The decade leap of China's innovative drug: global competition and cooperation

In the development history of China's pharmaceutical industry, the period from 2015 to 2025 is widely regarded as a decade of pivotal significance. With the advancement of reform in the evaluation and approval system, the gradual opening of the capital market, and the continuous improvement of policies supporting innovative drugs, China's innovative drug industry has gradually transitioned from a development stage dominated by generic drugs to a new phase that places greater emphasis on original research and globalized strategies. In 2024, the national-level release of the "Comprehensive Chain Support Plan for the Development of Innovative Medicines" further clarified the important position of innovative drugs within the strategic emerging industry framework.

Recently, the fifth episode of VCBeat's China Innovative Healthcare Assets Lounge Insight Relativity live broadcast officially aired. Yang Song, Chief Analyst of the pharmaceuticals industry at Tianfeng Securities, presented on the theme "A Decade Review of China's Innovative Drug Industry from 2015 to 2025." He systematically analyzed the industry's ten-year transformation across three dimensions—policy, industry, and capital markets—and provided an interpretation of future development trends based on the latest situation, offering professional insights for pharmaceutical practitioners and capital market investors.

Ten Years of Systemic Policy Reform: Strengthening the Institutional Foundation for Innovative Drug Development

In the development process of the pharmaceutical industry, regulatory policies are often important variables that influence the direction of the industry. Reviewing the policy development trajectory of China's innovative drug industry, Yang Song regarded 2015 as a landmark starting point during his live broadcast. He pointed out that the "7·22 Clinical Data Inspection" initiated in 2015 served as a watershed moment for the industry, marking a systemic shift in regulatory oversight for China's innovative drug sector. Over the following decade, the policy framework underwent multiple rounds of adjustments and improvements, gradually forming the current overarching guideline of "supporting genuine innovation and truly supporting innovation."

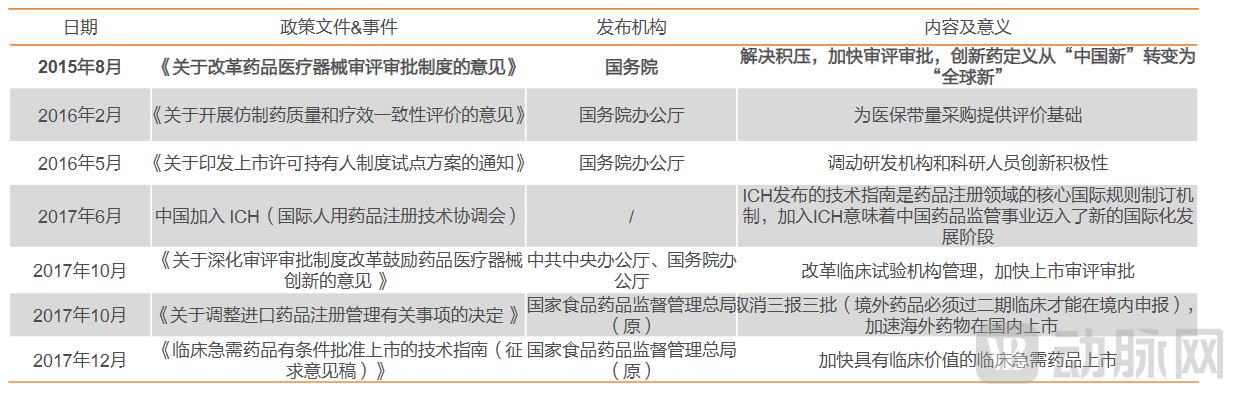

2015-2017 was a phase of breaking old systems and establishing new ones, as well as building a macro-policy framework. The "July 22 Clinical Data Inspection" initiated industry rectification, with about 80%-85% of drug application projects being withdrawn due to data issues, fundamentally eliminating the chaos of false research and development. Yang Song frankly stated: "After July 2, 2015, it marked that our entire industry began a systematic shift at the regulatory level. Before this, doing innovative drugs was more like being an early martyr rather than a pioneer." Subsequently, the release of the 2017 review and approval system reform documents further laid the foundational framework for subsequent pharmaceutical policies.

