Chinese medical device companies' cross-border M&A over the past decade: some spend $5.9 billion on loss-making firms, others invest $100 million for 10x returns

LivaNova

Medical Device Supplier

ANGELAIGN

Dental Medical Consumables Supplier and Service Provider

In the past two years, cross-border mergers and acquisitions have rebounded, with an increasing number of medical device companies in China accelerating their globalization through cross-border M&A. However, influenced by factors such as policy environment, geopolitical issues, and industry development, the cross-border M&A trends of Chinese-funded medical device companies have varied, and the logic behind these acquisitions has also shifted.

Han Qi, Research Director of Morning Whistle Group, stated: "From 2015 to 2017, cross-border mergers and acquisitions (M&A) by Chinese medical device companies reached a peak, with both transaction value and volume hitting record highs. From 2018 to 2023, tightening regulatory policies both domestically and internationally, the rise of U.S. investment protectionism, and the onset of trade wars caused a significant decline in the transaction value and volume of cross-border M&A by Chinese medical device companies, almost reaching a freezing point. Starting in the second half of 2023, cross-border M&A by Chinese medical device companies began to rebound and maintained a warming trend through 2024-2025."

(2016-2026 Cross-Border M&A Projects by Chinese Medical Device Companies, Incomplete Statistics)

In addition to the changes in transaction amount and quantity, the motivation for Chinese medical device companies to engage in cross-border M&A has also shifted compared to a decade ago.

In the past, a major motivation for cross-border mergers and acquisitions was to introduce overseas technologies and products. MicroPort's acquisition of LivaNova's cardiac rhythm management business brings a comprehensive portfolio of cardiac rhythm management products, accelerating the localization of pacemaker technology in China; after institutions such as Wandong Medical and Yuwell Medical jointly acquired Italy's top medical device manufacturer Esaote, they will fill the gap in Wandong Medical's ultrasound product line and localize Esaote's technologies and products; one of the purposes of Weigao Group's acquisition of U.S.-based Argon is to introduce innovative technologies, upgrade products, and enrich its interventional product line...

Nowadays, the core motivation for Chinese medical device companies engaging in cross-border mergers and acquisitions has shifted to accelerating global expansion and promoting international business. Such as Angelalign Technology acquiring Aditek to enter the orthodontic market in Brazil and South America; Mindray acquiring DiaSys Diagnostic Systems GmbH to accelerate the internationalization of its In Vitro Diagnostics (IVD) business and build a global localized supply chain platform; OrbusNeich acquiring PT Revass Utama Medika, an Indonesian cardiovascular intervention distributor, to strengthen its global direct sales team; Tianyi Medical acquiring NIKKISO's global CRRT (Continuous Renal Replacement Therapy) business to quickly penetrate the global CRRT market; Shanghai MicroPort Endovascular MedTech acquiring European medical device company Optimum Medical for further comprehensive and in-depth coverage of the European market and expansion into markets such as the United States and Japan; Medcaptain Medical acquiring Belgian distributor Vedefar to enhance international sales capabilities...

As cross-border M&A rebounds, an increasing number of domestic medical device companies are beginning to focus on cross-border acquisitions. However, cross-border M&A is more complex than domestic M&A, involving not only different cultures, laws, and regulations, but also potential issues such as macro market changes and significant challenges in integration and synergy post-acquisition.

Fortunately, there are now enough cross-border M&A cases for domestic medical device companies to learn from, in order to reduce risks.

Looking back at the cross-border M&A cases of Chinese medical device companies over the past decade, some have achieved remarkable results, some have gone unnoticed, and some have become a core factor dragging down the performance of domestic medical device companies. What impact did the completion of these cross-border M&As have on various businesses of related companies in China? Let's analyze this in detail.

In 2016, Sinocare, based on its globalization strategy, acquired Trividia, the world's sixth-largest blood glucose monitoring company, and PTS, a U.S.-based POCT company. The aim was to improve its product structure, introduce advanced technologies through acquisitions, extend its sales network into overseas markets, and lay the foundation for the company to widely develop multinational operations.

