Cofoe Medical rings the bell on Hong Kong stock exchange: home medical device's cyclical rebound and A+H journey

Cofoe

Intelligent Medical Device R&D, Production, and Sales Company

Cofoe Medical Technology Co., Ltd. (A-share code: 301087.SZ, hereinafter referred to as "Cofoe Medical") was listed on the Hong Kong Stock Exchange on May 6, 2026. The company has been listed on the Shenzhen Stock Exchange's ChiNext Board since 2021, and its H-share issuance in Hong Kong in 2026 will make it an A+H dual-listed company.

According to data disclosed in its listing documents, the company's revenue from 2023 to 2025 was RMB 2.854 billion, RMB 2.983 billion, and RMB 3.387 billion, respectively. Its gross margin increased from 41.1% to 51.7% over the same period, while annual profit rose from RMB 253 million to RMB 370 million, representing a cumulative net profit increase of 46% over three years. Against the backdrop of a post-pandemic cyclical adjustment in China's home medical device industry—where Yuwell saw its 2025 net profit decline by 17.94% year-on-year, Sinocare's net profit attributable to parent company shareholders fell by 71.61%, and BMC Medical's 2024 net profit dropped by 47.74%—Cofoe is one of the few home medical device companies that maintained dual growth in both revenue and profit while achieving a sustained increase in gross margin.

Why would a profitable company that has been stably listed on the A-share market for five years choose to make a move for the Hong Kong stock market at this moment? How did its five major product matrices achieve an increase in gross margin amid a generally downward industry environment? Where does Cofoe stand among comparable companies such as Yuwell, Sinocare, BMC Medical, and Omron? What will be the main uses of the raised funds?

This article systematically reviews six dimensions—industry landscape, product matrix, financial fundamentals, listing rationale, competitive positioning, risks, and observations—based on Cofoe Medical's Hong Kong IPO filing documents and publicly available data of comparable companies.

What is the home medical device industry experiencing in 2025?

China's home medical device industry has followed a curve of "rising first, then falling" over the past three years. During the pandemic period from 2020 to 2022, categories such as respiratory support, health monitoring, and disinfection and nursing experienced a rare surge in demand—sales of products like pulse oximeters, blood pressure monitors, nebulizers, and electronic thermometers all grew severalfold, while the performance and valuations of related listed companies simultaneously hit record highs. However, after entering 2024, the industry as a whole entered a post-pandemic digestion period, as pandemic-driven demand subsided, inventory pressures were released, consumer willingness weakened, and end-market prices came under pressure.

Looking at the 2024 to 2025 performance of major comparable companies, the industry's cyclical downturn is very evident. Yuwell achieved operating revenue of RMB 7.955 billion in 2025 (up 5.14% year-on-year), but net profit attributable to parent company shareholders was RMB 1.482 billion, down 17.94% year-on-year, while recurring net profit declined 16.10% year-on-year. In the first quarter of 2026, Yuwell's revenue declined 2.69% year-on-year, with net profit attributable to parent company shareholders down 31.44% year-on-year, reflecting sustained earnings pressure. Sinocare reported operating revenue of RMB 4.659 billion in 2025 (up 4.87% year-on-year), but net profit attributable to parent company shareholders was only RMB 93 million, a decline of 71.61% year-on-year. BMC Medical reported operating revenue of RMB 843 million in 2024 (down 24.85% year-on-year), with net profit attributable to parent company shareholders of RMB 155 million, a decline of 47.74% year-on-year. Even Omron Healthcare, the global leader in home blood pressure monitors, saw its sales decline 2.6% and operating profit decline 5.3% in fiscal year 2024.

● Two Types of Opportunities Amid the Industry Downturn

While the industry enters a period of adjustment, it is also releasing new structural opportunities for some companies. The first opportunity lies in the reshaping of product categories—demand for categories that were pulled forward during the pandemic (such as respiratory support and disinfection and nursing) is returning to normal levels, while demand for categories driven by aging (rehabilitation aids), chronic disease management (health monitoring), and consumption upgrades (traditional Chinese medicine physiotherapy) continues to rise. The second opportunity lies in channel and supply chain integration—experience with e-commerce platforms, pricing power of owned brands, and customer stickiness from customized production are becoming new sources of competitive moats.

