AQ and Xiaohe Health will heavily enter the C-end health scenarios with general-purpose intelligent agents, driving both traffic and popularity to new heights.

But on the other side of the track: the number of early-stage projects has not increased but decreased, financing and entrepreneurial activities continue to shrink, and only mid-to-late stage projects at Round B or later are continuously securing funding, with concentration steadily increasing. Focusing on clinical AI projects, which were once the hottest, there are even fewer startups that have been able to secure financing in the past two years.

Why Has Healthcare AI in the Primary Market Gone from Booming to Bleak in Just a Decade?

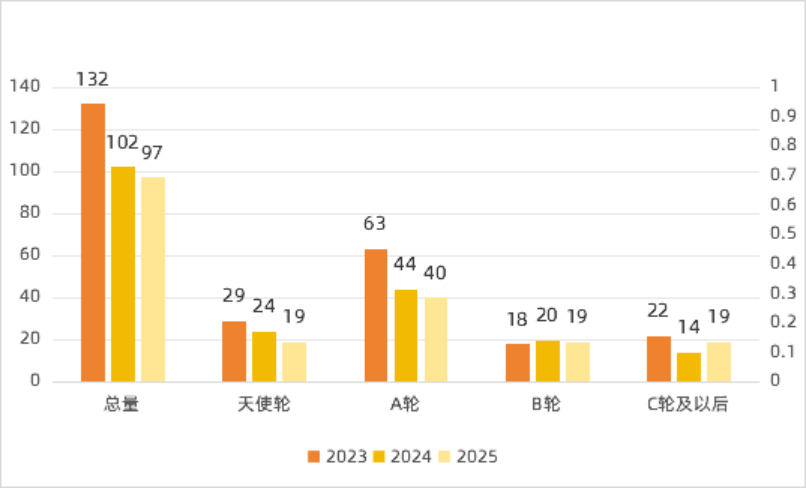

AI Investment Distribution by Rounds from 2023 to 2025 (Data Source: VBInsight)

During the epidemic, the director of the Department of Pathology at a tertiary hospital in Chengdu approached Cheng An (pseudonym), hoping to transform his accumulated experience in colorectal cancer within the pathology department into a digital system. The director possessed clinical and hospital data but lacked a technical team capable of engineering medical logic.

For Cheng An, the director's proposal was highly attractive. With no experience in the healthcare industry but an understanding that medical data and physician resources are the core barriers in medical AI, coupled with the company’s need to seek new growth points, he ultimately convinced the parent company to invest millions of yuan. A technical team of about 10 people was formed to initiate the development of an AI model for colorectal cancer under the guidance of the pathology department director.

With internet AI experience, the team launched the first version of the model in less than half a year, with an accuracy rate of about 85%. However, when trying to further optimize it, Cheng An discovered: Apart from this partner hospital, he could hardly obtain other external clinical data.。

Doctors hold markedly divided attitudes toward AI: Proactive practitioners have long partnered with established medical tech vendors and dismiss startups, while cautious ones prioritize data compliance and security and refuse to open up clinical data.

Fortunately, the flaws in the data were not an insurmountable problem. After accepting the reality, Cheng An's team began to adjust the algorithm itself, introducing few-shot learning to build a new model. With approximately 200 case samples, the new algorithm increased the detection rate to 97% and was able to handle multiple types of lesions such as colorectal cancer and hemorrhoids simultaneously, demonstrating preliminary clinical value.

In the internet industry, obtaining such data would already be considered as completing a phase of technical validation, allowing for an easy start to implementation attempts, while conveniently securing a few more rounds of financing. However, after squeezing into the circle of hospitals, Cheng An realized that he had greatly underestimated the barriers to entry in the medical industry.

Due to the lack of payers for medical AI, even with an initial product, it cannot be quickly monetized. Without cash flow, Cheng An urgently needs external funding to maintain the team's daily operations.

In 2023, Cheng An gained an opportunity to showcase AI capabilities at the Chongqing Jinfeng Laboratory in front of Academician Xiuwu Bian and his students. Ideally, by affiliating with the Chongqing Jinfeng Laboratory, the team could secure funding of 2 to 5 million yuan from the Chongqing government, alleviating their operational pressure.

As expected, Academician Xiuwu Bian affirmed the model's capabilities in the demonstration, but they ultimately failed to complete the affiliation as desired.

The threshold has become the biggest obstacle for teams to secure financing.

"There are both rigid and flexible thresholds here. For instance, to affiliate with a laboratory, the team's background is the first thing to consider. Regardless of the technical achievements you currently present, the team must be endorsed by senior experts in the medical industry — those well-recognized experts whose names resonate widely. Only then can you qualify to discuss the next steps of cooperation," Cheng An told VCBeat. "We didn’t have sufficient capital at that time."

After Chongqing failed to find a place to rely on, Cheng An approached the director of the pathology laboratory at Xiangya Hospital. "The director of Xiangya was very interested but made a series of requests: to convert the algorithm's architecture from Python to OpenCV or CUDA and to add recognition for 3-5 more diseases. If we meet these requirements, we can enter Xiangya’s pathology lab. A rough estimate suggests that achieving these goals will require at least 2 million yuan in additional costs."

During the period of seeking a laboratory affiliation, the Cheng'an team has also been looking for investors. Investment institutions generally recognize their technology but are unwilling to invest in medical AI companies that are too early-stage. They have also approached some private individuals for personal investment, but these bosses typically do not understand AI technology, making it impossible to verify and thus unlikely to lead to investment.

"Looking back now, I still feel a bit reluctant. We succeeded in technical verification, but in the next step, we spent more than half a year and didn't make any progress. In this semi-closed market, what we have in our hands are some ineffective rules."

