Performance recovery! Pharmaceutical CXO stock prices surge collectively

WuXi AppTec

New Drug R&D and Production Service Provider

ASYMCHEM

Pharmaceutical R&D and Production Outsourcing Service Provider

JOINN

Contract Research Organization (CRO)

Tigermed

Biopharmaceutical R&D Service Provider

Two days ago, on April 28, the A-share market witnessed a rare scene.

As the Q1 2026 earnings report was released, WuXi AppTec, the pharmaceutical CXO leader with a market value exceeding 300 billion RMB, hit the daily limit up just five minutes after the opening. Immediately, the upward trend of the entire pharmaceutical CXO sector was ignited, with

Asymchem hitting the limit up, Pharmaron rising by 5.42%, and the sector index surging over 2% at one point.

Unlike the previous purely conceptual hype, this wave of increase appears to be well-founded. As annual reports are gradually released, leading CXOs have seen their revenue double, gross margins significantly improve, and orders surge. Although the next day, the sector failed to maintain its strong momentum. However, the growth in performance has led to expectations of an industry recovery.

Has the New Cycle of Recovery Finally Arrived?

The day before the collective surge in CXO stock prices in the pharmaceutical industry, WuXi AppTec released its Q1 2026 earnings report. The data shows that in the first quarter of 2026, WuXi AppTec's revenue reached 12.426 billion RMB, a year-on-year increase of 28.8%. This marks the first time that WuXi AppTec's single-quarter revenue has exceeded 10 billion RMB. More importantly, as the traditional off-season for business, the revenue growth rate in the first quarter of 2026 surpassed the average level of 2025, raising higher expectations for WuXi AppTec's overall performance in 2026.

In fact, apart from WuXi AppTec, the recent financial reports of several pharmaceutical CXOs have shown many highlights. For example, according to the latest annual reports, in 2025, JOINN and Tigermed's net profits both doubled, with JOINN's growth rate at 327% and Tigermed's at 119.2%. Additionally, Asymchem, Porton Corporation, and Medicilon also significantly reversed their business performance in 2025. Among them, Asymchem's non-GAAP net profit growth rate reached 56.1%. Porton Corporation turned losses into profits, with operating cash flow seeing an 87% significant increase, while Medicilon, although still incurring losses, saw a substantial narrowing of its loss under the pull of rapid revenue growth.

However, a further analysis of the 2025 financial report data of several pharmaceutical CXOs reveals that the impressive operating performance is more attributable to localized structural adjustments rather than an overall cyclical recovery.

On the one hand, despite the emergence of scattered impressive performance data, not all pharmaceutical CXO sub-sectors have shown favorable growth trends. Overall, while CDMO performance has collectively improved, CRO continues to weaken as a whole.

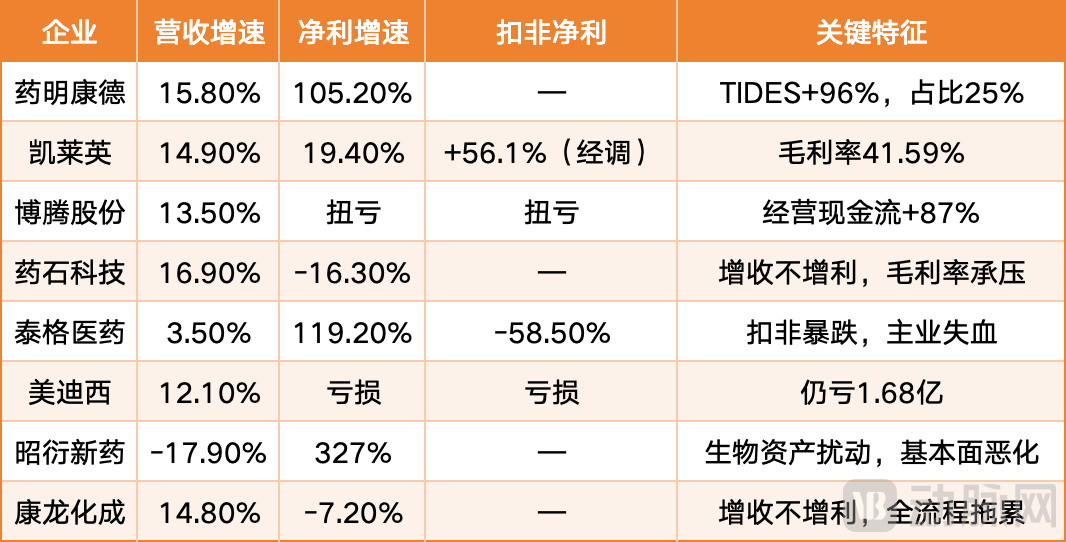

Partial Data from the 2025 Financial Reports of 8 CXOs Data Source: Compiled from financial reports

Partial Data from the 2025 Financial Reports of 8 CXOs Data Source: Compiled from financial reports

First, it is important to clarify that the eight pharmaceutical CXO companies included in this analysis are all leading enterprises. However, fluctuations in their financial data still reflect the ups and downs of the industry. Among them, WuXi AppTec, Asymchem, Porton Advanced, and PharmaBlock, as CDMOs, generally have higher revenue growth rates compared to CROs such as Tigermed, Medicilon, JOINN, and Pharmaron. Notably, among the eight pharmaceutical CXOs analyzed, JOINN was the only company to experience negative revenue growth.

