The $30B radiopharma blue ocean opens: AstraZeneca and Regeneron bet big as China grants first approval

AstraZeneca

Pharmaceutical Technology Research and Development Provider

Telix Pharmaceuticals

Radiopharmaceutical Developer

Since the beginning of 2026, the radiopharmaceutical sector has continued to gain momentum.

On March 19, 2026, AstraZeneca executives signed an agreement at a ceremony in the Guangzhou Development District. The deal marked the global pharmaceutical giant's commitment to establishing a production and supply base in Huangpu District, China, focused on actinium-225 radiopharmaceuticals. Less than a month later, on April 13, Regeneron and Australia-based Telix Pharmaceuticals announced a global strategic collaboration — an upfront payment of $40 million to secure four radiopharmaceutical development programs, with costs and profits shared equally on a 50/50 basis.

Within less than a month, these two major moves signal a clear message: the opportunity window for the radiopharmaceutical sector has fully opened.

Industry data show that the global radiopharmaceutical market was valued at approximately $10 billion in 2023 and is expected to grow to $30 billion by 2030, a threefold increase in just seven years. With sustained momentum, the radiopharmaceutical sector is rapidly emerging as a new battleground where multinational pharmaceutical companies and Chinese innovative drug developers are making strategic moves.

Since early 2026, major multinational corporations (MNCs) have been announcing a dizzying series of high-profile events in the radiopharmaceutical space, with two major deals occurring in just the past month.

Regeneron has joined forces with Telix, formally launching a deep, collaborative operating model in the radiopharmaceutical field. On April 13, the two companies announced a global strategic collaboration that goes beyond traditional licensing deals. Instead, they have adopted a strongly aligned mechanism of shared costs and shared profits to fully engage in the development and commercialization of next-generation targeted radiopharmaceuticals.

Under the agreement, Regeneron will pay an upfront payment of $40 million to initially launch four development programs, with an option to add four more — effectively doubling the scope of the collaboration as programs advance. If all programs progress successfully and achieve milestone payments, the total deal value could exceed $2.1 billion. The two parties have adopted a 50/50 cost and profit-sharing model, sharing global responsibilities for development, manufacturing, and commercialization — breaking away from the traditional "one party licenses, one party pays" licensing deal model to form a true community of interests. The agreement also includes flexible opt-out mechanisms: should Telix opt-out of co-funding a particular program, it would still be eligible to receive up to $535 million in development and commercial milestone payments, plus low double-digit royalties on net sales, balancing flexibility with collaboration security.

The core strength of this deal lies in the highly complementary, mutually reinforcing strategic value of the partnership. For Regeneron — a global antibody powerhouse known for its VelocImmune® fully human antibody platform and blockbuster products such as Libtayo — the radiopharmaceutical space was previously a blank spot. Through this collaboration with Telix, Regeneron gains rapid access to the entire radiopharmaceutical value chain with low upfront risk and an asset-light entry model. It can seamlessly link its proprietary antibody targets with Telix's established radiopharmaceutical conjugation expertise, global manufacturing and supply chain infrastructure, and theranostics platform, accelerating its transformation from an "antibody leader" into a "multimodal oncology therapy platform," while opening up significant potential for combining radiopharmaceuticals with immunotherapies.

For Telix, Regeneron's world-class antibody discovery capabilities and global clinical and commercial resources are key pieces to complement its shortcomings and elevate it to a platform-level company. Leveraging high-quality antibodies generated from the VelocImmune® platform, Telix can push beyond the current boundaries of radiopharmaceutical R&D and tackle the cutting-edge field of biologic-based radiopharmaceuticals. Combined with Regeneron's clinical development expertise and channel resources, this significantly improves project execution efficiency and the probability of global commercial success.

This deal structure sends a strong signal: in a radiopharmaceutical space characterized by high R&D barriers, stringent supply chain requirements, and complex global operations, MNCs have fully moved away from "going it alone" toward collaborative operations based on complementary technologies, shared risk, and shared profit. Only deep collaborations that integrate the entire chain — targets, radionuclides, delivery, manufacturing, and commercialization — can secure true leadership in the radiopharmaceutical sector.

On March 19, AstraZeneca formally signed a collaboration agreement with the Guangzhou Economic and Technological Development District Management Committee, announcing the construction of an RDC manufacturing and supply base in Guangzhou Development District and Huangpu District. The base will focus on producing actinium-225-based radiopharmaceuticals primarily for the precision treatment of prostate cancer and other malignancies.

