First A-to-H 18A listing: Mabwell pioneers dual-value circulation for mature biotech

Mabwell

Innovative Biopharmaceutical Company

On April 28, Mabwell officially listed on the Main Board of the Hong Kong Stock Exchange, becoming the first unprofitable biotech company to go public through the "A-share STAR Market + Hong Kong Stock 18A" approach. Notably, the "A to H 18A" pathway had no precedent in the capital markets until now. This means that the rules and pathways successfully navigated by Mabwell have become a "first" developed in discussions with the Hong Kong Stock Exchange.

In this global offering, Mabwell issued 47,130,200 H shares at an offering price of HKD 27.64 per share. Based on this calculation, the net proceeds amounted to HKD 1.189 billion. This morning, the opening price was HKD 28.30 per share, with a total market capitalization of approximately HKD 12.6 billion.

Over the past four years, Mabwell has grown from a yet-to-be-profitable R&D-focused Biotech into a Biopharma with mature commercialized products, core innovative pipelines entering the global late-stage development phase, and end-to-end capabilities.

At this juncture, the "A-to-H 18A" path represents the necessary route from the local market to global competition.

1From Biotech to Integrated Biopharma

Mabwell was founded in 2017. In early 2022, it went public on the A-share market under the fifth set of listing standards for STAR Market, at which time it had no products on the market and was positioned as an "innovative biopharmaceutical company," with its operations entirely focused on the R&D side—all pipelines were in clinical or preclinical stages. Now, as it heads to Hong Kong for an IPO, its positioning has evolved into "a Chinese pharmaceutical company renowned for its innovative capabilities in drug research and development as well as its end-to-end capabilities from drug discovery to commercial sales."

The clearest progress lies in Mabwell's transformation from a pure research and development entity to a full-industry-chain operator covering "R&D, manufacturing, and commercialization," with significantly enhanced self-sustaining cash flow. The company has successfully brought to market three biosimilars (MAILISHU®, MAIWEIJIAN®, and JUNMAIKANG®) and one innovative drug (MAILISHENG®, a long-acting G-CSF product). All three biosimilars have been included in the National Reimbursement Drug List and are not subject to national volume-based procurement.

MAILISHENG®, approved for marketing in May 2025, is the first innovative drug in China developed using albumin long-acting fusion technology and represents a new generation of long-acting granulocyte colony-stimulating factor (G-CSF), indicated for febrile neutropenia. Less than six months after approval, it has been included in the 2025 National Reimbursement Drug List (effective January 1, 2026).

MAILISHU® (Orthopedics) , the second biosimilar of Prolia® (denosumab) approved in China for the treatment of osteoporosis, was approved in March 2023 for the treatment of osteoporosis in postmenopausal women at high risk of fracture. In 2025, it was approved for marketing in Pakistan, becoming the first generic of its category in that country. Sales revenue for 2024 and 2025 reached RMB 124.4 million and RMB 202.8 million, respectively.

MAIWEIJIAN® (Oncology) , the first biosimilar of Xgeva® (denosumab) approved in China, was approved in March 2024 for the treatment of giant cell tumor of bone that is unresectable or where surgical resection is likely to result in severe morbidity. In 2025, it was approved for marketing in Pakistan, becoming the first generic of its category in that country. Sales revenue for 2024 and 2025 reached RMB 14.6 million and RMB 3.7 million, respectively.

JUNMAIKANG®, an adalimumab biosimilar, was approved in March 2022 for the treatment of rheumatoid arthritis, ankylosing spondylitis, and psoriasis. In November of the same year, supplemental applications were approved for additional indications including Crohn's disease, uveitis, polyarticular juvenile idiopathic arthritis, pediatric plaque psoriasis, and pediatric Crohn's disease. In July 2025, Mabwell regained the Marketing Authorization Holder (MAH) for Jun Maikang® from Junshi Biosciences, transitioning to fully autonomous management of the entire commercialization process. Sales revenue for the fourth quarter alone reached RMB 39.9582 million.

Over the four years, Mabwell has transitioned from an early stage of heavy investment and weak revenue to a mature development phase characterized by precise R&D, diversified income, and integrated industrial operations, directly manifested as continuous optimization of financial fundamentals.

