Elimination competition begins in China's surgical robot sector: Star companies bankrupt while market defies trends to grow

Wire Science

Surgical Robot R&D and Production Company

Longwell Medical

Developer and Manufacturer of Joint Replacement Surgical Robots

The bankruptcy liquidation of two star companies signals the start of an elimination competition in China's surgical robot sector.

In June 2025, Wire Science, a vascular interventional robotics company, entered the bankruptcy auction phase, with the starting bid for its 17 patents, 72 trademarks, and all fixed assets priced at only approximately 1.29 million RMB.

In January 2026, the Shanghai Pudong Court officially accepted the bankruptcy liquidation case of Longwell Medical, an orthopedic robotics company. Its TRex-RS system had achieved multiple technological breakthroughs and obtained its registration certificate in September 2024 but failed to achieve commercial success, ultimately collapsing just one and a half years after the product's approval.

Surgical robots have the attributes of medical devices, and their value lies in long-term accumulation rather than short-term speculation. The fall of two star companies indicates that this once red-hot financing track has entered the phase of industry consolidation.

In contrast, the overall market for surgical robots in China has maintained a high growth trend. In 2025, the sales volume of domestic surgical robots (including overseas sales) increased nearly twofold year-on-year; within the Chinese market alone, annual sales reached 456 units, marking a 17% year-on-year increase, with a market size of 3.13 billion RMB, reflecting a slight year-on-year increase of 1%.

On one side, star companies are going bankrupt and the industry is starting to consolidate; on the other side, the market size continues to expand with growth potential becoming more prominent. Why does such a contradiction exist in the surgical robot market? After the elimination competition begins, how will the market landscape evolve? In the surgical robot market, do small and medium-sized enterprises and newly-listed surgical robots still have opportunities to break through?

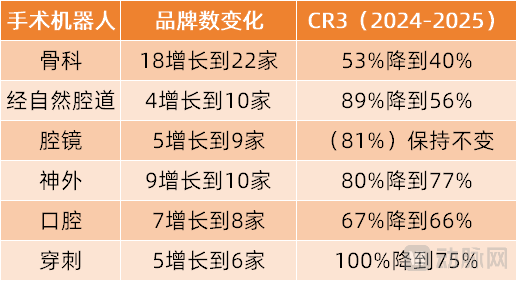

In 2025, approximately 52 new surgical robots were approved in China, and the number of commercial brands increased from 44 to 54. The supply side became more crowded, and market competition intensified.

Among them, in the sub-sectors of surgical robotics such as orthopedics, natural orifice, and laparoscopic surgery, the number of commercialized brands has increased significantly. For example, natural orifice surgical robots grew from 4 in 2024 to 10 in 2025; laparoscopic surgical robots increased from 5 to 9; and orthopedic surgical robots, the most competitive segment, grew from 18 to 22.

(Brand Numbers and CR3 Changes in the Surgical Robot Segment, Data Source: Shuojian Surgical Robot)

Although the number of commercialized brands is increasing, market changes in various subfields differ: In the orthopedics and natural orifice fields, a "even a good tiger can't withstand a pack of wolves" trend is emerging. The combined market share of the top three players (CR3) in these markets as a proportion of the overall market is declining. Orthopedics CR3 decreased from 53% in 2024 to 40% in 2025, while natural orifice CR3 dropped from 89% to 56%.

In the field of endoscopic surgical robots, small and medium-sized enterprises or new entrants have not affected the market share of leading companies, with their CR3 remaining unchanged at 81%. This indicates that in the field of endoscopic surgical robots, leading companies still maintain advantages in brand, product, channel, and technological iteration. New entrants or small and medium-sized enterprises that want to break through must achieve genuine innovation to overcome technical barriers and introduce differentiated products that better meet clinical needs to solve commercialization challenges.

In addition, in fields such as neurosurgery, oral/dental, and puncture surgical robotics, the number of brands has seen little change, while sales of surgical robots in these fields have all maintained growth. Among them, neurosurgical robot sales reached approximately 129 units in 2025, making it the third largest sub-segment in the surgical robotics field, currently in an accelerated volume ramp-up phase. Oral/dental and puncture surgical robots have sales in the range of tens of units, still in the early stages of commercialization but poised for accelerated penetration. Meanwhile, surgical robots for pan-vascular procedures and hair transplantation are still in the validation and promotion phase.