The plight of Cheng An, a cross-border entrepreneur, is a microcosm of the current survival status of early-stage medical AI. Nowadays, there is a significant decrease in entrepreneurs without a medical background. Even projects led by those with a medical background are exiting the market. Leading platforms and major companies are squeezing the survival space of startups.

The medical imaging AI track is particularly representative. In the early and mid-stages, the entire market was fragmented, consisting of a variety of start-up companies. Entrepreneurs from different backgrounds developed their own medical imaging AI applications, forming a dispersed yet highly targeted market.

But as the recognition of imaging AI gradually increases, leading equipment manufacturers are starting to enter the market. Initially, they integrated the ecosystem through cooperation, but now they have developed native AI applications, aggregating past advancements into a comprehensive solution that better meets doctors' needs for imaging AI. Startups are gradually losing their voice.

For radiology departments, AI applications that are better compatible with hardware and information systems and deliver more accurate and comprehensive lesion detection naturally bring a superior user experience. However, for independent medical imaging AI enterprises, the in-depth bundling of software and hardware continues to squeeze their living space, reducing their products from standalone offerings to bundled accessories of medical devices.

Not yet achieving stable commercialization, it has already lost its independent paid value.

Thus, when the older generation of enterprises has gradually begun to transition to other tracks, the barren land naturally struggles to nurture new life.

The AI track in medical informatization faces another kind of dilemma. In this track, the majority of hospitals are willing to pay for AI that comes from pre-existing systems (such as HIS, PACS, EMR, etc.).

Compared to imaging AI, the advantage of this type of track lies in the fact that hospitals have already developed a habit of paying, and there are existing business models that can be referenced without the need for additional cultivation.

But precisely because of this, there are too many competitors gathered here, including leading medical IT companies, later-stage startups, as well as the three major telecom operators crossing over and medical device companies integrating information flow.

When new trends like DeepSeek and OpenClaw emerge, industry giants are able to release solutions promptly and integrate them into systems quickly. By the time startups have developed their products and successfully established relationships with hospitals, the industry landscape has long changed from what it was when they first entered.

Although a stable ecological environment is eroding the soil for startups to sprout, many investors are still exploring emerging AI projects. However, compared to the past, their investment logic has changed, with higher requirements and a greater focus on later-stage investments.

"When large models like GPT and Claude emerged, we realized that AI agent technology had achieved a qualitative breakthrough, enabling startups and large companies to once again be on an equal footing in technology development. Theoretically, AI startups are highly worthy of investment," said Li Yingjie, Executive Director of INNO Angel Fund.

"But precisely because of this, we now don't focus too much on the pros and cons of AI technology. Instead, we look at who their investors are, what clinical pain points they have addressed, and whether these pain points are truly essential needs for doctors."

An increased focus on the payer essentially imposes additional requirements on the business model of medical AI.

In the wave of medical AI with CV and NLP as core technologies, there are very few companies that can make it to the secondary market. Their business models often focus on selling servers or charging per use, and in many cases, they do not truly address the needs of hospitals.

As hospitals deepen their engagement with AI, they are no longer focused on the form of business models but instead concentrate on AI that can truly provide additional revenue. They are also willing to adopt a “pay-for-performance” model.

Therefore, the AI companies that investment institutions are still willing to invest in now must be those that can build up their monetization capabilities in the short term.

From the current development status of the medical AI industry, there are not many companies adopting "pay-per-effect" as a business model. Among existing cases, automated writing of electronic medical records supported by large models is expected to become the first scenario for scaled pay-per-effect.

Leveraging the advantages in automated writing of electronic medical records, companies like FusionAI, Trizen Medical, and SenseTime Healthcare have gone against market trends by 2025. Among them, SenseTime Healthcare is unique due to the backing of SenseTime Technology, while FusionAI and Trizen Medica have genuinely achieved commercial scalability. The latter secured two rounds of financing within a year.

In the growth path of doctors, medical record writing is a fundamental task that runs throughout their career, but it is also repetitive labor that consumes a great deal of energy without directly enhancing clinical skills. Statistics show that nearly half of a doctor's working hours are spent on various types of documentation, which over time can easily lead to professional burnout.

At the same time, excessive documentation pressure also leads to a decline in the quality of medical records, with frequent occurrences of issues like copy-pasting and non-standard content, which in turn brings risks such as health insurance fee deductions, medical disputes, and litigation compensation. This not only troubles frontline doctors but also puts pressure on hospital administrators. Using AI to assist doctors in documentation can not only reduce their workload but also improve the quality of electronic medical records and lower the operational costs of hospitals.

Of course, there are many scenarios similar to the automation of electronic medical records. Whether it's traditional AI or current agents, the key lies in whether enterprises can find the right entry point to reduce costs and increase efficiency for hospitals, and transform the value created for hospitals into their own revenue.

Overall, the era of intelligent agents brings technological equity, but innovation in medical AI is still bottlenecked by "data." The bottom line of data security cannot be compromised, and how to unleash the value of data under the premise of compliance has become the key to breaking through industry barriers.

Indeed, ensuring the security of health data is crucial, but we may also need to find a middle ground to fully leverage the value of data while safeguarding its security.

Under the promotion of the National Data Bureau, mechanisms such as data trading markets and trusted data spaces are gradually being implemented. Some hospitals have already reached data trading agreements with startups, allowing health data to be reused under compliant conditions.

When start-ups can also obtain health data through legal channels, we believe that entrepreneurs who discover real medical needs will always return to the medical AI track, accelerating the advent of a truly intelligent healthcare era.