Policies and Significance of China's Innovative Drug Development from 2015 to 2017

Policies and Significance of China's Innovative Drug Development from 2015 to 2017

2018-2020: The industry entered a rapid development phase driven by policy empowerment. The establishment of the National Healthcare Security Administration restructured the pharmaceutical payment system, providing critical support for the commercialization of innovative drugs; the "4+7" volume-based procurement reduced the profit margins of generic drugs, compelling companies to transition towards innovation; the implementation of the STAR Market and Hong Kong's biotech listing system opened financing channels for innovative drug companies, with capital and policy synergistically driving industry expansion.

Policies and Significance of Innovative Drugs in China (2018-2020)

Policies and Significance of Innovative Drugs in China (2018-2020)

Under the wave of innovation, the clustering of targets and high-level repetitive research and development (R&D) problems have become prominent. From 2021 to 2023, the industry entered a phase of rational adjustment. In 2021, the National Medical Products Administration issued guidelines for anti-tumor drug R&D oriented toward clinical value, putting the brakes on homogenized R&D within the industry. In 2023, the healthcare anti-corruption campaign further drove the industry to eliminate worthless projects, with those lacking clinical value gradually being phased out. The PD-1 target became a typical example, with more than 120 projects in clinical stages and 25 approved in China, while only a single-digit number of similar targets were approved in the United States.

Policies and Significance of China's Innovative Drug Sector from 2021 to 2023

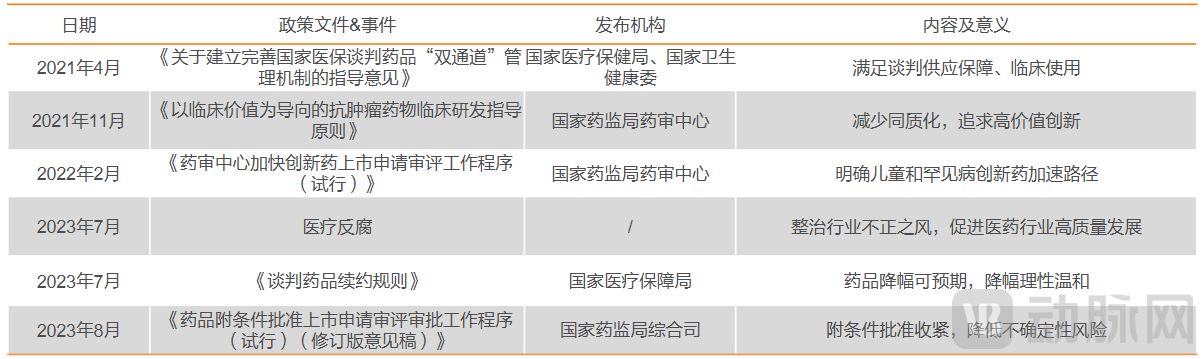

2024-2025: Innovative Drug Industry Receives Clear Strategic Positioning at the National Level. The "Comprehensive Chain Support Plan for the Development of Innovative Medicines" was released, marking the first time innovative drugs were included in the State Council's government work report and categorized as a strategic emerging industry; multiple departments such as the National Healthcare Security Administration, the National Medical Products Administration, and the National Health Commission have collaborated to form a full-chain policy support system covering R&D, evaluation, and payment.

Policies and Significance of China's Innovative Drug Development from 2024-2025

Policies and Significance of China's Innovative Drug Development from 2024-2025

Looking back on the ten-year development, China's innovative drug policy system has completed the evolution from "cleaning up order" to "systematic support": In the early stage, regulatory rectification and review reform reshaped R&D rules; in the middle stage, reforms in medical insurance and the capital market drove industrial expansion; in the later stage, it directly addressed the issue of homogeneity by returning to a clinical value orientation, ultimately establishing innovative drugs as a strategic industry at the national level.