From the annual reports of Sinocare over the years, it has achieved its goals in introducing products and technologies, but made little progress in expanding overseas markets.

This also reflects the difficulties in integrating and coordinating work. In 2017, Sinocare began exploring synergistic integration with PTS and Trividia in procurement, marketing, product development, and after-sales services. In 2019, Sinocare completed the coordination of procurement matters, achieving global allocation and sharing of procurement resources. In 2020, Sinocare worked with Trividia and PTS to promote the construction of a global after-sales service system. In 2022, Sinocare expanded its POCT testing business, including blood lipid and glycated hemoglobin tests, by leveraging the product lines of Trividia and PTS, achieving synergy in product combinations.

However, these synergistic integration efforts have not reached the ideal state. Trividia and PTS have often experienced performance losses and goodwill impairment, affecting Sinocare's profits. For example, in 2019, the business operations of PTS were impacted, resulting in goodwill impairment of 25 to 50 million RMB; Trividia's operating loss impacted Sinocare's investment income by approximately -60 to -75 million RMB. In 2020, both PTS and Trividia were in a state of operating loss. In 2021, Trividia continued to incur losses; in 2023, Trividia faced operating losses and goodwill impairment.

In 2023, Sinocare completed the controlling and consolidation of Trividia. As stated in its annual report: Completion of the controlling stake and consolidation of Trividia: reflecting on 8 years of synergy post-acquisition. Holding and consolidating is the foundation for promoting more effective synergy.

Perhaps due to the effectiveness of new collaborative integration strategies, in 2024, Sinocare achieved a revenue of 4.443 billion RMB, representing a year-on-year increase of 9.47%, with overseas income reaching 1.865 billion RMB, accounting for 41.98%. Among this, PTS maintained a profitable position, while Trividia realized dual growth in revenue and market share. Meanwhile, Sinocare utilized the automation production experience from PTS and Trividia to implement large-scale automated production at domestic factories. Additionally, Sinocare collaborated with Trividia to research and produce the first brand-new blood glucose meter under the True brand (which belongs to Trividia). This product was successfully launched through Trividia and entered the U.S. market.

Sinocare's integration and synergy with Trividia and PTS have reached a new stage.

In addition to integrated synergistic risks, macro market changes and policy shifts are also crucial factors affecting the outcomes of cross-border mergers and acquisitions. These factors are rare over the years but can have a significant impact on acquiring companies.

Taking Bluesail Medical as an example, in 2017, it acquired Biosensors International, the world's fourth-largest heart stent company, for approximately 5.895 billion RMB. The plan was to use the acquisition of Biosensors International as an opportunity to further extend into the high-value medical consumables field, achieve industrial upgrading, and form a strategic layout where high-value and low-value consumables businesses complement each other.

From the perspective of product portfolio, Bluesail Medical has indeed achieved industrial upgrading and completed a business layout that complements "high-value consumables + medium-to-low value consumables." However, after completing the acquisition, Bluesail Medical successively encountered various macro-environmental changes such as the trade war, the pandemic, and centralized procurement. These are all rare factors that can influence the entire market.

In 2018, the trade war began; in 2019, the COVID-19 pandemic emerged, affecting the number of coronary stent surgeries; in 2020, China organized its first centralized bulk procurement of high-value medical consumables (coronary stents), with the average price of coronary stents dropping significantly from 13,000 RMB to around 700 RMB, representing an average reduction of approximately 93%.

Affected by the above factors, Bluesail Medical's goodwill of 6.345 billion RMB arising from the acquisition of Biosensors International was continuously impaired from 2020 to 2024: approximately 1.76 billion RMB of goodwill impairment was recognized in 2020; another 1.698 billion RMB of goodwill impairment was recognized in 2021...

In response to sudden macro market changes, Bluesail Medical copes through diversified product layouts and globalized strategies. Specifically, when its cardiovascular business sales are restricted, its glove business accelerates development; when its stent products face centralized procurement in the Chinese market, the company intensifies promotion in Europe, the United States, and other regions.