The choice of actinium-225 is no coincidence. Actinium-225 emits alpha particles with high energy and short range (just a few cell diameters), offering potent tumor cell killing with minimal damage to healthy tissue, making it a "golden radionuclide" for next-generation radiopharmaceuticals. However, global supply of actinium-225 is extremely scarce. According to Yuan Dawei, founder of Quarkmed, the annual supply of actinium-225 can only support approximately several thousand to ten thousand treatments — the single greatest limitation to the development of actinium-225-based radiopharmaceuticals. By building manufacturing facilities directly in China, AstraZeneca demonstrates its strategic intent to rapidly bring innovative therapies to patients in China and the broader Asia-Pacific region.

Multinational pharmaceutical companies are now capturing high ground in the radiopharmaceutical space through a dual strategy of deep collaboration plus capacity pre-positioning — securing both cutting-edge technologies and project pipelines while also establishing localized production of scarce radionuclides ahead of time. The global radiopharmaceutical competition has formally entered a stage of value-chain positioning battles.

As multinational giants accelerate their push into the space, Chinese radiopharmaceutical companies are advancing in parallel across the entire chain — from intensified financing and clinical breakthroughs to new drug application acceptances and approved innovative products. Collectively, they are making strides in capital, technology, product development, and commercialization, with homegrown innovative forces rising rapidly.

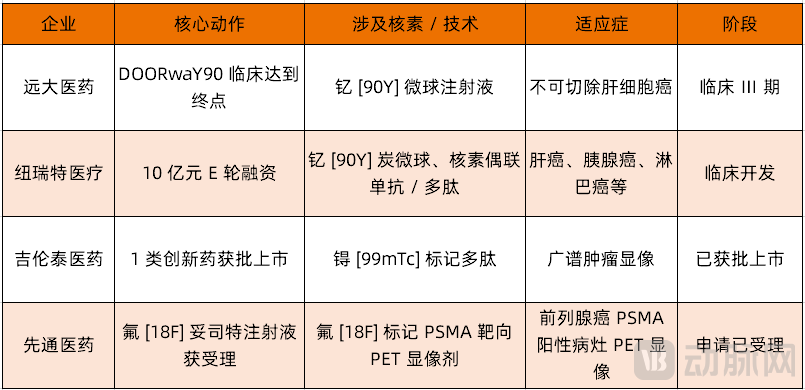

Since April, a flurry of positive developments has hit China's domestic radiopharmaceutical sector. Sinotau reached a milestone on April 15, when the new drug application for flotufolastat F-18 injection (XTR020 / POSLUMA®), a radiopharmaceutical for the precise diagnosis of prostate cancer, was accepted by the NMPA. This marks the first 18F-labeled PSMA-targeted diagnostic radiopharmaceutical to be submitted for approval in China. Based on pivotal Phase III clinical data in China, the drug demonstrated excellent diagnostic performance and safety in patients with biochemical recurrence of prostate cancer, and is expected to fill a gap in 18F-PSMA radiopharmaceutical diagnosis in China.

Key progress has also been made in clinical globalization. On April 13, Grand Pharmaceutical announced that its core product, Yttrium [90Y] microsphere injection (SIR-Spheres®), successfully met the prespecified primary endpoint in the U.S. DOORwaY90 clinical study for unresectable hepatocellular carcinoma. As a distinctive radiopharmaceutical combining internal radiation and interventional therapy, this clinical breakthrough not only validates its global competitiveness but will also accelerate its global commercial expansion.

On the capital front, domestic leaders continue to build momentum. On April 3, New Radiomedicine Technology completed a 1 billion RMB Series E financing round, with proceeds primarily directed toward clinical development of radiopharmaceuticals, medical isotope production, and market system build-out. As a platform company driven by both "isotope supply + drug development," New Radiomedicine has built a pipeline spanning Yttrium [90Y] carbon microspheres, radionuclide-drug conjugates, and other programs covering high-incidence cancers such as liver cancer, pancreatic cancer, and lymphoma, continuously strengthening its industrial chain moat.

Homegrown innovation also achieved a historic breakthrough. On April 2, Radio Medicinal's 99mTc-3PRGD2 was officially approved by the NMPA, becoming a landmark product among China's domestic Category 1 innovative radionuclide drug conjugates. This broad-spectrum tumor SPECT imaging agent can precisely identify tumors and neovasculature, clearly localizing lesions and metastases — marking the official transition of China's radiopharmaceutical sector from a "follow-on" and generic-driven era into a new phase of original innovation.