In addition to revenue indicators, other financial metrics of CDMOs also generally show signs of performance improvement, which is not as evident in CROs. For instance, WuXi AppTec and Asymchem have seen rapid increases in profit margins alongside substantial revenue growth, with WuXi AppTec even experiencing a doubling of net profit. In contrast, while Tigermed's net profit doubled, its revenue growth has been sluggish, and its non-GAAP net profit plummeted by 58.5%, indicating weakness in its core business. Meanwhile, JOINN's net profit tripled, but it faced negative revenue growth, with the increase in net profit mainly driven by fluctuations in the price of experimental monkeys.

On the other hand, even within the high-growth CDMO industry, the differentiation in performance is quite evident. In 2025, Pharmablock generated revenue of 1.974 billion RMB, a year-on-year increase of 16.9%, which is not a bad growth rate. However, the net profit attributable to shareholders was 184 million RMB, a year-on-year decrease of 16.3%, representing a typical case of revenue growth without corresponding profit growth. Pharmablock originated from its molecular building blocks business, providing high-purity, high-quality chemical building blocks for small molecule drug research and development. This business has a high technical threshold and stable gross margin, but its ceiling is limited, and its growth rate has slowed down. In recent years, Pharmablock has been transitioning to CDMO. However, its new process development, pilot-scale production, and commercial production businesses are still in the process of scaling up. In 2025, Pharmablock's gross margin was approximately 31%, a decrease of 7 percentage points from about 38% in 2023.

Comparison of Cyclical High Data for 8 CXOs Since 2021 Data Source: Compiled from Public Information

Comparison of Cyclical High Data for 8 CXOs Since 2021 Data Source: Compiled from Public Information

More importantly, if the observation period is extended back to 2021, aside from WuXi AppTec, Pharmaron, and PharmaBlock, most pharmaceutical CXOs' operating data remains at a historical low. Among them, Porton Advanced achieved revenue of 3.42 billion RMB in 2025, representing a decline of 51.48% compared to its cyclical peak in 2022. Asymchem and JOINN also fell by 34.96% and 30.22%, respectively, from their cyclical highs, with significant declines still evident.

Behind the Two Explosive Data Points

Another set of data that has drawn significant attention is that in 2025, WuXi AppTec, the leader in CDMO, and Tigermed, the leader in clinical CRO, are both overwhelmed with orders, with their order backlogs reaching record highs. This reflects an even more crucial underlying industry logic.

According to the annual report, by the end of 2025, WuXi AppTec's order backlog reached 58 billion RMB, a year-on-year increase of 28.8%. This is an unprecedented record in CXO history for a single company's order reserve, equivalent to approximately 14 months of WuXi AppTec's revenue. By the end of the first quarter of 2026, this figure climbed further to 59.8 billion RMB, a year-on-year increase of 23.6%, becoming the most impressive part of WuXi AppTec's explosive financial report. Meanwhile, Tigermed signed new orders worth 10.16 billion RMB in 2025, a year-on-year increase of 20.7%, setting a new historical record.

However, it is important to note that the growth logic behind the same explosive orders varies.

First, let's look at the explosive order volume of WuXi AppTec. The driving force behind it lies in capitalizing on industry trends and making early strategic arrangements, which follows the logic of an incremental market. According to the annual report, the main driver of WuXi AppTec's performance growth this time comes from its peptide business. In 2025, revenue from WuXi AppTec's peptide and oligonucleotide business (TIDES) reached 11.37 billion RMB, a year-on-year increase of 96%, with its share of the company's total revenue rising from approximately 15% three years ago to 25%. This is the concentrated release of GLP-1 drug commercial production capacity, essentially driven by incremental contributions from a few major clients and key product varieties.

Although there are hundreds of GLP-1 pipelines under research globally, only a few have truly entered the commercialization stage. These orders are highly concentrated among leading CDMOs with the capability to mass-produce peptides. Take semaglutide as an example: the annual API demand ranges from tens to hundreds of kilograms, which cannot be met simply by expanding existing small-molecule production lines. It requires specialized solid-phase synthesis equipment, large-scale purification systems, and unique formulation capabilities. There are only a handful of CDMOs worldwide that possess the ability to commercially mass-produce peptides, with WuXi AppTec's TIDES being the largest in scale. More importantly, due to high technical barriers, peptide businesses exhibit stronger customer stickiness. Once a pharmaceutical company selects a peptide supplier, the cost of switching is extremely high, making it difficult for new entrants to break in.

In WuXi AppTec's financial report, there is an easily overlooked ratio that illustrates its position in the peptide market. In 2025, WuXi AppTec's revenue growth rate was 15.8%, but its net profit growth rate reached 105.2%. The nearly 90-percentage-point scissors gap is evidence of its market influence.