As the number of entrants increases and the number of approved products grows, market competition in the surgical robotics field is becoming increasingly fierce. For instance, in current surgical robot bidding processes, after the announcement of winning bids, many projects often face complaints from competitors, leading to the restart of the bidding process. It usually takes three or four rounds of negotiation to finalize the winning bidder. In some bidding projects, bids are canceled due to an insufficient number of suppliers and then restarted later.

Zhang Tai from Loyal Valley Capital stated: "Restricted by allocation permits and the congestion in the multi-port track, this is the most intense competition we have ever witnessed. However, it also represents the fastest globalization we've ever seen: innovation-driven single-port coverage in developed Western European countries, and cost-effective multi-port coverage in emerging markets have both achieved commendable results."

In the past, the competition in the surgical robot market was relatively mild. For instance, if one surgical robot company decided to participate in an industry exhibition or academic conference, other competitors would most likely attend the same event to seize exposure opportunities and explore potential customers.

The change in competitive means includes issues such as the tendering party customizing parameters to pre-determine the winning enterprise, as well as intensified commercial competition and rivals stepping up complaints. It is expected that with the bidding market becoming increasingly fair, just, and transparent, competition in the surgical robotics market will continue to focus on product quality. Support from local governments and channels will remain rare cases.

Zhang Taihao from Loyal Valley Capital believes: "The root of this intense competition lies in excessive capital investment. Investors are overly optimistic about the scale of the track, believing that latecomers still have opportunities to break through, thus injecting too much funding into the track. Additionally, due to the large-scale imitation of Intuitive Surgical's technical route, the homogeneity of technology is bound to lead to talent mobility, resulting in technology spillover."

Under fierce competition, the market has begun to enter the elimination phase. Surgical robot companies that have not secured commercial orders must quickly achieve commercial installations to raise sufficient funding for future development.

Chen Yuemeng, founder of Meio CardiNav Medical, stated: "Survival of the fittest is ultimately a positive development for the industry as a whole. For hospitals, they can obtain higher-quality products at a lower cost by setting better parameters through the bidding process. For companies, if their products lack innovation and fail to meet clinical needs, they will face the risk of elimination. This will drive companies to enhance innovation and develop products based on actual clinical requirements. On the other hand, the approval cycle for surgical robots is relatively long. If companies cannot quickly profit from approved products, they will face significant financial and revenue pressures."

Overall, the fierce competition in the market is beneficial for companies with strong product innovation capabilities and a rich product portfolio to gain more market share; for companies with a single product and insufficient innovation capabilities, they may face crises.

In the surgical robotics field, leading companies continue to maintain a strong position.

In the bidding market, leading companies have a significantly higher win rate, while small and medium-sized enterprises or new entrants have a relatively lower win rate. For example, in sub-sectors such as natural orifice and oral/dental surgical robots, the CR3 (the combined market share of the top three players) stands at 56% and 66%, respectively. In fields such as endoscopic, neurosurgical, and puncture surgical robots, the CR3 exceeds 70%, reaching 81%, 77%, and 75%, respectively. This means that brands outside the top three can only compete for the remaining 30% to 40% of the market, and most of these brands are small and medium-sized enterprises or new entrants.

This is because leading companies have transformed their advantages in capital, teams, and technology into a first-mover advantage in commercialization, and through this first-mover advantage, they have accumulated product maturity and cost advantages.

Chen Yuemeng, founder of Meio CardiNav Medical, stated: "First, the cost advantage of leading enterprises is significant. Their early investments in molds, production, and R&D costs have been gradually amortized through scaled production, resulting in relatively lower unit costs. This gives them more bargaining power in price wars and enables them to offer more competitive bids in centralized procurement and provincial tenders."

Secondly, leading companies often have a presence across multiple sub-segments, with well-established product systems and rich product portfolios, enabling them to meet the diverse clinical needs of hospitals and more easily align with various parameter requirements in bidding processes. In contrast, small and medium-sized enterprises typically focus on a single product and struggle to address comprehensive needs.