Comparison of Major Participants in the Nuclear Medicine Track (Source: VCBeat)

From capital injection to clinical globalization, from acceptance of a diagnostic radiopharmaceutical NDA to breakthroughs in therapeutic agents, and ultimately to the successful approval of a Category 1 innovative radionuclide drug conjugate, China's radiopharmaceutical industry has formed a complete closed loop encompassing R&D, clinical development, industrialization, and commercialization. This marks the official entry of China's radiopharmaceutical industry into a new phase characterized by accelerated innovation, self-sufficiency, and global advancement.

The commercial value of radiopharmaceuticals is determined by three interconnected links: upstream supply, midstream R&D, and downstream commercialization. Whether the industry can sustainably realize the projected $30 billion market opportunity, however, depends on three external constraints — production capacity, regulation, and reimbursement — which together form the complete competitive framework for the sector.

1) Three Layers of Value Chain Barriers: Who Can Control the Commercial Lifeline of Radiopharmaceuticals?

Upstream radionuclide supply is the "choke point" of the radiopharmaceutical sector. Medical isotopes such as yttrium-90, technetium-99m, and actinium-225 depend on nuclear reactors or accelerators for production. Global high-abundance medical isotope production capacity has long been concentrated among a few suppliers. A stable upstream radionuclide supply is a core competitive strength in the sector.

Midstream drug development relies on the overall coordination of targets, radionuclides, and delivery systems. Radiopharmaceutical R&D differs from traditional small molecules and biologics in that it requires simultaneous alignment of tumor targets, radionuclides, and delivery vehicles. These three technical demands raise the R&D bar while also creating differentiation advantages for companies with integrated capabilities.

Downstream commercialization presents a unique "last-mile" challenge specific to radiopharmaceuticals. Radionuclides have short half-lives — approximately 64 hours for yttrium-90 and only 6 hours for technetium-99m — requiring products to complete the entire process of manufacturing, quality control, transport, and administration within a narrow time window. Commercialization demands not only a sales force but also infrastructure such as cold-chain logistics and hospital nuclear medicine departments. This is the core reason why AstraZeneca chose to build a manufacturing facility in China — being close to the market means being close to patients.

2) Three Key Growth Variables Determine the Industry's Growth Ceiling

The rapid rise of the radiopharmaceutical sector is no accident. On the technology front, radiopharmaceuticals (RDCs) replicate the successful logic of ADCs by combining precise targeting with potent killing. Novartis's Pluvicto (lutetium-177 PSMA) breakthrough in prostate cancer treatment has already validated the commercial feasibility of this technological approach. However, whether the industry can continue to expand is still constrained by production capacity, regulation, and reimbursement.

Global medical isotope production capacity remains limited overall. The production technology for alpha emitters such as actinium-225 is extremely demanding. If upstream supply capability fails to keep pace with downstream innovation and clinical demand, it will directly constrain the pace of market expansion. Meanwhile, radiopharmaceuticals are subject to dual oversight from drug regulatory authorities as well as environmental and radiation safety agencies. The speed at which China's relevant regulatory system matures will significantly affect the efficiency of innovation in the sector. Furthermore, the scope of reimbursement coverage and the level of payment support in the Chinese market will determine whether these innovative therapies can reach the broader patient population.

The opportunity window for the radiopharmaceutical sector has opened. From Regeneron's deep strategic collaboration with Telix, to AstraZeneca's RDC manufacturing facility investment in China; from Grand Pharmaceutical's clinical breakthrough, to New Radiomedicine Technology's intensified financing round, and ultimately to Radio Medicinal's approval for market entry — the series of events since early 2026 is drawing a clear roadmap for radiopharmaceutical industrialization.

For Chinese pharmaceutical companies, those that can build synergistic advantages across three dimensions will be well-positioned to secure a place in this blue-ocean market: first, self-sufficiency in upstream radionuclide supply; second, precise and differentiated positioning of targets and radionuclides; and third, the construction of a closed industrial chain spanning R&D, manufacturing, and commercialization.

As global pharmaceutical companies collectively double down on the radiopharmaceutical space, a more critical question emerges: to what extent can Chinese companies transition from "followers" to "leaders" in this full-chain competition — from radionuclides to drugs? The answer may lie in the clinical data and capacity build-out over the next two to three years.