Cofoe Medical's differentiated positioning sits precisely at the intersection of these two types of opportunities. On one hand, the company maintains a high degree of product matrix coverage across its three major categories—rehabilitation aids, medical nursing, and health monitoring—avoiding over-reliance on any single category (such as respiratory support). On the other hand, the company's sales channels are primarily e-commerce self-operation, supplemented by a distributor network and customized production business, with economies of scale and pricing power continuing to expand as revenue grows. This combination has enabled Cofoe to achieve revenue growth of 13.5%, a gross margin increase of 1.1 percentage points, and net profit growth of 18.6% amid a broadly downward industry environment.

5 Major Product Matrices: How Did They Generate 3.387 Billion RMB in Revenue?

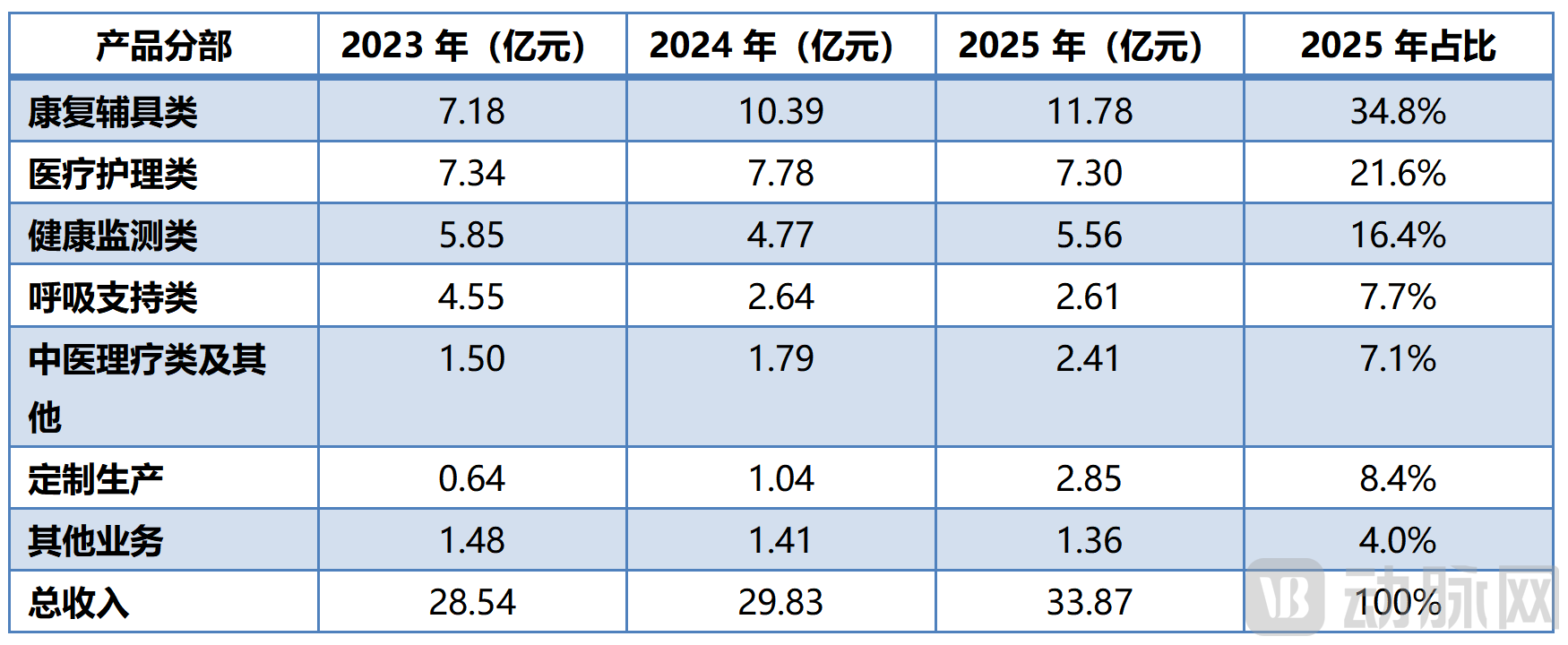

Cofoe Medical's business structure consists of three segments: "sale of medical health products," "customized production," and "other businesses." Among these, the sale of medical health products contributed RMB 2.966 billion in revenue in 2025, accounting for 87.6% of total revenue, and is divided into five major categories: rehabilitation aids, medical nursing, health monitoring, respiratory support, and traditional Chinese medicine physiotherapy and others.