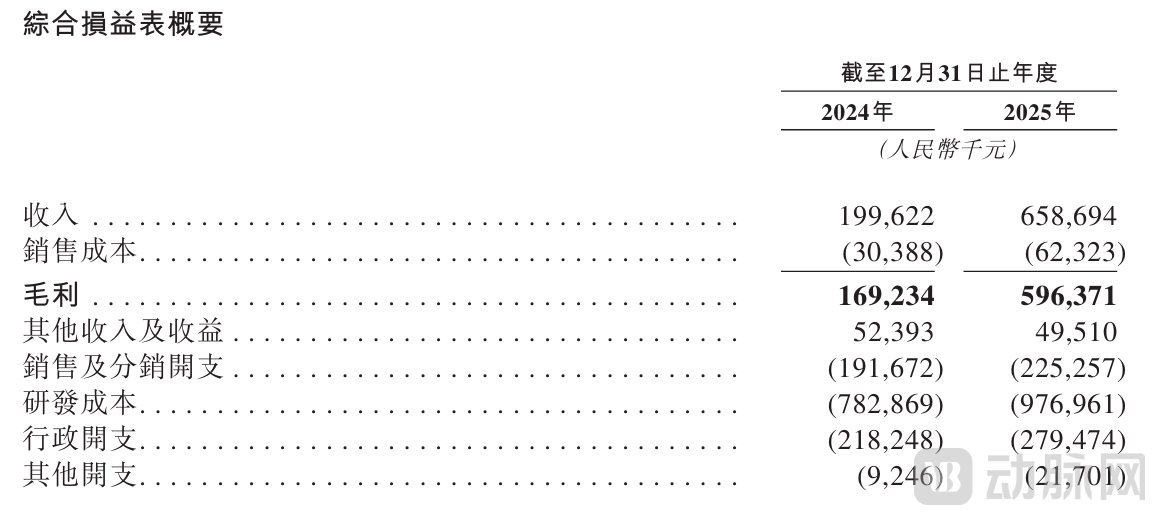

Summary of Comprehensive Income Statement

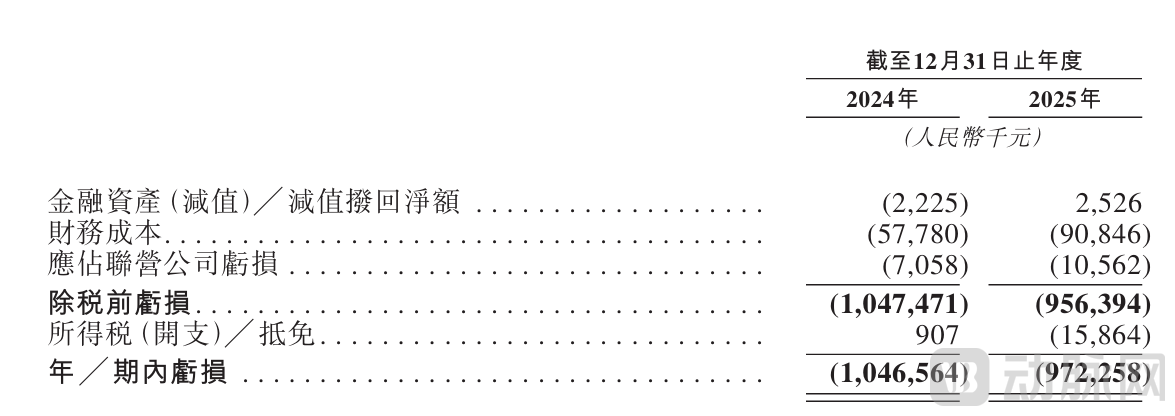

Summary of Cash Flow Statement

Overall, Mabwell remains in a phase of continuous research and development investment, with net losses of approximately RMB 1.047 billion and RMB 972 million in 2024 and 2025, respectively. However, positive signals of narrowing losses and stabilized cash flow have emerged, with year-end cash and cash equivalents reaching approximately RMB 1.228 billion and RMB 1.526 billion, respectively. Notably, the net amount of cash and cash equivalents reversed from a net outflow of RMB 416 million in 2024 to a net inflow of RMB 302 million. This improvement was primarily driven by leapfrog revenue growth and optimization of the business revenue structure.