From Imitation to Global Participation: The Activity of China's Innovative Drug Development Continues to Increase

Driven by the improvement of the policy system and continuous capital investment, China's innovative drug industry has undergone a structural leap in the past decade: transitioning from an early development model dominated by generic drugs to an industry system centered on innovative research and development, and beginning to deeply participate in global pharmaceutical innovation competition.

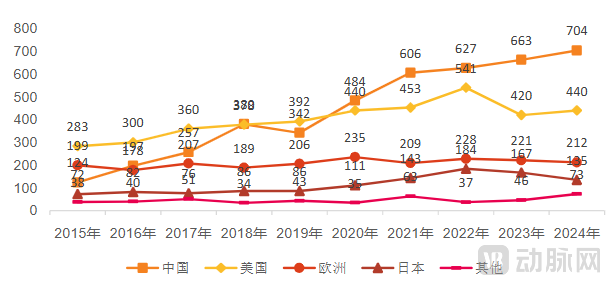

In terms of quantity, the activity of China's innovative drug research and development has already ranked among the top globally. Yang Song mentioned in the live broadcast that, as of 2024, the number of domestically produced innovative drugs approved in China ranks first globally. Although approximately 40% of these products are still mainly approved within the Chinese market, the participation of Chinese companies in the global competition for popular targets has significantly increased. As of June 2025, domestic companies account for over 60% of clinical trials targeting the top 10 global popular targets.

Number of Global Innovative Drug Developments (in units) and Research Countries/Regions During 2015-2024

Number of Global Innovative Drug Developments (in units) and Research Countries/Regions During 2015-2024

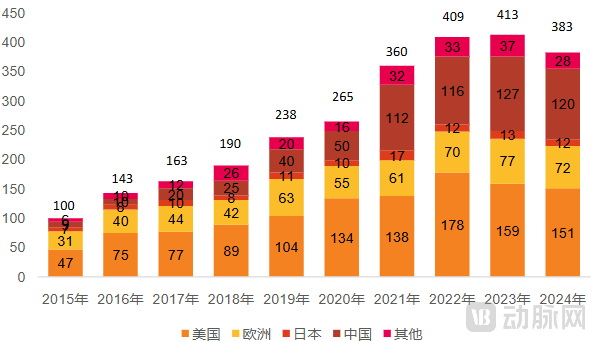

The improvement in innovation quality better reflects industrial strength, and the change in the proportion of First-in-Class (FIC) drugs is a core indicator. Shared data shows that in 2015, the proportion of FIC drugs independently developed by Chinese companies was less than 10%, but by around 2024, this proportion has significantly increased. In the global new drug R&D pipeline structure, China's FIC projects account for 24%, surpassing Europe (21%) and Japan (8%), and gradually narrowing the gap with the United States (43%).

Number and Countries/Regions of Global FIC Innovative Drug Development from 2015 to 2024

Number and Countries/Regions of Global FIC Innovative Drug Development from 2015 to 2024

At the same time, the gap in the R&D cycle for innovative drugs between China and the U.S. continues to narrow. Yang Song pointed out that, looking at the timeline over a longer period, 20 years ago, the launch of new drugs in China often lagged more than ten years behind the U.S.; by around 2015, the time gap for first-generation innovative products had shortened to 5-10 years. In recent years, with the improvement in R&D capabilities and reforms in the regulatory system, the pace of R&D for next-generation innovative drugs has significantly accelerated. In fields such as ADCs and PD-1/PD-L1 bispecific antibodies, some products have achieved nearly synchronized R&D progress with overseas companies. Overall, the time difference for new drug approvals between China and the U.S. has now been reduced to about 2-3 years, which has also driven an increase in cross-border collaborations and transactions.