Figure 1: Cofoe Medical Technology Co., Ltd. Revenue Structure by Product from 2023 to 2025 (Data Source: Cofoe Medical Technology Co., Ltd. PHIP)

● Rehabilitation Aids: A Core Growth Engine from 25% to 35%

The rehabilitation aids category has been Cofoe's most important growth engine over the past three years, with revenue increasing from RMB 718 million in 2023 to RMB 1.178 billion in 2025, representing a cumulative growth of 64% over three years. Its share of total revenue rose from 25.2% to 34.8%. This category includes products such as hearing aids, wheelchairs, nursing beds, and rehabilitation training equipment, with downstream demand driven by China's aging trend. According to data from the National Bureau of Statistics, China's population aged 60 and above reached 310 million by the end of 2024, accounting for 22.0% of the total population. Among all home medical device subcategories, rehabilitation aids have the smallest demand elasticity affected by the pandemic cycle, making them a relatively stable "long slope with thick snow" track.

Even more noteworthy is the gross margin trend of the rehabilitation aids category: it increased from 48.4% in 2023 to 62.1% in 2024, and further to 63.2% in 2025, representing a cumulative increase of approximately 15 percentage points over three years. This gross margin level approaches the industry average for high-end medical equipment, reflecting Cofoe's dual breakthroughs in own-brand pricing power and production scale efficiency.

● Respiratory Support: Pandemic Dividend Fades, Contracting from 16% to 8%

The respiratory support category (including nebulizers, oxygen concentrators, ventilator accessories, etc.) was the largest beneficiary of pandemic-driven demand, still contributing RMB 455 million in revenue in 2023, accounting for 15.9% of total revenue. However, as the pandemic cycle ended, revenue from this category rapidly declined to RMB 264 million in 2024 (down 42%) and further to RMB 261 million in 2025, with its share shrinking from 15.9% to 7.7%. This change is highly consistent with the trend of comparable company BMC Medical, whose revenue declined 24.85% in 2024, reflecting the overall industry adjustment period for the respiratory support category.

● Customized Production: A Second Curve from RMB 64 Million to RMB 285 Million

Customized production (i.e., OEM/ODM business) grew from RMB 64 million in 2023 to RMB 285 million in 2025, increasing 4.5 times over three years, making it Cofoe's fastest-growing business segment. Most customers of this business are large medical device distributors, brand owners, or hospital groups, with higher bargaining power but stronger customer stickiness. The rise of customized production reflects that Cofoe's R&D and manufacturing capabilities have begun to gain substantial recognition from B-end industry clients, marking the company's evolution from an "own-brand retailer" to a "full-chain medical device service provider."

Why Did the Gross Profit Margin Increase from 41.1% to 51.7%?