In addition, Bluesail Medical has also increased its investment in the high-value consumables field through acquisitions, investments, and self-research. For example, in 2020, it acquired NVT, a well-known European valve intervention (TAVR) company, to enter the structural heart disease market; invested in artificial hearts to enter the heart failure field; invested in intravascular optical coherence tomography (OCT) to enter the vascular imaging field; and developed innovative products for neurointervention and peripheral intervention to enter the neurointervention and peripheral intervention fields. Through these strategic moves, Bluesail Medical continues to enhance its comprehensive influence in the high-value consumables sector.

Even though "fate seemed against it," Bluesail Medical managed to turn things around through perseverance and global strategic planning. In 2023, the price of coronary stents increased in the follow-up centralized procurement, significantly improving the operating performance of its cardiovascular division. This division achieved sales revenue of approximately 1 billion RMB, representing a year-on-year increase of about 30%, with gross profit margin in China growing by approximately 30%.

In contrast to Bluesail Medical, Fosun Pharma has been extremely "lucky." In 2017, Fosun Pharma acquired Breas, a leading European ventilator brand, for approximately RMB 621 million (medical device business). With the outbreak of the pandemic, the market demand for ventilators surged. Fosun Pharma promptly increased production capacity and allocated resources to ensure the global supply of ventilators. In 2020, Fosun Pharma produced over 18,000 ventilators for the frontlines of the global fight against the pandemic.

Driven by anti-epidemic products such as ventilators, Fosun Pharma's medical devices and medical diagnostics business achieved a revenue of 5.217 billion RMB in 2020, representing a year-on-year increase of 39.64%.

Thereafter, its ventilator business continued to grow driven by the global market. In 2023, Breas achieved solid growth in sales performance, with a restorative increase in demand for multifunctional non-invasive ventilators in markets such as Europe and the United States; In 2024, Breas's operating revenue, net profit, and operating cash flow steadily improved, with significant year-on-year growth in operating revenue in markets such as the United States and Canada; In 2025, the global sales volume of Breas ventilator products kept rising, with rapid growth in market penetration in the United States.

Overall, the changes in the macro environment are unpredictable and have a significant impact on the acquiring party, but these crises are industry-wide challenges faced by all enterprises. The acquiring party can overcome them and find new opportunities in the process.

In addition to the above-mentioned cases that reveal risks, there are also successful cases for reference.

For companies like Weigao Group and Angelalign Technology, cross-border mergers and acquisitions are an important way to accelerate their expansion overseas.

In 2017, Weigao Group acquired Argon Medical Devices, a U.S.-based manufacturer and distributor in the interventional oncology and vascular intervention fields, for approximately 5.45 billion RMB. This acquisition boosted the sales of Argon's products in the Chinese market and also facilitated the expansion of Weigao Group's products in overseas markets.

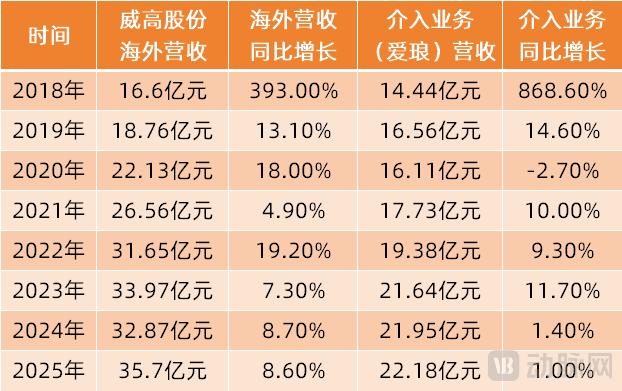

As an important step in global layout, Weigao Group has achieved gratifying results in acquiring Argon Medical Devices from the United States. Since Argon was incorporated into Weigao Group's interventional business in 2018, its interventional business and overseas revenue have maintained a relatively good growth trend despite facing multiple factors that impacted performance, such as centralized procurement and the pandemic. The revenue of its interventional business increased from 1.444 billion RMB in 2018 to 2.218 billion RMB in 2025. Weigao Group's overseas revenue also grew from 1.66 billion RMB in 2018 to 3.57 billion RMB in 2025.