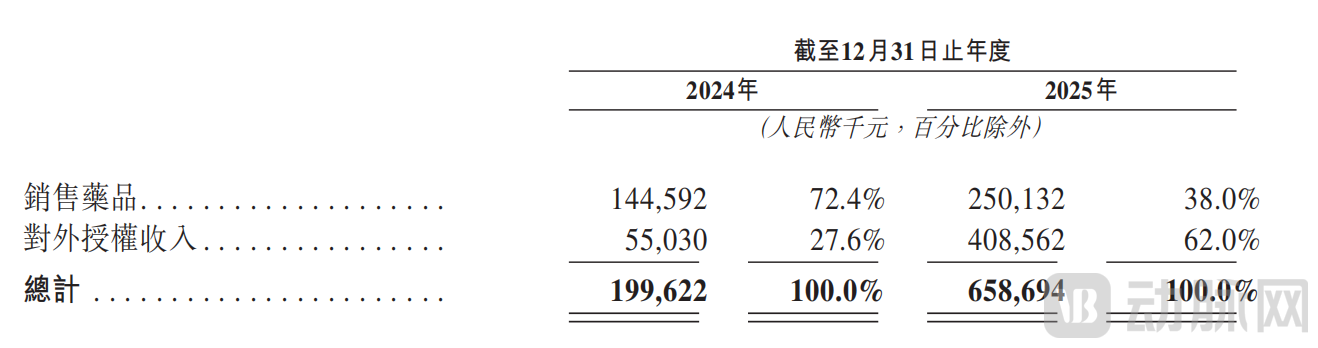

In 2024 and 2025, Mabwell's revenue reached approximately RMB 200 million and RMB 659 million, respectively, representing a substantial year-on-year increase of 229.8 percent. In particular, breakthroughs were achieved in both core growth drivers: out-licensing revenue amounted to RMB 55.03 million and RMB 409 million, accounting for 27.6 percent and 62.0 percent of total revenue, respectively; and product sales revenue amounted to RMB 145 million and RMB 250 million, accounting for 72.4 percent and 38.0 percent of total revenue, respectively.

Revenue Details by Nature

As commercialization accelerates, Mabwell's strategic focus has naturally extended from the local market to a global footprint. In the biosimilar segment, the company places particular emphasis on emerging markets and countries along the Belt and Road, adopting a "licensing plus local partnership" model, under which Mabwell grants its partners in target markets the rights to register, fill and finish, sell, and promote its products, leveraging their regulatory capabilities and commercial networks to rapidly achieve market entry and increase the share of overseas revenue.

Taking MAIWEIJIAN® and MAILISHU® as examples, Mabwell has entered into commercialization agreements (with commercial licenses) with leading pharmaceutical companies in multiple countries and regions, including Brazil, Peru, the Philippines, and the Middle East and North Africa. Additionally, the company has signed commercialization agreements (retaining ownership rights) with partners in 33 countries, including Colombia, Indonesia, and Thailand.

According to incomplete statistics from VCBeat, Mabwell's global licensing landscape

Not only that, but in the innovative drug sector, Mabwell also ushered in an outbound licensing boom in 2025:

In June 2025, Mabwell entered into an exclusive license agreement with Calico for 9MW3811 (a humanized monoclonal antibody targeting IL-11), receiving a one-time, non-refundable upfront payment of US$25 million. Mabwell is also entitled to receive up to US$571 million in milestone payments and royalties. Calico has obtained the exclusive rights to develop, manufacture, and commercialize 9MW3811 in regions outside Greater China.

In June, Mabwell granted Qilu Pharmaceutical the exclusive license rights to develop, manufacture, improve, utilize, and commercialize JUNMAIKANG® in the Greater China region. Mabwell is entitled to receive total payments of up to 500 million RMB, including a one-time, non-refundable upfront payment of 380 million RMB.

In September, its preclinical, dual-target small nucleic acid drug (siRNA) 2MW7141 was licensed out under the NewCo model, granting Kalexo Bio exclusive global rights. Mabwell will receive a one-time upfront payment and near-term payments totaling $12 million, with the potential total value of the deal reaching up to $1 billion, along with preferred shares of Kalexo upon achieving specified milestones.

The long-tail effect of early licensing deals gradually became evident, forming a continuous stream of milestone revenues. According to the 9MW3011 licensing agreement reached with DISC in 2023, Mabwell has successively received milestone payments of US$5 million for Phase I trials and US$10 million for Phase II trials, with a potential total transaction value of up to US$402.5 million.