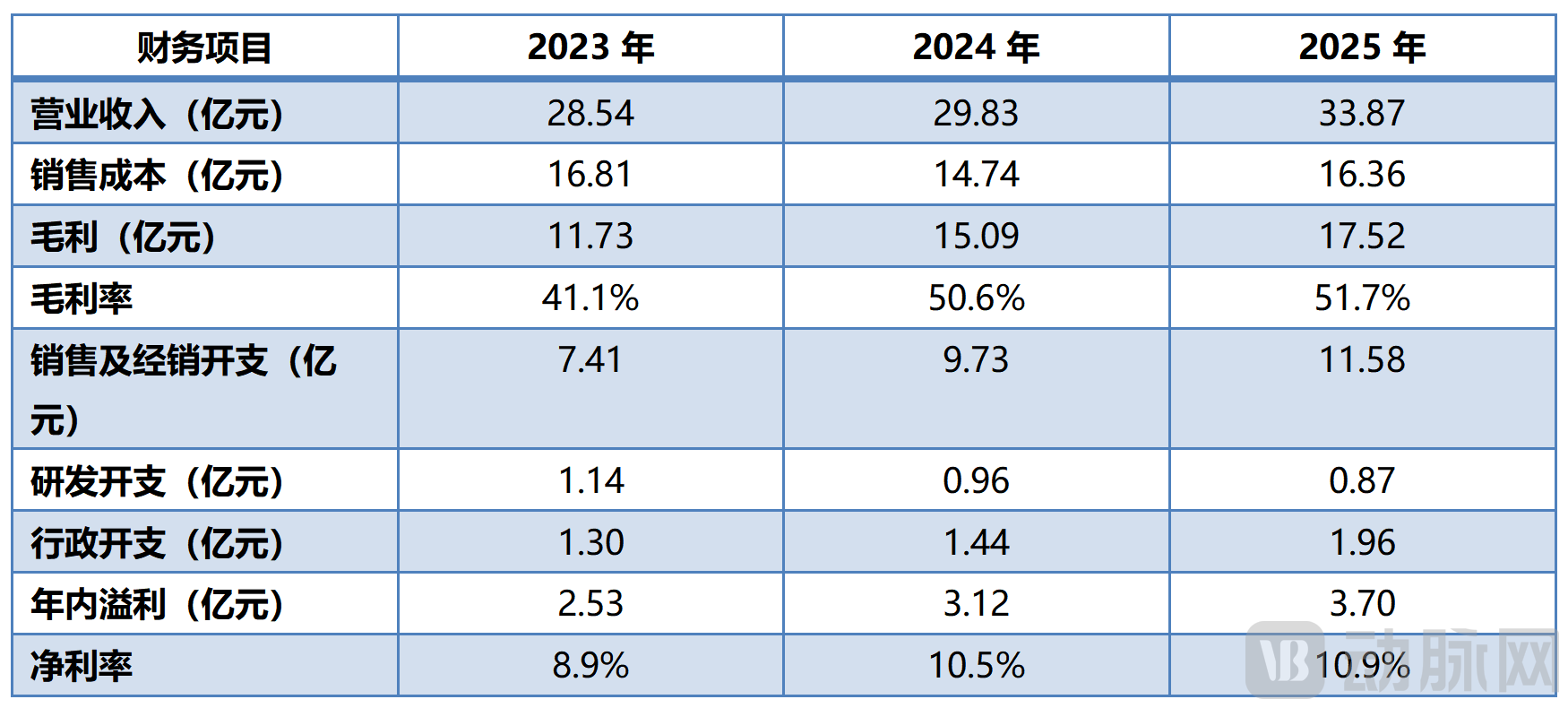

Cofoe Medical's financial performance from 2023 to 2025 stands out as an anomaly in China's home medical device industry. Against the backdrop of a general industry downturn, with competitors experiencing gross margin compression and net profit declines, Cofoe not only maintained revenue growth but also achieved sustained improvements in both gross margin and net profit.

Figure 2: Selected Items from Cofoe Medical Technology Co., Ltd.'s Consolidated Income Statement for 2023 to 2025 (Data Source: Cofoe Medical Technology Co., Ltd. HKEX PHIP)

Based on an analysis of the listing documents, the core drivers of Cofoe Medical's gross margin increase from 41.1% to 51.7% can be summarized into the following four points:

First, optimization of product mix. The rehabilitation aids category (with a gross margin of 63.2%) increased its share of total revenue from 25.2% to 34.8%, becoming the largest revenue source and directly lifting the overall gross margin. Over the same period, the medical nursing category (gross margin of 52.6%) maintained a share of approximately 21.6%, while the health monitoring category also maintained a gross margin of around 50%. Together, these three high-margin categories contributed over 70% of total revenue, driving a structural increase in the overall gross margin.

Second, an increase in the proportion of own-brand products. Cofoe's home medical device products are predominantly sold under its own "Cofoe" brand. Leveraging years of e-commerce operational experience and brand recognition, its own-brand products command strong pricing power in end-market pricing, avoiding the gross margin pressure typically faced by pure channel distributors or agency models.

Third, the release of production scale effects. The company's operating revenue in 2025 increased by 18.7% compared to 2023, yet its cost of sales only decreased slightly from RMB 1.681 billion to RMB 1.636 billion (with an actual decline occurring in 2024), indicating a significant dilution effect of fixed costs per unit of product.

Fourth, a relative easing of pricing competition pressure in the industry. The numerous small manufacturers that flooded into the market during the pandemic gradually exited as demand subsided after 2024. This reduced pricing competition pressure among the remaining leading players, creating a relatively favorable environment for Cofoe, whose own-brand products dominate its business.