(Weigao's Overseas Revenue and Intervention Business Performance After Acquiring Argon Medical Devices in the US)

Weigao Group stated: "The overseas sales of the interventional segment have laid a solid foundation for the group's overseas market layout." In 2023, Weigao Group integrated the overseas advantages of various business segments such as interventional, and established a unified overseas platform. Through this platform, Weigao Group's international strategy achieved significant breakthroughs in 2024-2025.

Compared with Weigao Group, Angelalign Technology's overseas revenue growth was more significant after acquiring Aditek, a leading orthodontic product manufacturer in Brazil, for approximately 140 million RMB in 2022.

After the acquisition, Angelalign Technology entered the Brazilian market through Aditek and established local business teams in Europe, Australia/New Zealand, and North America, officially stepping into the phase of "global organization + localized operations." Its overseas revenue increased from US$20.6 million in 2023 to US$80.5 million in 2024, and reached US$163 million in 2025, with year-over-year growth rates of 290.4% and 102.5%, respectively.

In terms of the number of cases completed with invisible orthodontic treatments, Angelalign Technology achieved 140,700 cases in overseas markets in 2024, representing a year-on-year increase of 326.4%; and reached 256,000 cases in 2025, marking an 82.1% year-on-year growth. In terms of revenue from invisible orthodontic treatments, the growth rate of overseas revenue (108.6%) is 10 times that of the domestic market (10.4%).

Currently, overseas business has become the core growth engine of Angelalign Technology's performance.

In addition, unlike the introduction of overseas products, Angelalign Technology exports Chinese solutions overseas. It helps the acquired company Aditek build a digital factory and enhance its intelligent manufacturing capabilities; it also provides Aditek with digital solutions to improve its service capabilities.

For some cross-border M&A cases, the core purpose is to introduce innovative products from overseas. Therefore, the increase in overseas revenue is limited, and the main impact is on the Chinese market.

Taking the acquisition of LivaNova's cardiac rhythm management business as an example, in 2017, MicroPort Medical acquired LivaNova's cardiac rhythm management business to accelerate the sales of cardiac rhythm management products in the Chinese market; the acquisition also helped expand the company's operational scale in Europe.

After the business was consolidated in 2018, MicroPort Cardiac Rhythm Management achieved an income of 158 million US dollars. MicroPort stated: From now on, the globalization strategy of the cardiac rhythm management business will be further implemented.

Although it hoped to use LivaNova's international marketing channels to expand overseas revenue when acquiring LivaNova's cardiac rhythm management business, MicroPort's cardiac rhythm management business has not shown rapid growth in the international market. Instead, domestic revenue has significantly increased under the support of the localization of cardiac rhythm management products in China.

2019 was the first full fiscal year after MicroPort's acquisition of its Cardiac Rhythm Management (CRM) business. The CRM business generated revenue of $209 million, representing a 32% year-on-year increase. Of this, international market revenue reached $201 million, while revenue from the Chinese market amounted to $8 million, showing significant growth.

(Revenue Situation of MicroPort Medical's Cardiac Rhythm Management Business in China and Globally from 2019-2025)

From 2019 to 2025, the revenue of MicroPort's cardiac rhythm management business in the international market remained relatively stable, fluctuating between 172 million and 207 million US dollars. However, its revenue in the Chinese market grew approximately threefold, increasing from 8 million US dollars to 22.7 million US dollars. The year-on-year growth rates for 2019, 2021, and 2024 reached 42.5%, 53.7%, and 51.3%, respectively. In 2025, the revenue of the cardiac rhythm management business in China declined by 6.1% year-on-year due to the slower-than-expected implementation of centralized procurement.