2Core ADC Pipeline Progresses Among Global Top Three

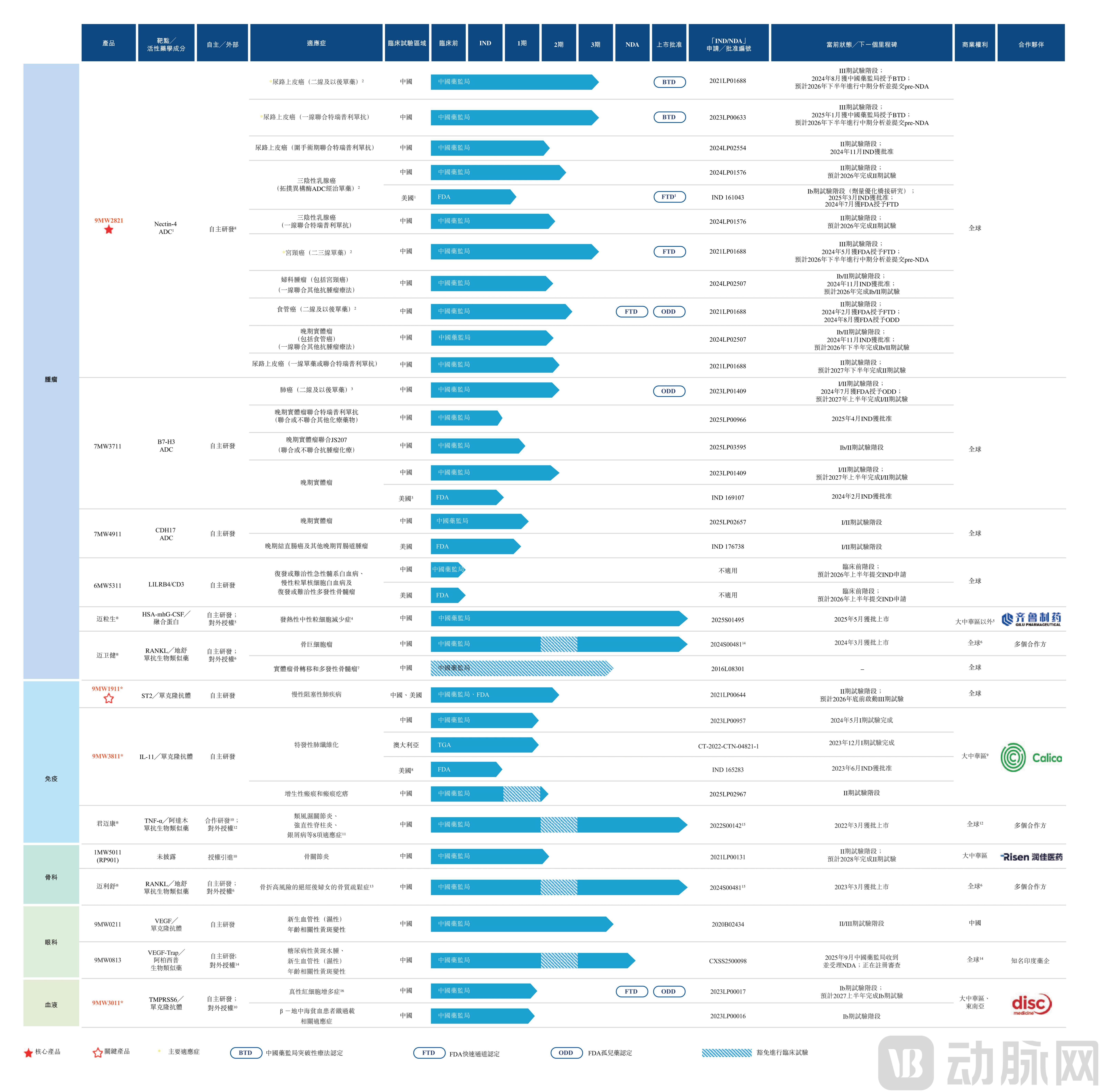

On the product narrative side, Mabwell currently has 10 drug candidates (1 at the NDA stage, 8 in clinical stages, and 1 in the preclinical stage). Its core technologies include an ADC drug development platform, an integrated high-efficiency antibody discovery platform, and a TCE bispecific/trispecific antibody development platform. The global clinical experience accumulated earlier and the solid platform technology will directly empower the advancement of the innovative pipeline, driving the company to establish a globally leading advantage in indication selection and clinical trial expansion.

Compared with the STAR Market prospectus, ADC has become the core narrative under Mabwell's oncology indications.

Post-Hearing Data Set - Pipeline Product Chart

Mabwell has established four core ADC technologies with independent intellectual property rights: the site-specific conjugation technology DARfinit; the optimally designed linker molecule IDconnect, which enhances the connection stability between antibodies and toxins; the novel camptothecin-based toxic molecule Mtoxin, serving as the warhead to kill target cells in ADCs; and the structure for conditional toxin release, LysOnly, which improves the overall safety and efficacy of ADC products.