It is worth noting that Cofoe's selling and distribution expenses increased from RMB 741 million to RMB 1.158 billion over the three years, a growth of 56%, far exceeding its revenue growth rate. The selling expense ratio increased from 26.0% to 34.2%, reflecting the company's continued increases in brand promotion, e-commerce advertising, and channel expansion. In contrast, R&D expenses decreased from RMB 114 million to RMB 87 million, with the R&D expense ratio declining from 4.0% to 2.6%. While this trend is consistent with the company's current strategic focus on channel expansion and brand strengthening, it also represents a potential risk point that warrants continued observation in the future.

As an Already Listed Company on the A-share Market, Why Aim for a Hong Kong Stock Listing?

Cofoe Medical was listed on the Shenzhen Stock Exchange's ChiNext Board in 2021 and has maintained a stable record of profitability and dividend payments as an A-share listed company over the past five years. From 2022 to early 2026, the company paid a cumulative total of over RMB 1.4 billion in cash dividends to its A-share shareholders. The combined interim and annual dividends planned for 2025 exceeded RMB 360 million—a fairly generous payout ratio for a company with an annual profit of RMB 370 million.

Given that the company already has a stable A-share financing channel and a consistent dividend-paying capability, the decision to proceed with an H-share issuance in Hong Kong typically reflects three considerations: first, to establish an offshore capital vehicle necessary for global business expansion; second, to attract international investors and enhance valuation benchmarks; and third, to meet the capital requirements of potential future major strategic initiatives such as cross-border mergers and acquisitions or overseas factory construction.

The use of proceeds disclosed in the PHIP document is divided into five categories: global expansion; product research and development and technological innovation (including artificial intelligence and Internet of Things applications); expansion of domestic sales channels and distribution networks in China; brand promotion and marketing activities; and working capital and general corporate purposes. The specific percentage allocations have been redacted as "[REDACTED]" at the PHIP stage and are expected to be disclosed in the final prospectus. The fact that "global expansion" is listed first among the five categories aligns with the accelerating trend of exports in China's home medical device industry and the increasing demand for cost-effective medical devices in European and American markets in recent years.

At the governance level, Cofoe's controlling shareholders include Mr. Zhang, Ms. Nie (who are married), Changsha Xiezi Hao Medical Investment Co., Ltd., and Changsha Keyuan Tongchuang Venture Capital Partnership (Limited Partnership). Among these, Changsha Xiezi Hao is held 90% by Mr. Zhang and 10% by Ms. Nie, while Changsha Keyuan is controlled by Mr. Zhang as its executive general partner. Mr. Zhang Zhiming (son of the controlling shareholders) serves as an executive director of the company. This is a typical "spouse co-holding plus family governance" structure, which is relatively common among A-share listed companies. The board composition complies with the listing rules of the Main Board of the Hong Kong Stock Exchange.

Where does Cofoe Stand Among Yuwell, Sinocare, BMC Medical, and Omron?