In Yang Song's view, the rapid improvement in both scale and quality of China's innovative drug industry within a relatively short period can be attributed to the gradual accumulation of industrial foundational capabilities. First, CXO companies like WuXi AppTec and Asymchem have established comprehensive service systems covering the entire chain from drug discovery to clinical production, continuously enhancing the collaborative ability of the industrial chain. Second, the engineer dividend has been fully unleashed; by 2025, the number of STEM doctoral graduates in China is expected to be about twice that of the United States, with biopharmaceutical professionals increasingly gathering in the industry. Third, there has been a dual increase in R&D investment and fundamental research—pharmaceutical enterprises listed on A+H shares invest over 100 billion RMB annually in R&D, while the number of high-quality papers in the biopharmaceutical field has grown, strengthening the transformation pathways between basic research and industrial R&D.

The most significant change in China's innovative drug industry over the past decade is not only the rapid growth in the number of research and developments but also the simultaneous improvement in innovation capabilities and industrial infrastructure. From a global industry perspective, Chinese companies are gradually transitioning from being participants in regional markets to becoming an important pole in the global innovation system.

Ten Years of Iteration in the Capital Market: From Capital Influx to Value Restructuring

If policy reshaped the industry's rules and R&D capabilities drove the industry's transformation, then the capital market has largely determined the pace of development for the innovative drug industry. Over the past decade, with the successive implementation of reforms on the STAR Market and the Hong Kong stock exchange, Chinese innovative drug companies have gradually gained access to financing channels. The capital market, in tandem with industry development, has experienced a full cycle ranging from initial exploration and concentrated capital inflows to deep adjustment.

From 2015 to 2018, in the early stage of the industry, the number of innovative drug companies was small, R&D capabilities were still being accumulated, and capital attention was limited. The focus of public offering funds' allocation in the pharmaceutical sector remained on traditional pharmaceuticals and Chinese medicine enterprises. Data shows that at that time, traditional pharmaceuticals accounted for about 30%-40% of public offering funds’ pharmaceutical holdings, while the Chinese medicine sector accounted for approximately 20%-25%. Innovative drug companies were hardly included in mainstream allocation ranges.

A turning point occurred around 2018. As the listing systems for biotech companies on the Sci-Tech Innovation Board and the Hong Kong stock market gradually improved, financing channels for innovative drug enterprises significantly broadened. From 2018 to 2021, pharmaceutical companies on China's A-share Sci-Tech Innovation Board and Growth Enterprise Market collectively raised nearly 200 billion yuan, while the financing scale in the Hong Kong stock market reached approximately 300 billion RMB. Over 500 billion RMB of capital inflow accelerated rapid industry expansion but also led to a temporary bubble. Some companies were able to secure financing based solely on pipeline planning, even before clinical data had been established. Yang Song mentioned during a live broadcast that during this period, the market paid more attention to the number of projects, stating, "As long as there is a pipeline, it could receive funding," with relatively insufficient evaluation by capital of research quality and clinical value.

As the issue of homogeneous R&D gradually emerged, coupled with changes in the macro capital environment, the innovative drug sector entered an adjustment phase around 2021. Several Hong Kong-listed and A-share innovative drug companies began actively reviewing their R&D pipelines, suspending some homogenous or non-core projects to focus resources on areas of strength. In this process, the proportion of public funds' holdings in the traditional pharmaceuticals sector significantly decreased, and the investment logic for innovative drugs gradually returned to rationality, placing greater emphasis on clinical value, differentiation capabilities, and product commercialization prospects.

In 2024, the innovative drug sector is experiencing a rational recovery. Data shows that by 2025, the proportion of public funds invested in innovative drug companies has rebounded to about 20%. The holding ratio of the Contract Development and Manufacturing Organization (CDMO) sector has stabilized at around 15%-20%. Together, these two sectors, along with traditional pharmaceutical companies, account for approximately 85%-90% of the pharmaceutical sector's allocation. In contrast, the holding ratio of the Traditional Chinese Medicine (TCM) sector has dropped to 3%-4%. From a structural perspective, the capital market is reassessing the value distribution within the pharmaceutical industry, with innovative drug companies possessing continuous R&D capabilities and core product potential regaining financial attention.