Tigermed's order explosion can be attributed to the redistribution of market shares caused by supply-side consolidation, which follows the logic of a stock market. According to the human genetic resources filing data from China's National Health Commission, the number of clinical CRO companies in 2025 will decrease by 69% compared to the peak in 2021. In other words, the surge in orders is not due to an expansion of the market pie, but rather a reduction in the number of competitors vying for it. However, the harsh winter for clinical CROs is far from over.

However, from a financial data perspective, the quality of Tigermed's orders is improving. In 2025, while signing new orders worth 10.16 billion RMB, Tigermed's revenue for the same year was only 6.833 billion RMB, creating a gap of 3.2 billion RMB. According to the revenue recognition rules for CXO companies, this 3.2-billion-RMB gap indicates that the 10.16 billion RMB in new orders mainly consists of larger and more complex projects, such as Phase III clinical trials, head-to-head registration trials, and international multicenter clinical trials. The unit price and gross profit margin of these types of projects are much higher than those of early-stage clinical trials.

Whether it is the increase in CDMO's influence in emerging fields or the shift of clinical CRO service ports to later stages, these are all positive signals in the development process of pharmaceutical CXO. Compared to a surge in order volume, the optimization of operational practices behind these explosive orders is undoubtedly more worthy of attention.

Certainty Hidden in Differentiation

Despite the inevitable differentiation, in a sense, this round of performance explosion in the pharmaceutical CXO sector essentially represents a concentrated realization of the upgrade in China's comprehensive pharmaceutical manufacturing capabilities. The process by which WuXi AppTec seized the GLP-1 wave is merely a microcosm of this upgrade.

On the one hand, at the micro enterprise level, moving from cost advantage to capability advantage. Traditionally, the core competitiveness of CXOs in China has been defined by their cost advantages. For the same R&D services, the quotations from domestic CXOs could be 30%-50% lower than those in Europe and America, which was the primary reason international pharmaceutical companies initially chose Chinese CXOs. However, after this round of growth, the narrative of cost advantage has started to become outdated. WuXi AppTec's TIDES business is projected to reach 11.37 billion RMB in revenue by 2025, with a year-on-year increase of 96%, a 25% growth in the number of clients served, and a 20.2% increase in orders on hand. Behind these figures, the domestic CXO services are no longer catering only to price-sensitive customers.

Around 2021, when GLP-1 drugs were still in the clinical trial stage, WuXi AppTec had already begun to expand its peptide production capacity. The decision at that time was not easy, as peptide synthesis equipment required significant investment, and the difficulty of process development was much higher than that of traditional small molecules. Moreover, it was still uncertain whether GLP-1 could become a "blockbuster" drug. However, WuXi AppTec chose to make an early bet by building a commercial peptide production line at its Changshu site, recruiting a professional peptide synthesis team, and establishing end-to-end capabilities from R&D to production. This laid the foundation for WuXi AppTec's GLP-1 business to start yielding results in 2023 and fully blossom between 2024 and 2025.

More importantly, this capability brings self-reinforcing operating performance. Once leading CXOs establish customer trust in a particular area, the cost for pharmaceutical companies to switch suppliers is extremely high. For instance, process validation takes 2-3 years, and FDA submissions need to be resubmitted. In the fiercely competitive battlefield of new drug development, time is more important than cost savings. Therefore, every major client of a leading CXO could potentially represent a long-term order spanning 5 to 10 years. WuXi AppTec's 58 billion RMB backlog of orders essentially represents highly certain future revenue secured by its capability moat. This kind of moat cannot be quickly replicated with money, leaving latecomers to watch the gap widen.

On the other hand, at the macro level of market efficiency, the concentration of resources and orders towards the top players has led to an optimization of the competitive landscape. As mentioned earlier, since 2021, the number of clinical CROs in China has significantly decreased, which is only one aspect of the supply-side consolidation within China's CXO industry. The CDMO sector is also experiencing an accelerated consolidation. The sharp decline in the number of clinical CROs has driven Tigermed to achieve a record high in new contract signings, while Asymchem's emerging business growth exceeded 50%, and Porton Corporation turned losses into profits, all benefiting from the market share left by exiting competitors. Once the increase in market concentration begins, it creates a self-accelerating positive cycle. Leading companies gain more revenue, allowing them to invest in R&D and capacity expansion, further enhancing their service capabilities, attracting larger clients, and driving continuous revenue cycles. WuXi AppTec plans to invest over 1 billion RMB in R&D by 2025, and Asymchem's investments in continuous flow reaction technology are reinforcing this "the strong get stronger" spiral.

Improved concentration means optimized efficiency in resource allocation. Over the past decade, the CXO industry has experienced "unchecked growth," with a flood of small and medium players entering the market, leading to severe homogenization and frequent price wars, plunging the entire industry into a "bad money drives out good" dilemma. After the supply-side consolidation, leading companies have more abundant funds to invest in R&D, improve quality systems, and expand compliant production capacity, forming a positive cycle. For end users, a clearer market landscape will also reduce supply chain management costs.

Overall, while emerging from the market downturn, China's CXO industry is also continuously growing. Of course, this process will become long and tortuous due to the cyclical fluctuations in downstream demand.