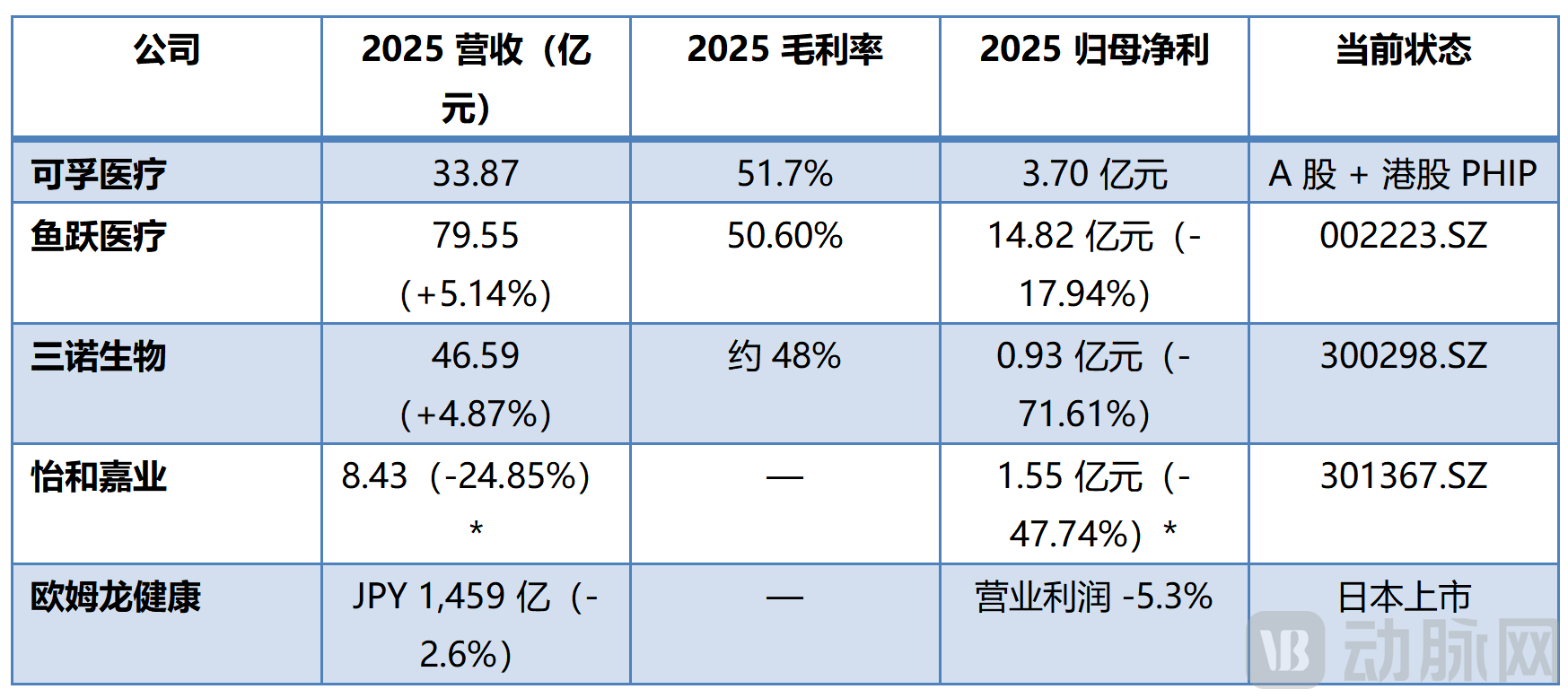

Figure 3: Comparison of Core Financial Data Between Cofoe and Comparable Companies (Note: BMC Medical data is from 2024, others are from 2025; Source: Annual Reports of Each Company)

From a scale perspective, Cofoe Medical's revenue of RMB 3.387 billion places it in the second tier of the industry. This is significantly below Yuwell's RMB 7.955 billion (approximately 43% of Yuwell's scale) and below Sinocare's RMB 4.659 billion (approximately 73% of Sinocare's scale), but substantially above BMC Medical's RMB 843 million. This scale position defines Cofoe as a "solid mid-tier player" in the industry—neither an absolute market leader nor a small niche player, but a multi-category comprehensive home medical device service provider that has achieved a certain level of both scale and product category coverage.

From a growth perspective, Cofoe is the only company among the five mentioned that achieved a simultaneous positive triple performance of revenue growth, gross margin improvement, and net profit growth in 2025. Yuwell saw revenue growth but declining net profit; Sinocare experienced slight revenue growth but a sharp decline in net profit; BMC Medical saw both revenue and net profit decline; and Omron Healthcare experienced an overall downward trend. Against this comparison, Cofoe's financial performance stands out as relatively unique within the industry.

From a profitability perspective, Cofoe's gross margin of 51.7% is higher than Yuwell's 50.60% and also higher than Sinocare's approximately 48% in 2025 (Sinocare's gross margin was 54.88% in 2024 but declined significantly in 2025 due to the impact of a patent litigation settlement and goodwill impairment), placing it at a relatively high level among the three comparable companies. Its net margin of 10.9% is comparable to Sinocare's 8.90% in 2024, but lower than Yuwell's historical normal level of 18% to 20%. This set of comparisons reflects that Cofoe's "profit conversion efficiency" still has room for improvement—the primary constraint being its relatively high selling expense ratio (34.2% versus Yuwell's approximately 18%).