From a longer-term perspective, the adjustment and recovery of the capital market essentially represent a process where investment logic returns to industrial patterns. As the industry moves beyond its early expansion phase, the criteria by which capital evaluates innovative drug companies have shifted. Future capital allocation will focus more on research and development capabilities, clinical data, and global potential, rather than solely relying on pipeline quantity as the basis for judgment.

The industry moves towards a high-quality development stage, focusing on molecular quality and commercial value

From 2024 to 2025, as the policy system gradually improves, industrial capabilities continue to strengthen, and the capital market returns to rationality, the development foundation of China's innovative drug industry will further solidify. Yang Song pointed out during a live broadcast that the core of industry development in the coming years will focus on "molecular quality enhancement" and "commercial value realization." China's innovative drug industry is transitioning from a previous phase of primarily scale expansion to a more refined development cycle that emphasizes efficiency and quality.

First, improving molecular quality and strengthening differentiated R&D has gradually become an industry consensus. After experiencing industry adjustments from homogeneous R&D, companies are now more focused on clinical value and competitive barriers when initiating R&D projects. Product quality and differentiation advantages have become the core considerations for project advancement. Companies' willingness to expand globally continues to grow, with BeOne Medicines' core product expected to achieve approximately $3.9 billion in global sales by 2025, surpassing the total revenue of some pharmaceutical companies in China, demonstrating the enormous market potential for innovative drugs going overseas.

Under the background of globalization, licensing cooperation in pharmaceutical enterprises continues to upgrade. The total amount of licensing transactions for innovative drugs in China in 2025 has exceeded 130 billion RMB, with upfront payments of approximately 6 to 7 billion US dollars. Compared with the "selling green shoots" model, where authorization occurs at the early R&D stage, companies are increasingly inclined to advance cooperation after completing proof of concept (POC) in clinical trials to enhance product value. Meanwhile, the European market is gradually becoming an important region for Chinese enterprises to carry out international cooperation.

On the industry side, the technical accumulation of platform-based enterprises is gradually being transformed into commercial results. Companies such as Hengrui Medicine and Innovent Biologics have, after more than a decade of research and development, built up diversified technology platforms and pipeline systems. The technologies and talent resources accumulated in the past are now entering a harvest period as projects move into the later stages of clinical trials or engage in international cooperation. Meanwhile, AI technology is deeply integrated into the entire drug R&D process, enhancing R&D efficiency in areas such as target screening and compound design, with multiple companies having already implemented related collaborations.

At the enterprise operation level, achieving profitability has become a new goal for the industry. Yang Song pointed out that innovative drug companies used to generally rely on continuous financing to support R&D, but as the industry gradually matures, an increasing number of companies have begun to seek a balance between R&D investment and commercial returns. According to his observations, by around 2026, nearly half of China's innovative drug companies will incorporate profitability into their phased plans, shifting the industry's business model from solely relying on capital to a more sustainable development path.

Looking at a longer cycle, Yang Song judged that in the next 1-3 years, China's innovative drug industry will still maintain a relatively high level of activity: On the one hand, the FIC proportion of Chinese enterprises in the global innovative drug R&D pipeline is expected to further increase; on the other hand, as more products enter overseas clinical trials or are approved for marketing, the export of innovative drugs will gradually become the norm. At the same time, at the capital market level, enterprise valuation will rely more on fundamental factors such as R&D capabilities and commercial performance, and industry competition will also focus more on quality and efficiency.

With continuous policy support and the steady accumulation of industrial capabilities, the development path of China's innovative drug industry is becoming increasingly clear. As the policies related to the "15th Five-Year Plan" are implemented and advanced, and with the continuous enhancement of enterprises' global R&D and cooperation capabilities, the participation and influence of China's innovative drug companies in the global pharmaceutical innovation system will further increase. As Yang Song mentioned during the live broadcast, in the next three to five years, innovation will become a brand-new growth driver for the development of China's biopharmaceutical industry, propelling China to occupy a more significant position in the global pharmaceutical landscape.