Third, the cooperation between leading enterprises and distributors is stable. Based on the first-mover advantage, leading enterprises have long-term cooperation with distributors, high stickiness, and stronger financial advantages, which enable them to provide better payment terms and profit margins for distributors. Therefore, they are more likely to receive active recommendations from distributors, further increasing the probability of winning bids.

Finally, the brands and stability of leading enterprises are more trusted by hospitals. When choosing surgical robots, hospitals not only focus on price but also value after-sales support and brand reputation. Surgical robots are expected to be used for 5-8 years after procurement, which requires the winning bidder to provide corresponding after-sales and operation maintenance services during that period. The market position of leading enterprises indicates higher quality assurance and a more reliable after-sales service system, reducing the procurement risks for hospitals. In this context, hospitals are more inclined to choose products from leading brands."

Zhang Taihao from Loyal Valley Capital added, "The products of leading companies have undergone multiple iterations over the years, continuously improved based on doctors' feedback, and thus have advantages in stability and performance. Moreover, for hospitals, in the past when there were no domestically produced surgical robots, many hospitals and clinical experts were willing to accompany domestic products through trial and error and improvements. However, now that there are already good domestically produced products, it might be difficult for hospitals to accompany a new brand through the same process of trial and error and improvement again."

Overall, hospitals' preference for products from leading companies further squeezes the survival space of small and medium-sized enterprises and new entrants, exacerbating the differentiation and competitive imbalance in niche markets.

Zhang Taihao judged: The surgical robot track will continue to be "overcrowded" for two to three years, and will eventually inevitably face a large-scale shakeout. "Just like in the medical imaging equipment field, only two or three companies may survive in good condition. Enterprises need to find their own positioning."

Regarding market changes in two to three years, Zhang Taihao provided a clear analysis from the perspective of corporate cash burn: new entrants need at least tens of millions in annual market expenses, plus continuous R&D investment, resulting in an annual cash burn of about 150 million RMB. Meanwhile, most surgical robotics companies have only raised 100 to 300 million RMB in financing, which is insufficient to sustain long-term expenditures. Therefore, the market consolidation will likely occur within two to three years.

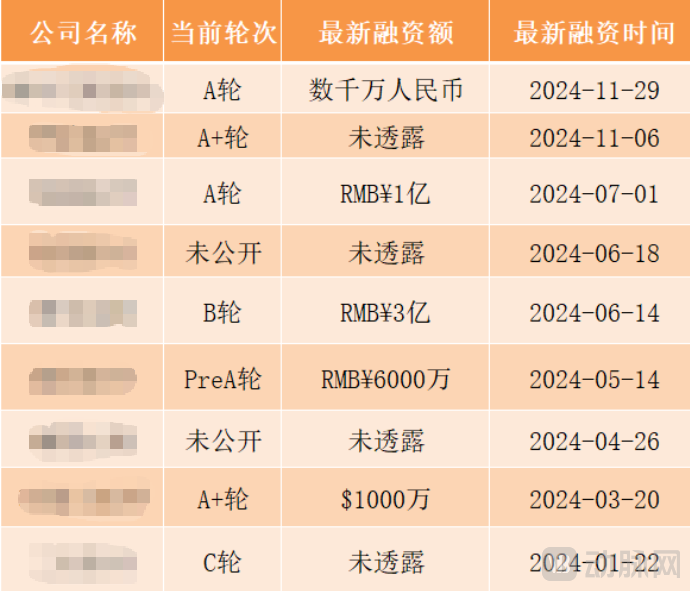

(Financing Situation in the Surgical Robotics Field in 2024)

Chen Yuemeng provided supporting evidence from the perspective of health economics: In January 2026, the National Healthcare Security Administration officially released the "Guidelines for the Establishment of Medical Service Price Items for Surgical and Therapeutic Auxiliary Operations (Trial)." This provides a real health economics evaluation model for surgical robots, allowing hospitals to charge fees based on the specific clinical value of the surgical robots. Through this model, it can be clearly determined which products can be charged and which tier of fees they fall under. This will accelerate the market shakeout of surgical robots. It is expected that by the end of 2027, the surgical robot market will bottom out, with products of lesser clinical value and higher homogeneity gradually being phased out.