Taken together, Cofoe's position in China's home medical device industry can be described as follows: a solid mid-tier player in terms of scale, currently outperforming the industry average in terms of growth, at the industry average level in terms of profitability, and still in an expansion cycle for channel and brand investment. Against the backdrop of a industry-wide adjustment period, Cofoe's relative advantages derive from the combination of a balanced product mix (not reliant on any single category), a high proportion of own-brand products, extensive e-commerce operational experience, and the emerging momentum of its customized production business.

Which Indicators are Worth Continuous Observation?

The PHIP document of Cofoe Medical lists five principal risk factors, each of which is genuinely real:

First, product market recognition and industry competition. Home medical device products are highly homogenous, and maintaining differentiation in both domestic and international competition is critical. Second, product portfolio expansion and new business execution risk. Expansion into new areas such as overseas markets, AI, and IoT applications may face execution challenges. Third, reliance on third-party e-commerce platforms. Changes in platform policies, rising traffic costs, or changes in cooperation with platforms such as Taobao, JD.com, and Pinduoduo could directly impact performance. Fourth, intellectual property protection risk. The product innovation cycle is relatively short, and without effective protection, R&D outcomes may be quickly replicated. Fifth, intensifying competition both domestically and internationally. Comparable companies such as Yuwell, Sinocare, and Omron, as well as emerging internet healthcare brands, continue to exert competitive pressure.

Based on the facts disclosed in the PHIP document and comparisons with peer companies, the following six indicators can be monitored to track Cofoe Medical's operating performance over the next 24 months:

First, whether full-year revenue and net profit for 2026 can maintain the growth momentum of 2025. The overall cyclical downturn in the home medical device industry has not yet ended. Whether Cofoe can continue to deliver growth expectations against industry headwinds will be the most critical observation point over the next 12 months.

Second, whether the gross margin of the rehabilitation aids category can be maintained above 60%. This category is the core driver of Cofoe's gross margin improvement. If the gross margin of this category declines in the future, the company's overall gross margin structure will face reassessment.

Third, whether the decline in the respiratory support category has bottomed out. After falling from RMB 455 million to RMB 261 million, this category had essentially stabilized on a sequential basis in 2025. If this category can maintain a level of RMB 250 million to RMB 280 million in 2026, it would indicate that the impact of the pandemic dividend fade has been largely absorbed.

Fourth, the customer structure and gross margin level of the customized production business. This business has grown 4.5 times over three years, but the gross margin of OEM/ODM business is typically lower than that of own-brand business. Its impact on the company's overall gross margin as it scales up needs to be monitored.

Fifth, whether the increase in the selling expense ratio can generate proportional revenue growth. The increase in the selling expense ratio from 26.0% to 34.2% is one of the company's most noteworthy financial changes at present. If future selling expenses fail to translate into corresponding revenue growth, it will directly erode net margin.

Sixth, the net proceeds from the Hong Kong H-share IPO and the actual progress of global business expansion. The company has designated "global expansion" as the primary use of IPO net proceeds. Indicators such as the proportion of overseas revenue, the pace of overseas sales network construction, and the establishment of overseas brand recognition over the next two to three years will directly determine the capital return efficiency of the H-share issuance proceeds.

In Conclusion

A secondary market analyst who has long followed the medical device industry once told the author that China's home medical device industry is undergoing a triple transformation: from channel-driven to brand-driven, from scale expansion to efficiency improvement, and from domestic-focused to globalized. In this transformation process, the few companies that can simultaneously grasp the four dimensions of brand, channel, product matrix, and globalization will achieve growth opportunities that exceed the industry average.

Cofoe Medical's financial performance from 2023 to 2025 provides a sample of "counter-trend growth amid an industry downturn." The sustainability of this sample will depend on whether the company can continue to translate its established elements—a balanced product matrix, own-brand advantages, e-commerce operational capabilities, and customized production business—into a larger global market share, more stable gross margin levels, and more solid research and development investment and brand accumulation over the next three to five years.

From five years of A-share listing to its H-share issuance in Hong Kong, Cofoe Medical has placed before Hong Kong investors an industry-level question: Can a Chinese home medical device company complete its global and brand transformation during a domestic industry cyclical downturn? The answer to this question will take five years or even longer to unfold. Along the way, every quarterly earnings report, every overseas market expansion progress update, and every commercialization achievement in a new product category will serve as an interim report card for this transformation.