According to the Frost & Sullivan report, the core product 9MW2821 is the ADC drug targeting Nectin-4 with the fastest progress in China, with three Fast Track Designations (FTD) and one Orphan Drug Designation (ODD) granted by the FDA, as well as two Breakthrough Therapy Designations (BTD) for monotherapy and combination therapy approved by the NMPA. It is currently in Phase III and pivotal Phase III clinical trials for multiple indications, including urothelial carcinoma, cervical cancer, triple-negative breast cancer, and advanced esophageal cancer, with plans to submit a New Drug Application (NDA) for monotherapy by 2027.

Among Nectin-4 ADC products globally for the treatment of urothelial carcinoma, 9MW2821 ranks second only to Padcev, the only approved product in its class, developed by Astellas/Seagen (Pfizer). Padcev saw significant sales growth in 2025, reaching USD 3.34 billion. Furthermore, 9MW2821 is leading in differentiated indication development and has become the first product of its kind globally to enter a pivotal Phase III clinical trial for cervical cancer.

Globally, there are 11 Nectin-4-targeted ADC candidates in clinical stages

The ADC products under research also include 7MW3711 (B7-H3-targeted ADC, in Phase I/II clinical trials) and 7MW4911 (CDH17-targeted ADC, in Phase I/II clinical trials), forming its differentiated competitive advantage in the ADC field.

At the same time, the pipeline reserve for monoclonal antibodies and TCE bispecific antibodies is abundant:

9MW1911 (ST2-targeting monoclonal antibody), a potential first-in-class macromolecular drug targeting the non-Th2 pathway for chronic obstructive pulmonary disease, has entered Phase Ib/IIa clinical trials in China and received IND approval for Phase IIa clinical trials in the United States; 9MW3811 (humanized IL-11-targeting monoclonal antibody), used for treating idiopathic pulmonary fibrosis and pathological scarring, has initiated Phase II clinical trials; 9MW3011 (TMPRSS6 monoclonal antibody) is indicated for various diseases related to iron homeostasis, with Mabwell holding commercialization rights in Greater China and Southeast Asia; 6MW5311, the world's first TCE (T-cell engager) bispecific antibody targeting LILRB4/CD3 to enter clinical trials, is used for treating hematologic tumors.

3Breaking the Ice A to H 18A

The uniqueness of the "A to H 18A" pathway lies in its dual attributes: It is not only a secondary listing from A-shares to H-shares but also an initial public offering conducted under the special rules for unprofitable biotech companies (Chapter 18A).

On the one hand, China's innovative pharmaceutical companies face common challenges at specific stages of development – the STAR Market listing provides precious early-stage development funding, supporting the critical transition from research and development to commercialization; when core products enter the global multicenter Phase III clinical stage, companies require more funding and resources under a global perspective, as a single market may encounter limitations in terms of refinancing efficiency and international capital base.

Based on the use of proceeds mentioned in the Hong Kong listing hearing materials (primarily allocated to global clinical trials of core ADC products), "commercialization of core products and global competition" will become the core strategy for Mabwell in its new phase. The "A+H" dual listing structure provides Mabwell with unique capital synergy advantages: the A-share market better understands the growth logic and development environment of local biotech companies, while the Hong Kong stock market helps establish regular communication mechanisms with international investors, focusing on new themes such as innovation value realization and global expansion.

Compared with the previous mainstay of Chapter 18A listings – pure R&D biotechs without marketed products – the "A-share veteran" Mabwell has multiple commercialized products and a significant revenue scale. In fact, this will attract more value investors who value the "R&D, manufacturing, and commercialization integration" capability, thereby enhancing the maturity and revenue quality of companies in the Chapter 18A sector.

On the other hand, from a macro perspective, Chinese innovative drug companies need a broader "dual capital circulation" model – seeking more flexible refinancing mechanisms, a more international investor base, while avoiding single-market risks. The question at hand is: given that the A-share valuation may already fully reflect the value of its existing product pipeline, how can a Hong Kong listing become a key step in telling the "global innovative drug story" and seeking a higher valuation ceiling?

At a time when out-licensing of innovative drug assets to global partners has become an inevitable path, Mabwell, as the first biotech to successfully navigate the "STAR Market Rule 5 + HKEX Chapter 18A" pathway, will open up a replicable financing and development channel for more already-listed companies that still need international capital to advance global clinical trials.