A similar case is the cross-border acquisition of Esaote. In 2017, Wandong Medical and Yuwell Medical, together with other domestic investors, acquired Esaote, a top Italian medical imaging company. Wandong Medical stated at the time: It is expected that the two parties will actively carry out domestic and international business collaboration in the future, promoting the rapid development of the company's business.

Before the acquisition, Wandong Medical's main products included DR, MRI, and high-end X-ray machines, lacking an ultrasound equipment product line. This acquisition enabled it to fill the gap in its ultrasound product line. The platform for promoting the localization and domestic production of Esaote's ultrasound products is Wandong Esaote (Suzhou) Medical Technology Co., Ltd., which was established by Wandong Medical.

Although rapid progress has been made in perfecting the product portfolio, the international business synergy that Wandong Medical anticipated has not materialized, with its overseas revenue remaining at a relatively low proportion. For instance, five years after the acquisition was completed, in 2022, domestic sales accounted for 89% of Wandong Medical's revenue, while overseas revenue only made up 11%.

Until 2023, when Wandong Medical accelerated its global layout, its overseas revenue began to grow rapidly. In 2024, Wandong Medical's overseas revenue reached 233 million RMB, a year-on-year increase of 68.36%, accounting for 16.32% of total revenue. In 2025, its overseas revenue amounted to 360 million RMB, a year-on-year increase of 54.38%, representing 29.61% of total revenue.

In addition, the main impact of the acquisition of Sirtex, an Australian liver cancer treatment device company, on the acquiring companies is also in the Chinese market. In 2019, Grand Pharmaceutical Group, in collaboration with CDH Investments, acquired Sirtex for approximately 9.5 billion RMB to introduce Sirtex's core product, SIR-Spheres Y-90 resin microspheres. This product is a targeted radiation therapy technology for liver cancer, capable of selectively and efficiently killing tumor cells while causing minimal damage to normal liver tissue.

In fact, the core purpose of Grand Pharmaceutical's acquisition this time is to introduce innovative products. In 2022, its SIR-Spheres Y-90 resin microspheres achieved a global cumulative treatment of 100,000 doses, and the product was approved for marketing in China in January 2022.

After the product was launched, its growth rate did not disappoint Grand Pharmaceutical. Between 2022 and 2025, Y90 microsphere injection (SIR-Spheres) is expected to achieve approximately 15 times revenue growth over four years.

Since its launch, the product has been included in more than 50 Huiminbao (city-specific customized commercial medical insurance) plans — including Beijing Universal Health Insurance, Shanghai Hu Hui Bao, Wuhan Fu Han Kang, and Chongqing Yu Kuai Bao — as well as 3 special drug insurance plans, covering over 24 provincial-level administrative regions and more than 100 cities.

Overall, during the decade from 2016 to 2026, Chinese medical device companies have introduced overseas innovative technologies and products through cross-border mergers and acquisitions, accelerated industrial upgrading, promoted global layout, and reaped abundant rewards. However, Chinese medical device companies have also suffered and gained experience in cross-border mergers and acquisitions.

From the M&A boom in 2016 to the trough after 2018, and then to the market recovery in the past two years, Chinese medical device companies have once again begun to view cross-border M&A as an important means of business growth. At the same time, instead of simply considering "buying technology and addressing weaknesses," these companies are now planning to achieve high-quality international expansion through global resource integration, the export of Chinese solutions, and the coordination of domestic and international technologies.

It should be noted that cross-border M&A does not end with spending money. The acquirer also needs to consider synergistic integration, leverage the strengths of both parties, and achieve a "1+1>2" effect.

Standing at the starting point of a new round of cross-border M&A surge, the market is influenced by regulatory, geopolitical, and macroeconomic factors. However, Chinese medical device companies have accumulated extensive experience in dealing with these challenges. In the future, Chinese medical device companies will implement cross-border M&A with greater precision and methods, promoting the Chinese medical device industry to occupy a more significant position in the global medical market.