Moreover, after the leading companies go public, the difficulty for other companies to go public will increase significantly. Eventually, they will either be acquired or eliminated by the market. Zhang Taihao lamented, "The players who should enter the game have already entered. It will be very difficult for the companies that come later to break through."

Difficult, does not mean "impossible."

In the new energy vehicle market, Lei Jun said: "The world will not always be dominated by the strong; latecomers always have a chance."

This statement also applies to the surgical robotics field. Just as Intuitive Surgical's laparoscopic robot Da Vinci dominated the market for 20 years, domestic brands like MedBot®, Surgerii Robotics, and Edge Medical have emerged. Additionally, a group of leading companies in niche markets have appeared in specialized fields such as orthopedic, neurosurgical, and puncture surgical robots.

Surgical robots with differentiated innovation will definitely have the opportunity to grow into “leaders”. The key is that these enterprises need to seize the "opportunity" with "innovation".

For example, Meio CardiNav Medical innovates in terms of indications and application scenarios. Instead of choosing fields with many players such as orthopedics, natural orifice surgical robots, or neurosurgical robots, it has opted for vascular interventional surgical robots. Within the realm of vascular interventional surgical robots, it has chosen the cardiac electrophysiology (AF ablation) field, an area where other companies have not yet established a presence.

In addition to track differentiation, products in the same track can also achieve breakthroughs through differentiated innovation. In the field of endoscopic surgical robots, Ronovo Surgical has independently developed China's first modular split-design surgical robot. Additionally, Surgerii Robotics has innovated through a new technical approach, creating a single-port endoscopic surgical robot with fully snake-like robotic arms, enhancing the range of motion, force load capacity, and flexibility. This not only addresses various pain points of traditional rigid multi-port and single-port endoscopic surgical robots but also positions the company as another leading enterprise in the field of endoscopic surgical robotics.

Driven by innovation, Meio CardiNav Medical's Tixiang surgical robot has been clinically applied in 10 hospitals, including Beijing Anzhen Hospital and People's Hospital of Chongqing Liangjiang New Area, within six months of its approval. Ronovo Surgical's surgical robot has completed one commercial installation and successfully performed numerous high-difficulty surgeries, such as bronchial sleeve resection. Surgerii's single-port surgical robot has performed over 3,000 surgeries in China…

Overall, in the surgical robotics market, although leading companies have comprehensive advantages in terms of funding, channels, product iteration, and market share, newcomers still have the opportunity to break through by means of technological innovation, indication innovation, and procedural innovation. This allows them to achieve commercial implementation and gain recognition from clinical experts and the market.

Although the industry has experienced some short-term fluctuations, the long-term growth logic of the surgical robotics market has remained unchanged.

First, the penetration rate of surgical robots in China is still at a relatively low level, but the clinical value of surgical robots has been validated, offering significant benefits to both medical staff/patients and hospitals; market demand is clear and strong.

Second, the increase in competitors in the surgical robot market has led to a decrease in product average prices, which is expected to activate a broader market. For instance, hospitals with originally limited budgets may consider purchasing surgical robots after the price reduction.

Third, the global market is a new growth engine. Chinese-produced surgical robots represented by companies such as MedBot, Edge Medical and Surgerii Robotics, have successfully explored overseas markets, with significant increases in overseas revenue. For instance, MedBot's new order sales revenue from overseas markets in 2026 increased by over 400% year-on-year; Edge Medical's overseas end-user income accounted for more than 50% of total revenue in 2025. This provides an exemplary model for Chinese surgical robot companies seeking to expand abroad.

Fourth, the state has introduced multiple policies to promote the implementation of surgical robots, such as guidelines for medical service pricing projects for surgical robots, DRG-excluded payment policies, and even the inclusion of surgical robot projects in medical insurance in some regions.

Under the influence of the aforementioned four major factors, the surgical robot market is still expected to maintain a high growth rate.

However, the number of configuration certificates might be a limitation for the accelerated application of endoscopic surgical robots. As of December 30, 2025, out of the 559 configuration certificates planned during the 14th Five-Year Plan, 463 have been issued, leaving 96 remaining. Currently, many hospitals have the intention and need to purchase but are unable to do so due to the lack of configuration certificates.

The market is still looking forward to and paying attention to the configuration arrangements for surgical robots in the 15th Five-Year Plan.